In an interview with CNBC’s Andrew Ross Sorkin, the CEO of Palantir (PLTR) Alex Karp pitched us why America should view his company Palantir as a force for global good and why investors should invest in this company.

I wasn’t convinced after hearing his answer, and the dead giveaway was his avoidance of the question about why he continues to dilute the volume of shares in the software company.

On the revenue side of things, it’s been quite good, with the software business exploding in revenue from $560 million in 2018 to annual revenue of $1.54 billion in 2021.

His tech company overwhelmingly benefits from geopolitical catastrophes like kinetic wars ,which is why the military conflict in Eastern Europe is so lucrative for Palantir.

In the interview, he hyped his software as the great equalizer to Russia’s army, claiming that the reason a “small” country can fight toe to toe with Russia is with the help of the Palantir software.

That claim was a bit of a stretch, but why not use the global stage to hype up one's product and abilities?

Karp also took a victory lap on the brutal governmental lockdowns of 2020 and 2021 around the world, saying his company “saved millions of lives” by integrating Palantir with government services.

Basically, if the world is trending badly and the worse the better for the tech firm to the point of mass violence and anarchy, his company will ride those coattails to profits.

Yet the stock price has swan dived from $40 to $7.

You read that correctly.

Part of the problem of Karp’s software company is clearly the economic and financial backdrop that has forced interest rates higher and caused rampant inflation. I won’t discount that.

But the more important excuse for the appalling stock performance is because of Karp aggressively diluting shares.

The number of shares has increased by around 200% since the 2020 IPO and many of those shares have gone to upper management.

Karp and his friends have a habit of cashing out these diluted shares because they are still worth hundreds of millions even after the dilution, and Karp is still owed newly minted shares each year for around the next 10 years.

Sounds like a bad deal for the incremental investor.

In short, Palantir has served as the personal piggy bank for Alex Karp and his executive management team.

Instead of rewarding the shareholders, he has milked the company for profits while pouncing on public money to fund his software company.

In almost every interview I have seen him participate in, he doesn’t miss a chance to bash the Silicon Valley establishment either and almost calls them un-American.

Although he is highly forthright about his responsibility to be an American-first company, his shunning of external investors is why every reader should avoid this company.

If you invest hard-earned money into this firm, your money will be cashed out by Karp like his personal ATM.

It’s like an annual procession – rinse and repeat.

He’s just waiting until the end of 2023 for his new tranche of diluted shares to hit his account, and then he will sell them on the open market and withdrawal more fiat dollars.

Aside from the stock dilution circus, the company is actually quite solid with a competitive moat around its proprietary software.

The one negative I can think of is the lack of profitability with the firm losing half a billion dollars last year.

However, the company is growing too fast so that super growth justifies the loss-making.

Karp needs to stop running the company only for the purpose of his personal bank account and PLTR’s shares will never go up until he accommodates outside shareholders.

This is a $7 today, but because of Karp’s financial mismanagement of PLTR, it should be a $25-$30.

Until there is proof that Karp has changed strategies and incorporates a vision of prioritizing shareholder returns, readers will need to look elsewhere to make money in the tech sector.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-01-18 15:02:422023-01-31 18:32:40Follow The Money

Below please find subscribers’ Q&A for the October 21 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: Bank of America (BAC) said the US consumer is strong and lending is robust. Does this mean no recession in 2023?

A: It could, because remember that while some sectors are clearly in recession, like real estate and automakers, and have been for a while, others are absolutely booming, like the airline business, and the banking business. There may not be a recession in here, or if there is one, it’s a very slight one. Count on the market to first discount a severe recession which would take the S&P 500 down to $3,000-$3,200 or so; and that’s what markets do, always overly pessimistic at the bottom and overly euphoric at tops. You can make your living off of this.

Q: What do you think about OPEC's behavior (USO) and its influence on the price of oil?

A: Clearly, they’re trying to influence the midterm elections and get an all-republican pro-oil Congress, which will be nicer to OPEC. That’s certainly what they got with the last administration and it’s safe to say that the pro-climate administration of Biden and the Saudis get along like oil and water. But long term, OPEC knows it’s going to zero, and in fact, Saudi Arabia has plans to turn their entire oil supply into hydrogen which can be exported and burned cleanly. I know the team here at UC Berkeley that’s working on that with the Saudi government. Cheap hydrogen also means airships come back, how about that? Hindenburg anyone?

Q: Will draining the Strategic Petroleum Oil Reserve (SPR) backfire, meaning deflation for the US economy and administration?

A: No, the SPR outlived its usefulness maybe 30 years ago—it’s essentially a government subsidy for Texas and Louisiana, and for the oil industry, that has taken on a life of its own. When we started the SPR in 1975, the US got more than half of its oil from the Middle East. Now, it’s almost zero. It goes to China instead. If we are a net energy producer and we have been for over 5 years, why do we even need a petroleum reserve? So no, I think we should shut it down and sell all the oil that’s in there. And it becomes even less relevant as more of the US economy turns over to alternatives.

Q: How do we operate our military with no oil?

A: The pentagon is working on a no-oil future, developing alternative fuels for all kinds of things that you wouldn’t imagine are possible. For example, instead of using diesel, jet fuel, or gasoline for our vehicles, you outfit them with electric batteries, and when the batteries go dead you just air drop new fully charged ones. It’s much better than trying to transport gasoline across the desert in a giant fuel bladder, which can be taken out by a single bullet and is what they do now. Take the pilots out of fighters and they become so light they can operate on battery power. So yes, the pentagon has actually been in the forefront of using every alternative technology they can get their hands on from the early days. Better they get them first before an enemy does.

Q: We will almost always need petroleum; far too many products use it as an ingredient.

A: That is absolutely right. Some will probably never be replaced, like asphalt, feedstock, or plastic. However, those represent less than 10% of the current oil demand. So yes, there always will be an oil industry, it just might be a heck of a lot smaller than it is now. You eliminate cars from the picture, and that’s half of all oil demand in the United States right there. And in most places in the United States, it will be illegal to sell a car that uses gasoline in 12 years. And do you make 30-year investments based on demand for your product dropping by half in 12 years? No, you don’t, which is why the oil companies themselves won’t invest in their own industries anymore. They’re only paying out profits as dividends and buying back shares, which they never used to do.

Q: Do you think the Standard & Poor’s 500 Index (SPX) $3,500 was the bottom?

A: No, we actually did get a little bit lower than that. We will be in a bottoming process over the next several months, but the pattern will be the same. Tiny marginal new bottoms, maybe 100 points lower than the last, and then these gigantic rallies. If we do make bottoms they will only be for seconds, so the way to deal with that is to only put in really low-limit orders to buy stuff, assuming 1,000 points down, and just keep entering the order every day. Eventually, you’ll get one of these throw-away fills when the algorithms panic and a bunch of market orders hit the market. That's the way to deal with that.

Q: I would say that Biden is trying to influence the elections by releasing oil reserves.

A: Absolutely he is, but then so is the oil industry, taking half of the refineries off stream 2 months before the elections, and spiking oil prices. So it’s a battle of the oil price going on here. No love lost between the oil industry and Biden, and US consumers for that matter. I don’t care if gasoline is $7 a barrel because I never buy it; I am all electric. But for a lot of working people, that’s definitely a lot of money.

Q: How concerned are you about the US going to a cashless currency?

A: I’m not worried because I pay my taxes and I don’t break any laws. If you don’t pay taxes and do break laws, like engaging in drug dealing or bribery, you should be extremely worried, as that would be the eventual goal of a cashless economy. That and the fact that the government has to spend $300 million a year printing paper money, which they’d love to get rid of. And of course, it’s cheaper for businesses to use digital currencies. Most countries in Europe don’t use physical currency anymore—it’s credit cards only.

Q: Do you expect Tesla (TSLA) to pop after earnings?

A: I have no idea; it depends on what the report says but suffice it to say that Tesla is historically cheap. It has the lowest PE multiple now than it has in the entire 13-year history of the company. Scale in on the LEAPS with Tesla—that’s what I’d be doing down here.

Q: Could the US debt situation spiral into something that gets out of hand?

A: No, because the purchasing power of debt is now deflating at an 8.4% annual rate, which means that it goes to zero in about 8.57 years. This is how the government always wins when issuing debt. It’s been going on since the French first issued government debt 300 years ago. Who pays for that? Bond investors. Anybody who owns bonds now has seen their purchasing power go up in smoke. That’s why it’s been a one-way zero bid market for two and a half years—they’ve been dumping like crazy.

Q: Should I buy debt here or sell it?

A: We’re actually getting close to a bottom in the junk debt market, which means you’re going to be yielding around 10%. That means the value of your holding doubles in 6 years, and the default rates never reach the high levels predicted by analysts in junk bonds. That has always been the key to junk bonds in the whole 50 years that I've been following this market. My neighbor up in Tahoe, Mike Milliken, made billions off that assumption.

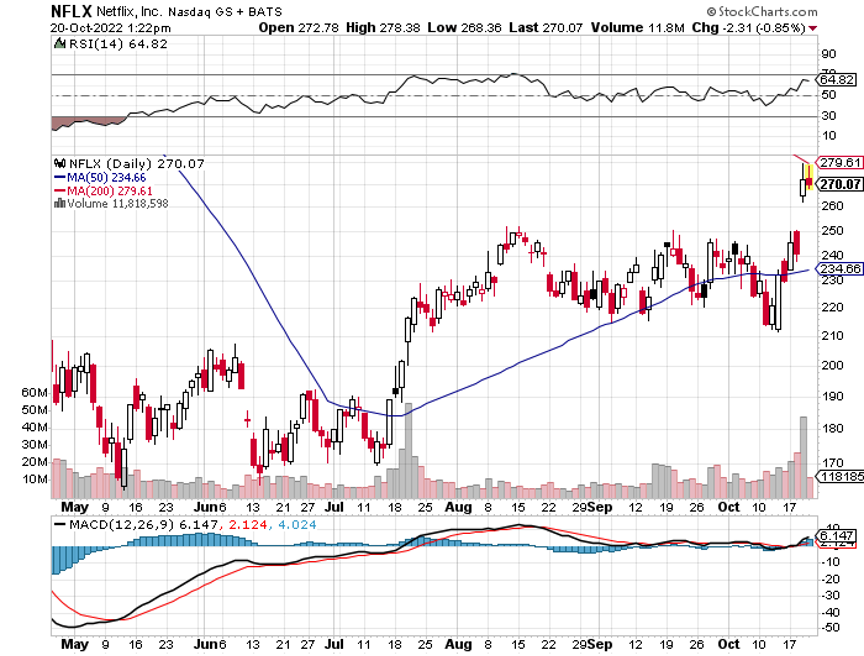

Q: What do you think about Netflix (NFLX)?

A: Well, my advice was to buy it, to a lot of people. They’re clearly changing their business model for the better—they’re going to start picking up ad revenues, they’re cracking down on password sharing, and they delivered a 20% return in stocks. Plus their share price has just dropped down from $700 to $165. Great LEAP candidate here.

Q: What kind of position is best if a recession hits?

A: Cash. Cash is now yielding 4.4%. The best cash alternative is 90-day T-bills issued by the US Treasury. Execution costs almost zero, and liquidity is essentially infinite; but, remember also that bull markets start 6 to 9 months before recessions end. You just have to watch your timing. Which means that if the recession ends in say July, you have to be buying stocks today. Just keep that in mind, ladies and gentleman.

Q: How do you see the futures of semis?

A: Anything you buy here now will triple in three years, but it becomes a question of how much pain you want to take in the meantime. Everyone in the investment management industry thinks the same, and it really is a classic “catch-a-falling-knife” situation— knowing that the payoff down the road is enormous. Virtually all companies are designing new semis into their products at an exponential rate.

Q: Are LEAPS part of the service?

A: Yes, they are. I will send you one tomorrow. But concierge customers get first priority because that’s what they’re paying for.

Q: How far out should we go?

A: On LEAPS, always take the maximum maturity, which is usually 2 years and 4 months. And the reason is that the second year is almost free—they charge you almost nothing for going out to maximum maturity. And if we have a recession that does last longer than people think, that extra year of maturity will be worth its weight in gold. It’ll be the difference between a zero return and a 10x return.

Q: Can we go back into the ProShares UltraShort 20+ Year Treasury (TBT)?

A: No, it would be a horrible idea to buy the (TBT) here after it just moved from $14 to $36. That’s what you buy before it goes from $14 to $36. We’re topping out in all of these short bond plays, so avoid them like the plague.

Q: How much is the Concierge Service?

A: It’s $12,000 a year—and a bargain price at that! Almost everybody ends up covering that on their first trade, and you get an entire portfolio of LEAPS and a dedicated LEAPS website with the service. You also get my personal cell phone number so you can call me while I'm either on the beach in Hawaii or on the ski slopes of Lake Tahoe. If anyone has questions about the concierge service, contact customer support at support@madhedgefundtrader.com.

Q: What are your thoughts on data analytics companies Snowflake (SNOW) and Palantir (PLTR)?

A: Love Snowflake, hate Palantir because the CEO isn’t interested in promoting a share price. With (SNOW), you have Warren Buffet as a major holder, so that’s all you need to know there. (SNOW) also has a 75% fall behind it.

Q: Thoughts on the Ukraine/Russia war?

A: It’ll drag on well into next year, and obviously the Iranian drones are the new factor here. I wouldn’t be surprised if there were suddenly an accident at a certain factory in Iran; that’s what happens when these things play out.

Q: Is Snowflake (SNOW) a buy right now?

A: It’s like all the rest of tech. High volatility, could have lower lows, but long-term gains are at least a triple from here. You know how much risk you can take.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Dungeon in Montreux Castle on Lake Geneva in Switzerland

https://www.madhedgefundtrader.com/wp-content/uploads/2022/10/john-thomas-Montreux-Castle--e1666366030403.jpg550361Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-10-21 09:02:112022-10-21 11:12:04October 19 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the October 5 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: Is the final low in, or could we retest yet again (SPY)?

A: We could retest yet again, but it’s very important to notice that the marginal new lows are very small. The low we had on Friday, the last day of September and Q3, was only 800 points lower than the low we had in June—you had to work 4 months just to get a new low of only 800 points. So I think that's the way it's going to go. If we do get new lows, it’ll be incremental new lows—we’re not crashing to 3,000 or anything like that.

Q: What do you think Tesla (TSLA) will bottom at in the short term?

A: $200 or $210. The Tesla deal is a disaster for Elon Musk. It will amount to a huge diversion of management time; he’s going to be facing regulatory hurdles, and even though he said we’re going ahead for the deal, a lot of people still don’t believe it because the financing for the deal may have vaporized in the massive increase in interest rates that has occurred since February. So, there are still a lot of non-believers in this deal. I’d rather have him making solar panels, electric cars and launching rockets, not getting into the social media morass and taking over a broken company. The shareholders clearly don’t like it either, taking the shares down $30 in two days. By the way, if you look at the charts, you notice that people were front-running the Twitter deal by dumping Tesla stock the day before. So yes, it kind of peed on our Tesla parade for the short term; long term it keeps going up and the bad news is in the price.

A: No, not the long-term ones, just the short-term ones.

Q: Is it possible that bonds are bottoming here, even if we expect further Fed rate rises?

A: Yes, the Fed only has control of overnight rates, and those are rising. In fact, overnight rates are now higher than 10-year rates, and could go much higher still—that's called inversion of the yield curve. We’re almost certainly getting another 150-basis point rise in overnight rates. 10-year bonds or 20-year bonds could well stay around this level, or maybe just a little bit lower. So yes, the bond short is gone. It worked great for us for 2.5 years, we caught a 43% decline in the TLT, but it’s game over. Time to find other trades, like buying stocks.

Q: Does Elon Musk have to sell more Tesla to buy more Twitter?

A: That is the big question being asked today because he already sold $16 billion worth of stock in Tesla to cover the Twitter purchase this year. With the debt markets having fundamentally changed in the last 6 months, the question is: does he have to raise more equity (i.e. sell more Tesla), or can he bring in other equity investors? Hopefully, if he does have to sell more Tesla, it’s not very much—it’s a $44 billion deal and he’s already put $16 billion into it, so maybe he raises another $6 billion to get up to a 50% control level, which the market can easily handle in a day or two. He’s handled all of his past Tesla share sales fairly easily, and he tends to do these at market tops when demand for the shares is overwhelming. Longer term, the much greater demand for selling Tesla shares will come from the equity raises he will need to do to build another six Tesla factories around the world. That could be anywhere from $400 billion to $800 billion, so that will be the much larger cash call, but those are years off at best.

Q: With so many big techs breaking down, how should we play the (ROM) (ProShares Ultra Technology ETF)?

A: From the long side is how you play it. But you really need these capitulation days, especially if you’re involved in 2X ETFs. There is a spectacular play setting up for the (ROM) because it’ll go from $24 (or whatever the final bottom is) to $100 in the next upcycle, so that is a great leverage play that you really want to get involved in.

Q: If I don’t have time to babysit my portfolio, am I better in LEAPS or physical stocks?

A: Well the LEAPS I’m putting out now have a 2 years 4 months expiration date, so you can literally just buy them and forget about them. On the other hand, if we don’t get an economic recovery in 2 years and 4 months, you’re better off buying stocks outright on 2:1 margin. You make less profit, but if we don’t get a recovery for 3, 4, 5 years, then you have no expiration problem with stocks, as opposed to with LEAPS. Now, there are ways to trade around your LEAPS, like financing the long and by shorting puts and getting in for zero, but that requires smaller positions because you have to maintain the margin for the short put side. So, if you want to play it safe, buy the stocks. You can even handle a lost decade with stocks, especially if their dividend pays. With LEAPS, you need a fairly immediate economic recovery, which we should get, especially if the Fed lowers interest rates next year, which it should.

Q: What is your view on the US dollar (UUP)?

A: The dollar seems close to peaking right around here. It will peak on the last day that the Fed raises interest rates, which could be on December 14th. In fact, they may not even wait until then. Depending on the inflation rate, they could only do a quarter or a half-point rate rise in December, thus giving the market their signal that way. Or not do it at all, and the sudden selloff that we had in the dollar, and the stabilization of bonds we had last week is telling you that’s on the table as a possibility. So, we saw really important moves for long-term trend considerations in the markets since last week.

Q: Time for Palantir (PLTR)?

A: No, because the CEO doesn’t give a damn about his stock, and the stock reacts accordingly. I gave up on Palantir for that reason.

Q: How do you see the Ukraine/Russia situation developing?

A: It drags on for another year, Russia keeps losing and throwing men into the meat grinder until Putin gets removed, which should happen next year at which point oil prices collapse. That may be why he blew up the Nordstream One pipeline, to tie the hands of a future Russian government.

Q: Is it safe to buy 30-day Treasury bills in November going into the next F1C meeting?

A: Yes, because they essentially have no risk—that’s basically a cash type investment. And if your broker goes bust you can just force them to hand over your Treasury bonds and not get tied up in any three-year bankruptcy proceeding. It’s an asset, not cash.

Q: Will it be time to buy LEAPS on the next market selloff?

A: Absolutely, yes.

Q: Do you believe Putin would use nukes?

A: No I don’t, because the radioactive cloud would fall back on him immediately. There are very few people who are both stock market experts and nuclear weapons experts; I happen to be one of those—probably the only one in the world in fact—because of my time spent with the atomic energy commission at the Nuclear Test Site in Nevada. The problem with bombing your next-door neighbor with nukes is that the nuclear fallout comes right back on you the next day. Most of Russia’s nukes don’t even work, they only have a handful that actually does, and if he does use one, I bet it would be a tiny one just to demonstrate that he has a working nuke—like just a one-megaton one as opposed to Hiroshima which was 20 kilotons. Or he could drop it in the Black Sea or do an above-ground test at their old nuclear test site that wouldn’t kill anyone, just to show that he has working nukes. I don’t think he will, because we would react in kind in twice the size.

Q: Time to buy ARK Innovation ETF (ARKK)?

A: You might start with a small starter position, just to get it into your portfolio so you remember to buy it on the next dip. Cathy Woods’s leverage in this fund is tremendous. You really want to own it at a market bottom, but picking the actual bottom is going to be tough. One way to achieve this is to just go out and buy Tesla—that way you don’t have to pay the management fee—or buy the top 5 holdings in ARK directly, which includes Roku (ROKU) among others. So yes, I’m watching it; I prefer buying things on the way up and missing the first 10% than to catch a falling knife, and boy has this thing been a falling knife this year.

Q: Do you like biotech here?

A: Absolutely; please subscribe to the Mad Hedge Biotech Letter for biotech recommendations plus LEAPS on biotech plays by clicking here.

Q: Energy is still the best sector now?

A: Yes, but for how long? You don’t want to be left standing when the music stops playing, and that is imminent in the oil industry. It will be illegal to sell gasoline cars in California after 2035, and gas makes up half the oil use in the US.

Q: Did you know that oil reserves (USO) are the lowest since 1984?

A: Yes, I think you may have read that in my newsletter, and that’s because of Biden’s efforts to reduce US gasoline prices through a million barrel per day release from the strategic petroleum reserves in Texas and Louisiana. If we are a net energy producer, why do we even have reserves? It’s an out-of-date holdover from the Cold War.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Tokyo 1975

https://www.madhedgefundtrader.com/wp-content/uploads/2022/10/john-thomas-mount-everest.jpg322238Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-10-07 09:02:352022-10-07 12:20:40October 5 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the February 2 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, Nevada.

Q: Thoughts on Palantir Technologies Inc. (PLTR)?

A: Well, we got out of this last summer at $28 because the CEO said he didn’t care what the share price does, and when you say that, the market tends to trash your stock. But Palantir is also in a whole sector of small, non-money-making, expensive stocks that have just been absolutely slaughtered. And of course, PayPal (PYPL) takes the prize for that today, down 25% and 60% from the top. So, we’re giving up on that whole sector until proven otherwise. Until then, these things will just keep getting cheaper.

Q: Given the weakness in January, do you think we still have to wait until the second half of the year for a viable bottom?

A: Definitely, maybe. If things are going to happen, they are going to happen fast; we got the January selloff, but that’s nowhere near a major selloff of 20%. And the fact is, the economy is still great so that’s why this is a correction, not a bear market. At some point, you want to buy into this, but definitely not yet; I think we take another run at the lows again sometime this month. We just have to let all the shorts come out and take their profits so they can reestablish again.

Q: Why are bank stocks struggling?

A: A lot of the interest rate rises that we’re getting now were already discounted last year—banks had a great year last year—so they were front running that move, which is finally happening. To get more moves out of banks, you’re going to have to get more interest rate rises, which we will get eventually. We still like the banks long term, we still like financials of every description, but they are taking a break, especially on the “sell everything” index days. A lot of the recent selling was index selling—banks have a heavy weighting in the index, about 15%. So, they will go down, but they will also be the ones that come back the fastest. We’re seeing that in some of the financials already, like Berkshire Hathaway (BRKB) and Morgan Stanley (MS) which are both close to all-time highs now.

Q: What about the situation with Russia and Ukraine?

A: It’s all for show. This is a situation where both the US and Russia need a war, or threat of a war, because the leaders of both countries have flagging popularity. Wars solve those problems—that’s why we have so many of them by the United States. We’ve been at war essentially for most of the last 40 years, ever since Ronald Reagan came in.

Q: I didn’t exit my big tech positions before the crash, should I just hang onto them at this point?

A: The big ones—yes. The Apples (AAPL), the Googles (GOOGL), the Amazons (AMZN) —they’re only going to drop about 20% at the most, maybe 25%, and then they’ll go to new highs, probably before the end of the year. If you’re good enough to get out and get back in again on a 20% move, go for it. But most people can’t do that unless they’re glued to their screens all day long. So, if you have stock, keep the stock; if you have options, get out of the options, because there the time decay will wipe you out before a turnaround can happen. This is not an options environment, unless you’re playing on the short side in the front month, which is what we’re doing.

Q: When you send out the trade alerts, I have a hard time getting them executed. How do you advise?

A: Move the strike price, go out in maturity, and you can get our prices at slightly higher risk. Or, just leave it and, quite often, people’s limit orders get done at the end of the day when the algorithms have to dump their positions at the close because they’re not allowed to carry overnight positions. Also, even if you get half of my trade alerts, you’re doing pretty good—we’re running at a 23% rate in 6 weeks, or 200% annualized. And remember, when I send out a trade alert, you’re not the only one trying to get in there, so you can even go onto a similar security. If I recommend Alphabet (GOOGL), consider going over to Microsoft (MSFT), because they all tend to move together as a group.

Q: I am sitting on a 16% profit in the ProShares Ultra Technology (ROM), which you recommended. Should I take the money and run, and get back in at a lower price?

A: Yes, this is just a short covering rally in a longer-term correction, and you make the money on the volume. You win games by hitting lots of signals, not hanging on to a few home runs where people usually strike out.

Q: You said inflation will be short lived, so why would there be 9 interest rates after the initial 4?

A: It’s going to take us 8 interest rates just to get us back to the long-term average interest rate. Remember the last 2% is totally artificial and only happened because there was a financial crisis 13 years ago. So, to normalize rates you really need to get overnight rates back up to about 3.0%. And that means 12 interest rate hikes. If you don’t do that, you risk inflation going from controllable to uncontrollable, and that is the death of the Fed. So, that’s why I expect a lot more interest rate rises.

Q: Will the tension between Russia and the Ukraine affect the market?

A: No, it hasn’t so far and I don’t expect it to. Although, it’s hard to imagine going through all of this and not seeing a shot fired. When that one shot gets fired, then maybe you get a down-500-point day, which it then makes back the next day.

Q: Anything to do with Alphabet (GOOGL) announcing its 20 to one split?

A: No, it’s too late. We had a trade alert out on a Google 20 call spread which we actually took profits on this morning. So, nice win for the Mad Hedge Technology Letter there. There’s nothing to do with these splits, it’s not like they’re going to un-announce it, this isn’t a risk-arbitrage situation where there’s always an antitrust risk hovering over the deal that may crash it. This is pretty much a done deal and doesn’t even happen until July 1. People think bringing the share price from $3,000 down to $150 makes it available for a lot more potential retail buyers, which it does. It also makes call spreads on the options a lot cheaper too. When we put out these alerts, we can only do one or two contracts, even tying up $10,000—divide that by 20 and all of a sudden your cheapest Google call spread cost $500 instead of $10,000.

Q: Can you speak about the liquidity on your strikes? Sometimes we’re trading against strikes that have no open interest.

A: Whenever you put in an order for one strike, even if there’s nothing outstanding on that strike, algorithms will arbitrage against that strike—where your order is—against all the other strikes on the whole options chain. So, don’t worry if you have limited open interest or no open interest on our trade alerts. They will get done, and it may get done by some algorithm or some market maker taking more of another strike, that’s how these things get done. It’s all thanks to the magic of computers.

Q: Do you have thoughts about Freeport-McMoRan (FCX)? I have some profitable LEAP positions open.

A: It’ll go higher, keep them. And I like the whole commodity space, which means iron ore (BHP), copper, steel (X), etc.

Q: Would you trade Barclays iPath Series B S&P 500 VIX Short-Term Futures ETN (VXX) at this point?

A: No, because we’re dead in the middle of the recent range. That’s a horrible place to enter—you only enter (VXX) on extremes on the upsides and the downside.

Q: What should I do about Airbnb (ABNB) at this price? They’ve been profitable for 2-3 years, with revenues rising.

A: I think Airbnb is one of the best run companies in the world, and I expect their earnings to keep growing like crazy, especially once we get out of the pandemic. I am also a very frequent Airbnb user, having stayed in Airbnb’s in at least 10 countries, so I’m a big fan of them. The stock just got dragged down by the small tech bust but it will come back. This is a “throwing the baby out with the bathwater” situation.

Q: Are there any good LEAPS candidates now?

A: I’m not doing any LEAPS until we reach the final cataclysmic selloff of the correction. Otherwise, the time value will run against you enormously; I’d rather wait for better prices.

Q: Do you see a cataclysmic selloff?

A: Yes, I do. Maybe in a few more weeks, and maybe next week if we get a really hot 8%+ inflation rate—that would really kill the market.

Q: What will tell you if inflation is ending or slowing labor?

A: Labor is 70% of the inflation calculation. So, when these huge pay awards slow down, that's when inflation slows down. By the way, a lot of pay increases that are happening now are catch-up from the last 40 years of no pay increases for American workers in real inflation adjusted terms. So, a lot of this is catch-up—once that’s done, you can forget about inflation. Also, the long-term pressure of technology on prices is downwards, so allow that to reignite deflation, and that will be your bigger issue over the long term.

Q: What should I do about Editas Medicine Inc (EDIT) or CRSPR Therapeutics AG (CRSP)?

A: Don’t touch the sector, it’s out of favor. Let this thing die a slow death. When they come up with profitable products, that’s when the sector recovers. So far, everything they have works in labs but there are no mass-produced Crispr products, they’re trying for mass production on sickle cell anemia and a couple of other things, but still very early days in CRSPR technology.

Q: When will this recording be posted?

A: In two hours, it will be posted on the website. Go to “My Account” and you’ll find the last 13 years of recorded webinars.

Q: What do you mean by “stand aside from Foreign Exchange”?

A: The volatility in the foreign exchange market is just so low compared to equities and bonds, it’s not worth trading right now. When you can trade everything in the world—foreign exchange is at the bottom of the list. If I see a good entry point, I’ll do a trade; but do I trade Tesla (TSLA) with a volatility of 100%, or foreign exchange with a volatility of 5%? Those are the choices.

Q: Should I do any short plays in oil (USO)?

A: Generally, you don’t want to short any commodity unless you're a professional; I say that having been short beef futures when Mad Cow Disease hit in 2003 and you had three limit-up days in a row in the futures market. That happens in the commodity areas—liquidity is so poor compared to stocks and bonds that if you get caught in one of these one-way moves, you can’t get out. So that is the risk; and I’ve known people who have gone bust trading oil both long and short, so this is for professionals only. With stocks you get vastly more data and information than you do in the commodity markets where industry insiders have a much bigger advantage.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Aga Sophia Mosque in Istanbul

https://www.madhedgefundtrader.com/wp-content/uploads/2022/02/john-thomas-in-instanbul.png560420Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-02-04 11:02:562022-02-04 14:06:17February 2 Biweekly Strategy Webinar Q&A

Investors shouldn’t stress too much about the drop in Palantir stock.

It’s still a great company that is on pace to do what it promised — achieve annual revenue growth of 30% or more through 2025.

In fact, they will easily surpass those projections, and any of these mini pullbacks that we are seeing now is just a matter of not fulfilling sky-high expectations and coming in a tad below that.

I can accept that and so should you.

Why is this data analytics company so great?

It is the connective tissue that connects analytics to operational systems which leads to winner business decisions.

Such architecture offers enterprises with action APIs that allow first model and simulate, and second, orchestrate and execute complex cross-functional transactions.

As the health crisis limited visibility and indicators, many started to trust the power of Palantir’s platforms and installed the technical infrastructure, to translate that into coordinated, orchestrated actions in the operations of their business.

Credit should go to Palantir’s developers who created a secret sauce to supercharge earlier-stage companies, enabling them to deliver a central operating system for their data and to scale rapidly from day zero.

These companies, they're not just managing their data and their operations, they are wielding them to blitz, scale, and conquer at a devastating rate.

Palantir’s clients originate from a diverse set of industries and continue to partner with innovative companies across industries such as automotive, biotech, healthcare, media, and the government.

Now, they are generating major product innovation that extends the openness and flexibility of their infrastructure for developers calling it Operational APIs or OPIs for short.

This liberates the ontology to serve as a nervous system, the cardiovascular system of the enterprise as a unified action and orchestration layer.

This manifests itself in a way that inventory can be allocated, production can be scheduled, orders can be fulfilled. To accomplish these deceptively simple actions requires communication with potentially tens of source systems transactionally.

Palantir allows you to orchestrate complex cross-system decisions to win and turn market disruption into competitive glory.

For example, a large industry company is unlocking value by integrating Microsoft Power apps with the Palantir Foundry platform. This powers workflows and writing data back to external operational and transactional systems

State defense contracts have been hyper-lucrative to PLTR.

PLTR has demonstrated its usefulness in the production of the A320 of RAM pickup trucks, auto parts, PPE, and tractors. PLTR can leverage its technology so customers can do it better, faster, and cheaper.

It’s a win-win for everyone.

And the defense industrial base is seeing that it can have the same impact on the production of fighter jets, naval ships, and land vehicles.

Lastly, their dealing in healthcare is shooting through the roof with cornerstone partnerships with the NHS, MD Anderson Cancer Center, 70 academic medical centers through the NIH's N3C, the Department of Veteran Affairs, and even more regional US providers means that PLTR is helping to manage over 300 million patient lives and growing.

Complex clinical care continues to be the recipient of cutting-edge products and continued innovation.

It’s not surprising that PLTR’s US commercial revenue growth accelerated once again to 103% year over year and this flavor of business offers the longest runway for PLTR to grow.

They more than doubled their commercial customer count.

Palantir management guided us to 34% growth in government revenue during the third quarter, while this segment was up 66% in the second quarter, but I believe this is highly misunderstood.

Just the nature of working with the government, the bureaucracy, and the single entity nature of it, deals aren’t going to be flying in left and right.

There is a processional nature to working with the US government because its such a monolith.

The more salient story here is the in-roads of the commercial business which will turn into its core identity.

The commercial business will be the x-factor driving PLTR into surpassing its revenue promises, and investors will acknowledge that as commercial revenue begins to overpower the defense contracts.

Revenue for the full year is expected to be about $1.53 billion or 40% year-over-year growth which conspicuously gets over any bar that tech growth companies are expected to jump over.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/11/palantir.png388920Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-11-10 15:02:212021-11-17 01:06:18Data Analytics at Its Finest

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-10 10:04:292021-09-10 12:21:31September 10, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.