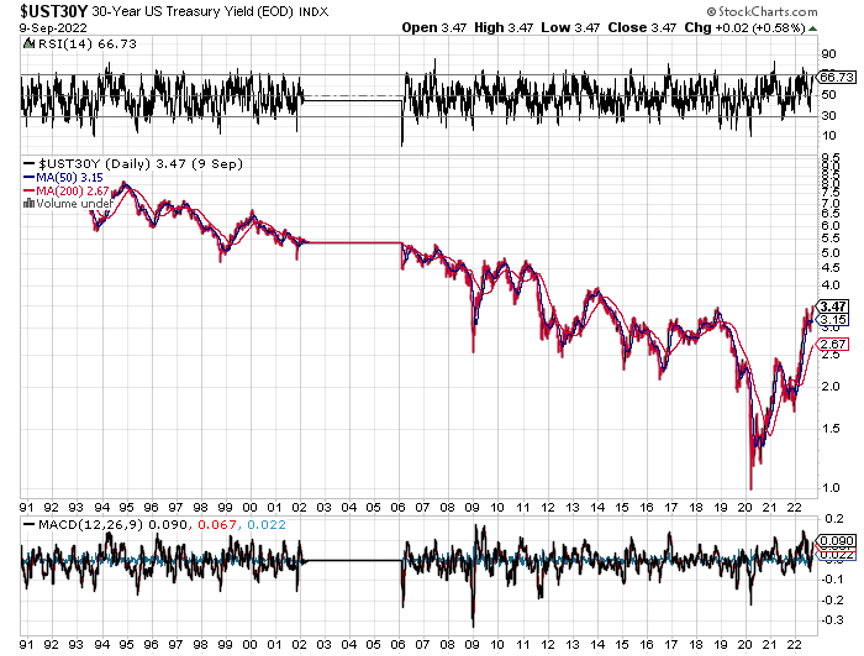

With ten-year US Treasury yields hitting 4.00% yesterday, it’s time to pay the piper for the last 15 years of the borrowing rampage of epic proportions.

This is not a new thing.

We are, in fact, becoming the United States of Debt.

That Washington is taking the lead in this frenzy of borrowing is undeniable. The last administration took the national debt from $23 trillion to $28 trillion during four years of prosperity that was entirely borrowed from the future.

The Biden administration will eventually take that figure up to an eye-popping $38 trillion. That will be the final bill for ending the pandemic, putting 25 million people back to work, and bringing the second Great Depression to a close.

The National Debt exceeded US GDP in 2016, taking the debt to GDP ratio to the highest point since WWII.

Treasury Secretary Janet Yellen recently confided to me that, “It’s the kind of thing that should keep you awake at night.”

It gets worse.

According to the Federal Reserve Bank of New York, total personal debt topped $19 trillion by the end of 2020. An overwhelming share of personal consumption is now funded by credit card borrowing.

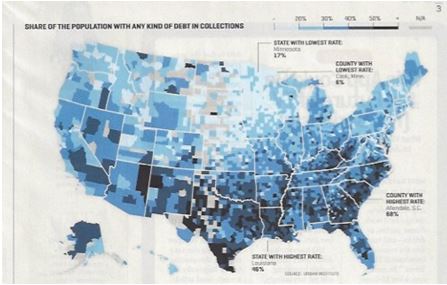

Some 33% of Americans now have debts in some form a collection, and that figure reaches an astonishing 50% in many southern states (see map below). Call it the Confederate States of Debt.

Corporations have also been visiting the money trough with increasing frequency, taking their debt to $6.1 trillion, up by 39% in five years, and by 85% in a decade.

The debt to capital ratio of the top 1,000 companies has ballooned from 35% to 54% and is now the highest in 20 years.

Another foreboding indicator is that corporate debt is rising faster than sales, with debt rising by a breakneck 8.5% annualized compared to 4.6% for sales over the past decade.

Automobile debt now tops $1 trillion and with lax standards has become the new subprime market.

And remember that other 800-pound gorilla in the room?

Student debt now exceeds $1.6 trillion and is rising, as is the default rate. Provisions in the last tax bill eliminate the deductibility of the interest on student debt, making lives increasingly miserable for young borrowers. And you wonder why the US birth rate is so low.

Of course, you can blame the low interest rates that have prevailed for the past decade. Who doesn’t want to borrow when the inflation adjusted long-term cost of money is FREE?

That explains why Apple (AAPL), with $270 billion in cash reserves held overseas, borrowed last year via ultra-low coupon 30-year bond issues, even though it doesn’t need the money. Many other major corporations have done the same.

And while everything looks fine on paper now, what happens if interest rates ever rise and stay high?

The Feds will be in dire straight very quickly. Raise short term rates to the 6% seen at the peak of the last cycle, and the nation’s debt service rockets from 4% to over 10% of the total budget. That’s when the sushi really hits the fan.

You can expect the same kind of vicious math to strike across the entire spectrum of heavily leveraged borrowers going forward, including big borrowers like cruise line, airlines, you, and me.

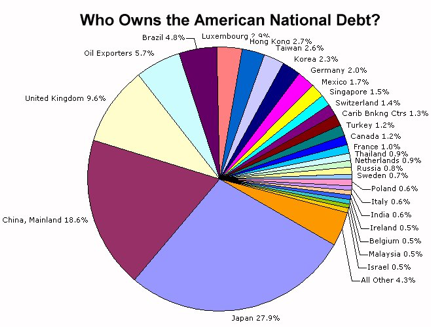

We are also witnessing the withdrawal of the Chinese as major Treasury bond buyers, who along with other sovereign buyers historically took as much as 50% of every issue. Threaten a war on your largest lender and it plays hell with you cash flow.

Rising supply against fewer buyers sounds like a recipe for eventually much higher interest rates to me.

Just watch this space for the next Trade Alert regarding when to get back in for the umpteenth time.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/02/american-debt.jpg285447Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-29 10:02:592022-09-29 12:12:42The United States of Debt

When I was a little kid during the early 1950s, my grandfather used to endlessly rail against Franklin Delano Roosevelt.

The WWI veteran, who was mustard gassed in the trenches of France and was a lifetime, died in the wool Republican, said the former president was a dictator and a traitor to his class, who trampled the constitution with complete disregard.

Republican presidential candidates Hoover, Landon, and Dewey would have done much better jobs.

What was worse, FDR had run up such enormous debts during the Great Depression that, not only would my life be ruined, so would my children’s lives.

As a six-year-old, this disturbed me deeply, as it appeared that just out of diapers, my life was already going to be dull, brutish, and pointless.

Grandpa continued his ranting until a three pack a day Lucky Strike non-filter habit finally killed him in 1977.

He insisted until the day he died that there was no definitive proof that cigarettes caused lung cancer, even though during his war, they referred to them as “coffin nails.”

He was stubborn as a mule to the end. And you wonder whom I got it from?

What my grandfather’s comments did do was spark in me a lifetime interest in the government bond market, not only ours, but everyone else’s around the world.

So, what ever happened to the despised, future destroying Roosevelt debt?

In short, it went to money heaven.

And here I like to use the old movie analogy. Remember, when someone walked into a diner in those old black and white flicks? Check out the prices on the menu on the wall. It says “Coffee: 5 cents, Hamburgers: 10 cents, Steak: 50 cents.”

That is where the Roosevelt debt went.

By the time the 20 and 30-year Treasury bonds issued in the 1930’\s came due, WWII, Korea, and Vietnam happened, and the great inflation that followed.

The purchasing power of the dollar cratered, falling roughly 90%. Coffee is now $1.00, a hamburger at McDonald’s is $5.00, and a cheap steak at Outback cost $12.00.

The government, in effect, only had to pay back 10 cents on the dollar in terms of current purchasing power on whatever it borrowed in the thirties.

Who paid for this free lunch?

Bond owners who received minimal and often negative real inflation-adjusted returns on fixed income investments for three decades.

In the end, it was the risk avoiders who picked up the tab. This is why bonds became known as “certificates of confiscation” during the seventies and eighties.

This is not a new thing. About 300 years ago, governments figured out there was easy money to be had by issuing paper money, borrowing massively, stimulating the local economy, creating inflation, and then repaying the debt in devalued future paper money.

This is one of the main reasons why we have governments, and why they have grown so big. Unsurprisingly, France was the first, followed by England and every other major country.

Ever wonder how the new, impoverished United States paid for the Revolutionary War?

It issued paper money by the bale, which dropped in purchasing power by two thirds by the end of conflict in 1783. The British helped too by flooding the country with counterfeit paper Continental money.

Bondholders can expect to receive a long series of rude awakenings sometime in the future.

No wonder Bill Gross, the former head of bond giant PIMCO, says he will get ashes in his stocking for Christmas next year.

The scary thing is that eventually, we will enter a new 30-year bear market for bonds that lasts all the way until 2049. However, after last month’s frenetic spike up in bond prices and down in bond yields, that is looking more like a 2022 than a 2019 position.

This is certainly what the demographics are saying, which predicts an inflationary blow-off in decades to come that could take short term Treasury yields to a nosebleed 12% high once more.

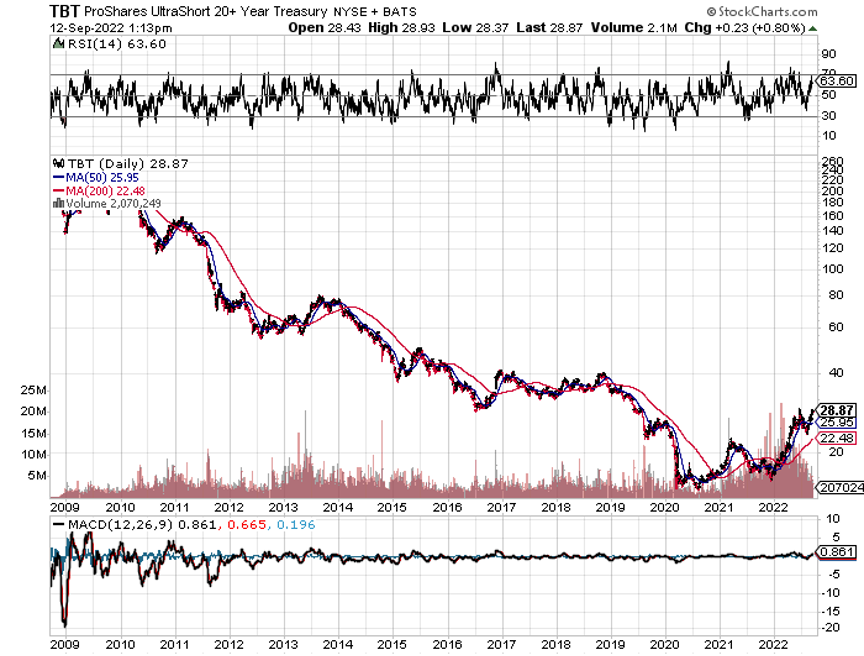

That scenario has the leveraged short Treasury bond ETF (TBT), which has just cratered down to $23, double to $46, and then soaring all the way to $200.

If you wonder how yields could get that high in a decade, consider one important fact.

The largest buyers of American bonds for the past three decades have been Japan and China. Between them, they have soaked up over $2 trillion worth of our debt, some 12% of the total outstanding.

Unfortunately, both countries have already entered very negative demographic pyramids, which will forestall any future large purchases of foreign bonds. They are going to need the money at home to care for burgeoning populations of old age pensioners.

So who becomes the buyer of last resort? No one, unless the Federal Reserve comes back with QE IV, V, and VI. QE IV, in fact, has already started.

There is a lesson to be learned today from the demise of the Roosevelt debt.

It tells us that the government should be borrowing as much as it can right now with the longest maturity possible at these ultra-low interest rates and spending it all.

With real, inflation adjusted 10-year Treasury bonds now posting negative yields, they have a free pass to do so.

In effect, the government never has to pay back the money. But they do have the ability to reap immediate benefits, such as through stimulating the economy with greatly increased infrastructure spending.

Heaven knows we need it.

If I were king of the world, I would borrow $5 trillion tomorrow and disburse it only in areas that create domestic US jobs. Not a penny should go to new social programs. Long-term capital investments should be the sole target.

Here is my shopping list:

$1 trillion – new Interstate freeway system

$1 trillion – additional infrastructure repairs and maintenance

$1 trillion – conversion of our energy system to solar

$1 trillion – construction of a rural broadband network

$1 trillion – investment in R&D for everything

The projects above would create 5 million new jobs quickly. Who would pay for all of this in terms of lost purchasing power? Today’s investors in government bonds, half of whom are foreigners, principally the Chinese and Japanese. Notice that I am not committing a single dollar in spending on any walls.

How did my life turn out? Was it ruined, as my grandfather predicted?

Actually, I did pretty well for myself, as did the rest of my generation, the baby boomers.

My kids did OK too. One son just got a $1 million, two year package at a new tech startup and he is only 30. Another is deeply involved in the tech industry, and my oldest daughter is working on a PhD at the University of California. My two youngest girls became the first ever female eagle scouts.

Not too shabby.

Grandpa was always a better historian than a forecaster. But he did have the last laugh. He made a fortune in real estate, betting correctly on the inflation that always follows big borrowing binges.

You know the five acres that sits under the Bellagio Hotel in Las Vegas today? That’s the land he bought in 1945 for $500. He sold it 32 years later for $10 million.

Not too shabby either.

32 Years of 30-Year Bond Yields

Not Too Shabby for $500

https://www.madhedgefundtrader.com/wp-content/uploads/2015/12/Bellagio-e1467928305548.jpg271400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-09-14 10:02:152022-09-14 12:28:23What Ever Happened to the Great Depression Debt?

Thanks to the relentless increase in prices, the value of my home has risen by $4 million over the last ten years, and $2 million over the last three years alone.

And I’m not the only one.

Some 66% of Americans own their own homes and may have seen similar price increases or more.

So, what if the price of a gallon of milk goes up by $1? I’ll happily pay that if it means my largest personal investment appreciates at triple-digit rates. Besides, I’m lactose intolerant anyway, and all my kids have grown up.

I’ll tell you what else inflation does. It makes stocks really cheap. That’s because investors fear that the Fed will raise interest rates by too much, destroy company earnings, and trigger a recession.

This is counterintuitive because companies actually benefit from inflation because they can get away with faster price increases more often, boosting profits. I took my kids out to a graduation dinner yesterday and practically had to take out a second mortgage to do so.

Personally, I believe that such a stock market bottom is close. But while the last bottom was within 10%, or 200 S&P 500 (SPX) points in terms of price, it is only 50% in terms of time. That signals a great new bull market for stocks beginning sometime this summer. Then anything you touch will double in three years.

You will look like a genius….again!

You can see who agrees with me by looking at which stocks are already getting bought up. Coca-Cola (KO), Johnson & Johnson (JNJ), and Procter & Gamble (PG) are the kind of safe, dividend-paying, brand name stocks that very long-term investors like pension funds love to own. They tend to buy and hold….forever.

No meme stocks here.

It isn’t just the Fed that is raising interest rates, which can only control overnight rates. The US budget deficit is falling at the fastest rate since WWII, possibly taking us to a budget surplus by year-end. As a result, the money supply is shrinking at the fastest rate in 60 years.

QT, or quantitative tightening, will fan the flames when it starts on January 1, ultimately taking up to $9 trillion out of the financial system.

Remember all that liquidity from QE, near-zero rates, and massive government spending that saved the economy from Armageddon? Play for movie in reverse and you get the oppositive result, i.e. falling share prices….at least for a while.

The battle as to who is right about the direction of the economy continues unabated. Is it bonds or stocks? At the rates that stocks have been plunging, stocks are essentially anticipating another Great Depression.

Ten-year US Treasury yields that soared from 1.33% to 3.12% in a mere six months are proclaiming that happy days are here again and will last forever. Since January, the average monthly mortgage payment has jumped by $450 a month. If that isn’t recessionary, I don’t know what is.

As a 53-year veteran of these markets, I can tell you that the bond market is always right. That’s because the money spent on equity research has shrunk to a shadow of its former self in recent decades, while bond research is as strong as ever.

Always listen to the guy with the $10 million budget and ignore the one with the $500,000 budget, which means that in the coming months, equity prognosticators will realize the error of their ways and come over to my way of thinking once again.

The Fed Minutes were not so horrible, downplaying the risk of a full 1% rate rise, triggering a 1,000-point rally in the Dow. With five up days in a row, this is starting to look like THE bottom. Is this the light at the end of the tunnel?

Q1 GDP dives 1.5% in its final read. It’s the worst quarter since the pandemic began during Q2 2022. Weekly Jobless Claims dropped 8,000 to 210,000.

NVIDIA Rips, surprising to the upside on almost every front, sending the stock up $30, or 18.75%. Mad Hedge followers bought (NVDA) last week. This is one of the best-run companies in the world. I expect the shares to rise from the current $178.51 to $1,000 in five years. Buy (NVDA) on dips.

The Consumer will keep driving the economy, says Bank of America CEO Brian Moynihan. Betting against the American consumer has always been a fool’s errand. I’m with Brian. Cash levels this high were never followed by recessions.

Only 18% of Americans will increase stockholdings this year, which is usually what you get at market bottoms. It was closer to 100% at the December top. Yet another signal that we are approaching the bottom in price, if not time.

New Home Sales dive in April, down 16.6% on a signed contract basis, the weakest in two years. The macro is definitely conspiring against the market. It’s all about interest rates. The average monthly mortgage payment has rocketed by $450 a month since January. Inventories have also soared from 6 to 9 months.

Advertising is in free fall, especially the online version, a usual pre-recession indicator. It is the easiest and first expense companies cut when they expect flagging sales. Look no further than yesterday’s astonishing 43% collapse in Snap (SNAP). Notice that TV commercials are getting endlessly repeated as the number of advertisers and ad rates fall. If I see one more ad for Interactive Brokers, I’ll shoot myself.

The EV Shortage worsens, with wait times for a new Tesla extending beyond a year. I can sell my Model X for more than I paid for it three years ago. Gasoline at $6.00 is converting a lot of drivers, and gas lines this summer loom. Big three dealers are price gouging on the few EVs they have, charging well over list. Good luck finding a Rivian pick-up; that’s a two-year wait. Maybe that makes (TSLA) a “BUY” down here?

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With some of the greatest market volatility seen since 1987, my May month-to-date performance recovered to +8.80%.

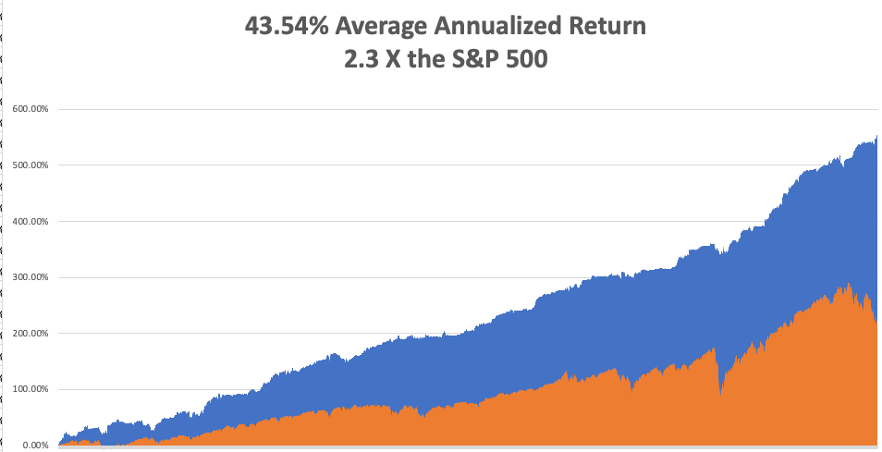

My 2022 year-to-date performance exploded to 38.98%, a new high. The Dow Average is down -9.30% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 61.22%.

Last week was a quiet one, with me using the monster rally to add new shorts in Apple (AAPL) and the S&P 500 (SPY).

That brings my 14-year total return to 551.54%, some 2.40 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 43.54%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 84 million, up 1.5million in a week, and deaths topping 1,004,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, May 30, markets are closed for Memorial Day. On Tuesday, May 31 at 9:00 AM EST, the S&P Case Shiller National Home Price Index for March is released.

On Wednesday, June 1 at 10:00 AM, JOLTS Job Openings for April are published.

On Thursday, June 2 at 8:30 AM, Weekly Jobless Claims are out. We also learn the ADP Private Employment Report for May.

On Friday, June 3 at 8:30 AM, the big Nonfarm Payroll Report for May is disclosed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, as a lifetime oenophile, or wine lover, I long searched for the Holy Grail of the perfect bottle. I finally found my quarry in 1989.

During the 19th century, Russia was still an emerging country that sought to import advanced European technology. So, they sent agents to the top wine-growing regions of the continent to bring back grapevine cuttings to create a domestic wine industry. They succeeded beyond all expectations building a major wine industry in Crimea on the Black Sea.

Then the Russian Revolution broke out in 1918.

Czar Nicholas II and his family were executed, and eventually, the wine industry was taken over by the Soviet state. They kept it going because wine exports brought in valuable foreign exchange with which the government could use to industrialize the country.

Then the Germans invaded in 1941.

Not wanting the enemy to capture a 100-year stockpile of fine wine, the managers of the Massandra winery dug a 100-yard-deep cave, moved their bottles in, bricked up the entrance, and hid it with shrubs. Then everyone involved in storing the wine was killed in the war.

Some 45 years later, looking to expand the facility, some Massandra workers stumbled across the entrance to the cave. Inside, they found a million bottles dating back to the 1850s kept in perfect storage conditions. It was a sensation in the wine collecting world.

To cash in, they hired Sotheby’s in London to repackage and auction off the wine one case at a time. It was the auction event of the year. For years afterwards, you could buy glasses of 100-year-old ports and sherries from the Czar’s own private stock at your local neighborhood restaurant for $5, the deal of the century.

I attended the auction at Sotheby’s packed Bond Street offices. The superstars of the wine collecting world were there with open checkbooks. I sat there with my paddle number 138 but was outbid repeatedly and wondered if I would get anything. In the end, I managed to pick up some of the less popular cases, a 1915 Madeira, a 1936 white port, and a 1938 sherry for about $25 a bottle each.

For years, these were my special occasion wines. I opened one when I was appointed a director of Morgan Stanley. Others went to favored clients at Christmas. My 50th, 60th, and 70th birthdays ate into the inventory. So did the birth of children number four and five. Several high school fundraisers saw bottles earn $1,000 each.

One of the 1915’s met its end when I came home from the Gulf War in 1992. Hey, the last Czar didn’t drink it and looked what happened to him! Another one bit the dust when I sold my hedge fund at the absolute market top in 1999. So did capturing 6,000 new subscribers for the Mad Hedge Fund Trader in 2010.

It turns out that the empties were quite nice too, 100-year-old hand-blown green glass, each one is a sculpture in its own right.

I am now reaching the end of the road and only have a half dozen bottles left. I could always sell them on eBay where they now fetch up to $1,000 a bottle.

But you know what? I’d rather have six more celebrations than take in a few grand.

Any suggestions?

Stay Healthy,

John Thomas

CEO & Publisher

https://www.madhedgefundtrader.com/wp-content/uploads/2022/05/madeira.png1178884Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-05-31 11:02:492022-05-31 12:43:43The Market Outlook for the Week Ahead, or Why I Love Inflation

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ALL QUIET ON THE WESTERN FRONT)

(SPY), (TLT), (TBT), (GOOGL), (AAPL), (MSFT), (BRKB), (NVDA), (JPM), (BAC), (WFC), ($BTCUSD)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-05-23 10:04:072022-05-23 16:38:00May 23, 2022

When I first joined Morgan Stanley in 1983, a number of my clients were old enough to have experienced the 1929 stock market crash and the Great Depression that followed.

One was Sir John Templeton, who confided in me over lunch at his antebellum-style mansion at Lyford Cay in the Bahamas, that his long career started with a lot of excitement, and then became incredibly boring for a decade.

It looks like we entered the incredibly boring phase on January 4, when the stock market began its current downtrend. Last week brought the longest weekly losing streak since 1923, some eight weeks so far.

The market is actually down a lot more than it looks, meaning that we are a lot closer to the bottom than you think. Some 87% of the S&P 500 is down more than 10% and 61% is down 20%. The damage is far worse with the NASDAQ, with some 93% of shares down 10%, and a gut-punching 73% down 20% or more.

While tech has already gone down a lot, some 32% so far this year, it is still trading at an 18% premium to the main market. Remember, in this business, timing is everything. If you invested in tech at the Dotcom peak in 1999, it took you 14 years to break even. Latecomers in this cycle could suffer a similar duration of pain and suffering.

And while these are the kind of moves that usually precede a recession, there is still an overwhelming amount of data that says it won’t happen. We here at Mad Hedge Fund Trader analyze, dissect, and examine data all day long.

I will once again repeat what my UCLA math professor told me a half-century ago. “Statistics are like a bikini bathing suit; what they reveal is fascinating, but what they conceal is essential.”

For a start, 3.6% unemployment rates are not what recessions are made of. Double-digit ones are. The next jobless rate print in June is likely to be down, not up. The country in fact is suffering its worst worker shortage in 80 years. There are currently 6 million more jobs than workers. And wages are rising, putting more money in the pockets of consumers.

Last month, airline ticket prices rose by 25%. Good luck trying to get a plane anywhere as all are full. Last winter, I bought a first-class round-trip ticket from San Francisco to London for $6,000. Today, the same ticket is $10,000. During recessions, planes fly empty, routes get cancelled, and staff laid off. Airlines also go bust and are not subject to the takeover wars we are seeing now. Recessions also bring dramatic credit crises. Rising default rates force banks to retreat from lending, FICO scores tank, and debt markets dry up. It’s all quiet on the western front now, with all fixed income and liquidity indicators are solidly in the green. And while interest rates are higher, they are nowhere near the peaks seen during past recessions.

All this may explain that after the horrific market moves we have already seen but we may be only 4% from the final bottom in this bear move to an S&P 500 at $3,600, or 7% from an (SPX) of $3,500. That means it is time to start scaling into long-term positions now in the best quality names.

That’s why I have been aggressively piling on call spreads in technology that are 10%-20% in the money with only 19 days to expiration, making money hand over fist.

An interesting headline caught my attention last week. The Russians were stealing farm equipment from Ukraine on an epic scale. When they couldn’t steal it, such as when the electronics were disabled, they were destroying it.

That means the Russians didn’t invade Ukraine to get more beachfront territory on the Black Sea, although that is definitely a plus. They want to destroy a competitor’s agricultural production in order to raise the value of their own output.

Yes, this is the beginning of the Resource Wars that could continue for the rest of this century. Resource producers like the US, Russia, Canada, Australia, and Ukraine will be the big winners. Resource consumers like China, India, and the Middle East will be the big losers.

JP Morgan cuts US GDP Forecasts, with the second half marked down from 3% to 2.4% and 2023 from 2.1% to 1.5%. This means no recession, which requires two back-to-back negative quarters.

China’s Industrial Production collapses by 2.9%, and Retail Sales fell by a shocking 11.1%. The Shanghai shutdown is to blame. It means longer supply chain disruptions for longer and another drag on our own economy. If Tesla has a bad quarter, it will be because of a shortage of vehicles in China. So, will the end of Covid in China bring the bull market back in the US?

The US Budget Deficit is in free fall, putting our hefty bond shorts at risk. While Trump was president the national debt exploded by $4 trillion, a dream come true for bond shorts. Since Biden became president, the annual budget deficit has plunged from $3.1 trillion to $360 billion for the first seven months of fiscal 2022, and we could approach zero by yearend. An exploding economy has sent tax revenues soaring, and taxpayers still have to pay a gigantic bill for last year’s monster capital gains in the stock market. Biden has also been unable to get many spending bills through the Senate, where he lacks a clear majority.

India Bans Food Exports. Climate change is destroying its output with heat waves, while the Ukraine War has eliminated 13% of the world’s calories. This is a problem when you have 1.2 billion to feed. Expect food inflation to worsen.

Consumer Sentiment hits an 11-year low according to the University of Michigan, dipping from 64 to 59.1. Record gas prices and soaring inflation are the reasons, but spending remains strong off the super strong jobs market.

Homebuilder Sentiment hits a two-year low, down from 77 to 69 in May, according to the National Association of Homebuilders. Recession fears and soaring interest rates are the big reasons.

Building Permits dive in April by 3.2%, and single family permits were down 4.6%. The onslaught of bad news for housing continues. Avoid.

Target implodes on terrible earnings, taking the stock down 25%, the worst in 40 years. They finally got the inventory they wanted. Too bad consumers are too poor to buy it with $6.00 a gallon.

Commodities send Battery Costs soaring by 22%. Who knew you were going long copper, lithium, and chromium when you bought your Tesla? It’s a good thing you did. Now you can give the middle finger salute when you drive past gas stations.

Average Household now spending $5,000 a year on gasoline, which is $5,000 they’re not spending on anything else. Just ask Target (TGT) and Walmart (WMT). My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With some of the greatest market volatility seen since 1987, my May month-to-date performance recovered to +4.79%.

My 2022 year-to-date performance exploded to 34.97%, a new high. The Dow Average is down -16.4% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 62.99%.

This week, I added new long positions in Visa (V) and Microsoft (MSFT) when the Volatility Index (VIX) was in the mid $30s. I also did a nice round trip on an Apple (AAPL) short which brought in $1,740. I also took profits on two longs in the (SPY) and two shorts in the (TLT). Overall, it was a great week!

That brings my 14-year total return to 547.53%, some 2.40 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 43.78%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 82.5 million, up 300,000 in a week and deaths topping 1,000,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, May 23 at 8:30 AM EST, the Chicago Fed National Activity Index for April is out. On Tuesday, May 24 at 8:30 AM, New Home Sales for April are released.

On Wednesday, May 25 at 8:30 AM, Durable Goods for April are published.

On Thursday, May 26 at 8:30 AM, Weekly Jobless Claims are disclosed. The first look at Q2 GDP is printed.

On Friday, May 27 at 8:30 AM, Personal Income & Spending is out. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, one of my fondest memories takes me back to England in 1984 for the 40th anniversary of the D-Day invasion of France. On June 6, 160,000 Americans stormed Utah and Omaha beaches, paving the way for the end of WWII.

My own Uncle Al was a participant and used to thrill me with his hair-raising D-Day experiences. When he passed away, I inherited the P-38 Walther he captured from a German officer that day.

The British government wanted to go all out to make this celebration a big one as this was expected to be the last when most veterans, now in their late fifties and sixties, were in reasonable health. President Ronald Reagan and prime minister Margaret Thatcher were to be the keynote speakers.

The Royal Air Force was planning a fly past of their entire fleet that started over Buckingham Palace, went on the to the debarkation ports at Southampton and Portsmouth, and then over the invasion beaches. It was to be led by a WWII Lancaster bomber, two Supermarine Spitfire, and two Hawker Hurricane fighters.

The only thing missing was American aircraft. The Naval and Military Club in London, where I am still a member, wondered if I would be willing to participate with my own US-registered twin-engine plane?

“Hell yes,” was my response.

Of course, the big concern was the weather, as it was in 1944. Our prayers were answered with a crystal clear day and a gentle westerly wind. The entire RAF was in the air, and I found myself the tail end Charlie following 175 planes. I was joined by my uncle, Medal of Honor winner Colonel Mitchell Paige.

We flew 500 feet right over the Palace. I could clearly see the Queen, a WWII veteran herself, Prince Philip, Lady Diana, and her family waving from the front balcony. Massive shoulder-to-shoulder crowds packed St. James Park in front.

As I passed over the coast, much of the Royal Navy were out letting their horns go full blast. Then it was southeast to the beaches. I flew over Pont du Hoc, which after 40 years still looked like a green moonscape, after a very heavy bombardment.

In one of the most courageous acts in American history, a company of Army Rangers battled their way up 100-foot sheer cliffs. After losing a third of their men, they discovered that the heavy guns they were supposed to disable turned out to be telephone poles. The real guns had been moved inland 400 yards.

We peeled off from the air armada and landed at Caen Aerodrome. Taxiing to my parking space, I drove over the rails for a German V2 launching pad. I took a car to the Normandy American Cemetery at Colleville-sur-Mer where Reagan and Thatcher were making their speeches in front of 9,400 neatly manicured graves.

There were thousands of veterans present from all the participating countries, some wearing period uniforms, most wearing ribbons. At one point, men from the 101st Airborne Division parachuted overhead from vintage DC-3’s and landed near the cemetery.

Even though some men were in their sixties and seventies, they still made successful jumps, landing with big grins on their faces. The task was made far easier without the 100 pounds of gear they carried in 1944.

The 78th anniversary of the D-Day invasion is coming up shortly. I won’t be attending this time but will remember my own fine day there so many years ago.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Pont du Hoc

https://www.madhedgefundtrader.com/wp-content/uploads/2022/05/pont-du-hoc.png584882Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-05-23 10:02:242022-05-23 16:37:27The Market Outlook for the Week Ahead, or All Quiet on the Western Front

Our Bond Shorts are at Risk, thanks to a US Budget Deficit in Free Fall. I shall mourn this development as the loss of a close relative, particularly a rich uncle who writes me a check once a month, as selling short bonds and betting that interest rates will rise has been a huge moneymaker for me for years.

Since November, we have captured an eye-popping $42 points of downside in the United States Treasury Bond Fund (TLT). In two years, we have seized a mind-blowing $67 points. Don’t thank me, I’m just doing what you paid me to do.

While Trump was president, the national debt exploded by $4 trillion, a dream come true for bond short sellers. Trump spent a lifetime sticking lenders with hefty bills and the US government is no exception.

But all good things must come to an end. Since Biden became president, the annual budget deficit has vaporized, from $3.1 trillion in Trump's final year to a mere $360 billion for the first seven months of fiscal 2022, and we could approach zero by yearend.

An exploding economy and record employment have sent tax revenues soaring. The unemployment rate has shrunk from 25% to 3.6%. And taxpayers still had to pay a gigantic bill for last year’s monster capital gains in the stock market.

Covid spending, in the hundreds of billions last year, has been whittled down to near nothing. Biden has also been unable to get many spending bills through the Senate, where he lacks a clear majority.

Pare down government spending in a major way and you get new support for the bond market, the first since Clinton balanced the budget in 1999. Some investors are wondering if the 3.12% peak for the ten-year US Treasury bond seen last week could even be the top for this cycle. With the futures market already pricing in a 200 basis points in rate hikes this year, it’s entirely plausible.

I think we may have a shot at a 3.50% yield by next year. That equates to a (TLT) of around $100. But let’s face it, we are approaching the tag ends of this trade. Time to find better fish to fry. NVIDIA (NVDA) at $120 or Apple (AAPL) at $135 anyone?

We are seeing the same scenario play out at the state level. California saw a staggering $75 billion surplus last year. Among the luxuries Sacramento is considering are gas tax rebates for California drivers, undergrounding 20,000 miles of powerlines to prevent wildfires, and construction of a second transbay BART line.

Of course, all of this surplus wealth is temporary, as it always is. But “Laissez le bon temps roller.”

https://www.madhedgefundtrader.com/wp-content/uploads/2022/01/john-thomas-pilot-e1661438842642.png354450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-05-17 11:02:372022-05-17 12:21:11Our Bond Shorts Are At Risk

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SIFTING THROUGH THE WRECKAGE),

(SPY), (TLT), (TBT), (GOOGL), (AAPL), (MSFT), (BRKB), (NVDA), (JPM), (BAC), (WFC), ($BTCUSD)LA),

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-05-16 10:04:552022-05-16 16:08:34May 16, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.