Global Market Comments

November 9, 2020

Fiat Lux

FEATURED TRADE:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or THE ROARING TWENTIES HAVE JUST BEGUN),

(SPY), (TLT), (TSLA), (CAT), (JPM), (GOLD), (UNP), (UPS), (AMGN)

Global Market Comments

November 9, 2020

Fiat Lux

FEATURED TRADE:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or THE ROARING TWENTIES HAVE JUST BEGUN),

(SPY), (TLT), (TSLA), (CAT), (JPM), (GOLD), (UNP), (UPS), (AMGN)

I have a prediction to make.

If you are unhappy about the election result, the world will still turn, the sun will rise in the east and set in the west, and the moon will continue to wax and wane every month.

There, I promise I won’t talk about politics for another four years unless it’s for the Official Incline Village, Nevada Bear Wrangler.

The plywood has started coming down from storefronts in San Francisco, no doubt stored away for another day. Mass celebrations have broken out everywhere.

It is now back to the serious business of making money.

That is easy for me to do because I have just enjoyed the most profitable week in the 13-year history of the Mad Hedge Fund Trader. From the Thursday low last week, our 2020 year-to-date performance has rocketed by an eye-popping 11.46%. This was a once-in-a-decade setup and I struck while the iron was hot.

For only the third time this year, I went 100% fully invested right before the election, and every position dutifully made money across all asset classes. Stocks (SPY) and gold (GLD) soared, while the US Treasury bond market (TLT) and the US dollar (UUP) crashed. On the stock side, everything went up like the true quantitative easing, liquidity-driven market that it is.

My fundamental call on the market came true. It made no difference who won the election, the mere fact that it is over is a major positive for stocks.

With such a historic move last week, the major indexes have pulled forward performance from the rest of 2020 and possibly a piece of 2021 as well. So, I expect to see sideways chop for the next seven weeks with a slight upward bias.

I don’t need to remind the veterans out there that this is the perfect environment for vertical bull call spreads. We may stay fully invested for a while and shoot for a record performance for 2020.

The chance of a market crash now is effectively zero. If for some reason we do get a 5% pullback, for Heaven’s sake please dive in with both hands. The Roaring Twenties and the next American Golden Age have only just begun. Globalization resumes its inevitable course.

The only thing that would trigger a selloff is an exponential growth of the pandemic, which with 122,000 cases and 1,200 deaths yesterday has already started. I have believed all along that the third peak in cases will be the final hyperbolic one, with deaths eventually topping the 1919 Spanish Flu peak of 650,000.

So far, the stock market has chosen to ignore these grim numbers, preferring instead to focus on vaccine hopes. There is effectively no government in Washington until January 21, 2021 so there is no one to step in and stop it. When the market does notice, the next buying opportunity of the decade may be at hand.

Stocks started expecting a Biden Win on Monday when they exploded right out of the gate. The Volatility Index (VIX) will plunge from $40 to $24 in a heartbeat. This was the biggest post-election rally in 100 years, with a 65% voter turnout not seen since women first got to vote in 1918. Buy dips in the (SPY).

The flip side is that massive spending will create monster deficits. Abuse from Trump has prompted the world’s largest buyer of US Treasury Bonds (TLT), China, to cut back their holdings from $1.24 trillion to $1 trillion. If China won’t buy our debt, who will? Sell short the (TLT) on rallies.

The Senate is another story. If the Republicans win, it will block most Biden programs and gridlock government for two years. Gridlocked government is normally good for stocks, except when you have a global pandemic and a Great Depression. No bold action is possible.

Expect slower economic growth as a result, fewer trading opportunities, and less asset appreciation. The Senate’s main job now is to make sure Biden fails. However, if Biden takes Georgia, we won’t know for sure until two Senate runoff elections take place there in January.

Jay Powell isn’t going anywhere, so interest rates are staying at near zero for three more years, according to yesterday’s press conference. Quantitative easing is still the name of the game.

Gold has turned, with the standard 100-day correction over. New highs beckon. The drivers are US interest rates remaining near zero for years, stockpiling by foreign central banks, and a recovering US economy. Notice also that the correlation between US stocks and gold this year has been 1:11. Gold is just another quantitative easing asset class these days. I’m starting to look at silver too, which usually has much more upside volatility.

China’s PMI is up for eight months, to 51.6%, better than expected. The world’s first post-pandemic economic keeps powering on. Anything over 50 is showing expansion.

The US ISM Nonmanufacturing Index hit a two-year high in October, down from 57.5 estimated to 57.5. That’s a two-year high.

The Nonfarm Payroll Report surprises at 638,000 for October, taking the headline Unemployment Rate down to a still recessionary 6.9%. Some 268,000 government jobs were lost, including 147,000 census workers. The rest came from teachers laid off by cash-starved local governments. Leisure & Hospitality jumped by 271,000. There are still 10 million fewer employed than when the pandemic started. The news crushed the bond market, where I’m short. Keep selling rallies in the (TLT).

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Global Trading Dispatch exploded to another new all-time high last week.

The Friday prior to election week, I picked up new longs in the (SPY), (TSLA), and (CAT). Then on Monday, I bet the ranch, going 100% “RISK ON,” throwing the dice on a post-election melt-up and adding the (TLT), (JPM), (GOLD), (UNP), (UPS), and (AMGN).

It worked in spades.

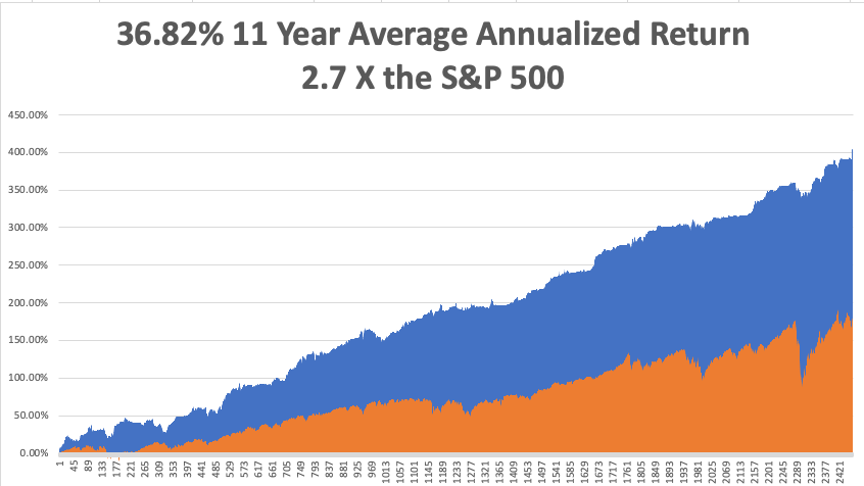

That keeps our 2020 year-to-date performance at a blistering +44.16%, versus a LOSS of -.06% for the Dow Average. That takes my 11-year average annualized performance back to +36.82%. My 11-year total return stood at new all-time high at +401.96%. My trailing one-year return appreciated to +52.23%.

The coming week will be a sleeper compared to the previous one. We also need to keep an eye on the number of US Coronavirus cases and deaths, now over 10 million and approaching 240,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, November 9 at 12:00 PM EST, US Consumer Inflation Expectations for October are out.

On Tuesday, November 10 at 7:00 AM EST, we get the NFIB Business Optimism Index for October.

Wednesday, November 11 is Veterans Day and I’ll be leading the local parade. The stock market is still open.

On Thursday, November 12 at 8:30 AM EST, the Weekly Jobless Claims are announced. At 9:30 AM EST, the US Inflation Rate for October is released.

On Friday, November 13, at 9:30 AM EST, the US PPI for October is printed. At 2:00 PM we learn the Baker-Hughes Rig Count.

As for me, driving back from Lake Tahoe, I couldn’t help but sadly notice what a terrible wreck the country is in.

Stores everywhere are shuttered and schools are closed down. Many of my favorite businesses and restaurants are gone for good. Parts are unobtainable because someone in the supply chain either went out of business or died. You can’t go anywhere without being swathed in masks and hand sanitizer.

The new president has a big job ahead of him.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 5, 2020

Fiat Lux

FEATURED TRADE:

(A NOTE ON OPTIONS CALLED AWAY),

(SPY), (UNP), (TSLA), (CAT), (JPM), (GOLD), (UPS), (AMGN), (TLT)

Global Market Comments

November 2, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE ELECTION IS HERE!)

(INDU), (SPY), (TLT), (CAT), (TSLA), (GOLD), (JPM), (VIX), (VXX)

That was a great lead into Halloween last week, where frightening share price movements scared the living daylights out of all of us. The Dow Average dove by 7.0% last week and is down 8.9% from the September 1 peak. It was the worst performance in seven months.

Of course, I saw it all coming a mile off, predicting a selloff going into the November 3 presidential election and a rally once the great uncertainty is removed. That’s why I have run several short positions over the past month, all of which proved successful, and am long flipping to the long side.

The next generational peak at 120,000 is now only 93,499 points away. Time to get moving.

Of course, technical analysts who were eternally bullish at the market top are now wringing their hands over the double top on the charts that even a two-year-old can spot. It’s only giving us a better entry point for longs that will carry us through to yearend.

The stock market has priced in a contested election. If that doesn’t happen, and the winning candidate takes the White House by a landslide, markets will have to immediately back out that dire scenario. Stocks could soar by 1,000 points immediately on the first whiff of a challenge0-proof victory margin.

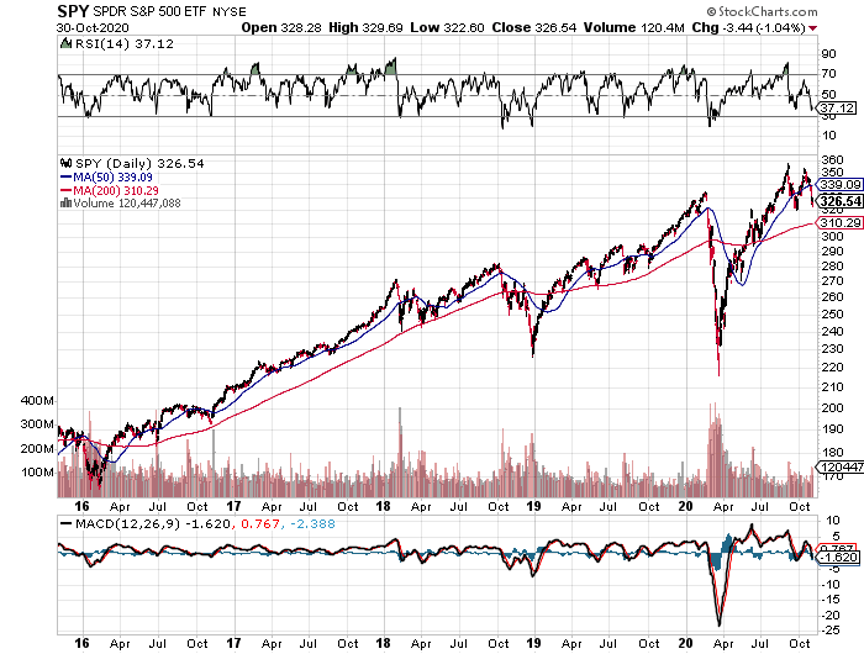

This time, we have the luxury of trading against a line in the sand at a (SPY) of $310, the 200-day moving average. Look at the chart below and you’ll see that this was not only close to the highs in 2018 and 2019 and a recent bottom in 2020. As if driven by the force of gravity, the market seems strangely driven to the $310 level.

It’s almost impossible to lose money on call spreads bought at market bottoms when the Volatility Index (VIX) is over 40%, as it was on Thursday and Friday. It’s time to strike while the iron is hot, and other investors are jumping off of bridges.

I’ll be piling into domestic recovery stocks like banks, construction, couriers, railroads, and gold and selling short bonds and the US dollar.

The election has already taken place, as 85 million votes have been cast in early voting. Many states have already seen double their 2016 turnouts. We just don’t know the outcome yet. It’s likely that new Covid-19 infections could top 100,000 on election day.

I’ll be up all night on Tuesday watching the results come in and keeping a hawk-eye on the overnight futures trading in Asia, the only open markets. Watch for Florida and North Carolina to report first.

One of the great ironies of trading last week was that after delivering the best earnings performance in stock market history, we saw one of the worst share price performances.

That’s because all of the great stimulants for the economy in recent months, the prospect of a massive stimulus package, declining Covid-19 cases, and plunging interest rates, will take a three-month vacation while the United States changes governments.

We really do work in a “what have you done for me lately” industry.

It was all about tech earnings last week, with Amazon (AMZN), Alphabet (GOOGL), and Microsoft all reporting. We have to wait until next week for Apple (AAPL). They all knocked the cover off the ball. Only Apple (AAPL) disappointed on a 20% YOY sales drop.

It seems everyone was waiting for the iPhone 12. Stock was off $10. Sales in China also took a big hit. Expect a massive resurgence in Q4. iPhones are selling faster than Apple can make them. Buy (AAPL) on dips. The stock jumps 8%. Forget about the DOJ antitrust suit. Buy (GOOGL) on dips.

Crashing bond prices show that a recovery is imminent, with ten-year US Treasury yields ($TNX) jumping 20 basis points in a month to a four-month high. Buy (SPY) on dips and sell short (TLT) on rallies.

Existing Home Sales soared by 9.4% in September, up a staggering 20% YOY. Inventories fell to a record low 2.7 months. Median prices are up an astounding 14.8% YOY to $311,800. Zillow believes this madness will continue for at least another year. Sales were strongest in the Northeast, with most of the action in single-family homes. Homes over $1 million have doubled, and vacation homes are up 35%.

Q3 GDP exploded with a 33.1% rate, double the highest on record and in line with expectations. All cylinders are firing, except for the 20% of the economy that went bankrupt during the pandemic. The stock market fully discounted this on September 1 when stocks peaked. The US won’t recover its 2019 GDP until 2023. With Corona cases now soaring, are we about to go back into the penalty box?

Weekly Jobless Claims posted at 751,000, an improvement, but still near a record high. It’s the lowest report since pre-pandemic March 14. I think a lot of these losses are structural….and permanent.

The World’s Biggest ETF is bleeding funds, with the (SPY) losing $33 billion this year. Massive selling at market tops has been a major factor. Most of the selling was in February and March when the pandemic started, and the money never came back. It also belies the widespread shift into tech stocks this year. Out with the boring, in with the exciting. Dry powder for the coming Roaring Twenties?

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Global Trading Dispatch hit another new all-time high last week. October closed out at a moderate 1.51% profit.

I took a big hit on a long in Visa (V), thanks to a surprise prosecution from the Department of Justice over their Plaid merger. I more than offset that with short positions in the (SPY) and (JPM). Then on Friday, I leaned into the close, picking up new longs in the (SPY), (TSLA), and (CAT) betting on a post-election rally.

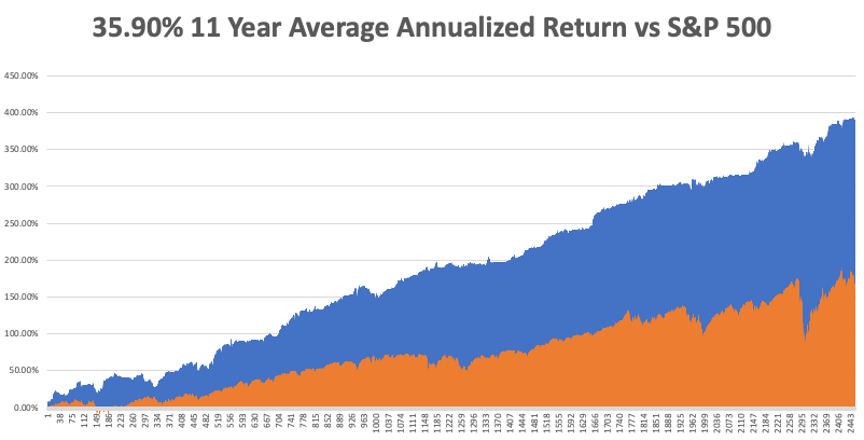

That keeps our 2020 year-to-date performance at a blistering +36.03%, versus a LOSS of -7.5% for the Dow Average. That takes my 11-year average annualized performance back to +35.90%. My 11-year total return stood at a new all-time high at +391.94%. My trailing one-year return appreciated to +42.48%.

The coming week will be one of the most exciting in history as election results trickly out Tuesday night. As if we didn’t have enough to worry about, it is also jobs week. We also need to keep an eye on the number of US Coronavirus cases and deaths, now over 9 million and 232,000, which you can find here.

On Monday, November 2 at 8:00 PM EST, US Vehicle Sales for October are released. Alibaba (BABA) and Sanofi (SNY) report earnings.

On Tuesday, November 3, we get the US Presidential Election. Early results in Florida will start coming out at 7:30 PM EST. TV networks, makers of campaign tchotchke and bumper stickers, and talking heads will go into mourning. Coca-Cola (K) reports earnings.

On Wednesday, November 4 at 9:15 AM EST, the ADP Private Employment Report is out. QUALCOMM (QCOM) and Wynn Resorts (WYNN) report earnings.

On Thursday, November 5 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, November 6 at 8:30 AM EST, the October Nonfarm Payroll Report is announced. Barrick Gold (GOLD) reports earnings. At 2:00 PM we learn the Baker-Hughes Rig Count.

As for me, I went to San Francisco for dinner with an old friend last night and I couldn’t believe what I saw. Storefronts were boarded up, the streets vacant, with only the homeless ever present. The cable cars have quit running.

We ate outside at my favorite Italian restaurant Perbacco on Market Street where the heat lamp blasted away. The restaurant is owned by my transplanted Venetian friend Umberto Gibin. He was running it at 50% capacity with 25% of the staff just to break even.

I hope he makes it.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 26, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MIXED MESSAGES)

(SPY), (TLT), (UUP), (FCX)

It was definitely a week of mixed messages in the stock market.

Is Covid-19 going to disappear by itself shortly, or is it the worst thing since the black plague?

Are we going to get a $2 trillion stimulus package out of Washington, or not?

Are stocks too expensive, or still cheap?

We are being told the answers to these questions loud and clear, we just can’t hear them.

For this election looks to set all records on turnout. Every city in the country is seeing lines of voters snaking around the block waiting 2-8 hours. But which way are they voting? Are there hoards of hidden Biden voters coming out of the woodwork, or Trump ones? We won’t know the result for eight more days.

In the meantime, the markets bide their time.

Which raises one last question: how low can stocks fall over the next seven trading days?

In the meantime, some asset classes aren’t willing to sit on their hands any longer. Interest rates have started to rise, hitting a four-month high. This has knocked 15 points off of bond (TLT) prices. Yet, contrary to expectations, the US dollar is hugging a multiyear low (UUP), while commodity prices (FCX) soar.

All of this spell a record economic recovery in 2021. All that remains is for stock prices to play catch-up.

The word is that there is over $1 trillion sitting on the stock market ready to dive in the day after the election, possibly tacking on at least 10% to the major indexes by yearend. There could be one hell of a post-election celebration, no matter who wins.

Baby Boomers are unloading stocks to Gen Xers mostly, but Millennials as well. Of course, they have all the money, with a 53% ownership of all stocks, compared to 27% for Gen Xer’s and a mere 3% for Millennials. The Greatest Generation, born before 1946, have been shrinking their share ownership since 1990 and own only 17% of the total now. A coming jump in capital gains taxes will accelerate the process.

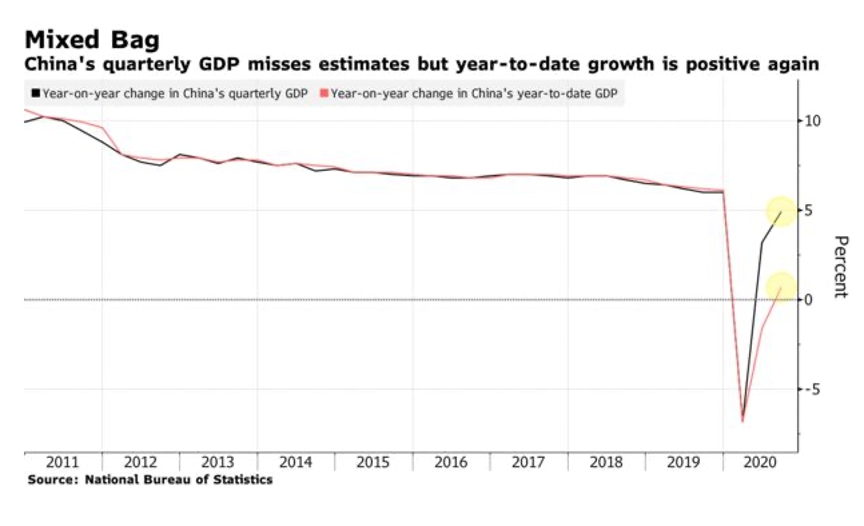

China’s Economy soared by 4.9%, in Q3 YOY with the pandemic in the rear-view mirror. First into the Coronavirus brings first out. Retail sales are through the roof and industrial production and business investment is accelerating.

Goldman Sachs says a Blue Wave will increase spending and boost the stock market. Total one-party control of the government eliminates the haggling that we are currently seeing in Washington and will deliver more Covid-19 aid faster. It should more than offset the ill effects of tax increases.

Beware of the coming Tax Loss Selling. A Biden win could unleash a torrent of selling as investors rush to beat an increase in the capital gains tax. That’s when you buy.

US Housing Permits blow the roof off at 1.553 million, up a staggering 22% YOY and a 13-year high. I wondered why I was suddenly getting a lot of flat tires on the freeway. They’re caused by nails and screws falling off the back up pickup trucks on the way to jobs. The long-term structural housing shortage continues. 30-year money at 2.75% makes a big difference.

Tesla generates a record profit for the fifth consecutive quarter in a row. The company is relying on its China factory to hit its 2020 target of 500,000 million units. Again, $397 million in regulatory credits drive earnings, payments from other carmakers who are lagging on electric car production. Gross margins rose 250 basis points to 23.5%. S&P 500 listing here we come! Next target $2,500!

Weekly Jobless Claims dropped to 787,000, better, but still horrible. California is finally reporting again.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Global Trading Dispatch hit a new all-time high last week by staying 100% in cash. I was just as grateful for having no positions on the up 600-point days as I was on the down 600-point days. Safe to say that I will be an increasingly more aggressive buyer on ever smaller dips and a seller on bigger rallies. October has now reached to a welcome 1.89% profit.

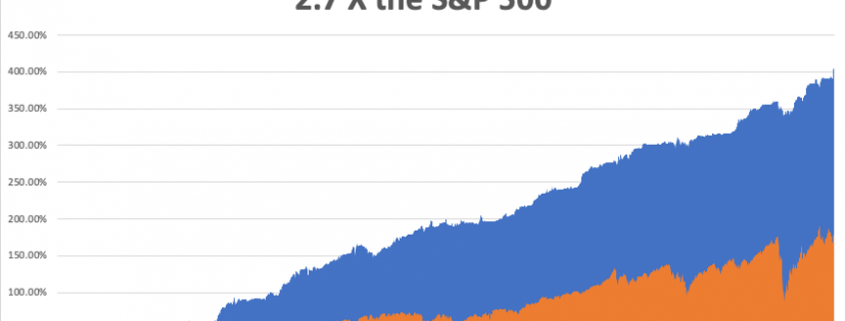

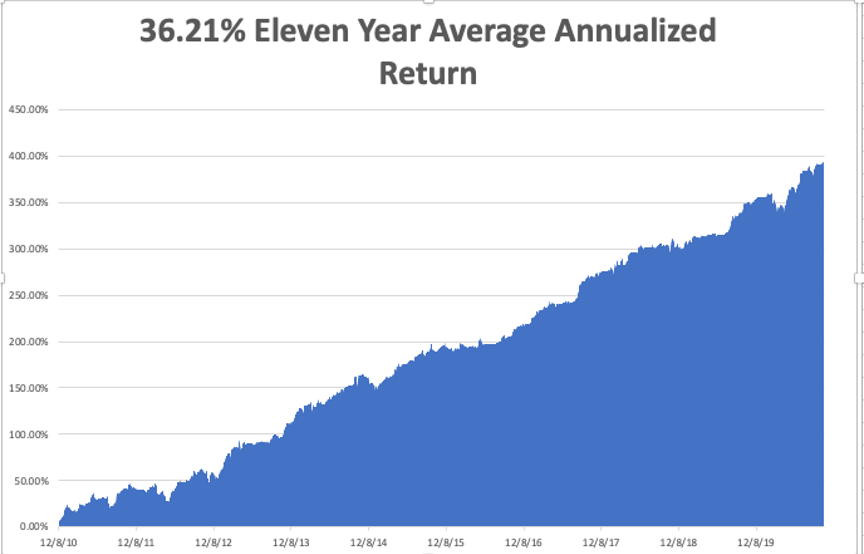

That keeps our 2020 year-to-date performance at a blistering +36.29%, versus a LOSS of -0.57% for the Dow Average. That takes my eleven year average annualized performance back to +36.21%. My 11 year total return stood at new all-time high at +392.30%. My trailing one year return appreciated to +42.86%.

The coming week will be a dull one on the data front. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, now at 225,239, which you can find here.

On Monday, October 26 at 10:00 AM EST, New Home Sales are published. Ely Lilly (LLY) and Merck (MRK) report earnings.

On Tuesday, October 27 at 9:00 AM EST, the S&P Case Shiller Home Price Index for August is released. Microsoft (MSFT) and Pfizer (PFE) report earnings.

On Wednesday, October 28, at 2:00 PM EST, the EIA Cushing Crude Oil Stocks are out. Boeing (BA) and Visa (V) report earnings.

On Thursday, October 29 at 8:30 AM EST, the Weekly Jobless Claims are announced. At the same time, we get the first read on Q3 GDP. Alphabet (GOOGL) and Amazon (AMZN) report earnings.

On Friday, October 30, at 8:30 AM, Personal Income for September is printed. Exxon (XOM) reports earnings. At 2:00 PM we learn the Baker-Hughes Rig Count.

As for me, I’ll be charging up every electronic device I have as the San Francisco Bay Area is expected to suffer a complete power blackout for the next three days. PG&E is shutting off the juice because winds are expected to reach 70 miles per hour and it hasn’t raised in six months.

I won’t be affected because I am totally off the grid with my own solar and battery network. You can easily find me because mine will be the only house in the mountains with the lights on.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 23, 2020

Fiat Lux

Featured Trade:

(11 SURPRISES THAT WOULD DESTROY THIS MARKET),

(SPY), (USO), (AMZN), (MCD), (WMT), (TGT)

Global Market Comments

October 19, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

OR WHY THE NEXT TWO WEEKS ARE A WRITE-OFF)

(V), (SPY)

You can pretty much write off trading for the next two weeks.

The election has been decided. It’s going to be a scandal a day in the media, but everyone has already made up their minds. All attention will be devoted to politics at the expense of trading, investment, and research. In the end, the president will lose by more than 15 million votes. All that is left but the imprimatur of the Electoral College.

Yet the Democrats are not declaring victory, with the memory of the 2016 debacle too fresh, when overconfidence and complacency ruled.

The few who are trading are jockeying around to position for the 2021 market. That means keeping big tech and adding to positions in domestic recovery and industrial stocks, like banks, couriers, railroads, and drug companies.

Tech will keep rising because of the catapult into the future provided by the pandemic yet to be reflected by share prices. Domestic industrials will see a recovery that is normal when coming out of a tradition recession, or Great Depression.

But they are doing so hesitantly, with little conviction.

After all, there are national elections in two weeks.

As for me, I have limited myself to the cautious two positions, one long in Visa (V) and one short in the S&P 500 (SPY), both of which are making money.

So, it is a good time to do your research, build your short lists of stocks to buy, and gird your loins. The main event begins after November 3.

Markets jumped on stimulus hopes. Investors don’t really care if stimulus happens before or after a Biden win. They’re buying now. And Biden will almost certainly double up spending later in the year. No dips for latecomers. The post-election market melt-up has begun and new highs beckon. Fears of election disruption have vaporized.

Markets just entered the strongest six months of the year. It’s the inverse of sell in May and go away. October to May portfolios have yielded 64% annually for the past 20 years, while May to October investments yield exactly 4%. It traces back to America’s agricultural cycle of a century ago. Take every tailwind you can find.

The IMF predicted negative 4.4% growth for 2020, the worst since the Great Depression. Believe it or not, this is an upgrade from more dismal numbers. By comparison, the 2008-09 Great Recession brought only a 0.1% drawdown. If the US passes another stimulus package, it will recover its 2019 GDP in 2021 instead of 2022.

The new 5G iPhone is out! After a year of speculation, we get a better screen, improved camera, and magnetic charging for $999. The stock dumped on a classic “buy the rumor, sell the news.” Also out is a new mini iPhone for $699. Your neighborhood won’t have 5G for a year. Buy Apple (AAPL) on dips.

The US PC market saw best quarter in a decade, with millions of new home offices joining the fray. Some 71.4 million computers were shipped in Q3, up 3.6% YOY. Think enormous demand for new chips. Buy (AMD), (MU), and (NVDA) on dips.

Used car prices are soaring, jumping the most since 1969, and lifted the Consumer Price Index by 0.2% in September. It’s the fourth straight month of increasing inflation.

Ships are backed up in Los Angeles waiting to unload. America’s import boom and soaring trade deficit with China leaves no available dock space on the west coast. It’s another sign of a recovering economy.

US Producer Prices pop in September bringing the first YOY gain since March. They were up 0.4% following a 0.3% gain in August. Another sign of a recovering economy.

Weekly Jobless Claims ballooned to 898,000, now that California is reporting again. Not what you want to see going into an election. A slowing economy and spreading virus don’t help either. Some 25.5 million Americans are out of work.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Global Trading Dispatch hit a new all-time high last week by staying 100% in cash. I was just as grateful for having no positions on the up 600-point days as I was on the down 600-point days. Safe to say that I will be an increasingly more aggressive buyer on ever smaller dips and a seller on bigger rallies. October has now reached to a welcome 1.61% profit.

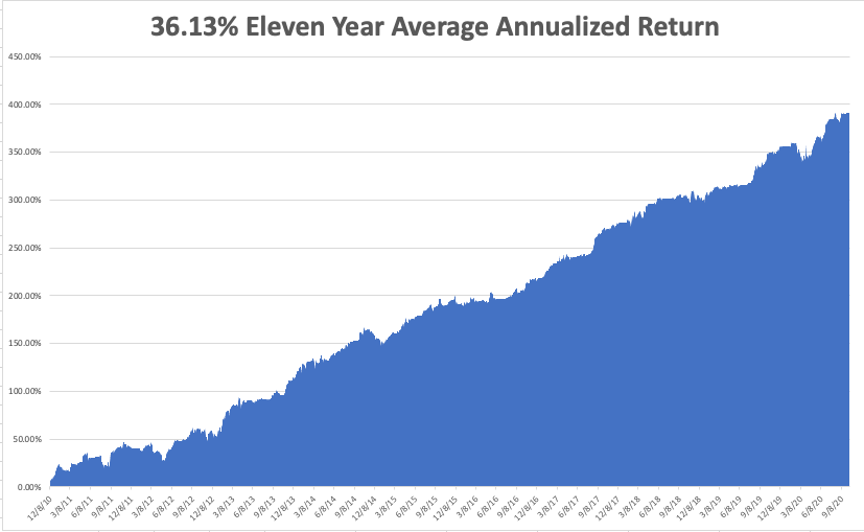

That keeps our 2020 year-to-date performance at a blistering +36.11%, versus a gain of 0.3% for the Dow Average. That takes my eleven-year average annualized performance back to +36.13%. My 11-year total return stood at a new all-time high at +392.02%. My trailing one-year return appreciated to +42.67%.

The coming week will be a dull one on the data front. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, now at 219,679, which you can find here.

On Monday, October 19 at 8:30 AM EST, the IMF/World Bank virtual annual meeting starts, so we can expect Fed speakers every day. (IBM) reports earnings.

On Tuesday, October 20 at 8:30 AM EST, Housing Starts for September are announced. Netflix (NFLX) reports earnings.

On Wednesday, October 21 at 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out. At 2:00 PM EST, the Fed Beige Book is published, a transcript of the Federal Open Market Committee meeting from six weeks ago. Tesla (TSLA) reports earnings.

change.

On Thursday, October 22 at 8:30 AM EST, the Weekly Jobless Claims are announced. At 10:00 AM EST Existing Home Sales for September are out. AT&T (T) reports.

On Friday, October 23, at 2:00 PM, we learn the Baker-Hughes Rig Count. American Express (AXP) reports earnings.

As for me, I saw a curious thing driving back from Lake Tahoe this weekend. Usually, I see a never-ending parade of out of state license plates moving to the Golden State.

This time, I saw telephone poles coming in by the truckloads, hundreds of them. These are to replace the many burned down in the horrific wildfires that incinerated an area the size of Connecticut. Apparently, California has run out of telephone poles.

Is there a public stock for a company that sells telephone poles?

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader