Mad Hedge Technology Letter

March 15, 2023

Fiat Lux

Featured Trade:

(THE UNKNOWN IN THE DIGITAL AD SPACE)

(NFLX), (WBD), (DIS), (CMCSA), (ROKU)

Mad Hedge Technology Letter

March 15, 2023

Fiat Lux

Featured Trade:

(THE UNKNOWN IN THE DIGITAL AD SPACE)

(NFLX), (WBD), (DIS), (CMCSA), (ROKU)

The uncertain digital advertising environment has been a thorn in the side of legacy media giants for quite some time.

Companies from Comcast (CMCSA) to Warner Bros. Discovery (WBD) are feeling the pressure as profitability struggles pile up.

Unfavorable macroeconomic headwinds coupled with decreased ad budgets amid a decline in linear TV and digital search trends put the ad market through the wringer in 2022.

Recent ad market softness comes as media giants like Disney (DIS) and Netflix (NFLX) have embraced ad-supported streaming alternatives as the race for eyeballs escalate.

Disney's direct-to-consumer division lost an eye-popping $4 billion-plus in 2022.

Warner Bros Discovery is now targeting $4 billion in cost savings over the next two years.

Advertising revenue within NBCUniversal's media division increased by 4% in Q4 because of a boost from the incremental revenue from the FIFA World Cup.

Looking ahead, the lack of brand name events in 2023 such as the World Cup, Olympics, or U.S. midterm elections, will likely be a drag on ad spend in 2023.

Those events greatly aided the battered industry with the domestic ad market totaling $318 billion last year — an increase of 8% compared to 2021.

Similarly, Spotify (SPOT) CFO Paul Vogel told investors during the latest earnings call: "Advertising in Q4, overall, it's definitely continued to be very up and down."

Spotify's Q4 ad-supported revenue, boosted by podcasting, grew 14% on a year-over-year basis to €449 million — accounting for 14% of total revenue.

Disney and Netflix rolled out their ad tier products at a time when the ad market is in flux, but the move seems to have been a lucrative one.

At the time of the debut, the company said over 100 advertisers bought inventory for the launch — bucking the trend of a global ad spend slowdown.

Similar to Disney, Netflix is playing the long game when it comes to its recently launched ad-supported tier, which officially debuted in November.

In its latest shareholder letter, Netflix said engagement for ad-supported subscribers "is consistent with members on comparable ad-free plans, is better than what we had expected, and we believe the lower price point is driving incremental membership growth."

Investors should run to higher grounds to avoid the upcoming slaughter in legacy media.

The cord cutter phenomenon is real and the pivot to work-from-home culture has really stuck the fork in many traditional services that used to be part of American culture.

Legacy media is one of the big losers – nobody watches analog television anymore.

Investors will need to seek attractive properties such as NFLX to buy the dip.

They benefit from the first mover advantage, but Disney is also finding their way after firing former CEO Bob Chapek and replacing him with the guy before him - Bob Iger. It’s not a pure streaming play which is also an issue for the likes of Amazon and I do think Roku is a little too growth based at this point in the business cycle.

The overall message is to avoid unproven tech assets for the time being with bank turmoil and interest rate tumult.

The only exceptions are active traders who use volatility in their favor and play from the long and short side. Traders usually don’t discriminate and can jump in and out of these sharp movements.

If traders want to get into streaming or social media stocks, that is fine, but stick with the brand names and shun the exotic names for now.

Call this the Dr. Jekyll and Mr. Hyde market.

On the up days, we see the kindly ministrations of Dr. Jekyll.

On the down days, we suffer from the evil hand of Mr. Hyde.

To say that traders are confused would be an understatement. Many seasoned pros have told me that this is one of the most difficult markets they have ever seen.

Fridays have been particularly treacherous when weekly options expire. Some 56% of all options trading now takes place with expirations of five days or less. Trading before 4:00 PM sees billions of dollars of hot money trying to force closing prices just in or out of the money for key at-the-money strike prices.

What is especially disturbing is that some 80% of the gain in the S&P 500 (SPY) this year has been in just seven names, Meta, (META), Alphabet (GOOGL), Microsoft (MSFT), Apple (AAPL), Amazon (AMZN), Netflix (NFLX) and Tesla (TSLA). Most other stocks went nowhere….or down. That much concentration means that any rallies lack confidence and will fail….for now.

Remember these names because when we finally do get a real upside breakout, they will be the leaders. You can take that to the bank.

Thanks to turmoil in the House of Representatives intent on a national default, bonds have given up 70 of the 120-basis point drop in yields since October. That deprives us of one of our biggest money makers of 2022, our long bond trades.

That means were are also seeing the automatic flip side of the bond trade, a strong US Dollar (UUP), and weak precious metals, (GLD) and (SLV), and emerging markets (EEM).

This too shall end.

If it was excess liquidity that caused stocks to rocket for 13 years, then maybe we should be focusing on what little liquidity is left. That would be the font of government money pouring into infrastructure and alternative energy plays.

Some $370 billion I know available for investment in ESG, would most of it going into the battery industry for the burgeoning electric vehicle industry. Even foreign firms like Finland’s Neste is moving to the US to cash in on federal munificence, converting an old US oil refinery to produce diesel fuel out of animal and vegetable fat (click here for the link).

Probably the best bet here is in California-based Enphase Energy (ENPH), which makes a 40% gross profit margins on microinverters for solar panels and has just seen a 42% dive in its share price. That makes (ENPH) a BUY. Hint: solar stocks always follow the price of oil to which it is tied, which has lately been down.

Some nimble and aggressive trading managed to push me back in the green for February, taking me up +0.93% on the month. That’s a dramatic improvement of +5.48% from a week ago.

You might even call it making a silk purse from a sow’s ear.

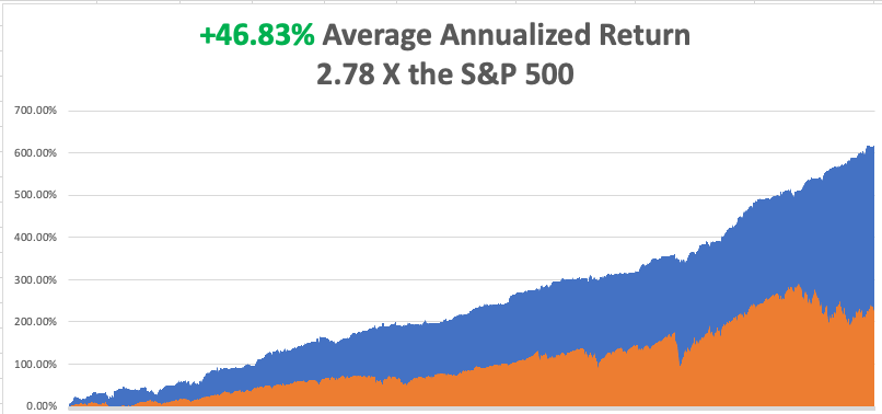

My 2023 year-to-date performance is still at the top at +23.28%. The S&P 500 (SPY) is up +4.32% so far in 2023. My trailing one-year return maintains a sky-high +86.58% versus -12.97% for the S&P 500.

That brings my 15-year total return to +620.47%, some 2.78 times the S&P 500 (SPX) over the same period. My average annualized return has recovered to +46.83%, still the highest in the industry.

Last week, I piled on a Tesla (TSLA) March $155-$260 short strangle betting that the stock can stay within a $95 range for 19 trading days. I also added a deep in-the-money long in the bond market for the first time in six weeks. Both positions turned immediately profitable.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

Q4 GDP Dips, from 3.9% to 2.7% in the October-December quarter. Consumption took a dive, which is amazing over the holidays. This is nowhere near a recession.

Fed Minutes Show More Hikes to Come, with the emphasis on the plural. That could take the overnight borrowing rate to a 5.40% high. It certainly pees on the parade for the falling interest rates crowd.

The Tail is Wagging the Dog, with short, dated options, often same-day expiration dominating trading every Friday. Billions of dollars are battling around key strike prices attempting to force expirations in or out of the money. No place for the little guy. Better to take Fridays off.

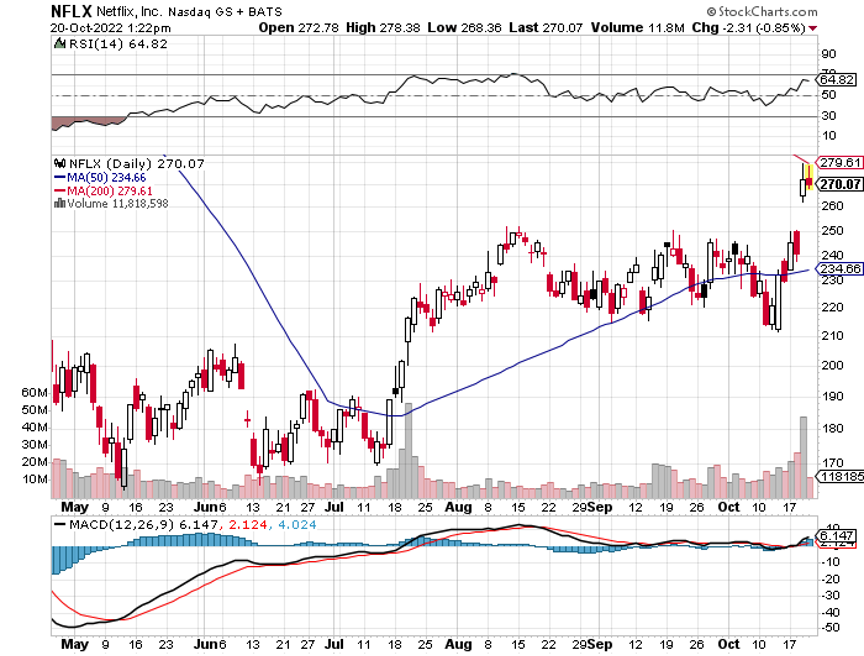

Netflix Slashes Prices in 30 countries, taking the stock down a modest 3%. (NFLX) is still the leader in the sector with 231 million subscribers, followed by Amazon (200 million), Disney Plus (162 million, HBO Max (95 million, Peacock (18 million), and Hulu 47 million). Buy (NFLX) and (AMZN) on dips.

Individual 401k’s Lost 23% in 2022, according to a study from Fidelity. High inflation is shrinking the remaining purchasing power even faster. A rising number of workers are also borrowing against their 401k’s to make ends meet. Such loans can go up to 50% of the principal. Better start making up the losses or you’ll be spending your golden years working at Taco Bell.

Apple to Add Glucose Monitor on its Watches, to aid diabetic clients. Some 38 million Americans have diabetes and given the obesity epidemic that figure is certain to rise. It highlights Big Tech’s move into the low-hanging fruit in health care.

Existing Home Sales Dive 0.7% in January, to a 4 million annualized rate, the weakest since October 2010. That makes 12 consecutive months of falling sales. The Median Home Price sold rose to $359,000. An imminent national debt crisis and spiking interest rates is not a great environment in which to sell your home.

Biden Ukraine Visit Tanks Gas and Oil Prices, cutting Russia’s chances of a win and eventually leading to a flood of oil on the market. Biden’s visit is sending the message to Putin that there’s no chance of a win here. Energy is hitting two-year lows across the board. Only energy stocks are staying high. Energy is getting so cheap it might be worth a trade.

Germany Accelerates Move Towards Alternatives, permanently cutting all ties with Russia energy. Europe’s biggest economy, and the fourth largest in the world, hopes to get 80% of its electricity from solar and wind by 2030. Hydrogen is also entering the picture. Other countries will follow.

On Monday, February 27 at 8:30 AM EST, US Durable Goods are out.

On Tuesday, February 28 at 9:00 AM, the S&P Case Shiller National Home Price Index for December is released.

On Wednesday, March 1 at 10:00 AM, the ISM Manufacturing PMI is printed.

On Thursday, March 2 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, March 3 at 8:30 AM, the ISM Non-Manufacturing PMI. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I usually get a request to fund some charity about once a day. I ignore them because they usually enrich the fundraisers more than the potential beneficiaries. But one request seemed to hit all my soft spots at once.

Would I be interested in financing the refit of the USS Potomac (AG-25), Franklin Delano Roosevelt’s presidential yacht?

I had just sold my oil and gas business for an outrageous profit and had some free time on my hands so I said, “Hell Yes,” but only if I get to drive. The trick was to raise the necessary $5 million without it costing me any money.

To say that the Potomac had fallen on hard times was an understatement.

When Roosevelt entered the White House in 1932, he inherited the presidential yacht of Herbert Hoover, the USS Sequoia. But the Sequoia was entirely made of wood, which Roosevelt had a lifelong fear of. When he was a young child, he nearly perished when a wooden ship caught fire and sank, he was passed to a lifeboat by a devoted nanny.

Roosevelt settled on the 165-foot USS Electra, launched from the Manitowoc Shipyard in Wisconsin, whose lines he greatly admired. The government had ordered 34 of these cutters to fight rum runners across the Great Lakes during Prohibition. Deliveries began just as the ban on alcohol ended.

Some $60,000 was poured into the ship to bring it up to presidential standards and it was made wheelchair accessible with an elevator, which FDR operated himself with ropes. The ship became the “floating White House,” and numerous political deals were hammered out on its decks. Some noted guests included King George VI of England, Queen Elisabeth, and Winston Churchill.

During WWII Roosevelt hosted his weekly “fireside chats” on the ship’s short-wave radio. The concern was that the Germans would attempt to block transmissions if broadcast came from the White House.

After Roosevelt’s death, the Potamac was decommissioned and sold off by Harry Truman, who favored the much more substantial 243-foot USS Williamsburg. The Potamac became a Dept of Fisheries enforcement boat until 1960 and then was used as a ferry to Puerto Rico until 1962.

An attempt was made to sail it through the Panama Canal to the 1962 World’s Fair in Seattle, but it broke down on the way in Long Beach, CA. In 1964 Elvis Presley bought the Potomac so it could be auctioned off to raise money for St. Jude Children’s Research Hospital. It sold for $65,000. It then disappeared from maritime registration in 1970. At one point there was an attempt to turn it into a floating disco.

In 1980 a US Coast Guard cutter spotted a suspicious radar return 20 miles off the coast of San Francisco. It turned out to be the Potomac loaded to the gunnels with bales of illicit marijuana from Mexico. The Coast Guard seized the ship and towed it to the Treasure Island naval base under the Bay Bridge. By now the 50-year-old ship was leaking badly. The marijuana bales soaked up the seawater and the ship became so heavy it sank at its moorings.

Then a long rescue effort began. Not wanting to get blamed for the sinking of a presidential yacht on its watch the Navy raised the Potomac at its own expense, about $10 million, putting its heavy lift crane to use. It was then sold to the City of Oakland, Ca for a paltry $15,000.

The troubled ship was placed on a barge and floated upriver to Stockton, CA, which had a large but underutilized unionized maritime repair business. The government subsidies started raining down from the skies and a down-to-the-rivets restoration began. Two rebuilt WWII tugboat engines replaced the old, exhausted ones. A nationwide search was launched to recover artifacts from FDR’s time on the ship. The Potomac returned to the seas in 1993.

I came on the scene in 2007 when the ship was due for a second refit. The foundation that now owned the ship needed $5 million. So, I did a deal with National Public Radio for free advertising in exchange for a few hundred dinner cruise tickets. NPR then held a contest to auction off tickets and kept the cash (what was the name of FDR’s dog? Fala!).

I also negotiated landing rights at the Pier One San Francisco Ferry Terminal, which involved negotiating with a half dozen unions, unheard of in San Francisco maritime circles. Every cruise sold out over two years, selling 2,500 tickets. To keep everyone well-lubricated I became the largest Bay Area buyer of wine for those years. I still have a free T-shirt from every winery in Napa Valley.

It turned out to be the most successful fundraiser in the history of NPR and the Potomac. We easily got the $5 million and then some. The ship received a new coat of white paint, new rigging, modern navigation gear, and more period artifacts. I obtained my captain’s license and learned how to command a former coast guard cutter.

It was a win-win-win.

I was trained by a retired US Navy nuclear submarine commander, who was a real expert at navigating a now thin-hulled 73-year-old ship in San Francisco’s crowded bay waters. We were only licensed to cruise up to the Golden Gate bridge and not beyond, as the ship was so old.

The inaugural cruise was the social event of the year in San Francisco with everyone wearing period Depression-era dress. It was attended by FDR’s grandson, James Roosevelt III, a Bay area attorney who was a dead ringer for his grandfather. I mercilessly grilled him for unpublished historical anecdotes. A handful of still-living Roosevelt cabinet members also came, as well as many WWII veterans.

As we approached the Golden Gate Bridge, some poor soul jumped off and the Coast Guard asked us to perform search and rescue until they could get a ship on station. No body was ever found. It certainly made for an eventful first cruise.

Of the original 34 cutters constructed only four remain. The other three make up the Circle Line tour boats that sail around Manhattan several times a day.

Last summer I boarded the Potomac for the first time in 14 years for a pleasant afternoon cruise with some guests from Australia. Some of the older crew recognized me and saluted. In the cabin, I noticed a brass urn oddly out of place. It contained the ashes of the sub-commander who had trained me all those years ago.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Captain Thomas at the Helm

Mad Hedge Technology Letter

February 3, 2023

Fiat Lux

Featured Trade:

(HIGH BETA IS SUDDENLY HOT)

(DOCU), (META), (LYFT), (AMZN), (NFLX)

The Federal Reserve swung its big stick again.

They are and will continue to be the largest influencer in tech share price action in the short-term and the last 2 days has proved it.

Whatever you think or say about the equity market, we can’t hide from the truth that liquidity will either wreak havoc on short-term price action or shoot it to the moon like we saw post-Fed announcement about the latest rate hike.

Tech shares lifted off like an Elon Musk spaceship to Mars and the Mad Hedge Technology Letter was tactical enough to take profits on a DocuSign (DOCU) put spread and stomp out in Meta (META) before the earnings report.

I was able to add some additional long tech as Friday is proving to benefit from the spillover effect.

No matter how we view it, volatility isn’t going anywhere any time soon.

Why?

Since January 2020, the US has printed nearly 80% of all US dollars in existence.

Lots of fiat paper sloshing around in the system has many unintended consequences.

When pushed into certain asset classes, the hot money polarizes price action. That’s how we got all the meme stock craziness.

This phenomenon won’t be going away anytime soon and the Fed slowly reducing their asset sheet pales in comparison to the liquidity hanging around on the sidelines.

The Fed hike means short-term rates now stand at between 4.5%-4.75%, the highest since October 2007.

The move marked the eighth increase in a process that began in March 2022. By itself, the fund's rate sets what banks charge each other for overnight borrowing, but it also spills through to many consumer debt products.

Tech shares took off because Chairman Powell acknowledged that “the disinflationary process” had started.

In a blink of an eye, the Nasdaq was up 2% and growth stocks were up 5%.

Powell intentionally didn’t pour cold water on the rally when he had a chance to smash it down with more hawkish rhetoric or a 50 basis point hike.

It appears highly likely that Powell isn’t interested in tech stocks or any equities for that matter experiencing another bloodbath like 2022.

There might be pitchforks out for him if there is a 30% loss in major indexes this year and perhaps he is scared that Washington would bring the heat. He likes his cushy job and the benefits that come with it.

I do believe this is only the first of a series of Powell Houdini acts where he is willing to disappear behind any sort of opportunity to smash down the markets and let them run wild.

Tech stocks will be a natural buy-the-dip opportunity during this deflation narrative.

We have a clear runway from 6.5% inflation to around 4% and during this 2.5% deflation drop, I can easily see the Nasdaq lurching higher.

I used Friday to add a bullish position in Lyft (LYFT) and Amazon (AMZN) after their terrible earnings while I took almost maximum profit in our Netflix (NFLX) call spread.

It was almost as if Powell announced a new round of QE or, well, sort of.

Global Market Comments

October 24, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MY SECRET MARKET INDICATOR),

(SPY), (USO), (TSLA), (TBT), (NFLX), (FXY), (SNAP)

I have access to inside information that is worth far more than any other technical or fundamental data out there.

It is almost always right and has made fortunes for me over the year, the dreams of avarice.

If the SEC knew about it, they would lock me up and throw away the key.

Here it is. But first, let me tell you about the performance it has delivered.

With some of the greatest market volatility in market history, my October month-to-date performance ballooned to +6.55%.

I used last week’s option expiration to take profits on my longs in JP Morgan (JPM), Visa (V), and Tesla (TSLA), and my one short in the S&P 500 (SPY). That leaves me with only one short in the (SPY) and 90% cash.

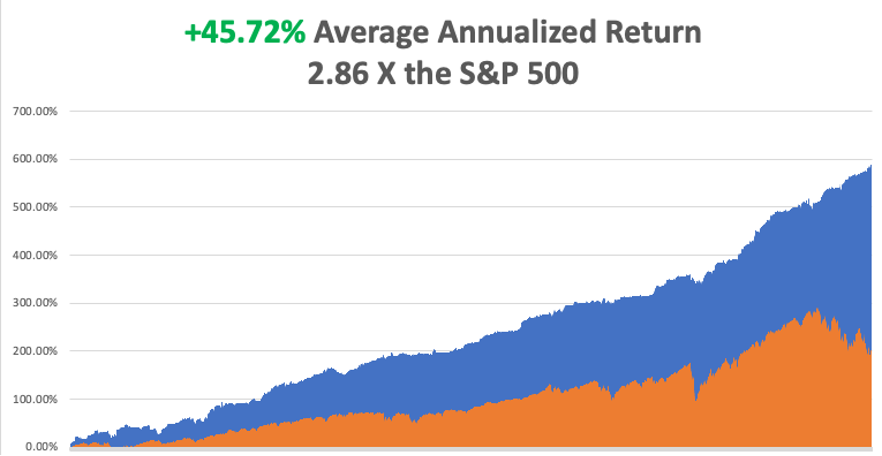

My 2022 year-to-date performance ballooned to +76.23%, a new high. The Dow Average is down -14.37% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +76.50%.

That brings my 14-year total return to +586.79%, some 2.86 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +45.72%, easily the highest in the industry.

So here is my unfair advantage:

I get to see what my own customers do, and I’m the only one who sees it.

For my own subscribers are among the most highly trained and disciplined in the market. 50% a year profits are common and every year, I learn of a couple of 1,000% profits (or 10X returns).

And here is what my customers are telling me today.

The end of the bear market is near. In fact, a “Big Turn” across all asset classes may be upon us.

Bonds are about to bottom out and yields peak. The US dollar may be double-topping. Commodities are crawling off a bottom. Price earnings multiples for stocked have just cratered from 21X to a decade low of 16X. Many stocks, like Tesla are trading at the lowest multiples in their lives.

Thus, the demand for LEAPS recommendations that offer tenfold two-year returns on far more modest equity appreciation has been skyrocketing.

I can’t blame them.

A final capitulation in the bond market is fast approaching. The United States Treasury Bond Fund (TLT) has collapsed by $88, from $180 to $92, or some 48.89%, covering the last six points in two days.

Ten-year yields have rocketed from 2.55% to 4.43% since August. The 2X short bond ETF (TBT) has spiked from $14 to $39 in a year. If you don’t cover the bond market on a daily basis, you may not know this.

It just so happens that I do.

It's an old investment nostrum that if you want to know what stocks are going to do, then take a close look at the bond market.

As Winston Churchill once said, “This is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.”

If you believe that the last interest rate hike in this cycle is only two months off, and we see interest rate cuts after that, then you need to be buying stocks now. You may be risking 10% of downside if you do, but miss out on 100% of upside if you don’t.

Here's another market old reliable. Markets always move more than you expect.

These may all sound like bold predictions. But then my followers are coming off of the best year for trading and investment in their entire lives. Confidence begets confidence.

If you are searching for global contagion, you don’t have far to look. The Japanese yen has cratered some 24% this year and is down by half from its last peak. That’s because the Bank of Japan, one of my old haunts, remains stubbornly insistent that ten-year JBG yields remain pegged at 0.25% while the US was raising from 0.25% to 4.43%.

You have to wonder what they are smoking in the Land of the Rising Sun. Their goal was to create a massive export boom with an ultra-cheap currency and runaway inflation with all the money printing. So far it hasn’t happened. GDP growth in Japan is stuck at snail-like 1.7%, while inflation remains a lowly 3.00%.

Go to Japan for the sushi, the public baths, and the Kurosawa samurai movies, not for inspiration on economic policy, which has been a disaster for 45 years. It’s tough to prosper against a gail-force demographic headwind.

Foreign exchange markets are easy to trade. You just follow the money and pile into the currency with the best yield advantage. Right now, that happens to be the US dollar (UUP).

Why wasn’t I selling short the Japanese yen (FXY) earlier this year? Because there were far better opportunities selling short US stocks, which I amply took advantage of.

It’s all in my numbers.

UK Government Collapses, with the resignation of prime minister Liz Truss in the shortest government in history. A new conservative leader will be elected next week. Truss took over a sinking ship. Her promised tax cuts delivered a fall in the British pound to a 40-year low. No matter what any future leader does, the UK standard will drop by half in the coming years, thanks to Brexit. THE HEAD OF LETTUCE WON!

30-Year Fixed Rate Mortgage Hits an Eye-popping 7.4%, in a clear Fed effort to shut down the real estate market. If this doesn’t kill the economy, nothing will. But home prices are nowhere near to 50%-70% declines seen in 20098-2011.

Existing Home Sales Plunge 23.8% YOY, in September, in the eighth straight month of sales declines. There are 1.2 million homes for sale, a six-month supply. The median home prices rose to $384,800.

Housing Starts Hit Two-Year Low, as the luxury end takes a hit. Starting families can no longer buy more houses than they can afford.

US Budget Deficit Drops by Half, after the sharpest decline in government spending in history. The red ink shrank from $2.78 trillion to only $1.38 trillion. It’s why I think the bond market may soon be bottoming out, with the (TLT) at $92 and the (TBT) at $38. A trillion here, a trillion there, and sooner or later, it adds up to a lot of money.

Ten-Year US Treasury Yields Hit 20-Year High, at 4.43%. If you’re waiting for rates to peak before buying stocks, it’s not yet. I’m looking for 4.50% before the crying is all over.

Fed Beige Book Says the Economy is Growing Modestly, an improvement from the last one. Travel & tourism is booming, auto sales are sluggish, and retail spending is flat. Manufacturing is steady, thanks to easing supply chain problems. High mortgage rates are a problem. Labor is still tight. It’s a very mixed report.

Tesla Earnings Beat Estimates for the 13th consecutive quarter profitability, taking the shares down 5%. Revenues came in at 24 billion, while units sold hot 340,000. The strong dollar is weakening Chinese and European sales. Tesla is still a decade ahead of the competition and boasts a global footprint. Production could hit 450,000-500,000 in Q4 once Austin and Berlin go to full production. The only competition will come from China. The Cybertruck comes out in 2023 and already has a million orders.

Netflix Earnings Blow Out, taking the stock up 15%, after a massive crackdown on password sharing. Some 30 million views are still watching the streaming channel for free. Some 2.41 new subscribers joined in Q3. The shift to advertising is next. Buy (NFLX) on dips.

SNAP Dives by 25%, thanks to a horrific earnings shortfall. Advertising Demand went from overwhelming to non-existent practically overnight. Small-cap growth is still being punished severely for any disappointments. The company is cutting 20% of its staff. Avoid (SNAP).

Supply Chain Problems are Disappearing, as two years of port congestion ease. A slowing economy is helping. After a year, I finally got my sofa from Vietnam. Overorders are coming back to haunt big retailers.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, October 24 at 8:30 AM, the S&P Global Flash PMI for September is released.

On Tuesday, October 25 at 7:00 AM, the S & P Case Shiller National Home Price Index for July is out.

On Wednesday, October 26 at 8:30 AM, New Home Sales for September are published.

On Thursday, October 27 at 8:30 AM, Weekly Jobless Claims are announced. US Q3 GDP is also announced.

On Friday, October 28 at 8:30 AM US Personal Income & Spending is printed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, back in 2002, I flew to Iceland to do some research on the country’s national DNA sequencing program called deCode, which analyzed the genetic material of everyone in that tiny nation of 250,000. It was the boldest project yet in the field and had already led to several breakthrough discoveries.

Let me start by telling you the downside of visiting Iceland. In the country that has produced three Miss Universes over the last 50 years, suddenly you are the ugliest guy in the country. Because guess what? The men are beautiful as well, the decedents of Vikings who became stranded here after they cut down all the forests on the island for firewood, leaving nothing with which to build long boats. I said they were beautiful, not smart.

Still, just looking is free and highly rewarding.

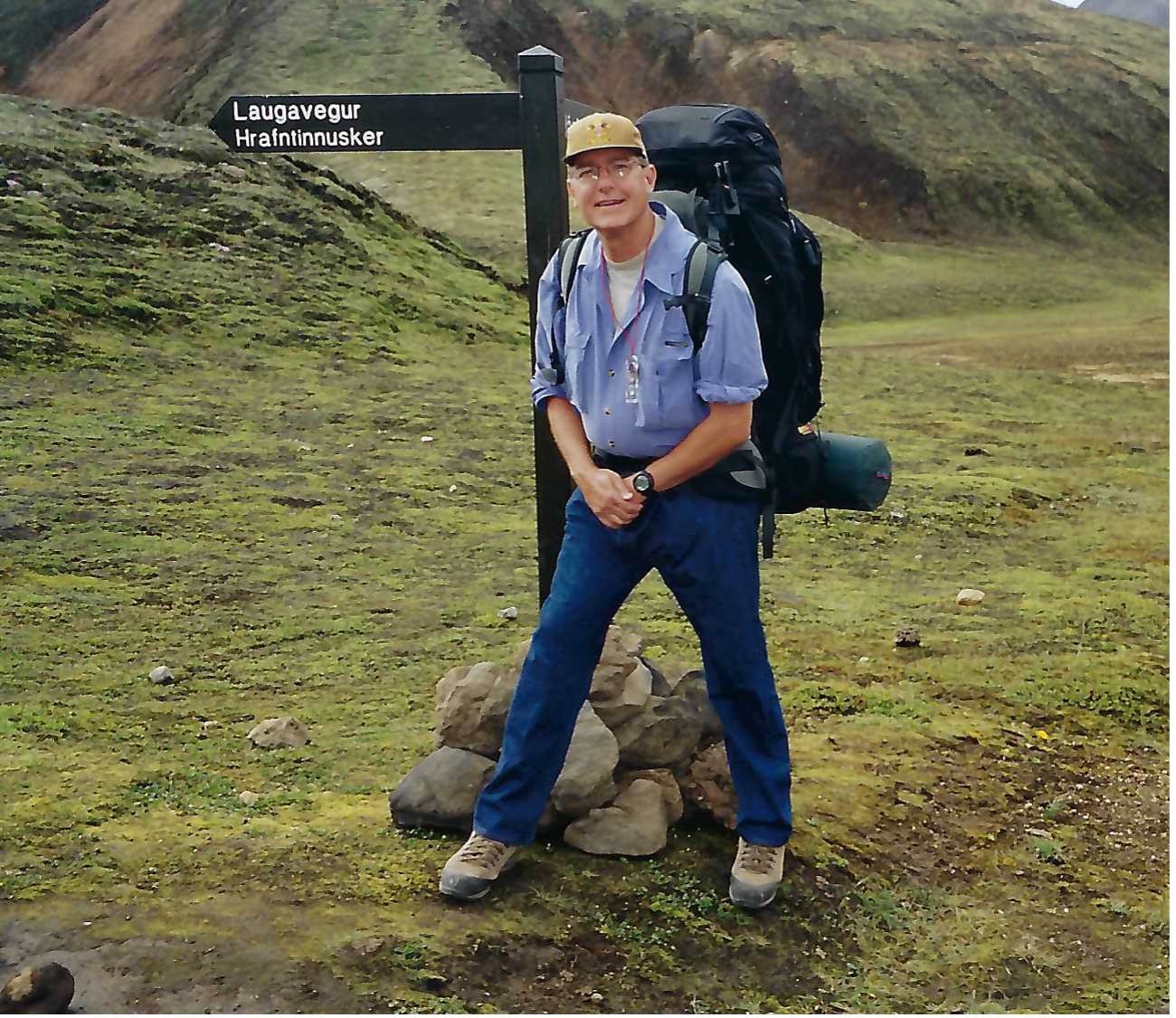

While I was there, I thought it would be fun to trek across Iceland from North to South in the spirit of Shackleton, Scott, and Amundsen. I went alone because after all, how many people do you know who want to trek across Iceland? Besides, it was only 150 miles, or ten days to cross. A piece of cake really.

Near the trailhead, the scenery could have been a scene from Lord of the Rings, with undulating green hills, craggy rock formations, and miniature Icelandic ponies galloping in herds. It was nature in its most raw and pristine form. It was all breathtaking.

Most of the central part of Iceland is covered by a gigantic glacier over which a rough trail is marked by stakes planted in the snow every hundred meters. The problem arises when fog or blizzards set in, obscuring the next stake, making it too easy to get lost. Then you risk walking into a fumarole, a vent from the volcano under the ice always covered by boiling water. About ten people a year die this way.

My strategy in avoiding this cruel fate was very simple. Walk 50 meters. If I could see the next stake, I proceeded. If I couldn’t, I pitched my tent and waited until the storm passed.

It worked.

Every 10 kilometers stood a stone rescue hut with a propane stove for adventurers caught out in storms. I thought they were for wimps but always camped nearby for the company.

One of the challenges in trekking near the north Pole is getting to sleep. That because the sun never sets and its daylight all night long. The problem was easily solved with the blind fold that came with my Icelandic Air first class seat.

I was 100 miles into my trek, approached my hut for the night and opened the door to say hello to my new friends.

What I saw horrified me.

Inside was an entire German Girl Scout Troop spread out in their sleeping bags all with a particularly virulent case of the flu. In the middle was a girl lying on the floor soaking wet and shivering, who had fallen into a glacier-fed river. She was clearly dying of hypothermia.

I was pissed and instantly went into Marine Corp Captain mode, barking out orders left and right. Fortunately, my German was still pretty good then, so I instructed every girl to get out of their sleeping bags and pile them on top of the freezing scout. I then told them to strip the girl of her wet clothes and reclothe her with dry replacements. They could have their bags back when she got warm. The great thing about Germans is that they are really good at following orders.

Next, I turned the stove burners up high to generate some heat. Then I rifled through backpacks and cooked up what food I could find, force-fed it into the scouts, and emptied my bottle of aspirin. For the adult leader, a woman in her thirties who was practically unconscious, I parted with my emergency supply of Jack Daniels.

By the next morning, the frozen girl was warm, the rest were recovering, and the leader was conscious. They thanked me profusely. I told them I was an American “Adler Scout” (Eagle Scout) and was just doing my job.

One of the girls cautiously moved forward and presented me with a small doll dressed in a traditional German Dirndl which she said was her good luck charm. Since I was her good luck, I should have it. It was the girl who was freezing to death the day before.

Some 20 years later, I look back fondly on that trip and would love to do it again.

Anyone want to go to Iceland?

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Iceland 2001 with German Girl Scout

Global Market Comments

October 21, 2022

Fiat Lux

Featured Trade:

(OCTOBER 19 BIWEEKLY STRATEGY WEBINAR Q&A),

(BAC), (USO), (SPY), (TSLA), (NFLX), (TBT), (PLTR), (SNOW)

Below please find subscribers’ Q&A for the October 21 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: Bank of America (BAC) said the US consumer is strong and lending is robust. Does this mean no recession in 2023?

A: It could, because remember that while some sectors are clearly in recession, like real estate and automakers, and have been for a while, others are absolutely booming, like the airline business, and the banking business. There may not be a recession in here, or if there is one, it’s a very slight one. Count on the market to first discount a severe recession which would take the S&P 500 down to $3,000-$3,200 or so; and that’s what markets do, always overly pessimistic at the bottom and overly euphoric at tops. You can make your living off of this.

Q: What do you think about OPEC's behavior (USO) and its influence on the price of oil?

A: Clearly, they’re trying to influence the midterm elections and get an all-republican pro-oil Congress, which will be nicer to OPEC. That’s certainly what they got with the last administration and it’s safe to say that the pro-climate administration of Biden and the Saudis get along like oil and water. But long term, OPEC knows it’s going to zero, and in fact, Saudi Arabia has plans to turn their entire oil supply into hydrogen which can be exported and burned cleanly. I know the team here at UC Berkeley that’s working on that with the Saudi government. Cheap hydrogen also means airships come back, how about that? Hindenburg anyone?

Q: Will draining the Strategic Petroleum Oil Reserve (SPR) backfire, meaning deflation for the US economy and administration?

A: No, the SPR outlived its usefulness maybe 30 years ago—it’s essentially a government subsidy for Texas and Louisiana, and for the oil industry, that has taken on a life of its own. When we started the SPR in 1975, the US got more than half of its oil from the Middle East. Now, it’s almost zero. It goes to China instead. If we are a net energy producer and we have been for over 5 years, why do we even need a petroleum reserve? So no, I think we should shut it down and sell all the oil that’s in there. And it becomes even less relevant as more of the US economy turns over to alternatives.

Q: How do we operate our military with no oil?

A: The pentagon is working on a no-oil future, developing alternative fuels for all kinds of things that you wouldn’t imagine are possible. For example, instead of using diesel, jet fuel, or gasoline for our vehicles, you outfit them with electric batteries, and when the batteries go dead you just air drop new fully charged ones. It’s much better than trying to transport gasoline across the desert in a giant fuel bladder, which can be taken out by a single bullet and is what they do now. Take the pilots out of fighters and they become so light they can operate on battery power. So yes, the pentagon has actually been in the forefront of using every alternative technology they can get their hands on from the early days. Better they get them first before an enemy does.

Q: We will almost always need petroleum; far too many products use it as an ingredient.

A: That is absolutely right. Some will probably never be replaced, like asphalt, feedstock, or plastic. However, those represent less than 10% of the current oil demand. So yes, there always will be an oil industry, it just might be a heck of a lot smaller than it is now. You eliminate cars from the picture, and that’s half of all oil demand in the United States right there. And in most places in the United States, it will be illegal to sell a car that uses gasoline in 12 years. And do you make 30-year investments based on demand for your product dropping by half in 12 years? No, you don’t, which is why the oil companies themselves won’t invest in their own industries anymore. They’re only paying out profits as dividends and buying back shares, which they never used to do.

Q: Do you think the Standard & Poor’s 500 Index (SPX) $3,500 was the bottom?

A: No, we actually did get a little bit lower than that. We will be in a bottoming process over the next several months, but the pattern will be the same. Tiny marginal new bottoms, maybe 100 points lower than the last, and then these gigantic rallies. If we do make bottoms they will only be for seconds, so the way to deal with that is to only put in really low-limit orders to buy stuff, assuming 1,000 points down, and just keep entering the order every day. Eventually, you’ll get one of these throw-away fills when the algorithms panic and a bunch of market orders hit the market. That's the way to deal with that.

Q: I would say that Biden is trying to influence the elections by releasing oil reserves.

A: Absolutely he is, but then so is the oil industry, taking half of the refineries off stream 2 months before the elections, and spiking oil prices. So it’s a battle of the oil price going on here. No love lost between the oil industry and Biden, and US consumers for that matter. I don’t care if gasoline is $7 a barrel because I never buy it; I am all electric. But for a lot of working people, that’s definitely a lot of money.

Q: How concerned are you about the US going to a cashless currency?

A: I’m not worried because I pay my taxes and I don’t break any laws. If you don’t pay taxes and do break laws, like engaging in drug dealing or bribery, you should be extremely worried, as that would be the eventual goal of a cashless economy. That and the fact that the government has to spend $300 million a year printing paper money, which they’d love to get rid of. And of course, it’s cheaper for businesses to use digital currencies. Most countries in Europe don’t use physical currency anymore—it’s credit cards only.

Q: Do you expect Tesla (TSLA) to pop after earnings?

A: I have no idea; it depends on what the report says but suffice it to say that Tesla is historically cheap. It has the lowest PE multiple now than it has in the entire 13-year history of the company. Scale in on the LEAPS with Tesla—that’s what I’d be doing down here.

Q: Could the US debt situation spiral into something that gets out of hand?

A: No, because the purchasing power of debt is now deflating at an 8.4% annual rate, which means that it goes to zero in about 8.57 years. This is how the government always wins when issuing debt. It’s been going on since the French first issued government debt 300 years ago. Who pays for that? Bond investors. Anybody who owns bonds now has seen their purchasing power go up in smoke. That’s why it’s been a one-way zero bid market for two and a half years—they’ve been dumping like crazy.

Q: Should I buy debt here or sell it?

A: We’re actually getting close to a bottom in the junk debt market, which means you’re going to be yielding around 10%. That means the value of your holding doubles in 6 years, and the default rates never reach the high levels predicted by analysts in junk bonds. That has always been the key to junk bonds in the whole 50 years that I've been following this market. My neighbor up in Tahoe, Mike Milliken, made billions off that assumption.

Q: What do you think about Netflix (NFLX)?

A: Well, my advice was to buy it, to a lot of people. They’re clearly changing their business model for the better—they’re going to start picking up ad revenues, they’re cracking down on password sharing, and they delivered a 20% return in stocks. Plus their share price has just dropped down from $700 to $165. Great LEAP candidate here.

Q: What kind of position is best if a recession hits?

A: Cash. Cash is now yielding 4.4%. The best cash alternative is 90-day T-bills issued by the US Treasury. Execution costs almost zero, and liquidity is essentially infinite; but, remember also that bull markets start 6 to 9 months before recessions end. You just have to watch your timing. Which means that if the recession ends in say July, you have to be buying stocks today. Just keep that in mind, ladies and gentleman.

Q: How do you see the futures of semis?

A: Anything you buy here now will triple in three years, but it becomes a question of how much pain you want to take in the meantime. Everyone in the investment management industry thinks the same, and it really is a classic “catch-a-falling-knife” situation— knowing that the payoff down the road is enormous. Virtually all companies are designing new semis into their products at an exponential rate.

Q: Are LEAPS part of the service?

A: Yes, they are. I will send you one tomorrow. But concierge customers get first priority because that’s what they’re paying for.

Q: How far out should we go?

A: On LEAPS, always take the maximum maturity, which is usually 2 years and 4 months. And the reason is that the second year is almost free—they charge you almost nothing for going out to maximum maturity. And if we have a recession that does last longer than people think, that extra year of maturity will be worth its weight in gold. It’ll be the difference between a zero return and a 10x return.

Q: Can we go back into the ProShares UltraShort 20+ Year Treasury (TBT)?

A: No, it would be a horrible idea to buy the (TBT) here after it just moved from $14 to $36. That’s what you buy before it goes from $14 to $36. We’re topping out in all of these short bond plays, so avoid them like the plague.

Q: How much is the Concierge Service?

A: It’s $12,000 a year—and a bargain price at that! Almost everybody ends up covering that on their first trade, and you get an entire portfolio of LEAPS and a dedicated LEAPS website with the service. You also get my personal cell phone number so you can call me while I'm either on the beach in Hawaii or on the ski slopes of Lake Tahoe. If anyone has questions about the concierge service, contact customer support at support@madhedgefundtrader.com.

Q: What are your thoughts on data analytics companies Snowflake (SNOW) and Palantir (PLTR)?

A: Love Snowflake, hate Palantir because the CEO isn’t interested in promoting a share price. With (SNOW), you have Warren Buffet as a major holder, so that’s all you need to know there. (SNOW) also has a 75% fall behind it.

Q: Thoughts on the Ukraine/Russia war?

A: It’ll drag on well into next year, and obviously the Iranian drones are the new factor here. I wouldn’t be surprised if there were suddenly an accident at a certain factory in Iran; that’s what happens when these things play out.

Q: Is Snowflake (SNOW) a buy right now?

A: It’s like all the rest of tech. High volatility, could have lower lows, but long-term gains are at least a triple from here. You know how much risk you can take.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Dungeon in Montreux Castle on Lake Geneva in Switzerland

Mad Hedge Technology Letter

October 19, 2022

Fiat Lux

Featured Trade:

(IGNORE THE APOCALYPSE RUMORS)

(NFLX), (FED)