Mad Hedge Technology Letter

April 24, 2024

Fiat Lux

Featured Trade:

(RUNNING ON FUMES)

(ARKK), (NVDA), (ROKU), (TSLA)

Mad Hedge Technology Letter

April 24, 2024

Fiat Lux

Featured Trade:

(RUNNING ON FUMES)

(ARKK), (NVDA), (ROKU), (TSLA)

This is a story of how important it is to accurately time the tech business cycle and to unload winners when they run dry.

I am talking about Cathy Wood’s ARKK (ARKK) fund and how it has suddenly gone south with no savior in sight.

The beginning of every tech innovation cycle is usually the best time to invest in “innovation” partly because this point in time also coincides with low interest rates.

Rates were historically low for a long time and ARKK did well.

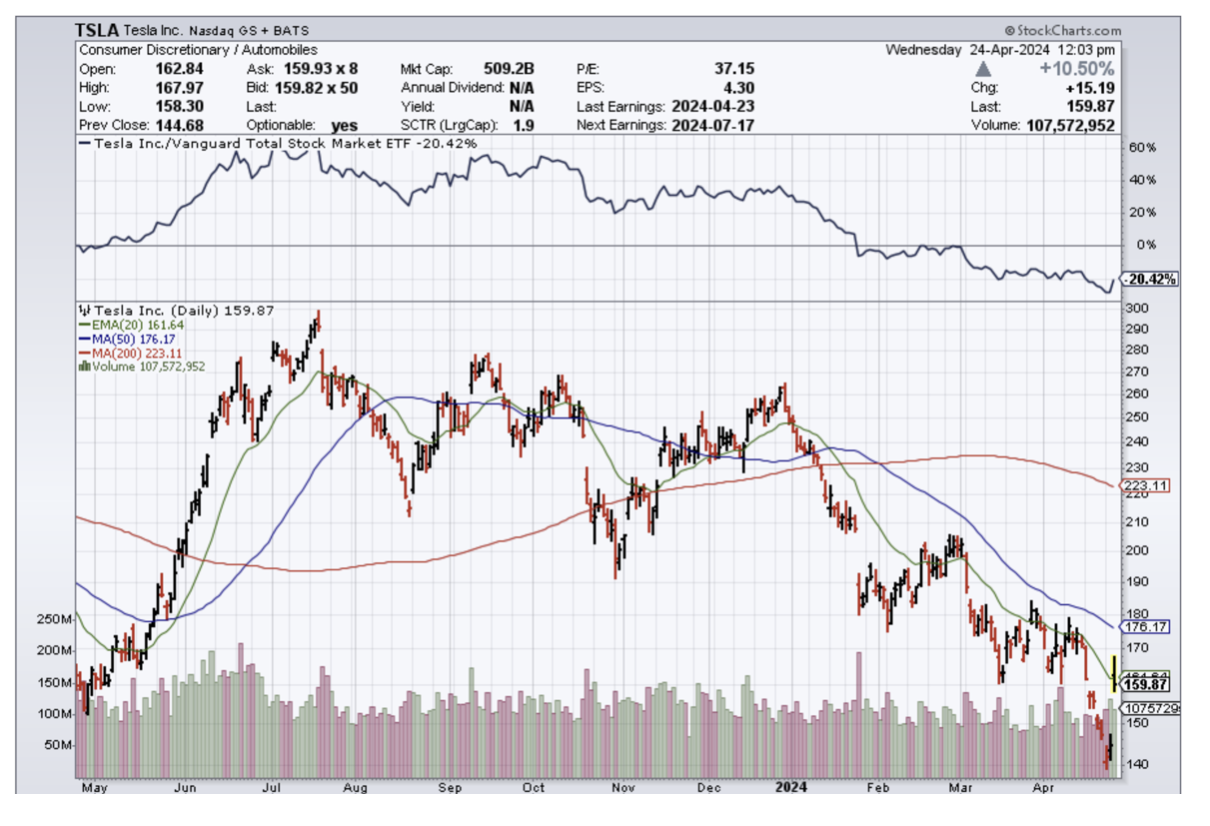

Many of these tailwinds have now gone in complete reverse and Wood’s biggest position Tesla (TSLA) is feeling the brunt of it.

Tesla issued a poor earnings report yesterday, but CEO Elon Musk turned around the price action by chronicling how Tesla is about to roll out cheaper cars.

Cheaper EVs play into the hands of the Chinese who can do it a lot cheaper for better quality.

Fighting the Chinese at its own game is a fool’s errand.

I believe the 12% pop today is largely due to algorithmic buying and when traders see through this empty strategy, it will usher in the next down leg for Tesla and one of its largest positions.

One of ARKK’s other large positions is in ROKU (ROKU) which navigates the streaming sub-sector.

Streaming, aside from Netflix (NFLX), has gone nowhere lately as prices for consumers have skyrocketed but services haven’t improved.

Growth has saturated is the end result.

It’s gone from bad to worse.

It’s a far cry when investors rushed into her funds and it won big during the pandemic when the star fund manager became a social-media sensation by making bold bets on disruptive technology stocks such as Tesla, Zoom Video Communications, and Roku.

Investors have pulled a net $2.2 billion from ARK Investment Management this year, a withdrawal that dwarfs the outflows in all of 2023. Total assets in those funds have dropped 30% in less than four months to $11.1 billion—after peaking at $59 billion in early 2021, when ARK was the world’s largest active ETF manager.

Loyal shareholders have become disillusioned and this should be a better year for the ARK style of investing in growth and disruptive technology, but they are concentrated in companies that have underperformed.

By the end of last year, ARK funds had destroyed more wealth than any other asset manager over the previous decade, losing investors a collective $14.3 billion.

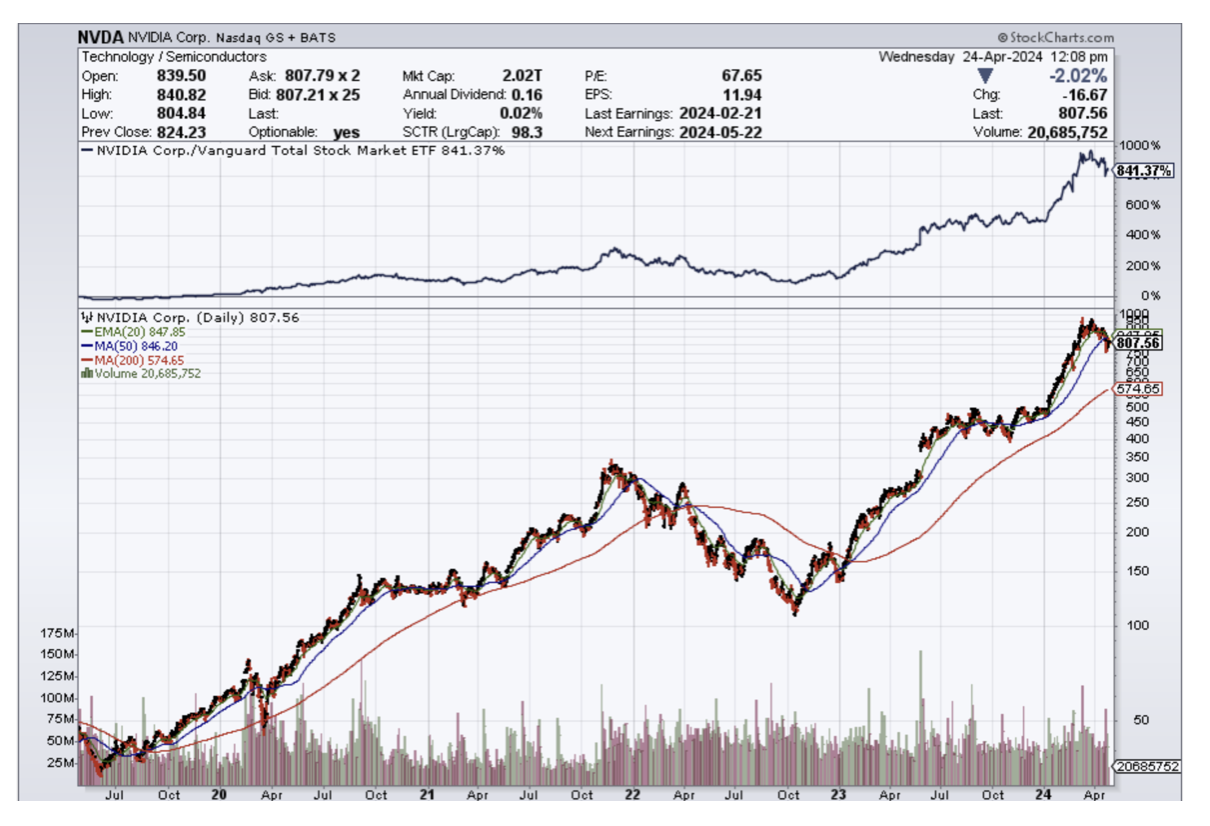

Nvidia’s absence in ARK’s flagship fund has been a particular pain point. The innovation fund sold off its position in January 2023, just before the stock’s monster run began. The graphics chip maker’s shares have roughly quadrupled since.

Wood, a longtime proponent of cryptocurrency, has done better standing by her bet on crypto exchange Coinbase Global, whose shares have quadrupled over the past year. The stock is still down 47% from its peak in 2021.

The ARKK ETF has lost 75% of its value since 2021 which has infuriated investors who thought they could chase innovation to sky-high valuations.

The ETF languishing in the doldrums represents Wood’s inability to innovate her trading philosophy and grapple with the reality that we are in a very late cycle in tech and blowing one’s wad on some pie-in-the-sky dream isn’t going to cut it in 2024.

Still with the robust business models that can weather high interest rates and high inflation.

Mad Hedge Technology Letter

March 15, 2023

Fiat Lux

Featured Trade:

(THE UNKNOWN IN THE DIGITAL AD SPACE)

(NFLX), (WBD), (DIS), (CMCSA), (ROKU)

The uncertain digital advertising environment has been a thorn in the side of legacy media giants for quite some time.

Companies from Comcast (CMCSA) to Warner Bros. Discovery (WBD) are feeling the pressure as profitability struggles pile up.

Unfavorable macroeconomic headwinds coupled with decreased ad budgets amid a decline in linear TV and digital search trends put the ad market through the wringer in 2022.

Recent ad market softness comes as media giants like Disney (DIS) and Netflix (NFLX) have embraced ad-supported streaming alternatives as the race for eyeballs escalate.

Disney's direct-to-consumer division lost an eye-popping $4 billion-plus in 2022.

Warner Bros Discovery is now targeting $4 billion in cost savings over the next two years.

Advertising revenue within NBCUniversal's media division increased by 4% in Q4 because of a boost from the incremental revenue from the FIFA World Cup.

Looking ahead, the lack of brand name events in 2023 such as the World Cup, Olympics, or U.S. midterm elections, will likely be a drag on ad spend in 2023.

Those events greatly aided the battered industry with the domestic ad market totaling $318 billion last year — an increase of 8% compared to 2021.

Similarly, Spotify (SPOT) CFO Paul Vogel told investors during the latest earnings call: "Advertising in Q4, overall, it's definitely continued to be very up and down."

Spotify's Q4 ad-supported revenue, boosted by podcasting, grew 14% on a year-over-year basis to €449 million — accounting for 14% of total revenue.

Disney and Netflix rolled out their ad tier products at a time when the ad market is in flux, but the move seems to have been a lucrative one.

At the time of the debut, the company said over 100 advertisers bought inventory for the launch — bucking the trend of a global ad spend slowdown.

Similar to Disney, Netflix is playing the long game when it comes to its recently launched ad-supported tier, which officially debuted in November.

In its latest shareholder letter, Netflix said engagement for ad-supported subscribers "is consistent with members on comparable ad-free plans, is better than what we had expected, and we believe the lower price point is driving incremental membership growth."

Investors should run to higher grounds to avoid the upcoming slaughter in legacy media.

The cord cutter phenomenon is real and the pivot to work-from-home culture has really stuck the fork in many traditional services that used to be part of American culture.

Legacy media is one of the big losers – nobody watches analog television anymore.

Investors will need to seek attractive properties such as NFLX to buy the dip.

They benefit from the first mover advantage, but Disney is also finding their way after firing former CEO Bob Chapek and replacing him with the guy before him - Bob Iger. It’s not a pure streaming play which is also an issue for the likes of Amazon and I do think Roku is a little too growth based at this point in the business cycle.

The overall message is to avoid unproven tech assets for the time being with bank turmoil and interest rate tumult.

The only exceptions are active traders who use volatility in their favor and play from the long and short side. Traders usually don’t discriminate and can jump in and out of these sharp movements.

If traders want to get into streaming or social media stocks, that is fine, but stick with the brand names and shun the exotic names for now.

Mad Hedge Technology Letter

November 9, 2022

Fiat Lux

Featured Trade:

(RISKY BUSINESS)

(ARKK), (SARK), (ROKU), (TSLA)

Tech growth is a sub-sector that readers really need to stay away from right now.

It’s toxic for the time being.

We are still right in the middle of the Fed Funds rate hike cycle and the pounding has been relentless with former tech darlings breaking records for lower lows.

The poster child for the excesses in tech growth is Cathie Wood who is the CEO of ARK (ARKK) innovation funds.

She has completely ignored “market timing” and has used every brash sell-off to go big without doing much research.

This strategy has proven to be highly unsuccessful, as many of her top holdings like Tesla are again in free fall.

CEO of Tesla Elon Musk just sold $4 billion of stock to divert into his new company Twitter which lost a massive amount of advertising revenue when he took over.

Yesterday, crypto experienced an unbelievable meltdown when the 2nd largest exchange FTX once valued around $35 billion was and still is on the brink of bankruptcy.

The same day Wood bet the ranch on crypto exchange Coinbase (COIN) adding 420,949 shares of COIN to the current 7.7 million that ARK Investment Management currently holds.

Bitcoin is down 13% at the time of this writing, representing yet another giant flop for Wood.

Wood is performing highly risky moves at the peak of turmoil in an industry that many think is a Ponzi scheme.

Her exploits are so infamous that it now has an inverse ETF that tracks the opposite of what she decides and performance has been stellar.

That ETF, called AXS Short Innovation Daily ETF (SARK), has soared more than 111% since launching a year ago. That’s the second best performance among the nearly 450 ETFs that launched over the past year.

Wood’s second biggest position is ad tech firm Roku (ROKU) which has gone from $460 to $48 today.

SARK’s first-year performance is among the 20 best of all-time measured against funds that are still trading.

Wood’s poor performance represents the pitfalls of choosing an investment adviser when they are one-dimensional and unable to acknowledge initial mistakes.

Instead of adjusting a flawed strategy, she has used it as the impetus to double down on a bad strategy.

The best hedge fund managers know when they are wrong and quickly reverse course or cut their losses.

Wood’s failures are quickly dealt with by blaming others, routinely saying that others “don’t do their research.”

Wood’s propensity to hype up tech like there is no tomorrow is now directly working against her.

She views any and every selloff as a brilliant entry point while ignoring broader market fundamentals.

In short, the day Cathie Wood is bearish is the day to go big into tech shares, because there are likely no more incremental buyers willing to hold the bag.

Truth be told, the Nasdaq currently sits 35% down from its November 2021 peak a year on.

I would call that pretty good, considering we are deleveraging from the biggest man-made financial bubble that was ever created in financial markets.

The bubble has caused the US Federal government to shoulder more than $31 billion of government debt that needs to be serviced with constant interest payments.

The only reason why tech shares are down 35% is because every investor believes the US Central Bank will kick the can down the road and save corporate America when push comes to shove.

This is precisely why recent bear market rallies have been epic, and any scintilla of interest rate loosening talk is met with thunderous buying.

If investors were more scared of the Fed, tech shares would be down at least 60% by now.

Global Market Comments

October 7, 2022

Fiat Lux

Featured Trade:

(OCTOBER 5 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (TSLA), (PLTR), (UUP), (ROM), (USO), (ARKK), (ROKU)

Below please find subscribers’ Q&A for the October 5 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: Is the final low in, or could we retest yet again (SPY)?

A: We could retest yet again, but it’s very important to notice that the marginal new lows are very small. The low we had on Friday, the last day of September and Q3, was only 800 points lower than the low we had in June—you had to work 4 months just to get a new low of only 800 points. So I think that's the way it's going to go. If we do get new lows, it’ll be incremental new lows—we’re not crashing to 3,000 or anything like that.

Q: What do you think Tesla (TSLA) will bottom at in the short term?

A: $200 or $210. The Tesla deal is a disaster for Elon Musk. It will amount to a huge diversion of management time; he’s going to be facing regulatory hurdles, and even though he said we’re going ahead for the deal, a lot of people still don’t believe it because the financing for the deal may have vaporized in the massive increase in interest rates that has occurred since February. So, there are still a lot of non-believers in this deal. I’d rather have him making solar panels, electric cars and launching rockets, not getting into the social media morass and taking over a broken company. The shareholders clearly don’t like it either, taking the shares down $30 in two days. By the way, if you look at the charts, you notice that people were front-running the Twitter deal by dumping Tesla stock the day before. So yes, it kind of peed on our Tesla parade for the short term; long term it keeps going up and the bad news is in the price.

Q: How do we get the concierge service?

A: Just contact customer support at support@madhedgefundtrader.com or call (347) 480-1034.

Q: Have you revised Tesla’s (TSLA) price target?

A: No, not the long-term ones, just the short-term ones.

Q: Is it possible that bonds are bottoming here, even if we expect further Fed rate rises?

A: Yes, the Fed only has control of overnight rates, and those are rising. In fact, overnight rates are now higher than 10-year rates, and could go much higher still—that's called inversion of the yield curve. We’re almost certainly getting another 150-basis point rise in overnight rates. 10-year bonds or 20-year bonds could well stay around this level, or maybe just a little bit lower. So yes, the bond short is gone. It worked great for us for 2.5 years, we caught a 43% decline in the TLT, but it’s game over. Time to find other trades, like buying stocks.

Q: Does Elon Musk have to sell more Tesla to buy more Twitter?

A: That is the big question being asked today because he already sold $16 billion worth of stock in Tesla to cover the Twitter purchase this year. With the debt markets having fundamentally changed in the last 6 months, the question is: does he have to raise more equity (i.e. sell more Tesla), or can he bring in other equity investors? Hopefully, if he does have to sell more Tesla, it’s not very much—it’s a $44 billion deal and he’s already put $16 billion into it, so maybe he raises another $6 billion to get up to a 50% control level, which the market can easily handle in a day or two. He’s handled all of his past Tesla share sales fairly easily, and he tends to do these at market tops when demand for the shares is overwhelming. Longer term, the much greater demand for selling Tesla shares will come from the equity raises he will need to do to build another six Tesla factories around the world. That could be anywhere from $400 billion to $800 billion, so that will be the much larger cash call, but those are years off at best.

Q: With so many big techs breaking down, how should we play the (ROM) (ProShares Ultra Technology ETF)?

A: From the long side is how you play it. But you really need these capitulation days, especially if you’re involved in 2X ETFs. There is a spectacular play setting up for the (ROM) because it’ll go from $24 (or whatever the final bottom is) to $100 in the next upcycle, so that is a great leverage play that you really want to get involved in.

Q: If I don’t have time to babysit my portfolio, am I better in LEAPS or physical stocks?

A: Well the LEAPS I’m putting out now have a 2 years 4 months expiration date, so you can literally just buy them and forget about them. On the other hand, if we don’t get an economic recovery in 2 years and 4 months, you’re better off buying stocks outright on 2:1 margin. You make less profit, but if we don’t get a recovery for 3, 4, 5 years, then you have no expiration problem with stocks, as opposed to with LEAPS. Now, there are ways to trade around your LEAPS, like financing the long and by shorting puts and getting in for zero, but that requires smaller positions because you have to maintain the margin for the short put side. So, if you want to play it safe, buy the stocks. You can even handle a lost decade with stocks, especially if their dividend pays. With LEAPS, you need a fairly immediate economic recovery, which we should get, especially if the Fed lowers interest rates next year, which it should.

Q: What is your view on the US dollar (UUP)?

A: The dollar seems close to peaking right around here. It will peak on the last day that the Fed raises interest rates, which could be on December 14th. In fact, they may not even wait until then. Depending on the inflation rate, they could only do a quarter or a half-point rate rise in December, thus giving the market their signal that way. Or not do it at all, and the sudden selloff that we had in the dollar, and the stabilization of bonds we had last week is telling you that’s on the table as a possibility. So, we saw really important moves for long-term trend considerations in the markets since last week.

Q: Time for Palantir (PLTR)?

A: No, because the CEO doesn’t give a damn about his stock, and the stock reacts accordingly. I gave up on Palantir for that reason.

Q: How do you see the Ukraine/Russia situation developing?

A: It drags on for another year, Russia keeps losing and throwing men into the meat grinder until Putin gets removed, which should happen next year at which point oil prices collapse. That may be why he blew up the Nordstream One pipeline, to tie the hands of a future Russian government.

Q: Is it safe to buy 30-day Treasury bills in November going into the next F1C meeting?

A: Yes, because they essentially have no risk—that’s basically a cash type investment. And if your broker goes bust you can just force them to hand over your Treasury bonds and not get tied up in any three-year bankruptcy proceeding. It’s an asset, not cash.

Q: Will it be time to buy LEAPS on the next market selloff?

A: Absolutely, yes.

Q: Do you believe Putin would use nukes?

A: No I don’t, because the radioactive cloud would fall back on him immediately. There are very few people who are both stock market experts and nuclear weapons experts; I happen to be one of those—probably the only one in the world in fact—because of my time spent with the atomic energy commission at the Nuclear Test Site in Nevada. The problem with bombing your next-door neighbor with nukes is that the nuclear fallout comes right back on you the next day. Most of Russia’s nukes don’t even work, they only have a handful that actually does, and if he does use one, I bet it would be a tiny one just to demonstrate that he has a working nuke—like just a one-megaton one as opposed to Hiroshima which was 20 kilotons. Or he could drop it in the Black Sea or do an above-ground test at their old nuclear test site that wouldn’t kill anyone, just to show that he has working nukes. I don’t think he will, because we would react in kind in twice the size.

Q: Time to buy ARK Innovation ETF (ARKK)?

A: You might start with a small starter position, just to get it into your portfolio so you remember to buy it on the next dip. Cathy Woods’s leverage in this fund is tremendous. You really want to own it at a market bottom, but picking the actual bottom is going to be tough. One way to achieve this is to just go out and buy Tesla—that way you don’t have to pay the management fee—or buy the top 5 holdings in ARK directly, which includes Roku (ROKU) among others. So yes, I’m watching it; I prefer buying things on the way up and missing the first 10% than to catch a falling knife, and boy has this thing been a falling knife this year.

Q: Do you like biotech here?

A: Absolutely; please subscribe to the Mad Hedge Biotech Letter for biotech recommendations plus LEAPS on biotech plays by clicking here.

Q: Energy is still the best sector now?

A: Yes, but for how long? You don’t want to be left standing when the music stops playing, and that is imminent in the oil industry. It will be illegal to sell gasoline cars in California after 2035, and gas makes up half the oil use in the US.

Q: Did you know that oil reserves (USO) are the lowest since 1984?

A: Yes, I think you may have read that in my newsletter, and that’s because of Biden’s efforts to reduce US gasoline prices through a million barrel per day release from the strategic petroleum reserves in Texas and Louisiana. If we are a net energy producer, why do we even have reserves? It’s an out-of-date holdover from the Cold War.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Tokyo 1975

Mad Hedge Technology Letter

May 11, 2022

Fiat Lux

Featured Trade:

TECH DESERVES WHAT IT DESERVES)

(RBLX), (ARKK), (ROKU), (TDOC), (ZM), (TSLA), (GM)

A bear market rally in tech would be an overwhelmingly healthy signal that the financial system is working in an orderly fashion.

Yet, as I say that, a looming recession inches closer.

How do I know that?

That was my first reaction when my eyes were stung by the headline of 8.3% inflation.

Sure, not a 10, but it is emblematic of the ongoing inflation concerns with items such as airplane tickets up 18% year over year in price.

Remember the consensus was that inflation pressures are trending towards peaking, potentially setting up for a nice bear market rally.

That narrative hit another catch-22, not as bad as it could have been, but clearly not great and prices biting at the backs of consumers.

The hope that inflation will be crammed back into the genie bottle is not going to happen until later this year and not for the right reasons.

Simply because comparables become easier to beat year over year.

Like I have mentioned in past tech letters, high-growth tech stocks are most sensitive to the fluctuation in rates and investors should be nowhere near growth funds like Cathy Wood’s ARK Innovation ETF (ARKK).

Another head-scratching move was ARK’s Cathy Wood selling Tesla (TSLA) shares and rolling them into GM (GM).

This is for the lady who likes to tell us that we aren’t “doing the research.”

Betting against Elon Musk is a fool’s game.

When it comes to EVs, I would put money on Musk to defy any odds.

Tesla will outperform GM, especially amid a backdrop of lithium prices spiking and supply chain issues going haywire.

Musk is simply the anointed guy that knows how to work miracles.

He only developed the EV industry as he saw fit, invented reusable space rockets, cut the price of space exploration by 10, and reimagined tunneling construction technology.

And by the way, his Neuralink brain interface company is working on implanting chips in human brains so we don’t need to use our fingers on keyboard anymore.

I wouldn’t want to compete with this man and to believe that GM will be able to nimbly outmaneuver Musk who has the audacity to aggressively solve anything no matter how many people he pisses off is not an incremental bet on “innovation” that Wood likes to tout she is participating in.

Neither is the purchase of Roku (ROKU), Zoom (ZM), or Roblox (RBLX) which have all tanked since she put new money to work in them in late April.

Inflation at 8.3% means that the real rate of inflation is still -7.55% and until that’s addressed, any bear market rally will be viciously sold breaching further levels down below.

The carnage in the tech world is indicative at the dregs of the barrel.

Tech IPOs are toxic.

Market for new issues has been bereft throughout the first four-plus months of this year, and nothing that would move the needle is on the tech IPO radar for the duration of the second quarter.

Companies that were aiming to go out in the first half of 2022 have no appetite to continue down that path because there simply won’t be a bid.

Going public today would require a complete revaluation of their business and leave many late-stage investors and employees with out-of-money stock.

Grocery deliverer Instacart is the only company in that class that’s been forthright with its slowing valuation. In March, the company said it cut its valuation by about 40% to $24 billion.

That’s how bad it is out there at the bush league end of the tech sector and many of these stocks that are public such as Teladoc are down 80%.

I do believe that many of these loss-making growth techs are rightfully down 80%.

They had time to show a profit and they failed in the allotted amount of time they were given.

Every window closes and the market moves forward with or without them.

In the near term, I am bearish on the market but I do believe we are oversold which could feed into a dead cat bounce to sell on.