I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have a comfortable seat next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini can navigate it.

I am anything but Houdini, so I foray downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up to date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

Chicago’s Union Station

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way, like Omaha, Salt Lake City, and Reno, to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my favorite photos from the trip below, although there is only so much you can do from a moving train and an iPhone 16 Pro.

Somewhere in Iowa

The Thumbnail Portfolio

Equities – buy dips, but sell rallies too Bonds – avoid Foreign Currencies – avoid Commodities – avoid Precious Metals – avoid Energy – avoid Real Estate – avoid

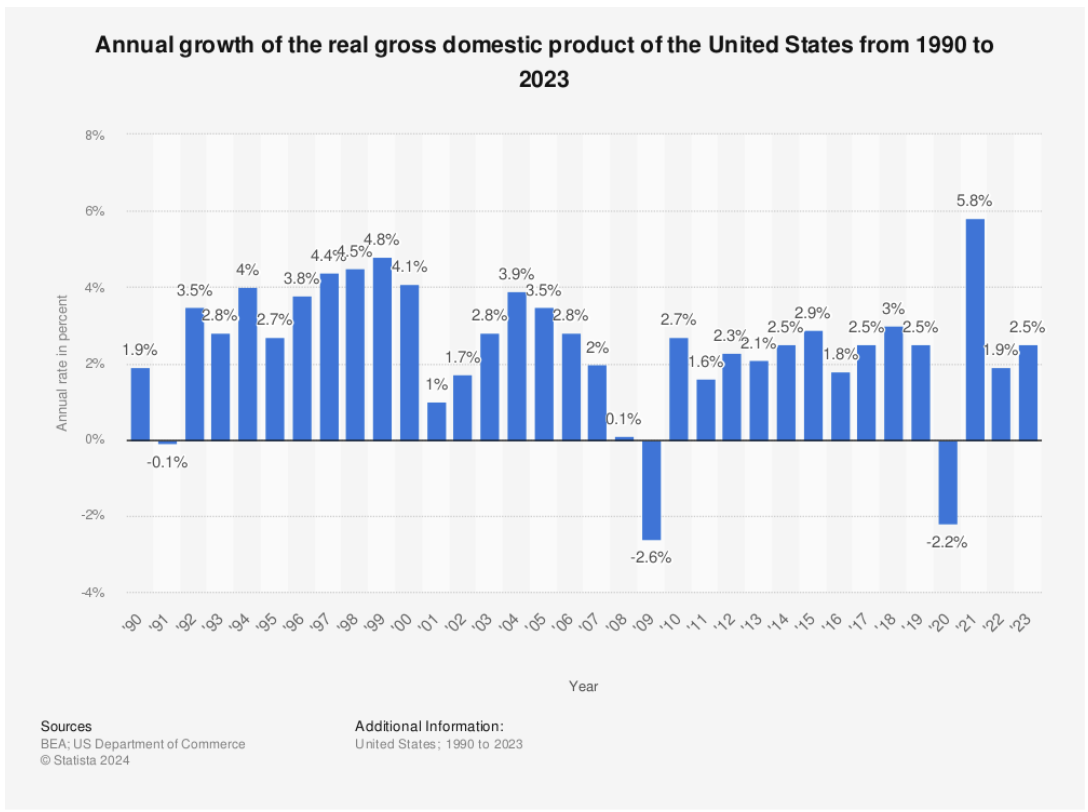

1) The Economy – Cooling

I expect a modest 2.0% real GDP growth with a 4.0% inflation rate, giving an unadjusted shrinkage of the economy of negative -2% for 2025. That is down from 0% in in 2024. This may sound discouraging, but believe me, this is the optimistic view. Some of my hedge fund buddies are expecting a zero return over the next four years.

Virtually all independent economists expect the new administration's economic policies will be a drag on both the US and global economies. Trade wars are bad for everyone. When your customers are impoverished, your own business turns south. This is a big deal, since the Magnificent Seven, which accounted for 70% of stock market gains last year, get 60% of their profits from abroad.

The ballooning National Debt is another concern. The last time Trump was in office, he added $10 trillion to the deficit through aggressive tax cuts and spending increases. If this time, he adds another $10-$15 trillion, the National Debt could reach $50 trillion by 2030.

There are two issues here. For a start, Trump will find it a lot harder and more expensive to fund a National Debt at $50 trillion than $20 trillion. Second, borrowing of this unprecedented magnitude, double US GDP, will send interest rates soaring, causing a recession.

The only question then is whether this will be a pandemic-style recession, which took stocks down 30% and recovered quickly, or a 2008 recession which demolished stocks by 52% and dragged on for years.

Hope for the best but expect the worst, unless you want to consider a future career as an Uber driver.

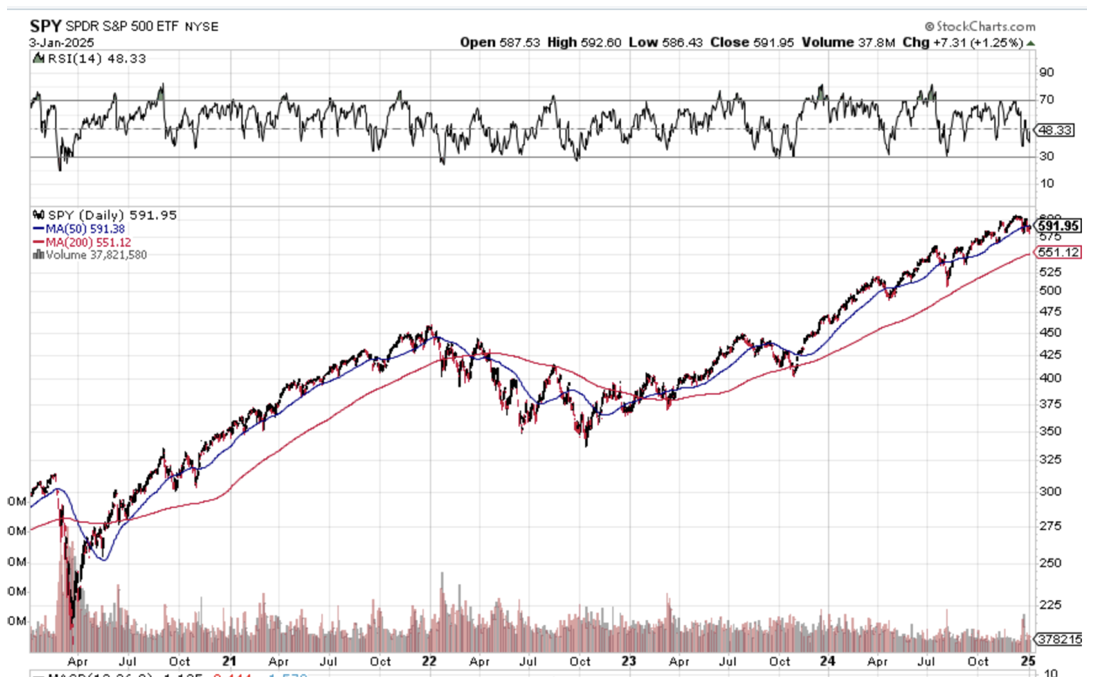

The outlook for stocks for 2025 is pretty simple. You are going to have to work twice as hard to make half the money you did last year with twice the volatility. You will not be able to be as nowhere near aggressive in 2025 as you were in 2024It’s a dream scenario for somebody like me. For you, I’m not so sure.

It’s not that US companies aren't growing gangbusters. I expect 2% GDP growth, 15% profit growth, and 12% net margin growth in 2025. But let’s face reality. Stocks are the most expensive they have been in 17 years and we know what happened after 2008. Much of the stock market gain achieved last year was through hefty multiple expansions. This is not good.

Big tech companies might be able to deliver 20% gains and are still the lead sector for the market. Normally that should deliver you a 15%, or $800 gain in the S&P 500 (SPX). We might be able to capture this in the first half of 2025.

Financials will remain the sector with the best risk/reward, and I mean the broader definition of the term, including banks, brokers, money managers, and some small-cap regional banks. The reason is very simple. Their income statements will get juiced at both ends as revenues soar and costs plunge, thanks to deregulation.

No passage of new laws is required to achieve this, just a failure to enforce existing ones. The hint for this is a new SEC chair whose primary interest is promoting the Bitcoin bubble. Buy (GS), (MS), (JPM), (BAC), (C), and (BLK).

However, this is anything but a normal year. Uncertainty is at an eight-year high, thanks to an incoming administration. If the promised policies are delivered, inflation will soar and interest rates will rise, as they already have. We could lose half or all of our stock market gains by the end of 2025.

The big “tell” for this was the awful market performance in December, down 5%. The Dow Average was down ten days in a row for the first time in 70 years. Santa Claus was unceremoniously sent packing. People Are clearly nervous. But then they should be with a bull market that is approaching a decrepit five years in age.

There is a bullish scenario out there and that has Trump doing absolutely nothing in 2025, either because he is unwilling or unable to take action. After all, if the economy isn’t actually broken, why fix it? Better yet, if you own an economy it is better not to break it in the first place.

Nothing substantial can pass Congress with a minuscule one-seat majority in the House of Representatives. There will be no new presidential action through tariffs and only a few token, highly televised deportations, not enough to affect the labor market.

Stocks will not only hold, but they may add to the 15% first-half gains for the year. I give this scenario maybe a 50% probability.

The first indication this is happening is when the presidential characterization of the economy flips in a few months from the world’s worst to the world’s best with no actual change in the numbers. Trump will take all the credit.

You heard it here first.

Frozen Headwaters of the Colorado River

3) Bonds (TLT), (TBT), (JNK), (PHB), (HYG), (MUB), (LQD) Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, or dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites returned home by train because their religion forbade travel by automobiles or airplanes.

The big question to ask here after a 100-basis point rise in bond yields in only three months is whether the (TLT) has suffered enough. The short answer is no, not quite yet, but we’re getting close. Fear of Trump policies should eventually take ten-year US Treasury bond yields to 5.00%, and then we will be ready for a pause at a nine-month bottom. After that, it depends on how history unfolds.

If Trump gets everything he wants, inflation will soar, bonds will crash, and 5.00% will be just a pit stop on the way to 6.00%, 7.00%, and who knows what? On the other hand, if Trump gets nothing he says he wants, then both bonds stocks and bonds will rise, creating a Goldilocks scenario for all balanced portfolios and investors.

That also sets up a sweet spot for entry into (TLT) call spreads close to 5.00% yields. A politician campaigning on one policy, then doing the opposite once elected? Stranger things have happened. The black swans will live.

If your basic assumption for interest rates is that they stay flat or rise, then you have to love the US dollar. Currencies are all about expected interest rate differentials and money always pours into the highest-paying ones. Tariffs will add fat to the fire because any reduction in international trade automatically reduces American trade deficits and is therefore pro-dollar.

This means that you should avoid all foreign currency plays like the plague, including the Euro (FXE), Japanese yen (FXY), British Pound (FXB), Canadian dollar (FXE), and Australian dollar (FXA).

A strong greenback comes with pluses and minuses. It makes our exports expensive and less competitive and therefore creates another drag on the economy. It demolishes traditional weak dollar plays like emerging markets and precious metals. On the other hand, it attracts substantial foreign investments into US stocks and bonds, which has been continuing for the past decade.

Above all, be happy you are paid in US dollars. My foreign clients are getting crushed in an increasingly expensive world.

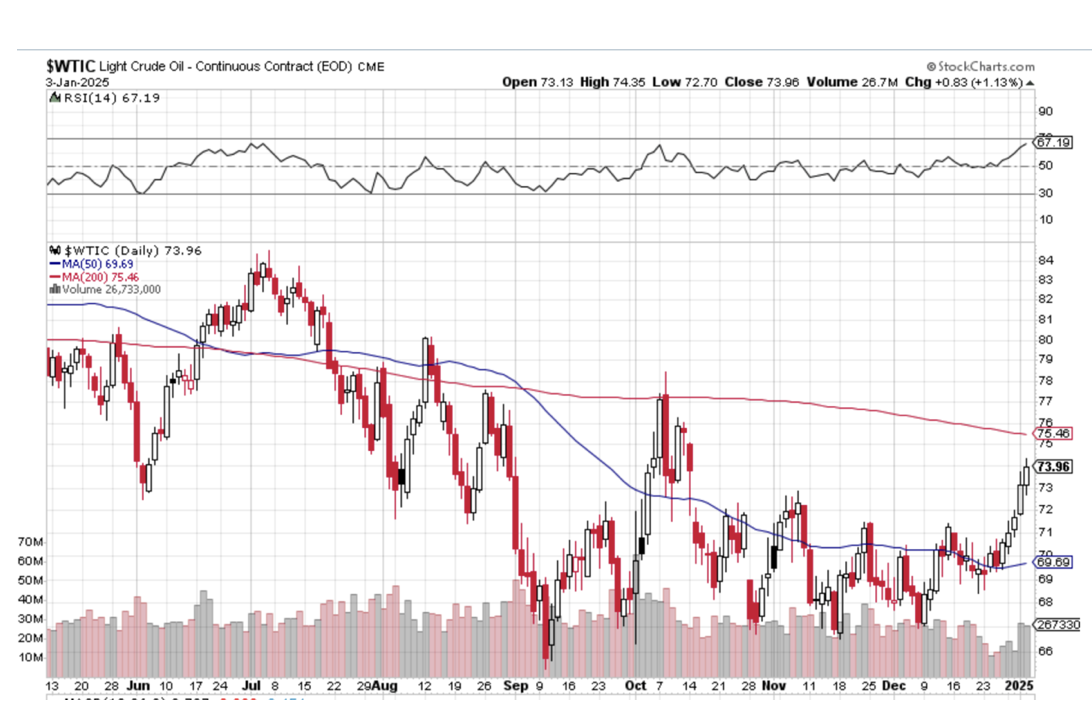

5) Commodities (FCX), (BHP), (RIO), (VALE), (DBA) Look at the chart of any commodity stock and you see grim death. Freeport McMoRan (FCX), BHP (BHP), and Rio Tinto (RIO), they’re all the same. They’re all afflicted with the same disease, over-dependence on a robustly growing China, which isn’t growing robustly, if at all.

I firmly believe that this will continue until the current leadership by President Xi Zheng Ping ends. He has spent the last decade globally expanding Chinese interests, engaging in abusive trade practices, hacking, and attacking American allies like Taiwan and the Philippines.You can only wave a red flag in front of the US before it comes back to bite you. A trade war with the US is now imminent.

This will happen sooner than later. The Chinese people don’t like being poor for very long. This is why I didn’t get sucked in on the Chinese long side in the fall, as many hedge funds did.

If China wants to go back to playing nice, as they did in the eighties and nineties, China should return to return to high growth and commodities will look like great “Buys” down here. If they don’t, American growth alone should eventually pull commodities up, as our economy is now growing at a long-term average gross unadjusted 6.00% rate. So the question is how long this takes.

It may pay to start nibbling on the best quality bombed-out names now, like those above.

Snow Angel on the Continental Divide

6) Energy (DIG), (USO), (DUG), (UNG), (USO), (XLE), (LNG), (CCJ), (VST), (SMR) Energy was one of the worst-performing sectors in the market for the second year in a row and 2025 is looking no better. New supplies are surging, while demand remains stuck in the mud, with the US now producing an incredible 13.5 million barrels a day. OPEC is dead.

EVs now make up 10% of the US auto fleet, and much more in other countries, are making a big dent. Some 50% of all new car sales in China, the world’s largest market, are EVs. The number of barrels of oil needed to increase a unit of American GDP is plunging, as it has done for 25 years, through increased efficiencies. Remember your old Lincoln Continental that used to get eight miles per gallon? Now it gets 27.

Worse yet, a major black swan hovers over the sector. If the Ukraine War somehow ends, some ten million barrels a day of Russian oil will hit the market. Oil prices should plunge to $50 a barrel.

There are always exceptions to the rule, and energy plays not dependent on the price of oil would be a good one. So is natural gas, which will benefit from Cheniere Energy’s (LNG) third export terminal coming online, increasing exports to China. Ukraine cutting off Russian gas flowing to Europe will assure there is plenty of new demand.

But I prefer investing in sectors that have tailwinds and not headwinds. Better leave energy to the pros who have the inside information they need to make money here.

If someone is holding a gun to your head tell you that you MUST invest in energy, go for the new nuclear plays like (CCJ), (VST), and (SMR). We are only at the becoming of the small modular reactor trend, which could accelerate for decades.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly, that it blew a passenger train over on its side. In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year. We also see countless abandoned 19th-century gold mines and the broken-down wooden trestles leading to huge piles of tailings, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

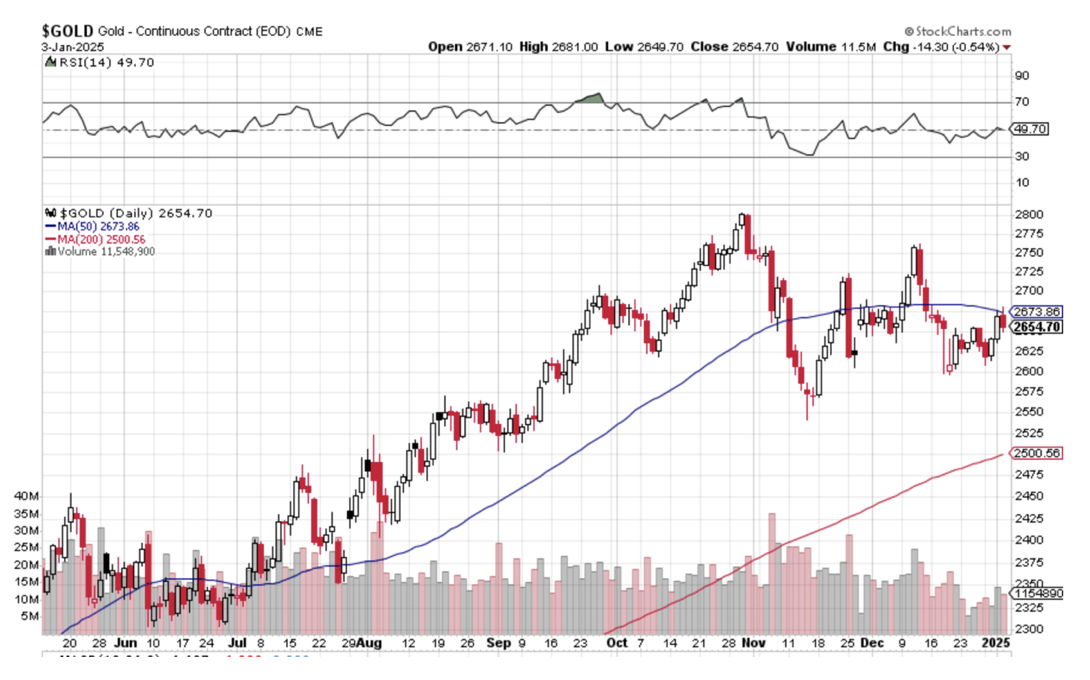

We certainly got a terrific run on precious metals in 2025, with gold at its highs up 33% and silver up 65%. The miners did even better. Even after the post-election selloff, it was still one of the best-performing asset classes of the year.

But the heat has definitely gone out of this trade. The prospect of higher interest rates for longer in 2025 has sent short-term traders elsewhere. That’s because the opportunity cost of owning precious metals is rising since they pay no interest rates or dividends. And let’s face it, there was definitely new competition for hot money from crypto, which doubled after the election.

The sector is not dead, it is resting. Central bank buying of the barbarous relic continues unabated, especially among sanctioned countries, like Russia and China. Gold is still the principal savings vehicle for many Chinese. They are not going to recover confidence in their own currency, banks, or government anytime soon. And there is still slow but steadily rising industrial demand from solar sectors.

Gold supply has also been falling for years, while costs are rising at least at double the headline inflation rate. So it’s just a matter of time before the supply/demand balance comes back in our favor. Where the final bottom is anyone’s guess as gold lacks the traditional valuation parameters of other asset classes, like dividends or interest paid. We’ll just have to wait for Mr. Market to tell us, who is always right.

Give (GLD), (SLV), (GDX), (GOLD), and (WPM) a rest for now but I’ll be back.

Crossing the Great Nevada Desert Near Area 51

8) Real Estate (ITB), (LEN), (KBH), (PHM), (DHI)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada. It is a route long traversed by roving bands of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the Transcontinental Railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley, California. Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

Real estate was a nice earner for us in 2024 in the new homes sector. The election promptly demolished this trade with the prospect of higher interest rates for longer. Expect this unwelcome drag to continue in 2025.

I am not expecting a housing crash unless interest rates take off. More likely it will continue to grind sideways on low volume. That’s because the market has support from a structural shortage of 10 million homes in the US, the debris left over from the 2008 housing crash. That’s why there is still a Millennial living in your basement. Homebuilders now prioritize profit margins over market share.

I expect this sector to come back someday. New homebuilders have the advantage of offering free upgrades and discounted in-house financing. Avoid for now (DHI), (KBH), (TOL), and (PHM).

Crossing the Bridge to Home Sweet Home

9) Postscript We have pulled into the station at Truckee amid a howling blizzard.

My loyal staff have made the ten-mile trek from my estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been cooling in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 80 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just coming into view across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my MacBook Pro, iPad, and iPhone, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak tonight and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above, which should be soon.

Good luck and good trading in 2025!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2025!

https://www.madhedgefundtrader.com/wp-content/uploads/2013/01/Zephyr.jpg342451april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-01-08 09:00:172025-02-20 12:40:412025 Annual Asset Class Review

It is always the sign of a great hedge fund manager when he makes money while he is wrong.

I have seen this throughout my life, trading with clients and friends like George Soros, Julian Robertson, Paul Tudor Jones, and David Tepper.

And wrong I certainly was in 2024.

I thought Trump would lose the election.

Then, I thought that markets would rocket no matter who won. Only the sector leadership would change.

How about one out of two?

The big question is: “Is a stock market crash now in front of us?” The answer is absolutely yes. It’s only a question of how soon.

At this point, we only know what Trump said. And as we all know, what Trump says and does, or can do are totally different things. It all adds a new and constant source of unknowns for the market.

Of course, it helps to have a half-century of trading experience, too. I like to tell my beginning subscribers, “Don’t worry, after the first 50 years, this gets easy.”

Except easy it is not, going into the next several couple of years.

In a few months, it will be Ground Hog Day, and Punxsutawney Phil will call the weather for the next six weeks from his hilltop in Gobbler’s Knob, Pennsylvania.

For the financial markets, it could mean six more MONTHS of winter.

Nobody wants to sell because they believe in a longer-term bull case going into yearend.

In the meantime, they are buying deregulation plays (JPM), (GS), (BLK), and Tesla (TSLA) as a hedge against the next Tweet.

We could see a repeat of the first half of 2017 when markets rocketed and then died.

This is what a Volatility Index (VIX), (VXX) is screaming right in your face, kissing the $13 handle.

The never-ending tweets are eroding the bull case by the day.

So, we’re at war with Canada now? Wait! I thought it was Mexico? No, it’s France. If it’s Tuesday, this must be Belgium.

And our new ally? Russia!

Even the Federal Reserve is hinting in yesterday’s statement that it is going into “RISK OFF” mode, possibly postponing a December interest rate cut indefinitely.

Unfortunately, that completely sucks the life out of our short Treasury bond trade (TLT), (TBT) for the time being, a big earner for us earlier this year.

Flat to rising interest rates also demolish small caps and other big borrowers (homebuilders, real estate, REITs, cruise lines).

The market is priced for perfection, and if perfection doesn’t show, we have a BIG problem.

All of this leads up to the good news that followers of the Mad Hedge Fund Trader enjoyed almost a perfect month in November.

Trade Alert Service in November

(DHI) 11/$135-$145 call spread

(GLD) 12/$435-$340 call spread

(TSLA) 12/$3.90-$400 put spread

(JPM) 11/$195-$205 call spread

(CCJ) 12/$41-44 call spread

(JPM) 12/$210-$220 call spread

(NVDA) 12/$117-$120 call spread

(TSLA) 12/$230-$240 call spread

(TSLA) 12/$250-$260 call spread

(TSLA) 12/$270-$275 call spread

(MS) 12/$110-$115 call spread

(C) 12/$60-$65 calls spread

(BAC) 12/$41-$44 call spreads

(VST) 12/$115-$120 call spread

(BLK) 12/$950-$960 call spread

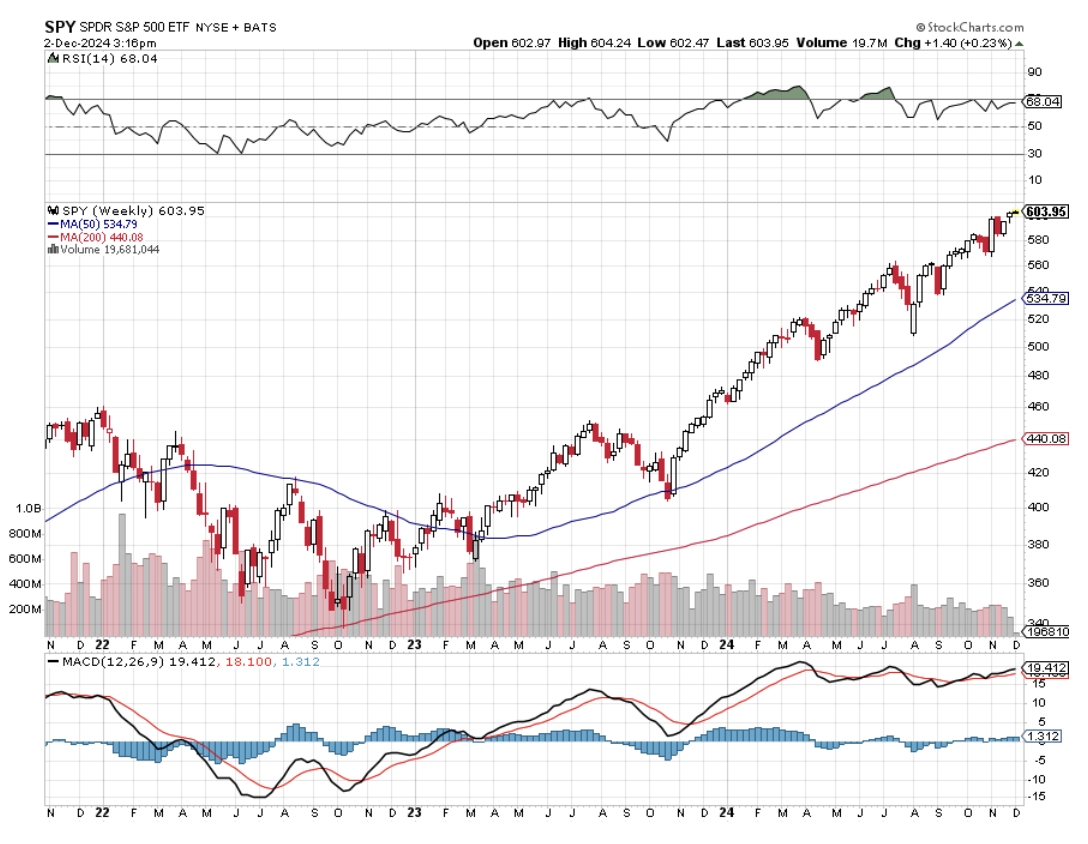

The net of all of this is that 2024 is looking like a gangbuster year for the Mad Hedge Fund Trader, up 18.96% in November and 72.00% YTD, compared to only 26.62% for the S&P 500.

It seems that the harder I work, the luckier I get.

Hanging With David Tepper

https://www.madhedgefundtrader.com/wp-content/uploads/2014/05/John-Thomas-David-Tepper.jpg303387april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-12-03 09:04:182024-12-03 11:36:37It's Groundhog Day

Below please find subscribers’ Q&A for the July 10 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village NV.

Q: Is the Fed waiting too long to cut interest rates?

A: Yes, they are. We are on a recession track if the Fed doesn’t move soon. In other words, the light at the end of the tunnel isn’t daylight—it’s an oncoming train. So, I think a September rate cut is a certainty. They want to see tomorrow’s data and make sure it’s cool. They need several months of really cool inflation data to justify the first rate cut and we probably are going to get that, so next update is tomorrow with the latest CPI number is crucial. Everybody’s sitting on their hands until then.

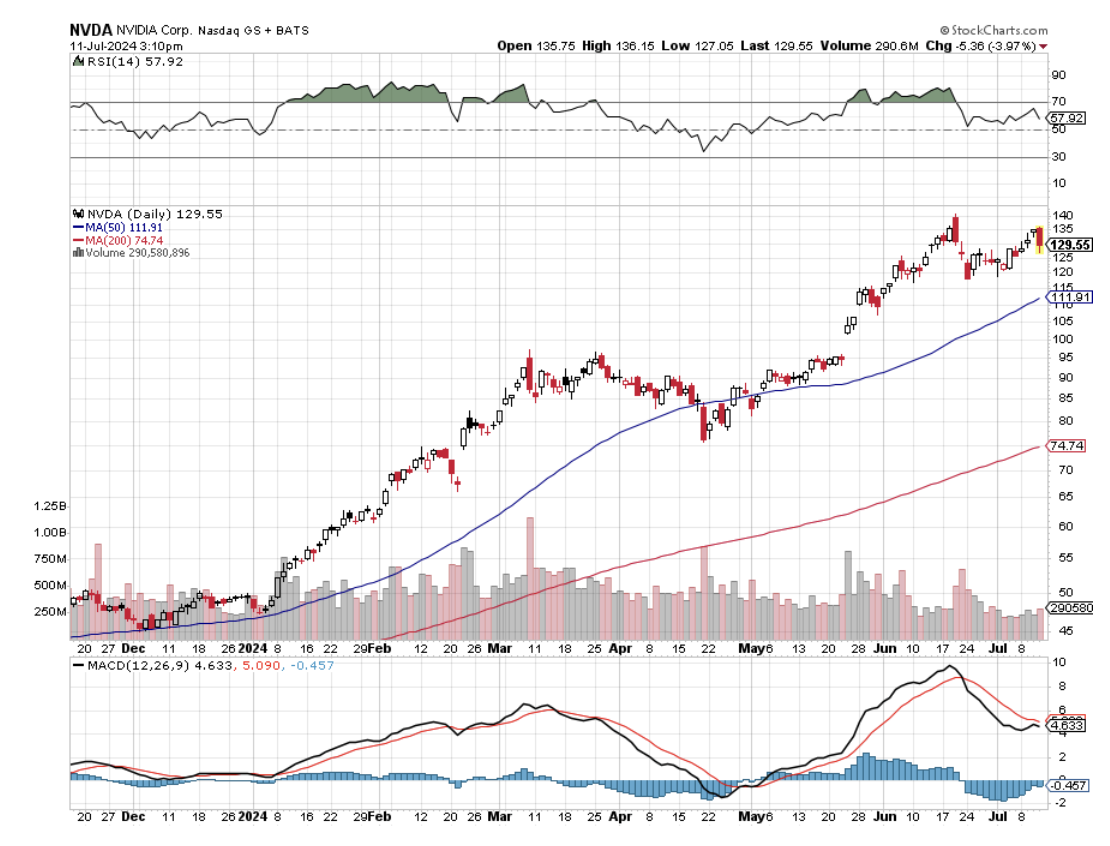

Q: When will NVIDIA (NVDA) hit a $4 trillion market valuation?

A: By the end of the year. We’re currently at $3.3 trillion, so another $700 billion is nothing for NVIDIA—you could do that in a day if you really wanted to. But give it until the end of the year, just to be conservative. The fact is, they have a global monopoly on the highest-priced product that everybody in the world has to buy or go out of business. It’s not a bad place to be—it’s kind of like where John D. Rockefeller was in the oil industry around 1900.

Q: What do you think about copper (COPX)? Should I maintain my longs?

A: Yes, all we need is further proof of falling interest rates and the entire commodities/precious metals sectors will take off like a rocket. So just sit with your positions. I put out a piece yesterday on copper. All that shines is not Copper, and it’s not dead it’s just resting, like the proverbial John Cleese parrot.

Q: Do you think a 10% stock market correction is likely before the election?

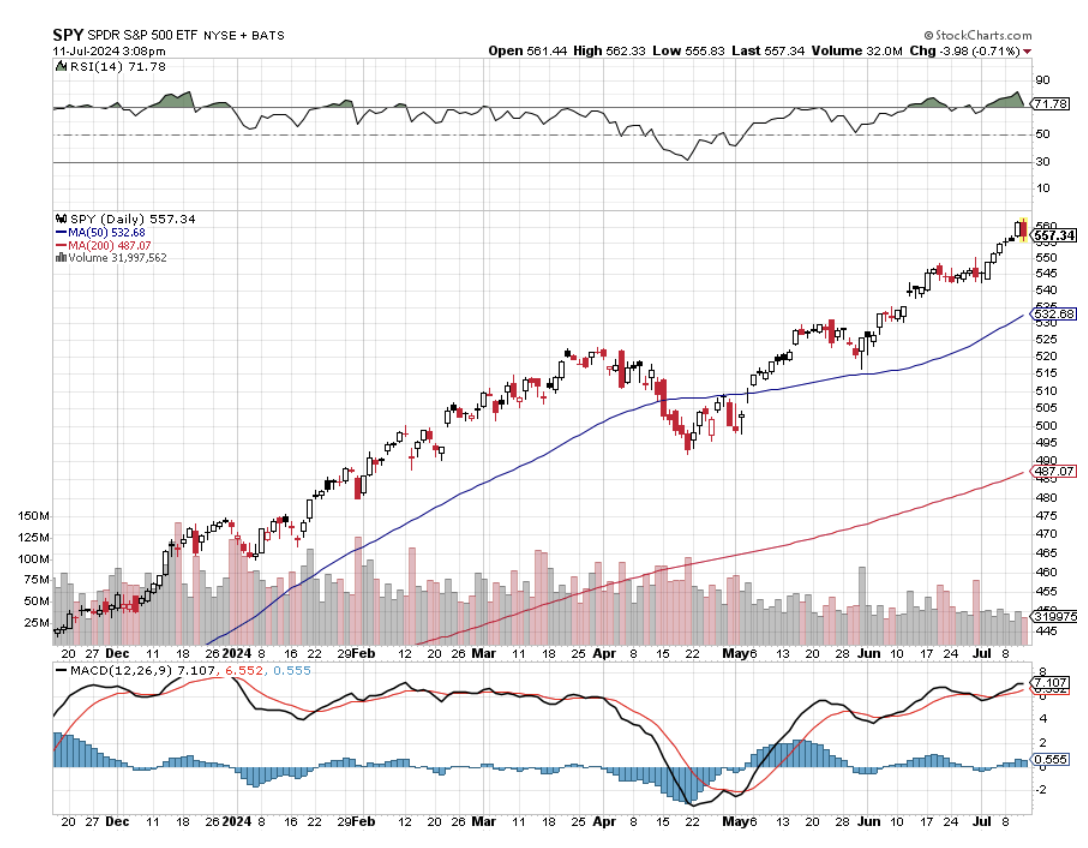

A: No, the most we’ve been able to get this year is 4% or 5% pullbacks, but not much more. We have a world with a cash glut that is underinvested in the face of a global monetary easing. Investors have been net sellers of stocks all of last year, so we were ripe for a meltup, which has, in fact, happened every day so far in July. So no, my S&P 500 target of 6,000 for the end of the year is starting to look too conservative given the moves that we’ve made lately. I’m very positive about that.

Q: Is the real estate market about to crash?

A: Well, the Florida housing collapse that is being driven by the insurance industry feeing that state. Insurance companies don’t like the hurricane risk going forward, which can cost tens of billions of dollars per event. Nobody there can get insurance anymore unless they pay outrageous amounts of money. Some people are only buying fire insurance to save money and skipping the storm insurance and rolling the dice, hoping the storms hit somewhere else in Florida. The fact is, you can’t get a home mortgage without insurance. Banks aren't willing to take the environmental risk of a house without insurance. No insurance means no bank loans, which means the market shrinks to a cash-only market. And there is a cash-only market in Florida, but it’s not at the $500,000 level, it’s more at the $50 million level. So that is a problem unique to Florida. Could it spread to other areas? Yes. Texas is having another energy crisis, as it has twice every year, ever since the power system was privatized there. No reserves for emergencies, no contingency, nothing that costs money basically. And then California definitely has a wildfire problem, although we’ve been getting off pretty light last year and this year. But the insurance companies don’t think like that. They are the classic 20/20 hindsight type companies.

Q: What’s the impact of the election on the market?

A: Zero. But it will defer buying until after the election. So if you have a 50/50 split on polls, uncertainty is at a maximum. People don’t like investing in uncertainty, they like sure things. After the election, you can expect a massive melt-up in the market no matter who wins because the uncertainty will be gone, and tech stocks will lead once again.

Q: What should I do with Nvidia (NVDA)?

A: I put out a report on this on Monday. You keep your long and write calls against them. And you can get quite a lot of money for just the August calls. I think the August $140 calls were selling for $3.50—they’re higher than that now, so you could even go out to August $145, and just keep doing that every month. If Nvidia takes off and you get taken out of your stock, you’re selling it essentially at $143.50. So that is an excellent trade—a lot of the big institutions are doing that now.

Q: Tesla's (TSLA) been on a big rally for the past month; do you expect it to continue?

A: I expect it to take a break, but the long-term uptrend is now back for good, for lots of different reasons. The immediate headline reason was because the Chinese government allowed the buying of Teslas for the first time—they are made in China after all. Second, they had a good earnings beat, so this caused a massive short-covering rally. The shorts got crushed by Tesla once again, as they have been consistently doing for the last 15 years, really. I saw a number of cumulative losses on short positions on Tesla stock since inception: $100 billion. Most of those losses were incurred by oil companies trying to put Tesla out of business.

Q: What do you call a substantial dip?

A: It’s different for every stock—for some it’s 2%, for others like Tesla or Nvidia it’s 20%. It depends on the volatility of the stock; you just have to look at the charts and make your own call.

Q: What do you think for the next earnings season?

A: It’ll be great for technology stocks and not so great for domestics as their businesses cool off.

Q: Is there anything Europe and American EV producers can do to compete against the Chinese at these lower prices?

A: Yes: keep quality high, therefore profits high, therefore profit margins high. That was the Japanese strategy in the US from the 1980s onwards, and it was hugely successful. You can cede the money-losing part—the low-end part of the market, to the Chinese. The quality of the Chinese EVs is terrible, they start to fall apart after four years, and I learned this from several Chinese EV drivers in Ecuador where they have a substantial market share already. But at $15,000 plus the shipping, you don’t make a lot of money in EVs.

Q: Is it a good time to buy put LEAPS on the ProShares UltraShort 20+ Year Treasury (TBT)?

A: Yes, especially if you’re willing to do an at-the-money and bet that the interest rates stay here or lower for the next year. You’d probably get a 100% return on that, but why bother? Because on the TBT itself, you have a much wider trading spread than the (TLT), therefore the dealing costs are higher. You might as well just go and do the long (TLT) LEAP instead.

Q: Chipotle Mexican Grill (CMG) stock has been really successful for the last five years, but it just dropped 20%, should I get in?

A: It’s a very low-margin business—I avoid those. There’s not a lot of meat in the burrito business. It doesn’t have the key elements of success. (Not just Chipotle, but with the whole industry.) It's not like you’re designing 96 stock microprocessors.

Q: Are AI stocks overhyped at this point?

A: Absolutely yes, but they can stay overhyped for another three or four years, so I think we're just at the beginning of a very long-term run. And the people who have been involved so far are making the biggest money in their lives.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.