Mad Hedge Biotech & Healthcare Letter

October 31, 2019

Fiat Lux

Featured Trade:

(ONE PLUS ONE EQUALS THREE WITH THE PFIZER-MYLAN DEAL),

(PFE), (MYL)

Mad Hedge Biotech & Healthcare Letter

October 31, 2019

Fiat Lux

Featured Trade:

(ONE PLUS ONE EQUALS THREE WITH THE PFIZER-MYLAN DEAL),

(PFE), (MYL)

"Greater than the sum of its parts." This is how the executives of Pfizer (PFE) described its merger with generic drug company Mylan NV (MYL) in the third quarter of 2019.

The deal, which is specifically between Mylan and Pfizer's off-patent department Upjohn, would result in the creation of the largest generics company by revenue in the world, reaching an enterprise worth $50 billion. In fact, this new company is anticipated to own roughly a third of all generics available today and approximately 15% of the generics market in the United States alone.

With the ever-changing pharmaceutical market, both Pfizer and Mylan have been grasping at straws in terms of reshaping their strategies and keeping up with the competition. Needless to say, this new powerhouse partnership comes as a relief for the investors of both Pfizer and Mylan.

This blockbuster deal allows Pfizer to focus its efforts on coming up with groundbreaking and more profitable products, hopefully beating its $54 billion sales in 2018. This move is a response to the insistent demand on the giant biopharma company to separate its Upjohn division, which works solely on legacy drugs, from the primary prescription-drug operations.

That way, Pfizer can focus on more lucrative, branded treatments like cancer medication Ibrance and pneumonia vaccine Prevnar.

This deal aligns with the recent moves by Pfizer acquiring potentially blockbuster treatments such as its $10.6 billion buyout bid of cancer treatment firm Array BioPharma earlier this year. This move is also reminiscent of Pfizer’s and GlaxoSmithKline’s (GSK) decision to merge their consumer healthcare departments.

Meanwhile, this all-stock deal provides Mylan with a financial lifeline following years of struggle. Its investors showed support over the deal as shares rose to as high as 19%, reaching $21.88 following the announcement.

While the generic drugs company, which is widely known for its emergency allergy medication EpiPen, is still far off from its all-time high of $67, this merger with Upjohn would allow both to amplify their efforts in dominating the market. More importantly, Mylan will retain a 43% stake in this new company.

For example, Mylan could boost Upjohn’s efforts in repackaging cholesterol drug Lipitor, nonsteroidal anti-inflammatory medication Celebrex, and erectile dysfunction medication Viagra as more attractive generic alternatives and boost their sales.

Since these drugs have expired or have expiring patents, their sales have been plummeting in the United States. With this merger though, Pfizer hopes to capitalize on the promising market called “branded generics” which has become quite popular in China.

“Branded generics” has gained a following in the Middle Kingdom due to the proliferation of fraudulent generic drugs – a trend that Pfizer has been eager to take advantage of seeing as the company actually moved Upjohn’s headquarters in Shanghai earlier this year.

Aside from Lipitor, Celebrex, and Viagra, the new company will also be handling the sales of over 7,500 Mylan products that include biosimilars and over-the-counter drugs.

With 165 markets targeted by this new company, its projected revenue is somewhere between $19 billion and $20 billion in 2020 and $22 billion in 2021. Meanwhile, its executives plan to solve the $25 billion worth of combined debt by targeting annual expense savings worth $1 billion to be reached by 2023.

In comparison, Mylan’s second-quarter adjusted earnings per share was at $1.03, with the company reaffirming its adjusted earnings for 2019 at $3.80 to $4.80 per share. Its profit for this year is estimated to reach $11.5 billion to $12.5 billion.

Meanwhile, Pfizer’s second-quarter report recorded $13.2 billion in sales, which indicates a 2% decrease from last year’s report during the same period. Meanwhile, Upjohn’s revenue fell by 11% year-over-year and hit $2.8 billion compared to the $3.1 billion last year.

With all these advantages, it can be safely said that Mylan was an excellent choice for Pfizer especially considering that the smaller company came in so cheap.

In 2018, Mylan was valued at $25 billion. Prior to the announcement in July though, Mylan only had a market cap of $10 billion. With the money saved on the deal, the newly formed company can push back on pricing and pour funds over marketing their generic products.

Even with the cheap buyout price, the new company will still be less levered compared to a stand-alone Mylan. It’s also projected to generate over $4 billion in free cash flow annually.

This deal eliminates a strategic bottleneck from Pfizer and solves the financial woes of Mylan. While there remains a lot to be seen in terms of achieving their goals, investors of both companies will definitely enjoy a brighter future.

After all, this new company boasts of an incredibly powerful mix of a portfolio that covers generics, branded products, over-the-counter meds, and biologics.

Buy Pfizer on dips. It is about to achieve a major breakout to the upside on the back of this fantastic deal.

Mad Hedge Biotech & Healthcare Letter

October 24, 2019

Fiat Lux

Featured Trade:

(SPECIAL CANCER ISSUE - PART II)

(LLY), (PFE), (GTHX)

The most groundbreaking biotechnology discoveries in this century have now reached the flashpoint between theoretical discussions and their realization. Billions of dollars have been poured into the research and development phases, with some companies already generating income. More impressively, potential cures for a number of fatal diseases are now in the pipeline. For early investors, this translates to massive earnings in the succeeding years.

Among the widely sought-after cures is for triple-negative breast cancer (TNBC), which is the most aggressive form of the disease. It also has a poorer prognosis compared to other types of breast cancer, so it’s crucial to offer treatments that can not only improve chances of survival but also improve the quality of life of the patients suffering from it.

Here are the three most promising developments in the search for the cure of TNBC.

Eli Lilly (LLY)

It’s always challenging to be a third-to-market treatment especially when you’re trailing a pioneering drug like Pfizer’s (PFE) groundbreaking drug Ibrance and Novartis’ blockbuster drug Kisqali. However, Eli Lilly (LLY) is hoping that its recent data on Verzenio would bolster its hold in the market.

While it remains to be seen if Verzenio can catch up with Ibrance’s success, the Eli Lilly drug has managed to surpass estimates by $19 million during the first quarter of 2019 following an underwhelming fourth quarter in 2018. As for the latest data on Verzenio, the company disclosed that a combination of the drug and hormone therapy improved the median to 46.7 months compared to the 37.3 months for those who solely underwent therapy.

The 9.4 survival advantage indicates a 25% decrease in mortality risk. Apart from that, patients also enjoyed a better quality of life as this combo allowed them to manage for 50 months -- or over four years -- without the need for follow-up chemotherapy. This is a huge advantage since hormone therapy alone only allowed 22 months before the next treatment.

The effects don’t end there though. Eli Lilly has another trick up its sleeve to make sure that it stands out from the drugs targeting similar diseases. According to the company, Verzenio is the only drug that can help patients with tough-to-treat diseases.

That is, the Eli Lilly drug took effect even on patients who were initially resistant to therapy as well as those who quickly relapsed after treatment. This resulted in a decrease in death risk by roughly 31%. While this aspect still requires additional tests, the results showed a promise that not even Pfizer’s Ibrance can deliver.

Merck & Co. (MRK)

Merck & Co. (MRK) has rallied virtually the entire force of its research and development team behind ensuring that Keytruda remains on top -- way ahead of competitors like Bristol Myers Squibb’s (BMY) Opdivo. At the moment, Merck’s moneymaker has approximately 1,050 clinical trials queued to assess the possibilities of this drug further dominating clinical practice.

So as Bristol Myers Squibb attempts to woo investors with the promising results of Opdivo, Merck has been busy adding another notch in its belt with another landmark first for Keytruda. Aside from its current applications, this Merck cash cow is also pegged as a promising treatment for TNBC when combined with therapy.

Based on the data on its breakthrough therapy designation, this indication is likely on the fast track towards an FDA approval soon. To date, Keytruda has more than 20 oncology indications in the United States alone with the giant biopharma receiving the green light to market the drug in China as well.

If things move forward as planned, Keytruda may very well be on its way to topple AbbVie Inc.’s (ABBV) Humira from the top of the list of best-selling drugs worldwide in the next five years. After all, revenues from the drug are expected to hit anywhere between $17 billion and $24 billion in 2024.

G1 Therapeutics (GTHX)

Joining the biopharma giants is newcomer G1 Therapeutics (GTHX). This up-and-coming firm has recently released its clinical data on oral selective estrogen receptor degrader (SERD) for metastatic TNBC. Called G1T48, this new treatment provided promising results when combined with the company’s own breakthrough therapy called trilaciclib.

For comparison, G1 Therapeutics’ combo is said to be more potent than AstraZeneca plc’s (AZN) Faslodex, which is currently the only FDA-approved SERD treatment in the market. Unlike Faslodex though, which requires intramuscular injection, G1 Therapeutics’ drug can be taken orally once a day. Needless to say, this mode of treatment offers an improved patient experience.

With such promising results, G1 Therapeutics plans to roll out new drug application submissions by the fourth quarter of 2019. If things move smoothly, then the treatment plan should be out in the market sometime in the second quarter of 2020.

Mad Hedge Biotech & Healthcare Letter

October 1, 2019

Fiat Lux

Featured Trade:

(THE PLAYERS GUIDE TO BIOTECH INVESTING)

(AMGN), (PFE), (NOVN), (ABBV), (ABT),

(AGN), (ROG), (GSK), (CELG), (JNJ), (BMY)

You can’t watch a game without a program, and the lineup for biotech and healthcare is truly astonishing. No surprise then that the fields account for more or less than 17% of US GPD.

Here is a listing of the biggest $100 billion plus products you have never heard of. The good news is that you have just stumbled across a sector that will generate no less than a staggering $1.4 trillion in sales over the next five years.

That means it’s certainly worth your time getting to know this field. With this amount at stake, it’s no wonder companies manufacturing these blockbuster drugs are sparing no expense to fight off patent vultures.

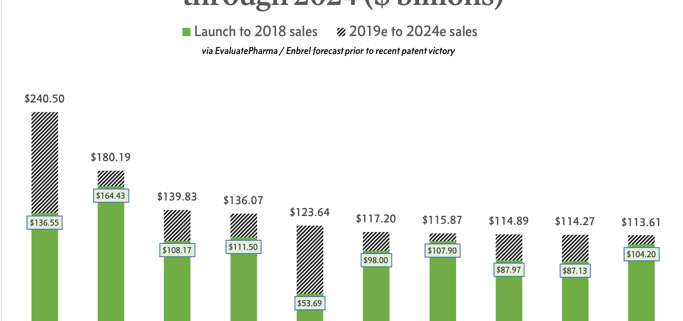

A good example is Amgen (AMGN), which recently won its case to extend the patent life of rheumatoid arthritis biological Enbrel against Novartis AG’s (NOVN) biosimilar arm Sandoz. Since each extra hour added to patent life means millions of dollars (and sometimes billions) in sales, the additional 10 years of exclusivity for Enbrel is a massive victory for Amgen.

In a recent study released by Evaluate Pharma, Enbrel was ranked third in the top 10 biggest sellers up to 2024. The forward-looking consensus projection anticipates Amgen’s golden goose to hit roughly $140 billion in total revenues in five years – a truly impressive performance particularly for a drug that has been around for more than 20 years. However, Enbrel’s longevity pales in comparison to the other behemoths in the biopharma realm.

Up until 2018, Pfizer’s (PFE) Lipitor held the title of earning the highest lifetime sales in the industry. Since its launch in 1997, the cholesterol drug has raked in $164.4 billion in revenues so far with the number estimated to reach $180 billion by 2024. Lipitor’s success is highlighted more by the fact that it's under a small molecule status and holds approval for a very narrow indication.

Overtaking Lipitor to take the top spot is AbbVie’s (ABBV) rheumatoid arthritis treatment Humira, which closed with $20 billion in sales in 2018 alone. While some AbbVie investors frown upon the over-reliance of the company on Humira, it appears that the efforts to protect the drug has paid off big time.

With patent protection (132 approved patents!) safeguarding its exclusivity in the market, Humira is projected to reach a total of $240 billion in revenues by 2024. Clearly, the rewards they’ve been reaping show no signs of abating anytime soon.

More importantly, Humira’s robust sales, which makes up almost 70% of the company’s profits, has provided AbbVie with the financial capacity to finally get out of the shadow of parent company Abbott Laboratories (ABT) and come up with its own pipeline. As it happens, AbbVie’s efforts towards this direction have already started with the massive purchase of Allergan (AGN) for $63 billion this year.

Apart from Lipitor, Humira, and Enbrel, there are three more blockbuster products with sales that hit the $100 billion mark as of 2018 -- a figure that would make Ecuador proud to claim as their annual GDP. These are Roche Holding Ltd. Genussscheine’s (ROG) chemotherapy drug Rituxan, Amgen’s anemia treatment Epogen, and GlaxoSmithKline’s (GSK) asthma medication Advair.

One biopharma bestseller that leapfrogged a lot of other drugs in the market is multiple myeloma medication Revlimid -- aka the drug that built Celgene (CELG). With an entry date of 2008, this drug is the newest one on the list. While Revlimid’s sales are impressive, what’s actually quite exciting is the fact that its projected revenues easily outstrip its already notable sales of $53.69 billion.

By 2024, this Celgene blockbuster is estimated to reach $123.64 billion in sales. There’s a caveat to this though as Revlimid’s success in the years to come is dependent on how Celgene plans to deal with generic competition chomping at the bit and ready to attack once the drug reaches its 2022 patent expiration date.

Another big-ticket drug that might see a bit of a decline in sales soon is from Johnson & Johnson (JNJ). While the company has always been aggressive when it comes to dominating the market for its Crohn's Disease drug Remicade, an investigation by the Federal Trade Commission (FTC) might put a damper on things soon. According to recent reports, JNJ has been suspected of contracting payers to ensure market control and stave off competitors.

Meanwhile, the three horsemen of Roche, namely, Rituxan, cancer and eye disease medication Avastin, and breast cancer treatment Herceptin, reached a collective amount of $365 billion in total sales. These three are anticipated to stay put on top of the industry in the next five years as well, thanks to their competitive pricing and aggressive strategies to protect their patents.

Rounding out the list is Amgen’s Epogen, which is expected to add $107.90 billion to the already astounding $115.87 billion it generated for the company. Meanwhile, GSK’s Advair, which brought in $113.61 billion, is expected to pour in an additional $104.20 billion by 2024.

Interestingly, the majority of the top 10 franchise drugs are biologics except for Sanofi’s (SAN) ulcer treatment Zantac, Bristol-Myers Squibb Co’s (BMY) heart medication Plavix, Advair, and of course, Lipitor. In fact, this is considered as the primary reason for their capability to fight off potential copycats for years.

In some cases, their monopoly of the market has allowed them to expand to include various other indications in their coverage. The massive sales of biologics are also rooted in their ability to demand big-ticket reimbursements. Unlike their generic competitors, brand recognition alone makes it more convenient for patients to ask for compensation.

Needless to say, the success stories of these drugs make it quite obvious why these biopharma companies employ a battalion of legal experts to fend off the rise of generics. While the onslaught of biosimilars cannot be helped, these lawyers ensure that patients opting for these versions of the medication would find it incredibly difficult to ask for biosimilar reimbursements.

Global Market Comments

March 15, 2019

Fiat Lux

Featured Trade:

(BUY JOHNSON & JOHNSON ON THE BAD NEWS),

(JNJ), ($INDU), (PFE), (NVS), (AZN)

When one of the 30 Dow Average companies ($INDU) gets into trouble, I sit up and take note, stand to attention and drill down with a magnifying glass.

After all, it may have a major important on an important tradable index, thus opening up an investment opportunity. It also may sound the alarm for a great single stock pick. That is certainly the case with New Brunswick, NJ based Johnson & Johnson, one of the oldest companies traded on the NYSE.

What piqued my interest today was the news that the company lost another talcum power lawsuit, which is alleged by plaintiffs to contain asbestos. This has been among the catalog of urban conspiracies for decades now.

Johnson & Johnson (JNJ) is, in fact, carrying on with their mission to strengthen their pharma sector which has consistently served as their top revenue driver in the past years. While their strong performance in this segment has always been led by their oncology portfolio, with sales of their cancer drugs increasing by 22.1% worldwide in the previous quarter, it looks like more and more products are on their way to becoming JNJ's blockbuster items.

The company estimates to launch more than ten new drugs -- all of which have the potential to be blockbuster products -- by 2021. On top of these, JNJ expects to complete 50 line extensions on their existing products. Both efforts are anticipated to temper the effects of generic drugs that are threatening to hamper the sales of a lot of key products in JNJ's portfolio.

The latest potential blockbuster drug for JNJ is Esketamine which is an anti-depressant aimed at treatment-resistant patients. This was developed by the company’s pharmaceutical arm, Janssen Pharmaceuticals Inc. This new groundbreaking product was approved on March 5 by the FDA and will be marketed as Spravato. It is hailed as the first prescription depression drug developed from ketamine, which is more commonly used as an anesthetic.

Although ketamine has long been tagged as a party drug, aka “Special K”, and is approved as an anesthetic, no company has patented its use. This is where Janssen swooped in and patented the left section of the molecule, called esketamine, and sent their application to FDA. The approval of this drug, which FDA described as a “breakthrough therapy” thus receiving priority review, translates to a potential cash cow for JNJ as it successfully legitimized the application of ketamine as an anti-depression drug.

Aside from depression, FDA is also taking into consideration the applicability of esketamine to patients afflicted with mood disorders such as bipolar disorder. The organization looks at it as a potential solution for reducing suicides as well.

Other drugs projected to rake in massive sales for JNJ pipeline include psoriatic arthritis Tremfya, prostate cancer medication Erleada, and metastatic urothelial cancer treatment Erdafitinib. With the addition of Spravato on the list, sales are expected to reach more than $1 billion.

However, no company is perfect and the same goes for products -- even if they are poised to become blockbuster drugs. A major hindrance for the success of Spravato is cost.

Here's a sample quote for potential patients.

A one-month initial treatment will cost somewhere from $4,000 to $7,000. The exact price will depend on the dosage and if it's availed wholesale. Expenses for follow-up treatments will reach $2,360 to $3,500 a month. All in all, Spravato could become as expensive as an electroconvulsive treatment or even a transcranial magnetic stimulation therapy. Worse, this treatment might have to be shouldered by the patients themselves.

Another deterrent for investors looking into JNJ is the continuing issue concerning the talcum powder lawsuits which claim that the talc items of the company contain asbestos that resulted in ovarian cancer among many of its female users. As of August 2018, a Missouri court has ordered JNJ to pay 22 women a total of $4.7 billion for damages. While the company announced its decision to appeal the ruling, the case has been a huge red flag for investors ever since.

Nonetheless, it appears that JNJ remains a solid stock for a lot of investors.

With an annual revenue of $81.6 billion, (JNJ) is anticipated to stay ahead of its competitors Pfizer (PFE) ($53.4B), Novartis (NVS) ($51B), and AstraZeneca (AZN) ($21.9B). Taking into consideration currency impact, which is expected to negatively affect sales by roughly 1.5%, JNJ's revenues are projected to hit $80.4 to $81.2 billion this year.

While it still has a long way to go, the recent approval of Spravato spelled higher confidence in JNJ's revenue growth this year. The company's purchase of robotic surgical instruments manufacturer Auris Health, for $3.4 billion further strengthened its dominance in the industry.

In the past month alone, its shares rose by 4.55%. Investors are also anticipating more growth until the next earnings report, which is anticipated to show $2.10 earnings per share for the company. This represents a 1.49% year-over-year increase.

You would think that the company that makes Viagra would be booming with all these baby boomers around.

It’s not.

As we come into the tag ends of the Q1 earnings season, it is hard to ignore the pitiful performance put on by Pfizer (PFE). Its fourth-quarter earnings were totally overshadowed by its disappointing outlook and underperforming shares.

The 168-year-old drug maker can expect sustainable growth in some of its product franchises, such as prostate cancer drug Xtandi, blood clot medication Eliquis, metastatic breast cancer drug Ibrance, and arthritis medicine Xeljanz.

However, generic competitors against Pfizer mainstays like Pristiq, an anti-depressant drug, and Viagra are threatening to trigger a massive decline in the former’s sales. With generic companies hot on its heels, Pfizer faces incredible pressure in terms of pricing and lower gross margins.

Expiring patents known as the loss of exclusivities (LOE) are also projected to contribute to their red ink by approximately $2.6 billion. In particular, Pfizer is expected to lose exclusive rights to its blockbuster drugs Lyrica in June 2019 and Chantix in the next few years. To date, their LOEs already cost Pfizer $2.1 billion in sales in 2017 and an additional $1.8 billion in 2018.

Pfizer is doing better than its competitors. In the past 12 months, Pfizer EPS stood at $1.86, which showed a 47.16% decline year-over-year. By comparison, major competitor Merck & Co., Inc. (MRK) EPS was at $0.69, suffering from a 281.58% decline year-over-year while Novartis (NVS) faced a 38.8% decline with an EPS of $0.52.

Pfizer’s recorded annual revenues of $53.4 billion, which puts it ahead of its major competitors Novartis ($51 billion) and Merck & Co., Inc. ($41.7 billion).

Bleak 2019 but promising 2022. That’s a long time to hold your breath.

As far as 2019 is concerned, the pharma heavyweight does not present any growth potential in both their top and bottom lines, with their midpoints offering slightly lower revenue and earnings compared with that in 2018.

Pfizer is projected to deliver a flat year-over-year performance regardless of the major headwinds primarily due to the strong sales of its remaining products. The company continues to remain confident as it awaits roughly 25 to 30 drug approvals up to year 2022.

Among these pending potential blockbuster products, 15 are expected to be approved by 2020. In addition, Xtandi, Ibrance, and Xeljanz/XR are slated for line extensions. With regard to long-term growth, Pfizer is well positioned to make headway on innovative medical breakthroughs in the next five years or so.

Pfizer is anticipated to reap the rewards of its $93 million investment in NextCure, which is a biopharmaceutical company focused on discovering and developing next-generation immuno-oncology-based drugs.

Pfizer has also been implementing various cost-cutting and productivity measures since 2017 in an effort to offset the effects of rising expenses and push for bottom line growth (read firing people).

Their efforts include investing in new market creation strategies as well as seizing opportunities to streamline their operations and cutting down organizational layers to eliminate (or at least reduce) bureaucracy.

These initiatives are anticipated to reach completion by 2019 and are expected to bring in approximately $1.4 billion in savings by 2020.

Given the challenges ahead, Pfizer seems to offer a promising future as seen in their efforts to curb their losses. While it remains to be seen if the company can come up with any notable acquisition to jumpstart their promised progress as early as 2020, Pfizer’s current products along with its pipeline candidates appear to be capable of delivering solid growth in succeeding years. Meanwhile, Pfizer is intent on providing a growing dividend to its shareholders.

In a nutshell, Pfizer’s current status is not ideal for investors interested in immediate profits. However, those who are patient enough to wait for a few more years could be in line to receive a dividend that could yield 3.5%.

Leave this one to the index funds and ETFs. There are better fish to fry in the space.

Global Market Comments

September 25, 2018

Fiat Lux

Featured Trade:

(AI AND THE NEW HEALTH CARE),

(GOOGL), (XLP), (XLV), (MRK), (BMY), (PFE),

(MONDAY, OCTOBER 15, 2018, ATLANTA, GA,

GLOBAL STRATEGY LUNCHEON)