The AI war is heating up thanks to the new kid on the block Cognition AI.

They have certainly one-upped the competition.

Cognition AI’s team has a new type of technology called Devin.

Devin is a software development assistant in the vein of Copilot, which was built by GitHub, Microsoft, and OpenAI, but, like, a next-level software development assistant.

Instead of just offering coding suggestions and auto-completing some tasks, Devin can take on and finish an entire software project on its own.

The technology can even create websites within seconds. No coder will ever be able to compete with this.

As it works, Devin shows all the tasks it’s performing and finds and fixes bugs on its own as it tests the code being written.

The founders of Cognition AI are Scott Wu, its chief executive officer; Steven Hao, the chief technology officer; and Walden Yan, the chief product officer.

One of the big breakthroughs claims they can force a computer to reason with stunning efficiency.

Reasoning in AI-speak means that a system can go beyond predicting the next word in a sentence or the next snippet in a line of code, toward something more akin to thinking and rationalizing its way around problems.

It’s possible to give Devin jobs to do with natural language commands, and it will set off and accomplish them.

As Devin works, it tells you about its plan and then displays the commands and code it’s using. If something doesn’t look quite right, you can give the AI a prompt to go fix the issue, and Devin will incorporate the feedback midstream.

Most current AI systems go haywire soon after it veers away from the script. Off-schedule variables usually are hard for current AI to stomach.

What does this mean for the tech sector and the future of work?

A naïve person would say this will free developers from the drudgery of mundane tasks and let them focus on more creative jobs.

However, the smart crowd understands this will be a great excuse to cut staffing costs to the bone.

This will allow many non-coders to join in the game and totally bypass going through software developers who more often than not lack common sense.

Remember when the Chinese consumer went from cash to paying with QR codes via smartphones, they skipped over the credit card and America is still stuck on the plastic card.

People will be able to create 1-man tech companies and do the job of 100 people in no time.

This certainly is a winner-takes-all scenario and the mid-term future is quite bleak for software developers.

It’s looking highly likely and I would say ironic that the software developers creating AI are about to do a disservice to their colleagues and rid the economy of 99% of software developers.

Of course, AI isn’t that good yet, but the path is being laid and the countdown has been initiated.

With a few years of furious development of high-quality AI, this will usher in a golden age of tech stocks, because they will finally be able to fire most of the staff.

The advancement of AI can guarantee higher tech shares no matter what and many might say stocks like Nvidia are cheap because this trend is still in the early innings.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-13 14:02:472024-03-13 16:18:20Cognition AI Is The Talk Of The Town

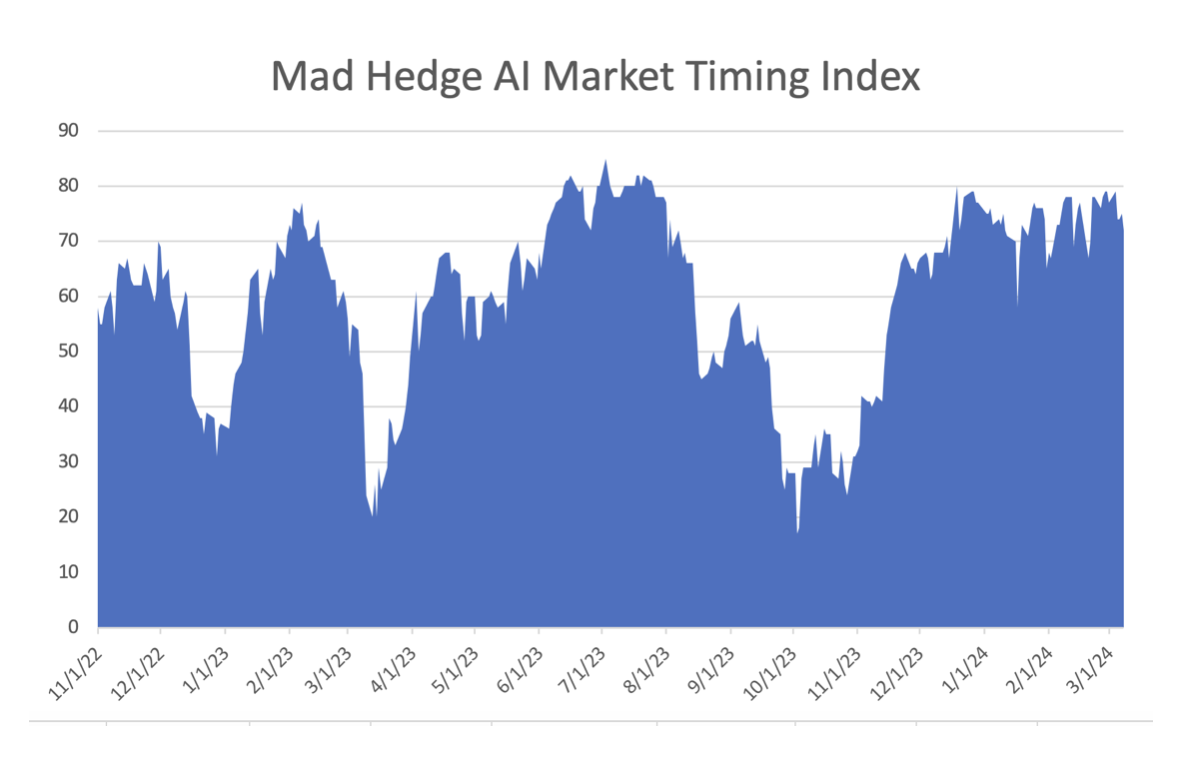

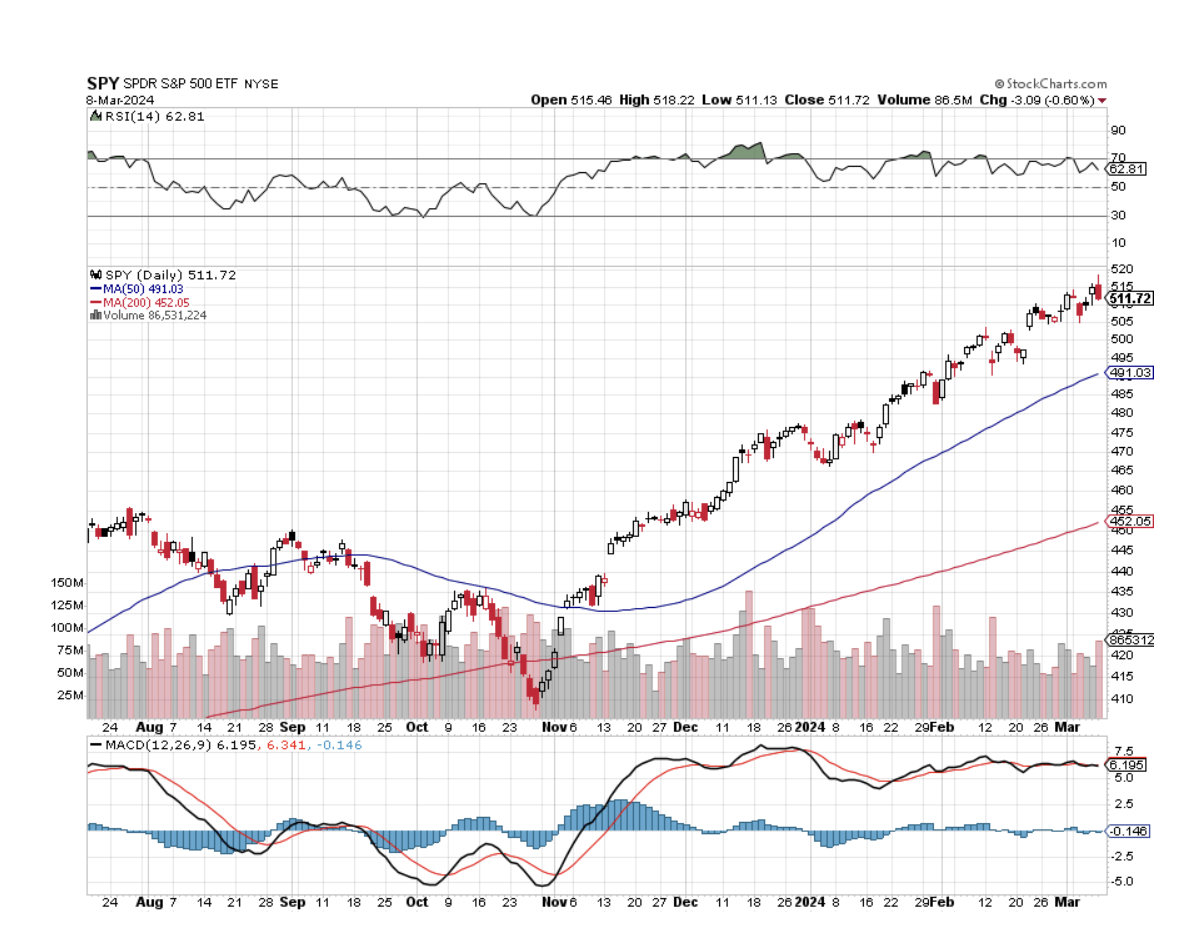

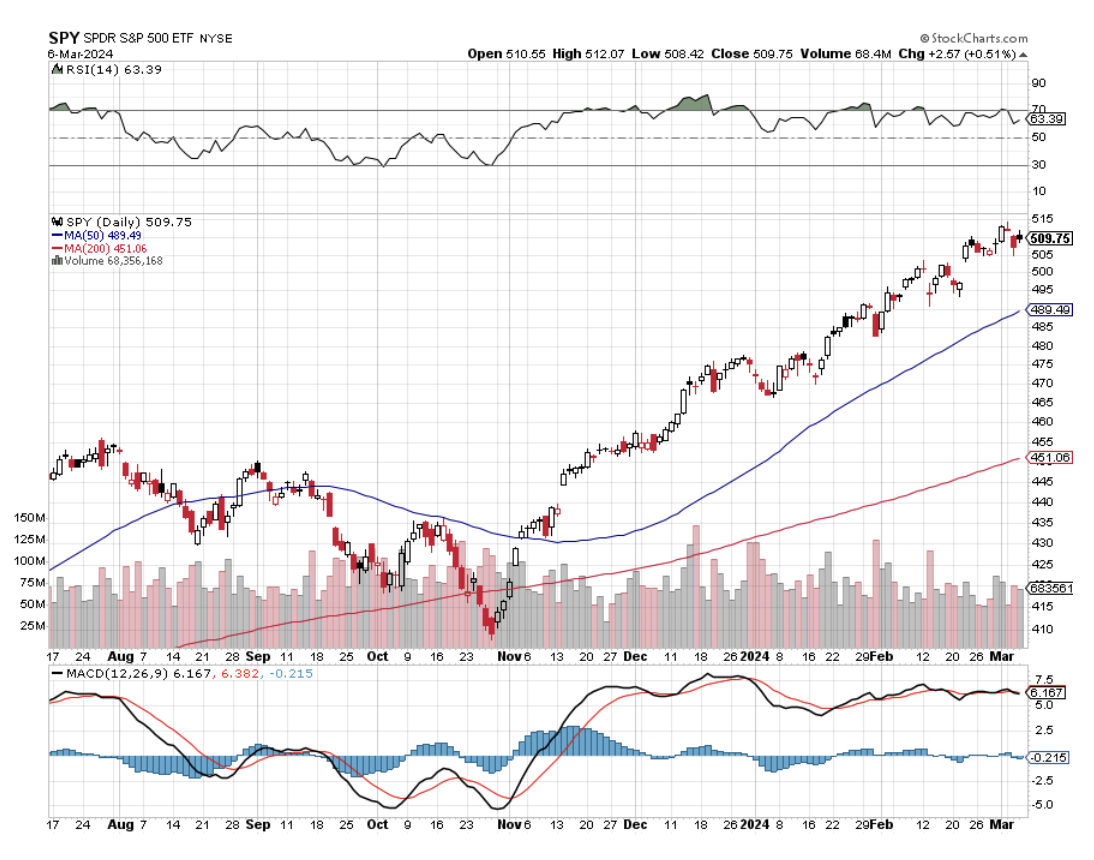

(The Mad MARCH traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HIGHER HIGHS)

(NVDA), (META), (IWM), (AMZN), (RIVN), (SNOW), (GLD), (GOLD), (NEM), (FXI), DELL), (AAPL), (TSLA), (CCJ), ($NIKK), (USO), (GOLD)

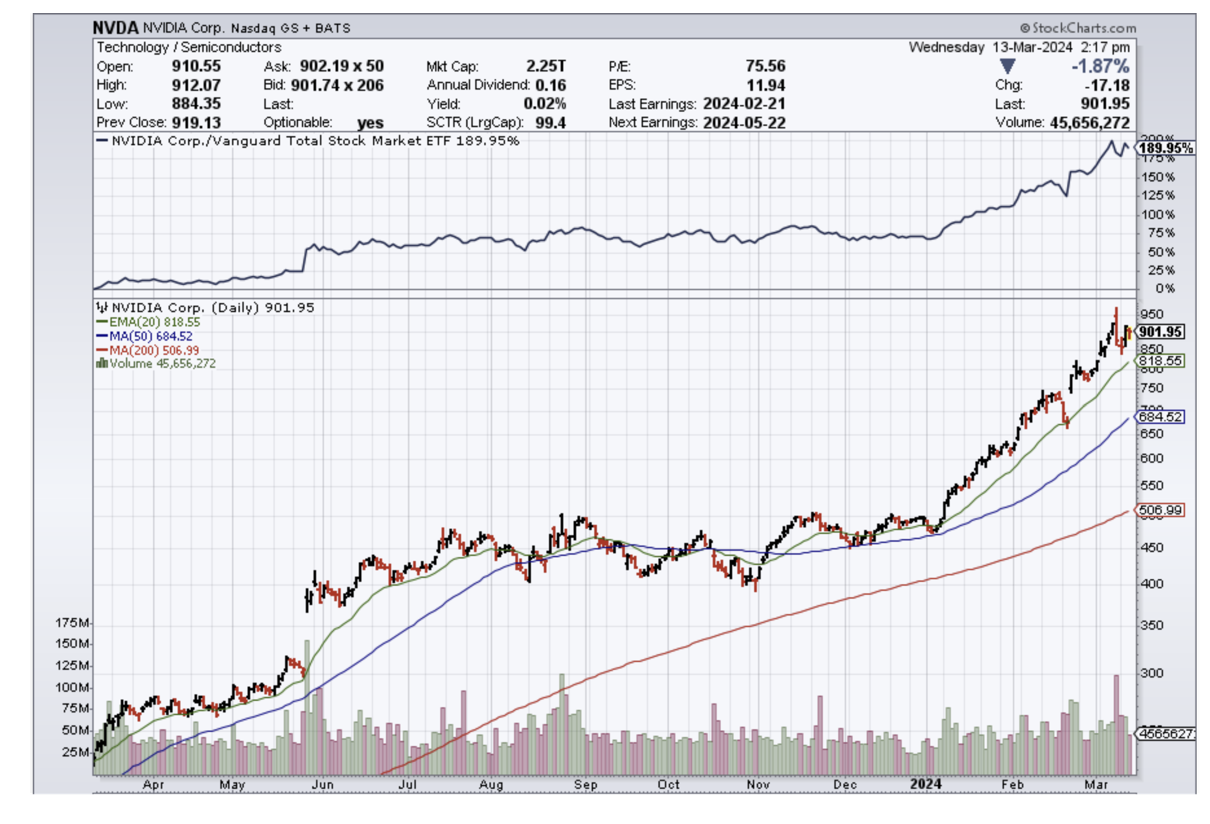

I was all ready to write another hyper-bullish report for the week. That was at least until noon EST on Friday. That’s when NVIDIA (NVDA) Peaked at $955 and then free fell $100 to $855. New all-time and then a new intraday low on huge volume and that is the textbook definition of a market top.

Not that we should be complaining. At the high, (NVDA) was up an unimaginable 105% so far this year. I spent my week buying back short put options for 50 cents that I initially sold for $20. With a quarterly quadruple witching due this Friday, anything can happen.

By the end of February, more than half of all analyst 2024 yearend targets were met. The response was a rush to raise yearend targets, triggering the current melt-up.

It always ends in tears.

And I’m about to tell you something that you will absolutely love to hear. Lower interest rates dramatically increase corporate stock buybacks, already set at $1.25 trillion for 2024. That’s because of the lower cost of capital.

What do more share buybacks automatically bring? High stock prices, especially for large positive cash flow companies like big tech.

As much as the permabears hate to admit it, good news really is good news.

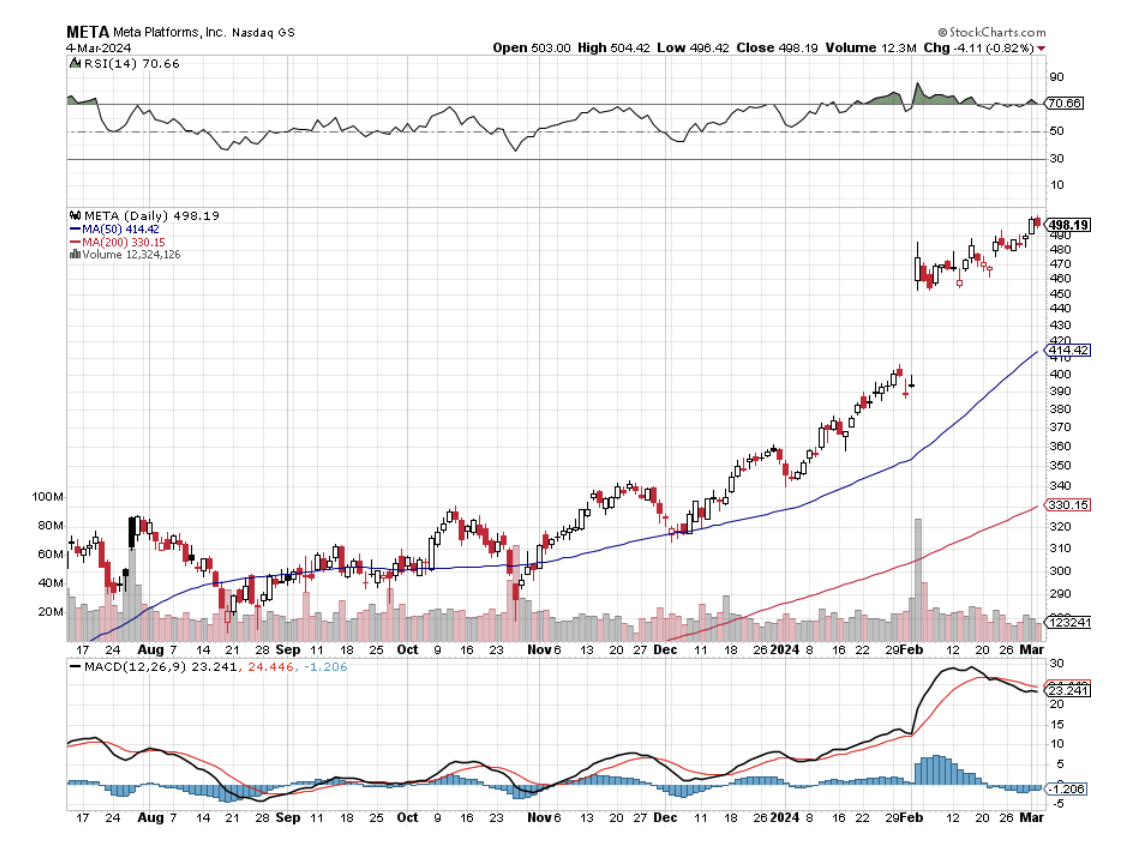

With all of the media obsession with NVIDIA (NVDA), my largest holding, and Meta (META), the fact is that the rally is broadening out. More than half of all industrial stocks are trading at all-time highs. Long-forgotten small caps (IWM) are also approaching 2021 all-time highs.

Going into this week managers were either overweight big tech and extremely nervous or out of big tech and kicking themselves. The urge to rotate is strong. But your standby rotation sectors, industrials, biotech, and banking have also seen big moves.

Which brings us to the subject of gold (GLD).

After a tedious one-year sideways consolidation, the barbarous relic blasted out to the upside above $2,200 an ounce, a new all-time high. After soaking up as much gold as they could over the past decade, China and Russia have finally taken the gold market net short, which is why we saw such dramatic price action.

With interest rates in the US soon to fall, the opportunity cost of owning non-yielding gold is about to shrink. That will cut the knees out from under the US dollar prompting a stampede into precious metals and Bitcoin.

Except this time, it’s different.

Gold miners usually outperform the yellow metal by four to one to the upside. Not so this time. Barrick Gold (GOLD) and Newmont Mining (NEM) were barely able to keep pace with the barbarous relic. That’s because inflation has boosted their costs and cut profit margins. After all, they are stock first and gold plays second.

Still, if gold reaches my $3,000 target in 2025 the LEAPS I sent out for (GOLD) last June should easily hit its maximum profit point of 298%.

That other weak dollar play, oil (USO) may not deliver the joys of past cycles and may in fact be trapped in a fairly narrow $60-$80 range. The futures markets are saying that the price of Texas tea will be lower in a year.

The US is now the world’s top oil producer at 13 million barrels/day and that is rising (thanks to enormously generous tax breaks), capping prices. Non-OPEC+ production is increasing, especially from Brazil and Canada. China, the world’s largest oil importer is missing in action. But low inventories, especially at the American Strategic Petroleum Reserve, are preventing a crash as well. Shale production is growing.

Still, even a $20 rally can have a dramatic impact on the share prices of the big US producers, like Exxon (XOM) and Occidental Petroleum (OXY), some 25% of which is now owned by Warren Buffet. Even without some sexy price action, this sector pays some of the highest dividend yields in the markets.

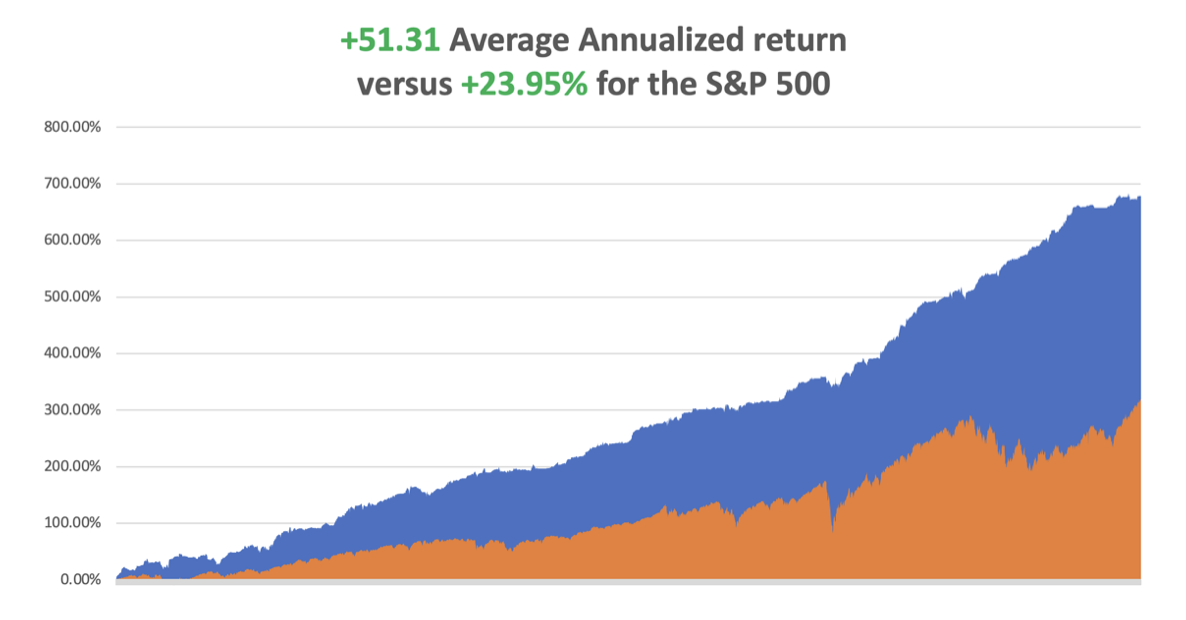

In February we closed up +7.42%. So far in March, we are up +0.70%. My 2024 year-to-date performance is at +3.21%. The S&P 500 (SPY) is up +7.11% so far in 2024. My trailing one-year return reached +54.28% versus +40.94% for the S&P 500.

That brings my 16-year total return to +689.74%. My average annualized return has recovered to +52.05%.

Some 63 of my 70 trades last year were profitable in 2023. Some 11 of 15 trades have been profitable so far in 2024.

I used the ballistic move in (NVDA) to take profits in my double long there. I am maintaining longs in (AMZN) and Snowflake (SNOW). I am both long and short the bond market (TLT) and I am 60% in cash given the elevated level of the stock markets.

Nonfarm Payroll Report Rose 275,000 in February. The Headline Unemployment Rate rose to 3.9%, a two-year high. The report illustrates a labor market that is gradually downshifting, with more moderate job and pay gains that suggest the economy will keep expanding without much risk of a reacceleration in inflation. These are very Fed friendly numbers.

JOLTS Job Openings Report Rises by 140,000 to 8,890,000, less than expected. Leisure and hospitality led with 41,000 new jobs, construction added 28,000 and trade, transportation and utilities contributed 24,000. Growth was concentrated among larger companies, as establishments with fewer than 50 employees contributed just 13,000 to the total.

Rivian Shares Soar, on news it is halting plans to build a new $2.25 billion factory in Georgia, an abrupt reversal aimed at cutting costs while the company prepares to launch a cheaper electric vehicle. Shifting planned production of the forthcoming R2 model to an existing facility in Illinois will allow Rivian to begin deliveries in the first half of 2026, earlier than expected. Buy (RIVN) on dips.

New York Community Bancorp Bailed Out, with a cash infusion led by former Treasury secretary Steve Mnuchin. The shares soared from $2 to $3.41. That takes the heat off the sector….until the next one. The US is shrinking from 4236 banks to only six banks. Who says politics doesn’t pay?

Europe Moves Towards Interest Rate Cuts, igniting a global bond market rally. Staff projections now see economic growth of 0.6% in 2024, from a previous forecast of 0.8%. They presented a more positive picture of inflation, with the forecast for the year brought to an average 2.3% from 2.7%. Market bets increased on rate cuts taking place as early as June, with the euro trading 0.35% lower against the British pound following the news.

Beige Book Comes in Moderate, saying "labor market tightness eased further," in February but noted "difficulties persisted attracting workers for highly skilled positions." The Beige Book is a review of economic conditions across all 12 Fed districts. Fed Chair Jerome Powell told Congress on Wednesday that the U.S central bank expected "inflation to come down, the economy to keep growing," but shied away from committing to any timetable for interest rate cuts.

China Targets 5% Growth for 2024, but nobody buys it for a second. A covid hangover, residential real estate crisis triggering a financial crisis, and constant invasion threats over Taiwan, make this target a pipe dream. Avoid (FXI) and all Middle Kingdom plays.

Gold Hits New All-Time High, at $2,141 an ounce on expectations of imminent rate cuts by the Fed. Gold, often used as a safe store of value during times of political and financial uncertainty, has climbed over $300 dollars since the start of the Israel-Hamas war. Buy (GLD), (GOLD), and (NEM) on dips.

Dell (DELL) Becomes an AI Stock, sending the shares up 47% in a Day. That’s been changing over the past year, as Dell has been reporting strong orders of servers designed to power generative AI workloads—many of which use chips supplied by AI kingmaker Nvidia. The company’s fourth quarter results convinced any doubters. Can Apple (AAPL) do the same?

Tesla Plunges on Poor China Sales, down $14.50 on sales data dimmed the outlook for Tesla's global deliveries, at a time when the top EV maker is battling a decline in demand and is weighed down by a lack of entry-level vehicles and the age of its product line-up. Not the time to be in EVs or solar. Buy (TSLA) on bigger dip.

US National Debt is Rising by $1 Trillion Every 100 Days. A trillion here, a trillion there, sooner or later that adds up to a lot of money. Eventually, someone is going to have to do something about this. The US national debt stands at $34.5 trillion, or $104,545 per person.

The Uranium Shortage is Getting Extreme, with yellow cake up 112% in a year. Owners of left-for-dead uranium mines are restarting operations to capitalize on rising demand for the nuclear fuel. Most of those American mines were idled in the aftermath of Fukushima when uranium prices crashed and countries like Germany and Japan initiated plans to phase out nuclear reactors. Now, with governments turning to nuclear power to meet emissions targets and top uranium producers struggling to satisfy demand, prices of the silvery-white metal are surging. Buy (Cameco (CCJ) on dips.

Japan’s Nikkei ($NIKK) Tops 40,000, a new 34-year high. The ultra-weak Japanese economy is giving the economy there a free lunch, but better hedge your currency exposure. Good thing I missed a dead market for 34 years.

NVIDIA Replaces Tesla as Top Traded Stock, with volumes migrating to the options market as well. Blockbuster profits are catnip for traders, while EV price wars aren’t. Tesla is down 52% from its all-time high two years ago and is one of the biggest percentage decliners in the Nasdaq 100 Index this year.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, March 11 at 7:00 AM EST, the Consumer Inflation Expectations are announced.

On Tuesday, March 12 at 8:30 AM, Inflation Rate for February is released.

On Wednesday, March 13 at 2:00 PM, MBA Mortgage Applications are published

On Thursday, March 14 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index.

On Friday, March 15 at 2:30 PM, the University of Michigan Consumer Sentiment is published. At 2:00 PM the Baker Hughes Rig Count is printed.

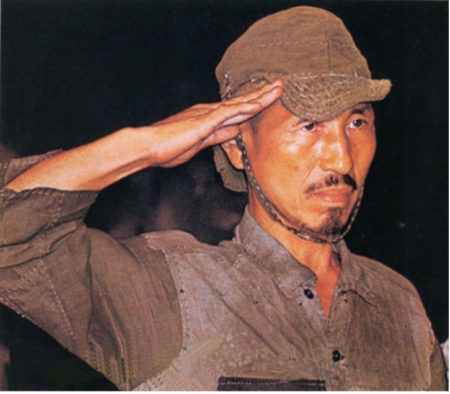

As for me, I have met many interesting people over a half-century of interviews, but it is tough to beat Corporal Hiroshi Onoda of the Japanese Army, the last man to surrender in WWII.

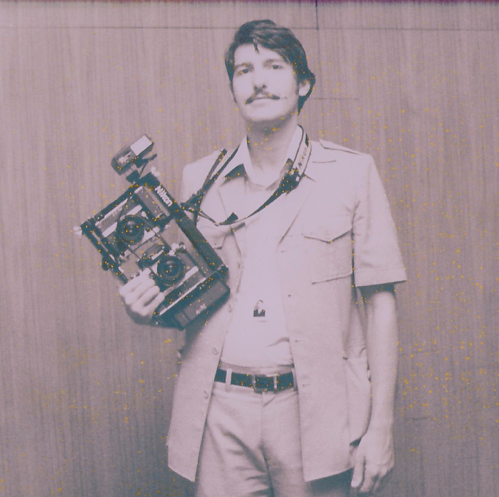

I had heard of Onoda while working as a foreign correspondent in Tokyo. So, I convinced my boss at The Economist magazine in London that it was time to do a special report on the Philippines and interview President Ferdinand Marcos. That accomplished, I headed for Lubang island where Onoda was said to be hiding, taking a launch from the main island of Luzon.

I hiked to the top of the island in the blazing heat, consuming two full army canteens of water (plastic bottles hadn’t been invented yet). No luck. But I had a strange feeling that someone was watching me.

When the Philippines fell in 1945, Onoda’s commanding officer ordered the remaining men to fight on to the last man. Four stayed behind, continuing a 30-year war.

As a massive American military presence and growing international trade raised Philippine standards of living, the locals eventually were able to buy their own guns and kill off Onoda’s companions one by one. By 1972 he was alone, but he kept fighting.

The Japanese government knew about Onoda from the 1950s onward and made every effort to bring him back. They hired search crews, tracking dogs, and even helicopters with loudspeakers, but to no avail. Frustrated, they left a one-year supply of the main Tokyo newspaper and a stockpile of food and returned to Japan. This continued for 20 years.

Onoda read the papers with great interest, believing some parts but distrusting others. His worldview became increasingly bizarre. He learned of the enormous exports of Japanese automobiles to the US, so he concluded that while still at war, the two countries were conducting trade.

But when he came to the classified ads, he found the salaries wildly out of touch with reality. Lowly secretaries were earning an incredible 50,000 yen a year, while a salesman could earn an obscene 200,000 yen.

Before the war, there was one Japanese yen to the US dollar. In the hyperinflation that followed the yen fell to 800, and then only recovered to 360. Onoda took this as proof that all the newspapers were faked by the clueless Americans who had no idea of true Japanese salary levels.

So he kept fighting. By 1974 he had killed 17 Philippino civilians.

After I left Lubang island, a Japanese hippy named Norio Suzuki with long hair, beads, and sandals followed me, also looking for Onoda. Onoda tracked him as he had me but was so shocked by his appearance that he decided not to kill him. The hippy spent two days with Onoda explaining the modern world.

Then Suzuki finally asked the obvious question: what would it take to get Onoda to surrender? Onoda said it was very simple, a direct order from his commanding officer. Suzuki made a beeline straight for the Japanese embassy in Manila and the wheels started turning.

A nationwide search was conducted to find Onoda’s last commanding officer and a doddering 80-year-old was turned up working in an obscure bookstore. Then the government custom-tailored a prewar Imperial Japanese Army uniform and flew him down to the Philippines.

The man gave the order and Onoda handed over his samurai sword and rifle, or at least what was left of it. Rats had eaten most of the wooden parts. You can watch the surrender ceremony by clicking here on YouTube.

When Onoda returned to Japan, he was a sensation. He displayed prewar mannerisms and values like filial piety and emperor worship that had been long forgotten. Emperor Hirohito was still alive.

When I finally interviewed him, Onoda was sympathetic. I had by then been trained in Bushido at karate school and displayed the appropriate level of humility, deference, mannerisms, and reference.

I asked why he didn’t shoot me. He said that after fighting for 30 years he only had a few shells left and wanted to save them for someone more important.

Onoda didn’t last long in the modern Japan, as he could no longer tolerate modern materialism and cold winters. He moved to Brazil to start a school to teach prewar values and survival skills where the weather was similar to that of the Philippines. Onoda died in 2014 at the age of 91. A diet of coconuts and rats had extended his life beyond that of most individuals.

Onoda wasn’t actually the last Japanese to surrender in WWII. I discovered an entire Japanese division in 1975 that had retreated from China into Laos and just blended in with the population. They were prized for their education and hard work and married well.

During the 1990’s a Japanese was discovered in Siberia. He was released locally at the end of the war, got a job, married a Russian woman, and forgot how to speak Japanese. But Onoda was the last to stop fighting.

The Onoda story reminds me of the fact that journalists learn very early in their careers. You can provide all the facts in the world to some people. But if they conflict with their own deeply held beliefs, they won’t buy them for a second.

Hiro Onoda Surrenders

Budding Journalist John Thomas

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-11 09:02:232024-03-11 12:13:02The Market Outlook for the Week Ahead, or Higher Highs

Below please find subscribers’ Q&A for the March 6 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: With your projections of the Dow going to $240,000 in 10 years, would it be wise to invest in the Dow?

A: The Dow is just an indicator that everybody understands and is familiar with what the media uses. What I tell people to do is if you are not an aggressive person, put half your money in the S&P 500 (SPX), which is getting most of the gains, and half in the technology (QQQ), which is getting all of the gains. If you're an aggressive person, say in your twenties, thirties, or forties, then you put all of your money in the Invesco QQQ NASDAQ Trust (QQQ) because you'll live long enough to survive the inevitable downturns.

Q: What should we do now with Palo Alto Networks (PANW)?

A: Keep it. It’s a fantastic long-term company. This is a rare opportunity to get in on the long side, as this is a company that I think could double over the next 3 to 5 years. Hacking is never going out of style and now they have AI. The selloff was caused by a major platform upgrade which may cause profits to dip for a quarter. That’s now in the price.

Q: With the successful launch of Bitcoin, should we allocate 5% or 10% of our portfolio to Bitcoin?

A: Only if you can handle a 90% decline at any time without warning because that's exactly what it did in 2021. Calling it a store of value is a fantasy. You also still have big theft issues with Bitcoin. You don't have theft issues if you have all your money at Morgan Stanley, Goldman Sachs, Merrill Lynch, and so on, so there is a security issue (with Bitcoin). The only way to bypass the security issues is to have a hot wallet, and the only way to have a hot wallet is to be a computer programmer yourself or have a degree in computer science—so it's not for most people. If you can navigate all of that, then maybe; but again, nobody knows when the next 90% decline is going to come. By the way, if I can find stocks with Mad Hedge Fund Trader that go up faster than Bitcoin, I'd much rather own the stocks, because at least I know what they make.

Q: Is Snowflake (SNOW) a buy here at $155?

A: Absolutely. Another great cybersecurity database company. But if we drop to $155, we're going to stop out of the front month call spread and try to buy it back lower down.

Q: Do you think it's wise to sell the semiconductor stocks now and buy them back lower down, and pay the taxes?

A: Probably not. They are really the most volatile sector in the market. If you sell now, it's unlikely you'll be able to pick up the next bottom and get back in, and you have to pay the taxes. So it's probably better just to keep a core long-term position in the semis, especially Nvidia (NVDA); and if it drops 200 points, just buy more. That's what I'm doing. I'm keeping all of my Nvidia LEAPS. All my call spreads and short put positions are about to expire at max profit, and I even have a little bit of stock that I'm keeping. So I think Nvidia goes to $1,000 at one point and now, the forecast of $1,400 is out there. So as Nvidia goes, so goes the entire rest of the semiconductor industry.

Q: You're only 30% invested. Are you looking for a pullback, or are you just waiting for new opportunities to appear?

A: Yes and Yes. I'm waiting for a fantastic company to come up with conservative guidance, which these days means an immediate 20 to 25% sell-off. That is your entry point for these good companies. That's how we got into Palo Alto Networks (PANW), and that's how we got into Snowflake (SNOW). In an extremely overbought market, those are your only opportunities until the market generally sells off or until the domestic plays finally start to take off, and we got the first hints of that last week.

Q: What is your view on junior gold mining stocks?

A: They are a buy here, absolutely, but you get enough volatility in the majors that you don't need to bother with the minors—that's always been my view. Because minors go out of business, they close mines, they don't find gold. A lot of minors have stocks go up on the possibility of gold being found, whereas the majors like Barrick Gold (GOLD) and Newmont Mining (NEM) actually have the gold, and it's just an industrial process of mining it. You know the minors, the juniors, are extremely speculative and high-risk, and that's why most of them are listed in Canada. They can't get a US listing. So that's enough of a tell for me to stay away.

Q: I just realized I have the wrong expiration date on my Amazon (AMZN) spread. Should I exit immediately?

A: What I would do is exit what you have and then wait for another down day on Amazon, and then put it back on. That's the way to deal with that one. The answer to all mistakes is to exit immediately. That's an automatic rule at Morgan Stanley; if you don't do that, you get fired. Or come up with a new set of logic as to why you own this position, which has been done by more than a few traders, I imagine.

Q: Would you be willing to be a Boeing 737 Max passenger right now or ever?

A: Yes! If you don't fly Boeings (BA), your life is suddenly very narrow and limited because you’re stuck on the ground. Boeing is the biggest-selling airplane in the world, and most fleets are made of Boeings. However, I'm a pilot, so if anything goes wrong I can run up front and take control, or at least tell the pilot what to do. I also have 25 parachute jumps, if they're handing those out in first class. So remember, every airplane without engines is a glider and I can land a glider anywhere. The company has major problems to sort out until it becomes a “BUY”.

Q: I cannot get into the (TLT) trade to save my life. Is the (TLT) April $89-$92 vertical bull call debit spread pushing the risk limits?

A: Yes. I would walk away from the trade and wait for a better entry point rather than chase.The whole fixed-income space has flipped from the bid side to the offered side, meaning we've gone from net sellers to net buyers. All asset classes have done that; you're seeing that in gold, silver, and even uranium. All the REITs are having a fantastic week. All interest rate plays are now being bid, and it's hard to buy stuff when things are being bid.

Q: What's it like being 6’4” and living in Japan?

A: Well, I did knock myself out a couple of times, banging myself on the door. You get used to bowing a lot, but bowing is a part of the culture in Japan. If you're watching the new Hulu miniseries, Shogun, you would know that. Once I was working for Sony and I was late for work, so I was running up the stairs, and they had a steel lintel to their door, and I just ran bang into that and knocked myself out. The Sony people thought, “Oh my gosh, we just killed a foreigner!” So yes, it was hard. The only clothes I could buy in Japan for ten years were belts and ties. I had to fly to Hong Kong and had everything else custom-made in those days.

Q: What's your opinion of Masters of the Air?

A: I absolutely love it. It's heartbreaking to watch. I knew a lot of guys who were there, and I was one of the last people trained on how to fly a Boeing B-17 Flying Fortress. Anybody who watched Masters of the Air with me gets to watch it with someone who is one of the last living people who rated on a B-17 as a pilot.

Q: Are we in a liquidity bubble right now?

A: Yes, we are, and boy, I love every minute of it. But we're not in the year 2000 in a liquidity bubble, we're in 1995 just getting started. And the profits from AI are just getting started which is what's creating this endless liquidity that people are seeing now.

Q: What should I buy the dip in Tesla (TSLA)?

A: There's no downside target for Tesla right now. We just have to wait for the meltdown in demand to finish, and who knows where that is. But with BYD entering the market, Tesla is definitely going to get more competition in emerging markets—that's where BYD is selling the cars now. I also understand they're selling them in Australia.

Q: How much longer can tech stocks keep rising?

A: 5 to 10 more years, but we are way overdue for some kind of pullback.

Q: What are your thoughts on Apple's (APPL) weakness?

A: Apple has become that great backward-looking company. It could drop to $160 or even $140, then we’ll be taking a serious look at some call spreads and LEAPS. You just wait. In four months when they announce their next batch of new products suddenly, they’ll become an AI company and recover the $200 level in no time.

Q: Should I dive into Coinbase (COIN)?

A: Absolutely not on pain of death! It's made its move. You're better off buying Nvidia (NVDA) at that kind of inclination because at least you know what they make.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

For years, I have been predicting that a new Golden Age was setting up for America, a repeat of the Roaring Twenties. The response I received was that I was a permabull, a nut job, or a conman simply trying to sell more newsletters.

Now some strategists are finally starting to agree with me. They too are recognizing that a ganging up of three generations of investment preferences will combine to drive markets higher during the 2020s, much higher.

How high are we talking? How about a Dow Average of 240,000 by 2035, up another 515% from here? That is a 40-fold gain from the March 2009 bottom.

It’s all about demographics, which are creating an epic structural shortage of stocks. I’m talking about the 80 million Baby Boomers, 65 million from Generation X, and now 85 million Millennials. Add the three generations together and you end up with a staggering 230 million investors chasing stocks, the most in history, perhaps by a factor of two.

Oh, and by the way, the number of shares out there to buy is actually shrinking, thanks to a record $1 trillion or more in corporate stock buybacks for the past decade.

I’m not talking pie-in-the-sky stuff here. Such ballistic moves have happened many times in history. And I am not talking about the 17th-century tulip bubble. They have happened in my lifetime. From August 1982 until April 2000, the Dow Average rose, you guessed it, exactly 20 times, from 600 to 12,000, when the Dotcom bubble popped.

What have the Millennials been buying? I know many, like my kids, their friends, and the many new Millennials who have recently been subscribing to the Diary of a Mad Hedge Fund Trader. Yes, it seems you can learn new tricks from an old dog. But they are a different kind of investor.

Like all of us, they buy companies they know, work for, and are comfortable with. During my dad’s generation that meant loading your portfolio with US Steel (X), IBM (IBM), and General Motors (GM).

For my generation, that meant buying Microsoft (MSFT), Intel (INTC), and Dell Computer (DELL).

For Millennials that means focusing on NVIDIA (NVDA), Netflix (NFLX), Amazon (AMZN), Meta (META), and Alphabet (GOOGL). Oh, and they like Bitcoin too (BITO).

That’s why the Magnificent Seven account for all of the past year’s monster gains.

There is another gale force tailwind pushing stocks up. The enormous profits created by artificial intelligence are essentially replacing the Federal Reserve as an unlimited source of liquidity. If you missed the quantitative easing and the free money of the 2010s, you get another pass at the brass ring. But you have heard me talk about this before so I won’t bore you.

There is one catch to this hyper-bullish scenario. Somewhere on the way to the next market apex at Dow 240,000, we need to squeeze in a recession. Bear markets in stocks historically precede recessions by an average of seven months. But for the time being, it looks like smooth sailing.

When I get a better read on precise dates and market levels, you’ll be the first to know.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/03/john-thomas-snow.jpg285259april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-06 09:02:172024-03-06 10:09:22Why the Dow is Going to 240,000

Sure, the narrative out there is that generative AI will transform the technology sector and the companies that coalesce around it.

That doesn’t always mean it will be great for everyone.

Many jobs can be mundane and boring.

AI is supposed to solve all that by unlocking time for these workers to do other tasks.

However, one trend that is picking up speed that could turn into a runaway freight train is the evolution of AI destroying most of the human job market.

It’s happening faster than people think.

If everyone loses their jobs except for a handful of CEOs running a company with AI, who will pay rent to small or corporate landlords?

Who will partake in a trip to a sports bar when these patrons lack salaries that are replaced by AI.

The next battleground of AI job removal is now reaching up to the middle manager echelon.

Confidence among middle-managers dropped to its worst-ever reading in February, pushing a broader index of US employee sentiment down to a record low.

The group’s confidence is now similar to that of entry-level workers, which fell last month to the lowest in seven years.

Decades after automation began taking and transforming manufacturing jobs, artificial intelligence is coming for the corporate management.

The list of white-collar layoffs is growing almost daily and includes jobs cuts at Google, Duolingo and UPS in recent weeks.

While the total number of jobs directly lost to generative AI remains low, some of these companies and others have linked cuts to new productivity-boosting technologies such as machine learning and other AI applications.

Generative AI could soon upend a much bigger share of white-collar jobs, including middle and high-level managers,

Generative AI speeds up routine tasks or make predictions by recognizing data patterns.

It has the power to create content and synthesize ideas—in essence, the kind of knowledge work millions of people now do behind computers.

Across all ranks, employee confidence fell to 45.1%, the lowest in data back to 2016.

Middle managers have to both direct more junior employees and answer to the senior ranks, making the position uniquely prone to burnout in the corporate ladder.

Tech firms like Meta and Google zoned in on those positions for cuts last year.

In announcing the job cuts, the companies cited similar themes around productivity and efficiency.

At some big tech firms, that can be gauged by how many people work under you, providing an incentive to overdo the staffing levels.

Companies that did just that are increasingly reducing staff and driving confidence down with it.

Although highly positive for revenue estimates, human workers will need to adjust to a modern cutthroat working environment where they need to do more and get paid less in technology.

The ironic thing about this is that the very technology they lusted over is the same technology putting the same workers out of a job.

Better be careful what you wish!

At a stock market level, this is highly positive and will lead to higher shares in tech companies like Nvidia and Super Micro computers.

Remember that wages are usually the highest expense and reducing them will almost always result in higher share prices.

It’s good that low confidence doesn’t affect the execution or existence of AI.

This is significantly bullish tech stocks short and long term and I expect every quarterly earnings transcript to talk about reducing staffing levels and higher efficiency.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-04 14:02:562024-03-04 14:26:21Middle Managers On The Chopping Block

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHO NEEDS THE FED?

(AAPL), (TSLA), (AAPL), (GOOGL), (MSFT), (MSFT), (BRK/B), (BA), (JPM), (BA), (C), (SNOW), (NVDA)

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.