Netflix (NFLX) adding 2.41 million global subscribers means the technology sector will not have the earnings apocalypse that many thought was around the corner.

It’s good news for tech stocks as a whole.

This is why tech stocks have rallied hard the last few days as well as news that there is a 100% probability of a .75% rate hike at the November 2nd Fed meeting priced into current tech valuations.

The market always loves certainty.

The multi-million subscribers added is commendable for the streaming company, but like many things in life, the devil is in the details.

Later in the earnings report, Netflix management says that “aggregate annual direct operating losses this year alone could be well in excess of $10 billion, compared with our +$5-$6 billion of annual operating profit.”

In short, Netflix is adding subscribers, at least this past quarter, but not in a profitable way.

They have had to dilute the quality of their services by integrating an ad model which goes against the spirit of what Neflix was intended to be.

Not only tech companies, but companies around the world are decreasing the quality of services through shrinkflation or “smart” packaging or just offering a worse version of a previously better iteration.

Costs have come up for everyone too but I don’t believe losing over $10 billion in annual operating losses will sit well with tech investors.

That means that Netflix must either raise the quality of their content so customers are inclined to pay higher prices or integrate more ads into their ad models.

The question must be asked, how much are Netflix subscribers willing to pay for a monthly service?

The premium package is already $19.99 and my bet is that NFLX experiences serious attrition if they go to $25 per month.

The ad version being priced at $6.99 is being too hyped up and I see it as a net negative for NFLX.

I don’t believe NFLX can do the undoable which is ramping up the quality of content in the short term.

Earnings apocalypse is off the table precisely because Americans are still spending because they still have jobs.

Yet, this sets the stage for weaker and shorter bear market rallies followed by thundering sell-offs.

This isn’t just about one indicator versus the next.

It was current US Treasury Secretary Janet Yellen who responded to a reporter in the past that she wasn’t worried about America’s large federal debt because “interest rates were low.”

Well, now there is finally a cost to rolling over that federal debt and tech stocks are valued lower for it.

Netflix is a symptom, not the main virus.

That is why Netflix adds over 2 million subscribers but will lose $10 billion annually to do it. This is also why the US economy boasts of full employment but has a negative GDP. As the zombie companies pile up, the key is to preserve free cash flow and as for the tech market, sell any big bear market rally.

US consumers still have money and they will have enough if they don’t lose their jobs, but the Fed is hoping to artificially induce a job crisis.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-10-19 15:02:152022-11-02 03:36:35Ignore the Apocalypse Rumor

As the tech job cuts go from bad to terrible, how does this shake out the tech sector?

Just this morning, Twilio (TWLO) announced a major purge sacking 11% of its workforce to focus on reducing operating costs and improving margins.

Is this the end of it for the mighty tech machine?

Hardly so.

Tech companies will get more lean, efficient, and cutthroat which many might argue they should have been like that in the first place.

It’s somewhat true that tech business models got somewhat bloated in the era of euphoria.

Some unnamed big tech companies almost became like adult daycare centers.

Like overshooting in terms of revenue, development, and achievements to the upside in tech, and I acknowledge there was a lot to celebrate, I believe that the same works in reverse.

Staff at tech companies will be disposed of ruthlessly, and tech companies will most likely overcut jobs as a way to get their points across and show shareholders that they will flesh out costs during tough times.

Tough times in the big tech world mean less than growth margins, but they are still doing better than any small business who are outright going bankrupt.

Tech companies are in an advantageous position because the technology they harness can be used to scale up using software.

Less staff that manufactures higher productivity is an executive’s dream.

This time around, I firmly believe that automation will start to reach further up the employment chain because automation gets better with each iteration.

Humans also complain, get sick, need bathroom and coffee breaks, ask for promotions and raises when software code doesn’t.

We aren’t to the point of one CEO and the rest bots and software, but that’s the direction we are headed.

The silver lining for many of these fired tech workers is that the labor market is on fire. Although the unemployment rate ticked up to 3.7% last month, it’s still hovering at a 50-year low. The data is there – there are about two job openings for every unemployed person.

More than 50,000 tech workers have been laid off since the beginning of this year.

These fired tech workers will be able to find new jobs rapidly and in many cases with a juicy promotion, higher wage, and better benefits like 100% remote work opportunities, because there is still a huge shortage of qualified workers. Skills are fungible too.

Many will be able to pivot into the financial world and find jobs on Wall Street, who for the past generation have been losing talent to tech.

As interest rates rise, banks become winners.

Lastly, the pedestrian interest rate rises executed by the US Central Bank means that the job market will stay a lot hotter than first expected.

Even if they do get to 4% in the Fed Funds rate by the end of 2023, 4% is still historically low and companies will still be hiring albeit with a more measured approach and lower wages.

The slow pace of rises hurt tech because it allows the fired workers more time and better opportunities to get entrenched in a new sector while job offers are still plentiful.

The net result is the opposite of what the Fed wants which is more inflation as fired tech workers rotate into better-paying jobs spending even more money on goods and services.

This feeds into the higher inflation problem.

In short, this is a death-by-a-hundred-cuts sort of reaction for tech stocks. Tech stocks won’t explode to the upside until the workers can’t just re-up to a cushy healthcare job or Wall Street job like now.

Short every rally in wounded tech stocks like Facebook (META) and Netflix (NFLX).

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-14 16:02:582022-10-03 02:31:17Job Market Working Against Tech Stocks

After a half-century in the markets, I have noticed that it is the investors with the correct long-term views who make the biggest money. My favorite example is my friend, Warren Buffet, who doesn’t care if an investment turns good in five minutes or five years.

Buffet’s Berkshire Hathaway (BRKB) is the largest outside investor in Apple (AAPL). And guess what his cost has been? By the time you add up the compounded dividends he has collected since he started buying the stock in 2011, it's zero. The value today? $15.5 billion.

Buffet didn’t buy Apple for its hardware, iPhone, or iTunes. He bought it for the brand, which has improved astronomically. Look at Berkshire’s portfolio and it is packed with brands, like American Express (AXP), Coca-Cola (KO), and Exxon (XOM).

When did Buffet last buy Apple? In May when it hit $130.

That’s why Warren Buffet is Warren Buffet and you are you.

While the inflation news last week has been great and it is likely to get better, I believe that investors are missing the bigger, more important long-term picture.

The fact is that markets are now discounting an earlier than expected end to the Ukraine War, much earlier.

I get constant updates on the war from the Joint Chiefs of Staff, Britain’s Defense Committee, and NATO headquarters and I can tell you that the war has taken a dramatic turn in Ukraine’s favor just in the last two weeks.

Russian casualties have topped 80,000, nearly half the standing army. They have lost 2,200 of their 2,800 operational tanks. Some 120 front line aircraft have been destroyed. This week, Ukraine attacked the principal Russian air base in Crimea, leaving the smoking ruins of seven more aircraft there.

Russia is in effect fighting a modern digitized war with 50-year-old Cold War weapons and it isn’t working. Its generals have no experience fighting wars against determined opposition. Putin would do better listening to the retired generals on CNN for military advice.

America’s High HIMARS (the M142 High Mobility Artillery Rocket System) has become the Stinger missile of this war. The Lockheed Martin (LMT) factory in Camden, Arkansas that makes these missiles is running 24/7 on doubled orders.

The sanctions against Russia have been wildly successful. The Russian economy is utterly collapsing. What oil they are selling now is at half price. Aircraft are being cannibalized for parts to keep others flying. Much of the educated middle class has fled the country. Draft dodging is rampant.

What does all this mean for you and me?

The commodity price spike the war prompted has ended and most are now in steep downtrends. Gold (GLD), where the Russians were major buyers, has been flat as a pancake. This has put our inflation numbers into freefall. Interest rate fears peaked in June and are now in the rear-view mirror.

As is always the case, markets have seen these developments and correctly ascertained their consequences far before we humans did (except for maybe me). It has been no surprise that they have been tracking the Russian defeat day by day and have been on an absolute tear since June 15.

Even small techs suffering 18-month bear markets have now begun major recoveries, with companies like Snowflake (SNOW), up 50%, Netflix (NFLX), up 39%, and Cathie Wood’s Innovation Fund (ARKK) up 57%. Even crypto has returned from the grave, with Ethereum (ETHE) up an eye-popping 105%.

But don’t go gaga over stocks just yet.

The Fed ramps up quantitative tightening in September to $95 billion a month and will deliver another interest rate hike. That's why I am running a double short in the bond market (TLT), (TBT) once again.

We also have the midterms to worry about which, with recent developments, promise to be more contentious than ever. Look for another round of tiring new election fraud claims.

That’s great because these events will give us good entry points lower down for trade alerts, not the short-term top we are looking at right now.

It helps that with ten-year US Treasury yields at 2.80%, it has an effective price earning multiple of 37, while stocks growing earnings at 10% a year boast a price earnings multiple of only 16. That sets up a massive, long stock/short bond trade which Mad Hedge will be pushing well on into 2023.

And you know what?

The smart guys I know in the hedge fund community are starting to model for the next Fed interest rate CUT. Markets will love it and discount this far in advance.

If you want to get on the train with me before it leaves the station, just keep reading this newsletter.

Yes, markets are now being driven by rate cuts and peace prospects, not rate rises and war!

Your retirement fund will love it.

I just thought you’d like to know.

CPI Dives to 8.5%, down 0.6% in July. The peak is in, and stocks rallied 500. Look for another drop in August, with gasoline prices falling daily. The 800-pound gorilla in the room has exited.

The Producer Price Index Dives 0.5%, confirming last week’s weak CPI number. And many core prices are indicating that we will get another drop when the August numbers are reported in September. It was worth another 300-point rally in the Dow Average, which is getting seriously overbought.

Consumer Inflation Expectations dive to 6.2% for the coming year and only 3.2% for three years. according to a New York Fed Survey. Expectations for food costs saw the largest decline. The CPI is out on Wednesday. No doubt a media onslaught over a coming recession has a lot to do with it.

Elon Musk Sells $6.9 billion worth of Tesla (TSLA) Stock, explaining the $100 drop in the shares last week. Ostensibly, this is to pay for Twitter if he loses his court case. Musk clearing took advantage of a 60% rise in (TSLA) to head off distress sales in the future. Musk also opened the door to share buy backs in the future. Buy (TSLA) on dips.

85,000 IRS Agents are Headed Your Way, but only if the government can hire them and only if you are a billionaire or a profitable large oil company. The rest of us will be ignored by this unpublicized portion of the Biden inflation bill.

US Dollar (UUP) Takes a Hit on CPI Report, which effectively showed that the US saw deflation in July. The greenback is pulling back the 20-year highs which gave you the cheapest European vacation in your lives. The prospect of interest rates rising at a slower pace is dollar negative. Buy (FXA) and (FXC) on dips.

Boeing (BA) Delivered its First 787 Dreamliner in a year, after long-awaited regulatory approval. The monster 30% rise in the shares off the June low predicted as much. A global aircraft shortage helps. Airbus is going to have to start earnings its money again. Keep buying (BA) on dips.

Weekly Jobless Claims Pop 12,000 to 262,000, a new high for the year. It’s not at concerning levels yet but is definitely headed in the wrong direction. Maybe it’s just a summer slowdown? Maybe not.

Shipping Container Charges are Plunging Everywhere, except in the US, which currently has the world’s strongest economy. It’s a sign that global supply chain problems are easing. But the US leads the world in demurrage, or delays, with New York the worst, followed by Long Beach. Import Prices are Plunging, thanks to a super strong dollar, taking more pressure off of inflation. They fell 1.4% in July according to the Department of Labor. Easing supply chain problems are helping. Biden has had the run of the table for months now

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil prices now rapidly declining, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

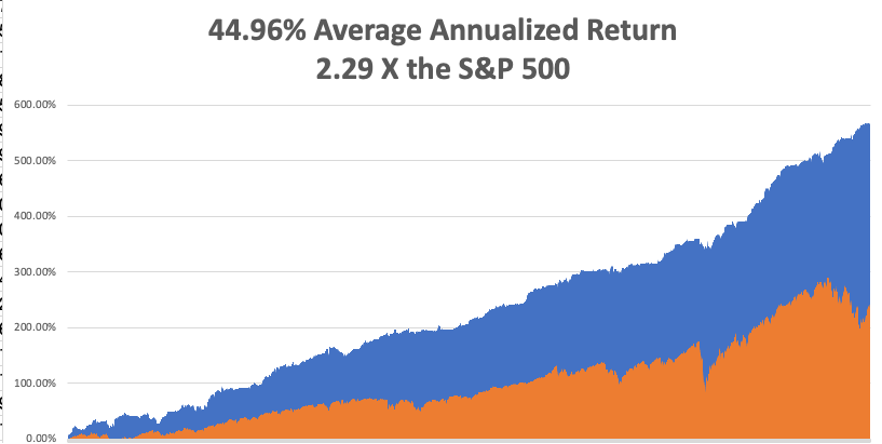

My August performance climbed to +2.14%. My 2022 year-to-date performance ballooned to +56.97%, a new high. The Dow Average is down -7.0% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 74.76%.

That brings my 14-year total return to 569.53%, some 2.56 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.96%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 93 million, up 300,000 in a week and deaths topping 1,037,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, August 15 at 8:30 AM EDT, the New York Empire State Manufacturing Index for August is released.

On Tuesday, August 16 at 8:30 AM, the Housing Starts for July are out.

On Wednesday, August 17 at 8:30 AM, Retail Sales for July are published. At 11:00 AM the Fed Minutes from the last meeting are printed.

On Thursday, August 18 at 8:30 AM, Weekly Jobless Claims are announced. Existing Home Sales for July are announced. On Friday, August 19 at 2:00 the Baker Hughes Oil Rig Count is out.

As for me, while we’re all waiting for the dog days of August to end, it is time to reminisce about my old friend George Schultz who passed away last year at the age of 101.

My friend was having a hard time finding someone to attend a reception who was knowledgeable about financial markets, White House intrigue, international politics, and nuclear weapons.

I asked who was coming. She said Reagan’s Treasury Secretary George Shultz. I said I’d be there wearing my darkest suit, cleanest shirt, and would be on my best behavior, to boot.

It was a rare opportunity to grill a high-level official on a range of top-secret issues that I would have killed for during my days as a journalist for The Economist magazine. I guess arms control is not exactly a hot button issue these days.

I moved in for the kill.

I have known George Shultz for decades, back when he was the CEO of the San Francisco-based heavy engineering company, Bechtel Corp in the 1970s.

I saluted him as “Captain Schultz”, his WWII Marine Corp rank, which has been our inside joke for years. Now that I am a major, I guess I outrank him.

Since the Marine Corps didn’t know what to do with a PhD in economics from MIT, they put him in charge of an anti-aircraft unit in the South Pacific, as he was already familiar with ballistics, trajectories, and apogees.

I asked him why Reagan was so obsessed with Nicaragua, and if he really believed that if we didn’t fight them there, would we be fighting them in the streets of Los Angeles as the then-president claimed.

He replied that the socialist regime had granted the Soviets bases for listening posts that would be used to monitor US West Coast military movements in exchange for free arms supplies. Closing those bases was the true motivation for the entire Nicaragua policy.

To his credit, George was the only senior official to threaten resignation when he learned of the Iran-contra scandal.

I asked his reaction when he met Soviet premier Mikhail Gorbachev in Reykjavik in 1986 when he proposed total nuclear disarmament.

Shultz said he knew the breakthrough was coming because the KGB analyzed a Reagan speech in which he had made just such a proposal.

Reagan had in fact pursued this as a lifetime goal, wanting to return the world to the pre nuclear age he knew in the 1930s, although he never mentioned this in any election campaign. Reagan didn’t mention a lot of things.

As a result of the Reykjavik Treaty, the number of nuclear warheads in the world has dropped from 70,000 to under 10,000. The Soviets then sold their excess plutonium to the US, which has generated 20% of the total US electric power generation for two decades.

Shultz argued that nuclear weapons were not all they were cracked up to be. Despite the US being armed to the teeth, they did nothing to stop the invasions of Korea, Hungary, Vietnam, Afghanistan, and Kuwait.

Schultz told me that the world has been far closer to an accidental Armageddon than people realize.

Twice during his term as Secretary of State, he was awoken in the middle of the night by officers at the NORAD early warning system in Colorado to be told that there were 200 nuclear missiles inbound from the Soviet Union.

He was given five minutes to recommend to the president to launch a counterstrike. Four minutes later, they called back to tell him that there were no missiles, that it was just a computer glitch projecting ghost images on a screen.

When the US bombed Belgrade in 1989, Russian president Boris Yeltsin, in a drunken rage, ordered a full-scale nuclear alert, which would have triggered an immediate American counter-response. Fortunately, his generals ignored him.

I told Schultz that I doubted Iran had the depth of engineering talent needed to run a full-scale nuclear program of any substance.

He said that aid from North Korea and past contributions from the AQ Khan network in Pakistan had helped them address this shortfall.

Ever in search of the profitable trade, I asked Schultz if there was an opportunity in nuclear plays, like the Market Vectors Uranium and Nuclear Energy ETF (NLR) and Cameco Corp. (CCR), that have been severely beaten down by the Fukushima nuclear disaster.

He said there definitely was. In fact, he was personally going to lead efforts to restart the moribund US nuclear industry. The key here is to promote 5th generation technology that uses small, modular designs, and alternative low-risk fuels like thorium.

Schultz believed that the most likely nuclear war will occur between India and Pakistan. Islamic terrorists are planning another attack on Mumbai. This time, India will retaliate by invading Pakistan. The Pakistanis plan on wiping out this army by dropping an atomic bomb on their own territory, not expecting retaliation in kind.

But India will escalate and go nuclear too. Over 100 million would die from the initial exchange. But when you add in unforeseen factors, like the broader environmental effects and crop failures (CORN), (WEAT), (SOYB), (DBA), that number could rise to 1-2 billion. This could happen as early as 2023.

Schultz argued that further arms control talks with the Russians could be tough. They value these weapons more than we do because that’s all they have left.

Schultz delivered a stunner in telling me that Warren Buffet had contributed $50 million of his own money to enhance security at nuclear power plants in emerging markets.

I hadn’t heard that.

As the event ended, I returned to Secretary Shultz to grill him some more about the details of the Reykjavik conference held some 36 years ago.

He responded with incredible detail about names, numbers, and negotiating postures. I then asked him how old he was. He said he was 100.

I responded, “I want to be like you when I grow up”.

He answered that I was “a promising young man.” I took that as encouragement in the extreme.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

We’re Getting Pretty High

https://www.madhedgefundtrader.com/wp-content/uploads/2022/08/wristwatch.jpg331441Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-08-15 09:02:082022-08-15 13:26:22The Market Outlook for the Week Ahead, or What the Market is Really Discounting Now

The reversion to the mean crowd who like to do no research and just buy certain shares when they go down anticipating a quick rebound needs to avoid former streaming darling Netflix (NFLX).

The company has gone from bad to worse and like your black sheep little brother who loves to play the victim, avoid at all costs!

NFLX has parlayed deteriorating content with an even worse future game plan that screams subscriber bleeding.

The headwinds are adding up to something that will be insurmountable quite soon and I don’t believe that has been accurately reflected in the stock price yet.

Let’s take the running of their clean brand.

They are damaging the brand by integrating it with a lower-cost, ad-supported tier in early 2023. This comes on the heels of Netflix tapping Microsoft to be its partner on the ad-supported offering.

For many years, NFLX was adamant they would never go this route only to do an about-face.

Already losing subscribers, inserting ads to only muddy the content further won’t move the needle in terms of improving the quickly eroding content quality.

Like on a sinking ship, they are trying to chug as many whiskey bottles as possible before the ship goes underwater.

Netflix had warned investors last quarter that it expected to shed around 2 million subscribers but only lost around 970,000 during the three-month period ending June 30.

This artsy game of claiming a pyrrhic victory because the subscriber loss was only around a million and not 2 is insane.

A million subscribers lost is detrimental to any subscriber-based company in any sphere of business.

And remember, NFLX is supposed to be the preeminent growth company, yes, the one that is losing 1 million subscribers every 3 months.

Let’s rate the business model today.

Will the median consumer bite at a monthly NFLX subscription?

In the current market environment, which is characterized by inflation, consumers alter spending. In concrete terms, this means that consumers are concentrating on fewer streaming services.

Also, an NFLX content archive that is shrinkflating doesn’t help and I am not talking in terms of volume.

They no longer have access to the hit shows of old like Friends or Seinfeld that many Millennial viewers love to watch because other streaming platforms have recalled that content.

Times are lean to the bone for NFLX these days.

What we have today is a streaming service that can’t make in-house blockbusters apart from Stranger Things and after that, the kitchen is barren.

Weirdly enough, NFLX executives have turned to anime as if it’s a broad solution to the content woes.

I’ll give you a hint - it’s not.

Stealing content ideas from their 14-year-old daughter won’t hack it in this climate.

Even worse, they are taking classic anime titles from Japan and Americanizing them.

This type of Frankenstein anime is hard to watch.

The conclusion of Stranger Things Season 4 is peak NFLX for 2022 as pitiful as that sounds.

The search for content has really gone into full drive with Amazon (AMZN) picking up France Ligue 1 soccer league rights for $250 million per year on a 3-year contract.

Things have moved on a lot in the content world with American tech companies scouring the world for quality content while NFLX has been stuck in neutral.

The stock has gone from $700 to $200, and the poor executive decisions today mixed with inferior content means that they will underperform any tech rally that is manufactured to end the year.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-08-03 16:02:382022-08-03 22:29:59Losing Its Mojo

Last weekend, I had dinner with one of the oldest and best-performing technology managers in Silicon Valley. We met at a small out-of-the-way restaurant in Oakland near Jack London Square so no one would recognize us. It was blessed with a very wide sidewalk out front and plenty of patio tables.

The service was poor and the food indifferent, as are most dining experiences these days. I ordered via a QR code menu and paid with a touchless Square swipe.

I wanted to glean from my friend the names of the best tech stocks to own for the long term right now, the kind you can pick up and forget about for a decade or more, a “lose behind the radiator” portfolio.

To get this information, I had to promise the utmost confidentiality. If I mentioned his name, you would say “oh my gosh!”

Amazon (AMZN) is now his largest holding, the current leader in cloud computing. Only 5% of the world’s workload is on the cloud presently so we are still in the early innings of a hyper-growth phase there.

By the time you price in all the transportation, labor, and warehousing costs, Amazon breaks even with its online retail business at best. The mistake people make is only focusing on this lowest of margin businesses.

It’s everything else that’s so interesting. While its profitability is quite low compared to the other FANG stocks, Amazon has the best growth outlook. For a start, third-party products hosted on the Amazon site, most of what Amazon sells, offer hefty 30% margins.

Amazon Web Services (AWS) has grown from a money loser to a huge earner in just four years. It’s a productivity improvement machine for the world’s cloud infrastructure where they pass all cost increases on to the customer who, once in, buy more services.

Apple (AAPL) is his second holding. The company is in transition now justifying a massive increase in earnings multiples, from 9X to 25X. The iPhone has become an indispensable device for people around the world, and it is the services sold through the phone that are key.

The iPhone is really not a communications device but a selling device, be it for apps, storage, music, or third-party services. The cream on top is that Apple is at the very beginning of an enormous replacement cycle for its installed base of over one billion phones. Moving from upfront sales to a lifetime subscription model will also give it a boost.

Half of these are more than four years old, and positively geriatric in the tech world. More than half of these are outside the US. 5G has added a turbocharger.

Netflix (NFLX) is another favorite. The world is moving to “over the top” content delivery and Netflix is already spending twice as much on content as any other company in this area. This is why the company won an amazing 44 Emmys last year. This will become a much more profitable company as it grows its subscriber base and amortizes its content costs. Their cash flow is growing by leaps and bounds, which they can use to buy back stock or pay a dividend.

Generally speaking, there is no doubt that the pandemic has pulled forward some future technology demand with the stay-at-home trend. But these companies have delivered normal growth in a hard world.

5G has enabled better Internet coverage for everyone and increased the competitiveness of the telecom companies. Factory automation has been another big area for 5G, as it is reliable and secure, and can be integrated with artificial intelligence.

Transportation will benefit greatly. Connected self-driving cars will be a big deal, improving safety and the quality of life.

My friend is not as worried about government-threatened break-ups as regulation. There will be more restraints on what these companies can do going forward. Europe, which has no big tech companies of its own, views big American tech companies simply as a source of revenue through fines. Driving companies out of business through cutthroat competition is simply not something Europeans believe in.

Google (GOOG) is probably more subject to antitrust proceedings both in Europe and the US. The founders have both retired to pursue philanthropic activities, so you no longer have the old passion (“don’t be evil”).

Both Google and Meta (META) control 70% of the advertising market between them, which is inherently a slow-growing market, expanding at 5% a year at best. (META)’s growth has slowed dramatically, while it has reversed at (GOOG).

He is a big fan of (AMD), one of his biggest positions, which is undervalued relative to the other chip companies. They out-executed Intel (INTC) over the last five years and should pass it over the next five years.

He has raised value tech stocks from 15% to 30% of his portfolio. Apple used to be one of these. Semiconductor companies today also fall into this category. Samsung with 40% margins in its memory business is a good example. Selling for 10X earnings is ridiculously cheap. It is just a matter of time before semiconductors get rerated too.

He was an early owner of Tesla (TSLA) back in the nail-biting days when it was constantly running out of cash. Now they have the opposite problem, using their easy access to cash through new share issues as a weapon to fight off the other EV startups. Tesla is doing to Detroit what Apple did to the cell phone companies, redefining the car.

Its stock is overvalued now but will become much more profitable than people realize. They also are starting to extract services revenues from their cars, like Apple has. Tesla will grow revenues by 30%-50% a year for the next two or three years. They should sell several millions of the new small SUV Model Y. Most other companies bringing EVs will fall on their faces.

EVs are a big factor in climate change, even in China, the world’s biggest polluter. In Europe, they are legislating gasoline cars out of existence. If you can make money building cars in Fremont, CA, you can make a fortune building them in China.

Tech valuations are high, there is no doubt about it. But interest rates are much lower by comparison. The Fed is forcing people to buy stocks, enabling these companies to evolve even faster.

Tech stocks have a lot more things going for them than against them. The customers keep coming back for more.

Needless to say, the above stocks should make up your short list for LEAPS to buy at the coming market bottom.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/09/oakland-fire-dept.png408608Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-08-02 10:02:162022-08-02 12:34:10An Insider’s Guide to the Next Decade of Tech Investment

(FACETIME ON COMPUTER NOT WHAT IT ONCE WAS) (XOM), (NFLX), (ZM)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-06-01 15:04:012022-06-01 18:19:53June 1, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.