For the last couple of nights, I have left my iPhone logged into the Argentina peso market, one of several troubled currencies igniting the emerging market contagion. Whenever the peso losses another handle to the US dollar, an alarm goes off. That gives me a head start on how American markets will behave the next day.

I have not been getting a lot of sleep lately. My poor phone has recently been sounding off like a winning slot machine at a Las Vegas casino.

Take a look at the long-term chart for the peso, and it?s clear that some traders have not gotten any sleep for five years, when the peso cratered 50% against the greenback. An imploding currency, soaring national debt, and sliding economy promise to send it lower.

Incompetent leadership doesn?t help either. You know that things are bad when your ships get seized by creditors when they land at foreign ports.

When I wrote my all asset class forecast for 2014, there was only one thing I knew for sure: this year would be harder than last. That has been my best prediction for 2014 so far.

The guaranteed shorts, those for the Japanese yen (FXY) and the Treasury bond market (TLT), have been rocketing to the upside since the opening bell rang on January 2. The no brainer longs, like financials (XLF) and consumer discretionaries (XLY), have been plummeting.

The heart wrenching 4.3% correction we saw for the S&P 500 (SPY), and the 5% hit for the Dow average this month, the worst weekly draw down in two years, has predictably brought the Armageddon crowd out of the closet once again. All of a sudden, a 10% correction best case, and Dow 3,000 worst case, are on the table once again. Do they have a leg to stand on?

Not really.

To achieve these big numbers on the downside, your really need a global systemic financial crisis. There isn?t one remotely on the horizon. Yes, there are difficulties in Argentina, the Ukraine, and Turkey. But they are locally confined.

Together, these countries account for less than 1% of global GDP. If they disappeared completely, they would barely make a blip in world GDP. They certainly are not important enough to panic you into emptying your ATM at the local mall on your next lunch break.

You also need excessive leverage. But that has been banned by prime brokers since the 2008 crash. An aggressive long today is 20% net long, not 200% as in the bad old days of yore. Nothing systemic there.

Sure, we aren?t getting the juice that we used to from the Federal Reserve. It is likely that they will further reduce the taper from $75 billion to $65 billion of bond buying per month at their 1:00 PM Wednesday press release.

If there were a one in a million chance that this would trigger a real market meltdown, my friend, Fed governor Janet Yellen, would run that release through the shredder as fast as you could say ?Go Bears?, sending markets flying.

Others are accusing a looming financial crisis in China as another culprit. Yes, the economic data has been soggy of late, to be sure. However, that is just the continuation of a four year old trend. You can safely forget about that one.

No country in history ever suffered a financial crisis with $4 trillion in foreign exchange reserves on hand, including over $1 trillion in US Treasury bonds close to all time highs in value. In fact many of the emerging markets said to be in trouble also boast large reserves, the product of running massive trade surpluses with a hyper consuming West for the past decade.

So if we can?t blame emerging markets or the taper for the downside, then what is causing the January swoon? You can blame it all on the hedge funds.

I have seen this time and again. Whenever too many people crowd into one end of a canoe, it rolls over. When the majority of funds have identical positions, they are guaranteed to fail. That is why we have had a looking glass market performance since the beginning of this year.

Except that this time we got a turbocharger. The peaking of concentration in the most popular trades perfectly coincided with the big New Year reallocation trade, taking prices to greater extremes. Much of the selling you are seeing down here is from latecomers who bought stock only three weeks ago and are now puking them out.

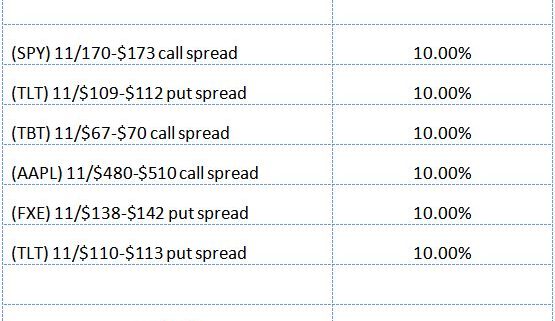

Of course, I saw all of this coming a country mile off. This is why I cut my net long from 100% 10 days ago to only 10%. It is why I am maintaining a year to date performance of +5.13%, compared to a Dow that is down -5%. It is one of my best gains relative to the index over a short period ever.

The same is true of my colleague, Mad Day Trader, Jim Parker. He is almost all in cash and is also well up on the year. He stuck his toe in the water with a small position in some calls on the (TBT) last week, but it got bit off by a shark almost immediately. So he quickly stopped out, as is his way. Of course, we have been comparing notes and sharing input throughout the selling. It appears that great minds think alike.

Jim?s proprietary in-house analysis predicts that the (SPX) will bottom out just above 1,730, the market close on the November 15 options expiration. If correct, that would give us a total start to finish correction of only 6.7%, which is in line with every other correction for the past two years. But the bottoming process could last a few weeks, and provide several more gut churning dumps. Fasten your seat belt.

When will this end? Watch for the parallel confirming cross market trends. The Treasury bond market is a big one, which appears to be peaking already, right at its 200 day moving average and the top of a six month trading range.? Announcement of the next taper could spark the selloff we need there. The Japanese yen is also important. A top here could signal a return to the carry trade and ?RISK ON?.

Since Emerging markets were the instigator of the crisis, look there as well for the first signs of a turnaround. Scrutinize the chart below, and you gain some heart.? It shows that we are a scant 70 cents from setting up a potential multiyear triple bottom at $37, and worst-case $36.

More specifically, you want to see Turkey (TUR), another instigator of this crisis, recoil from $39. Expect it to bounce hard there, as long as the world is really not ending.

Then it will be off to the races once more. I?ll be keeping my powder dry until then. Watch this space.

![USD per 1 ARS]() The Argentine Peso Against the US Dollar

The Argentine Peso Against the US Dollar