OpenAI’s splash into AI was the secret sauce as to why tech stocks have gone parabolic in 2023.

The platform achieved a remarkable milestone by amassing 100 million monthly active users quite early on, setting a record for the fastest-growing user base.

With ChatGPT’s widespread absorption, OpenAI has been looked at as the savior for revenue models in Silicon Valley.

However, this period of AI enthusiasm has proved to be short-lived, as the technology experiences its first real pullback.

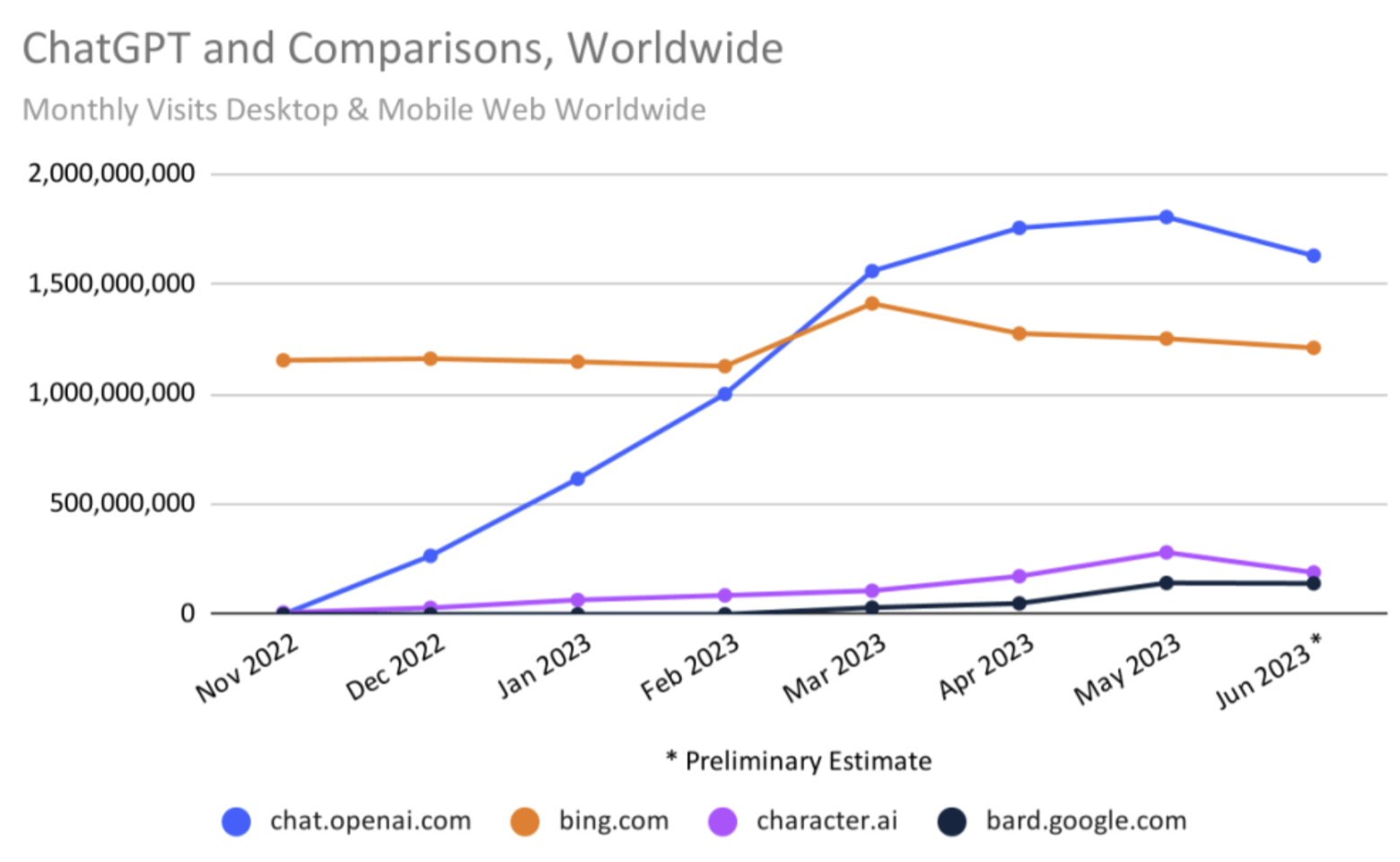

Based on the latest data, ChatGPT experienced a 9.7% decrease in desktop and mobile web traffic during June. The site also saw a decline of 5.7% in unique visitors.

This was followed by an 8.5% decrease in the average time users spent on the site. In the United States, the month-on-month traffic decline for the website was recorded at 10.3%.

The downtrend in traffic is quite surprising considering that groundbreaking new technologies which are still in their honeymoon phases never report any decrease in eyeballs whatsoever.

There's been a lot of buzz around artificial intelligence since ChatGPT was released seven months ago. About a month and a half before the chatbot was released to the public, the stock market bottomed in a bear market around the middle of October.

I am not saying the bottom will fall out of tech stocks, but the gaps up will probably cool down in the short term.

Take example one stock that has performed spectacularly – Nvidia (NVDA).

They have even managed to achieve this against a backdrop of challenging macroeconomic headwinds and a hawkish Federal Reserve.

The drop in ChatGPT interest is a warning sign that the beautiful girl has hit the wall.

It can’t be as simple as investors cheering on AI from the sidelines and then stocks go magically up. It’s not that easy.

The inherent technology needs evidence of outperformance and cannot lack substance.

A significant majority, comprising 61%, of ChatGPT’s user base consists of individuals from Generation Z.

This AI tool has gained considerable popularity for its educational applications.

For example, according to a research report, respondents reported using ChatGPT for educational purposes, with 33% utilizing it for educational assistance. 18% rely on it to comprehend complex concepts, and 15% use it to acquire new skills.

Investors need to understand that sliding interest in ChatGPT could be a catalyst for the AI bubble to lose air.

At the moment, AI's risks are as massive as its potential. We won't know until ten years later whether AI's impact is more akin to the internet or the Google Glass.

There are also other issues. Sam Altman, chief executive at OpenAI, has described the cost of running the services as “eye-watering.”

ChatGPT is free to use but also provides a premium subscription, where users can pay $20 a month to access OpenAI’s more advanced model, GPT-4.

Some 1.5 million people have signed up for the subscription, but the other tens of millions aren’t on board yet. For many people, it’s not worth paying for yet.

OpenAI has projected $200 million in revenue this year.

I believe it is time to take a short-term breather for the moment in AI. AI might turn out to be the shiny star many experts think it will be, but it doesn’t take one day to become that shiny start especially when the majority of OpenAI users are applying it to do their homework.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-07-07 14:02:032023-07-09 22:13:44Traffic Sags for the Generational Technology

Recently, I have been touting a 2022 track record of +84.63%.

I have a confession to make.

I lied.

In actual fact, my performance was far higher than that. In reality, I generated a multiple of that +84.63% figure.

That is because my published performance is only for my front-month short-term trade alerts. It does not include the LEAPS recommendations (Long Term Equity Anticipation Securities) issued in 2022, the details of which I include below.

LEAPS have the identical structure as a front month vertical bull call debit spread. The only difference is that while front-month call spreads have expiration dates of less than 30 days, LEAPS go out to 18-30 months.

LEAPS also have strike prices far out of-the-money instead of deep in-the-money, giving you infinitely more upside leverage. LEAPS are actually synthetic futures contracts on the underlying stock.

Of the 12 LEAPS executed in 2022, eight made money and four lost. But the successful trades win big, up to 1,260% in the case of NVDIA (NVDA). With the losers, you only write off the money you put up.

And you still have 18 months until expiration for my four losers, ample time for them to turn around and make money. In the case of my biggest loser for Rivian (RIVN), Tesla launched an unprecedented EV price way shortly after I added this position. Never take on Tesla in a price war. Black swans happen.

Of course, timing is everything in this business. I only add LEAPS during major market selloffs as the leverage is so great, over 20X in some cases, of which there were four in 2022.

If you would like to receive more extensive coverage of my LEAPS service, please sign up for the Mad Hedge Concierge Service where you can excess a separate website devoted entirely to LEAPS. Be aware that the Concierge Service is by application only, has a limited number of places, and there is usually a waiting list.

Given the numbers below, it is easy to understand why most professional full-time traders only invest their personal retirement funds in LEAPS.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Sweet Taste of LEAPS

https://www.madhedgefundtrader.com/wp-content/uploads/2023/06/john-thomas-red-wine.jpg292317Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-29 09:02:042023-06-29 12:30:12My 2022 LEAPS Track Record

Silicon Valley has gone from the least regulated industry to trending the other way. On a global scale, draconian regulations are rearing their ugly head to really stymy places like China and artificial intelligence.

The European Union just rolled out a slew of proposed regulations on AI that could hamper its ability to embed itself in many tech companies.

The net result is highly bullish for Silicon Valley companies minus the chip companies that are experiencing revenue cuts.

When rules tighten, the entrenched benefit disproportionately and this could trigger a continuation of the tech rally that has been blistering hot this year.

Inversely, it will become even more difficult for start-ups to become unicorns, because they suffer more at smaller sizes to digest the higher amount of regulation that mature tech companies never faced.

Much of this is occurring at the highest level as the White House is considering new restrictions on exports of artificial intelligence chips to China, potentially adding to a list of banned semiconductor technology from Nvidia, Advanced Micro Devices, and other US companies.

The U.S. Department of Commerce could prohibit shipments of chips from Nvidia and others to customers in China as soon as early next month.

Nvidia, which produces graphics chips that drive the technology behind OpenAI Inc’s ChatGPT and Alphabet Inc’s Bard chatbots, is one of those chip companies that could see a slide in revenue in the short term.

Across the pond where governments are specialists at regulation, the European Parliament has approved draft legislation to regulate AI-powered technology.

The Act applies to anyone who creates and disseminates AI systems in the EU, including foreign companies such as Microsoft, Google, and OpenAI.

As outlined in the Act, EU lawmakers seek to limit or prohibit AI technology they classify as unacceptable or high risk.

It’s a little vague who will be deemed high risk but in the crosshairs are technologies such as predictive policing systems and real-time, and remote biometric identification systems.

Silicon Valley cash cows can function without these intrusive elements.

The AI Act would give the European government the authority to levy heavy fines on AI companies that do not abide by its rules.

Financial penalties may be steeper than GDPR penalties, amounting to €40 million or an amount equal to up to 7% of a company’s worldwide annual turnover, whichever is higher.

Beyond the government’s power to enforce the Act, European citizens would have the power to file complaints against AI providers they believe are in breach of the Act.

European officials expect to reach a final agreement on the rules by the end of 2023 after spending years developing the legislation. Such swift and consistent momentum to regulate technology in Europe stands in stark contrast to the United States, where lawmakers are still grappling with initial regulatory steps.

If passed, the Act is expected to become law by 2025 at the earliest.

It’s a lot easier for tech firms to operate in the Wild West when there are no rules, but if there are rules, it’s better than American tech has already built cash cows to keep the party moving right along.

It’s true there won’t be much competition and possibly an oligarchy, but it will translate into much higher share prices for the likes of Apple, Tesla, Meta, Microsoft, Google, and Amazon.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-28 15:02:592023-07-12 00:39:50Regulation Heats Up

Keeping up with the Joneses – that’s what Amazon is doing with its foray into generative artificial intelligence.

Its cloud division AWS is building a $100 million AI center to go toe to toe with increasing competition in cloud infrastructure services

The upcoming AWS Generative AI Innovation Center will become the heart and soul of Amazon experts in AI and machine learning.

This is a seismic strategic move for Amazon whom we have heard very little about in the generative AI sphere so far.

However, most people in the know understand that Amazon wouldn’t let this get away from them and use time wisely to concoct something worthy enough to show they have some skin in the game.

Unsurprisingly, AMZN shares were up relative to other big tech companies in a down week last week on the Nasdaq.

AMZN shares haven’t had quite the mojo that stocks like Tesla or Microsoft have had this year and this call to action is an aggressive step towards the vanguard of technological development.

I highly applaud the management at AMZN for this chess move.

In generative AI, algorithms are used to create new content, such as audio, code, images, texts, simulations, and videos.

Amazon said Highspot, Twilio, Ryanair, and Lonely Planet will be among the first users of the innovation center. With the new center, the company expects to hijack additional cloud services amidst increasing competition in the cloud infrastructure market.

Enterprise spending on cloud solutions reached $63 billion worldwide in the first quarter of 2023, up 20% from the same quarter last year.

Microsoft and Google had the strongest year-over-year growth rates, gaining 23% and 10% in worldwide market share, respectively. Amazon, the leader in cloud infrastructure, kept its 32% market share in Q1.

Amazon recently debuted Bedrock, an AI solution that allows customers to build out their own ChatGPT-like models.

The company also announced the upcoming Titan, which includes two new foundational models developed by Amazon Machine Learning.

Tech is largely downsizing staff and firing diversity officers and other woke positions, but the one area that is pushing for greater numbers is artificial intelligence data scientists and a bevy of LinkedIn posts show they are on the lookout to poach talent.

Amazon, who crushed Microsoft and Google in the business of renting out servers and data storage to companies and other organizations, enjoys a commanding lead in the cloud infrastructure market.

However, those rivals are early into generative AI, even though Amazon has drawn broadly on AI for years to show shopping recommendations and operate its Alexa voice assistant.

Amazon also failed to create the first popular large language model that can enable a chatbot or a tool for summarizing documents.

One challenge Amazon currently faces is in meeting the demand for AI chips. The company chose to start building chips to supplement graphics processing units from Nvidia (NVDA), the leader in the space. Both companies are racing to get more supply on the market.

At a technical level, Amazon shares and the rest of tech shares are quite overbought in the short term.

Last week was a modest pullback between 1-2% in the Nasdaq and I view that as highly bullish because of its orderly nature and lack of volume.

No panic selling is what we want for the markets to optimize the next bullish entry point.

After the modest price action digests fully, I do expect another dip-buying shopping spree for tech shares.

Stay patient and stay hungry.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-26 14:02:032023-06-27 00:48:19Amazon Joins the Party

Below please find subscribers’ Q&A for the June 21 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, NV.

Q: When do we buy Nvidia (NVDA) and Tesla (TSLA)?

A: On at least a 20% dip. We have had ballistic moves—some of the sharpest up moves in the history of the stock market for large stocks—and certainly the greatest creation of market caps since the market was invented under the Buttonwood Tree in 1792 at 68 Wall Street. Tesla’s almost at a triple now. Tripling one of the world's largest companies in 6 months? You have to live as long as me to see that.

Q: Is it a good time to invest in Bitcoin?

A: No, absolutely not. You only want to invest in Bitcoin when we have an excess of cash and a shortage of assets. Right now, we have the opposite, a shortage of cash and an excess of assets, and that will probably continue for several years.

Q: Should I short Apple (APPL)?

A: Only if you’re a day trader. It’s hugely overbought for the short term, but still in a multiyear long-term uptrend. I think we could see Apple at $300 in the next one or two years.

Q: Is it better to focus on single stocks or ETFs?

A: Single stocks always, because a single stock will outperform a basket that's in an ETF by 2 to 1 or even 3 to 1. That's always the case; whenever you add stocks to a basket, it diversifies risk and dilutes the performance. Better to just own Tesla, and if you want to diversify, diversify to Nvidia, but then I live next door to these two companies. That's what I tell my friends. You only diversify if you don’t know what is going to happen, which is most investors and financial advisors.

Q: Is the bottom of the housing market in, and are we due for a spike in home prices when interest rates can only go lower?

A: Yes, absolutely. In fact, we will enter a new 10-year bull leg for housing because we have a structural shortage of 10 million homes and 82 million millennials desperately trying to buy them at any price. I just got a call from my broker and she is panicking because she is running out of inventory. Even the lemons are starting to move.

Q: When do you think energy will rise?

A: Falling interest rates could be a good key because it sets the whole global economy on fire and increases energy demand.

Q: Outlook for the S&P 500 (SPY) second half of the year?

A: We hit 4,800 at least, maybe even higher. That's about a little more than 10% from here, so it’s not that much of a stretch, not like it was at the beginning of the year when it needed to rise 25% to reach my yearend target.

Q: Best time to invest from here on?

A: Either a 10% pullback in the market, or a sideways move of 3 months—that's called a time correction. It usually counts as a price correction because of course, over 3 months, earnings go up a lot, especially in tech.

Q: I’m seeing grains (WEAT) in rally mode.

A: Yes, that's true. They are commodities, and just like copper’s been rallying, and it’s yet another signal that we may get a much broader global commodity rally in everything: iron ore, coal, energy, gold, silver, you name it.

Q: Will inflation drop to 2%, causing stocks to go on another epic run?

A: The answer is yes, I do see inflation dropping to 2% —maybe not this year, but next year; not because of any action the Fed is doing, but because technology is hyper-accelerating, and technology is highly deflationary. The tech product you bought two years ago is now half the price, and they offer you twice as much functionality with an auto-renew for life. So, that is happening across the entire technology front and feeds into the inflation numbers big time, including labor. There's going to be a lot of labor replacement by machines and AI in the coming years.

Q: Is Airbnb (ABNB) a good stock to buy?

A: Well, if we’re going into the most perfect travel storm of all time, which is this summer, and which is why I’m going to remote places only like Cortina, Italy. Airbnb is the perfect stock to own. It’s a well-run company even in normal times.

Q: Should I buy gold here on the pullback?

A: Yes, you should. Gold is also highly sensitive to any decline in interest rates, and by the way: buy silver, it always moves 2.5x as much as the barbarous relic.

Q: How can inflation not go up if commodities and wage demands are going up due to state and federal unions? What about farm equipment and truck supplies? Costs keep rising, should we buy John Deere (DE)?

A: There are three questions here. Inflation will not go up because, though commodities will rise, they are only 0.6% of the $100 trillion global economy, or $660 billion in 2022. That will be more than offset by technology cutting prices, which is 30% of the stock market. You have to realize how important each individual element is in the global picture. And regarding wage demands going up caused by state and federal unions, less than 11.3% of the workforce is now unionized and that figure has been declining for 40 years. Most growth in the economy has been in non-unionized technology firms which largely depend on temporary workers, by design. What IS unionized is mostly teachers, the lowest paid workers in the economy, so incremental pay rises will be small. Unions were absolutely slaughtered when 25 million jobs were offshored to China during the Bush administration. Buy farm equipment and trucks? Absolutely, buy John Deere (DE) and buy Caterpillar (CAT) on the next dip. I was actually looking at Caterpillar for the next LEAPS the other day, but it’s already had a big run; I'm going to wait for a pullback before I get CAT and John Deere. So, again, people see headlines, see union wage headlines—I say focus on the 89% and not on the 11% if you want to make good decisions.

Q: Is Boeing (BA) a buy on the dip?

A: Yes, they got 1,000 new aircraft orders and the stock hasn't moved. So yes, if you get any kind of selloff down to $200, I'd be hoovering this thing up.

Q: Can you please explain how the profit predictor works?

A: It’s a long story; just go to our website, log in and do a search for “profit predictor,” and you’ll get a full explanation of how it works. It’s actually where Mad Hedge has been using artificial intelligence for 11 years, which is why our performance has doubled. Just for fun, I'll run the piece next week.

Q: Gold (GLD) is having a hard time going up because Russia is being squeezed by other governments. Since they need cash, they may be either selling their gold or stop buying new gold.

A: That is a good point, but at the end of the day, interest rates are the number one driver of all precious metals—period, end of story. We’re long gold too, I’ve got lots of gold coins stashed around the world in various safe deposit boxes, and I'm keeping them. I’ve got even more silver coins, which take up a lot of space.

Q: Do you like India (INDA) long term?

A: Yes, it’s the next China. But as Apple is finding out it is very difficult to get anything done there. A radical reforming Prime Minster Modi may be changing things there with his recent Biden visit and (GE) contract to build jet engines.

Q: What do you think of General Dynamics Corp (GD)?

A: I like General Dynamics because I think defense spending is in a permanent long term upcycle as a result of the Ukraine war. And it won’t end with the Ukraine war—the threat will always be out there, and the buying is done by not only us but all the other countries that think Russia is a threat.

Q: Do you like MP Materials Corp (MP)?

A: Yes, I do. The whole commodities space is ready to take off and go on fire.

Q: What about Square (SQ)?

A: The only reason I’m not recommending Square right now is huge competition in the entire sector, where all the stocks including PayPal (PYPL) are getting crushed. I will pass on Square for now, especially when I can buy US Steel (X) at close to its low for the year.

Q: If you had to pick one: Nvidia (NVDA), Tesla (TSLA), Microsoft (MSFT), Meta (META), and Google (GOOGL), which is the best to buy for next year?

A: All of them. Diversify. If I have to pick the top performer, it’s going to be either Tesla or Nvidia, probably Nvidia. But you need at least a 10% correction before you do anything. Actually, the split-adjusted price for our first (NVDA) recommendation eight years ago was $2 a share.

Q: Do you like Crown Castle International (CCI)?

A: Yes, I like it very much—it has very high dividend yield at 5.5%. The reason it hasn’t moved yet is that as long as interest rates are high, any REIT structure will suffer, and (CCI) has a REIT structure. Sure, it’s in a great sector—5G cell towers—but it is still a REIT nonetheless, and those will start to recover when interest rates go down; that’s why we did a 2.5-year LEAPS on CCI. For sure interest rates are going to go down in the next 2.5 years, and you will double your money on (CCI). That’s why we put it out.

Q: Which mid cap will do best over the long term: Airbnb (ABNB), Snowflake (SNOW), or Palantir (PLTR)?

A: That’s easy: Snowflake. They have such an overwhelming technology on the database and security front; I would be buying Snowflake all day long. Even Warren Buffet owns Snowflake, so that’s good enough for me.

Q: Could you comment on the pace of EV adoption/potential for (TSLA) robot fleet acceleration and implications for oil investments in holding pattern till the eventual collapse to near 0?

A: Yes, oil may collapse to near zero, but it may take twenty years to do it—that’s how long it takes to transition an energy source. That’s how long it took the move from horses and hay to gasoline-powered cars at the beginning of the 20th century. A national robot fleet of taxis with no drivers at all is a couple of years off. There are about 1,000 of them working in San Francisco right now, but they still have more work to do on the software. When it gets foggy, they often congregate at intersections causing traffic jams. Suffice it to say that eventually Tesla shares go to $1,000 and after that, $10,000—that’s my bet. By the way, my Tesla January 2025 $595-$600 LEAPS are starting to look pretty good.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2018 in Australia

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-03.jpg400400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-23 09:02:392023-06-23 15:53:43June 21 Biweekly Strategy Webinar Q&A

Mad Hedge Technology Letter

June 16, 2023 Fiat Lux

Featured Trade:

(THE SKINNY ON AI) (CRM), (NVDA), (MSFT), ($COMPQ)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-16 14:04:352023-06-16 19:03:48June 16, 2023

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.