Global Market Comments

July 29, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GREAT ROTATION LIVES), or (FLYING THE 1929 TRAVELAIRE D4D),

(NVDA), (TSLA), (JPM), (CCI), (CAT),

(DHI), (SLV), (GLD), (BRK/B), (DE)

Global Market Comments

July 29, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GREAT ROTATION LIVES), or (FLYING THE 1929 TRAVELAIRE D4D),

(NVDA), (TSLA), (JPM), (CCI), (CAT),

(DHI), (SLV), (GLD), (BRK/B), (DE)

I am writing this from the famed Hornli Hut on the north ridge of the Matterhorn at 10,700 feet. I’m not here to climb the iconic mountain one more time. Seven summits are enough for me. What left do I have to prove? It is a brilliant, clear day and I can see Zermatt splayed out before me a mile below.

No, I am here to inhale the youth, energy, excitement, and enthusiasm of this year’s batch of climbers, and to see them off at 1:00 AM after a hardy breakfast of muesli and strong coffee. My advice for beginners is liberally handed out for free.

Each country in Europe has its own personality. Observing the great variety of Europeans setting off I am reminded of an old joke. What is the difference between Heaven and hell?

In Heaven, you have a French chef, an Italian designer, a British policeman, a German engineer, and a Swedish girlfriend, and it is all organized by the Swiss.

In hell you have an English chef, a Polish designer, a German policeman, a Spanish engineer, no girlfriend, and it is all organized by the Italians.

When I recite this joke to my new comrades, I get a lot of laughs and knowing nods. Then they give me better versions of Heaven and hell

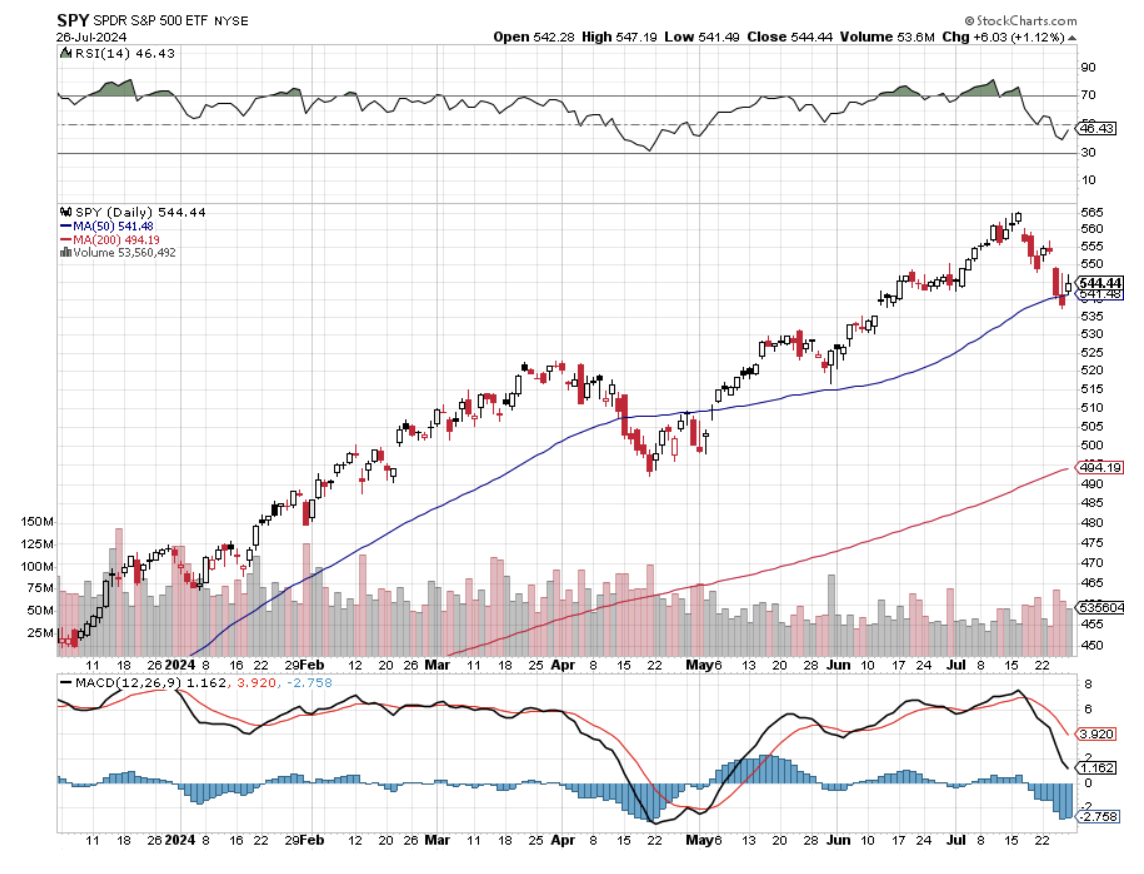

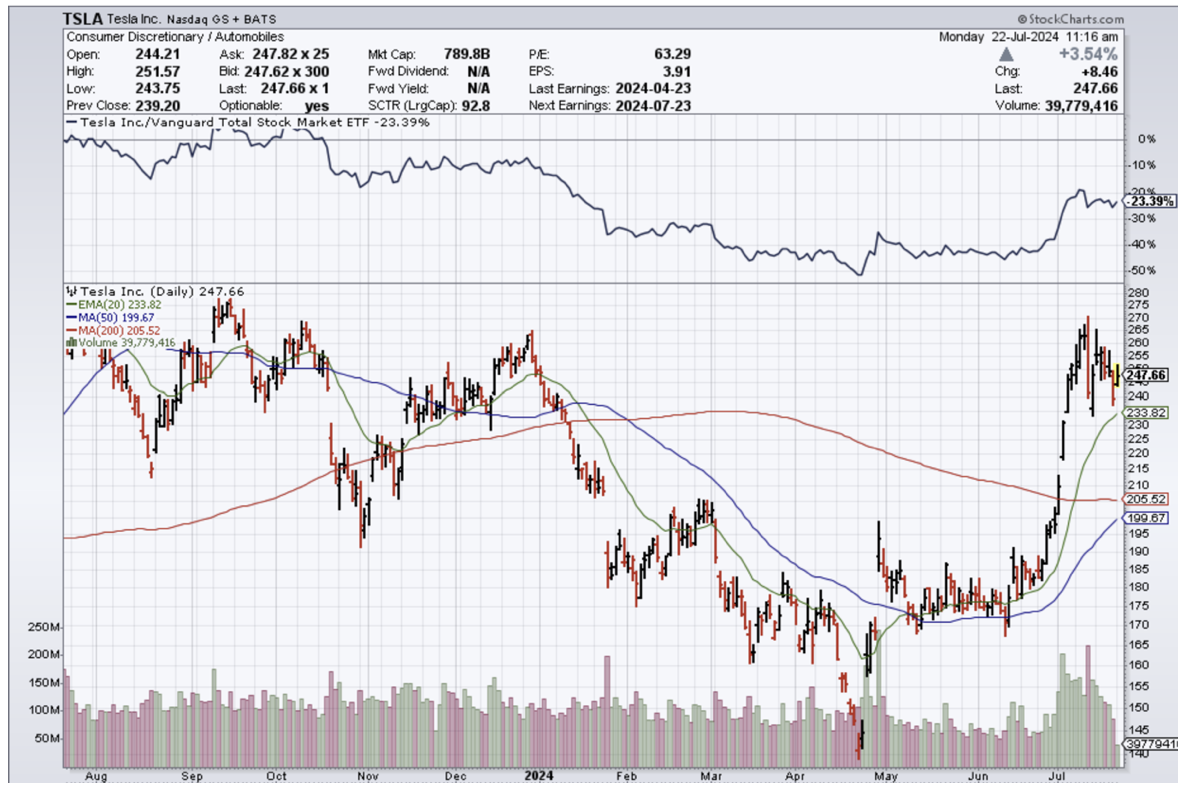

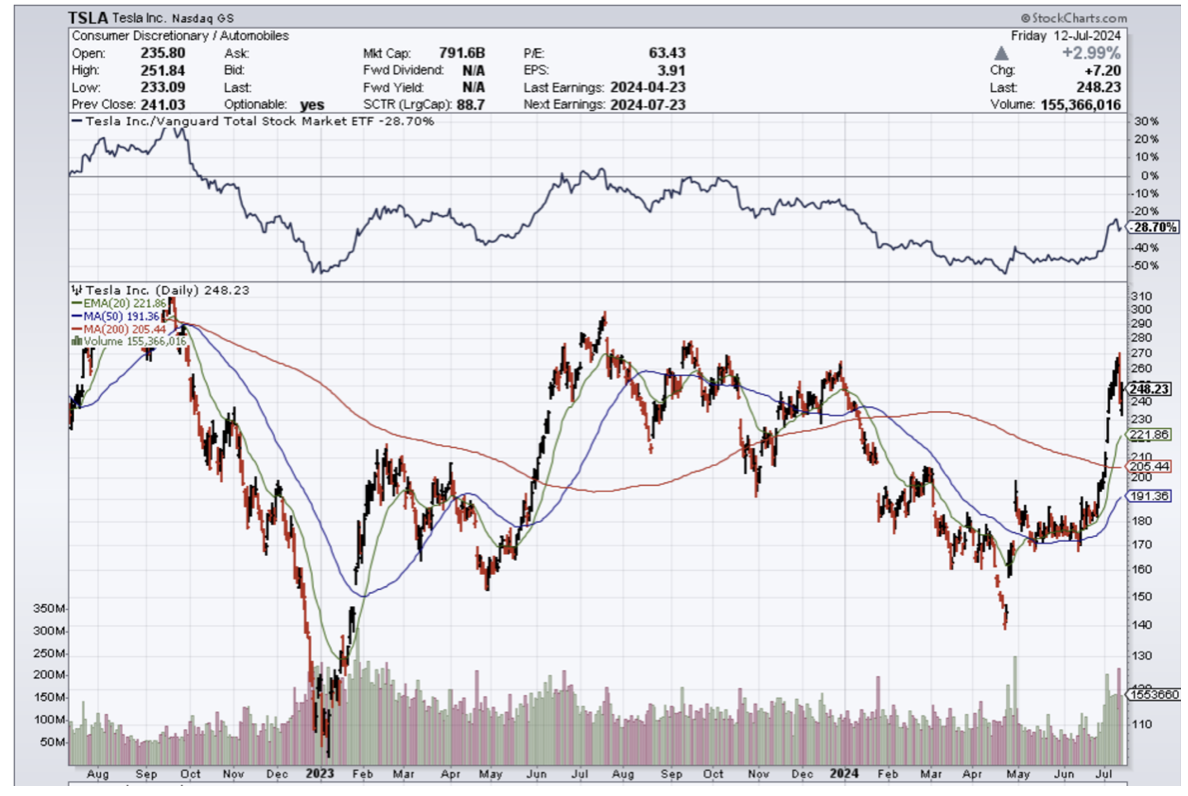

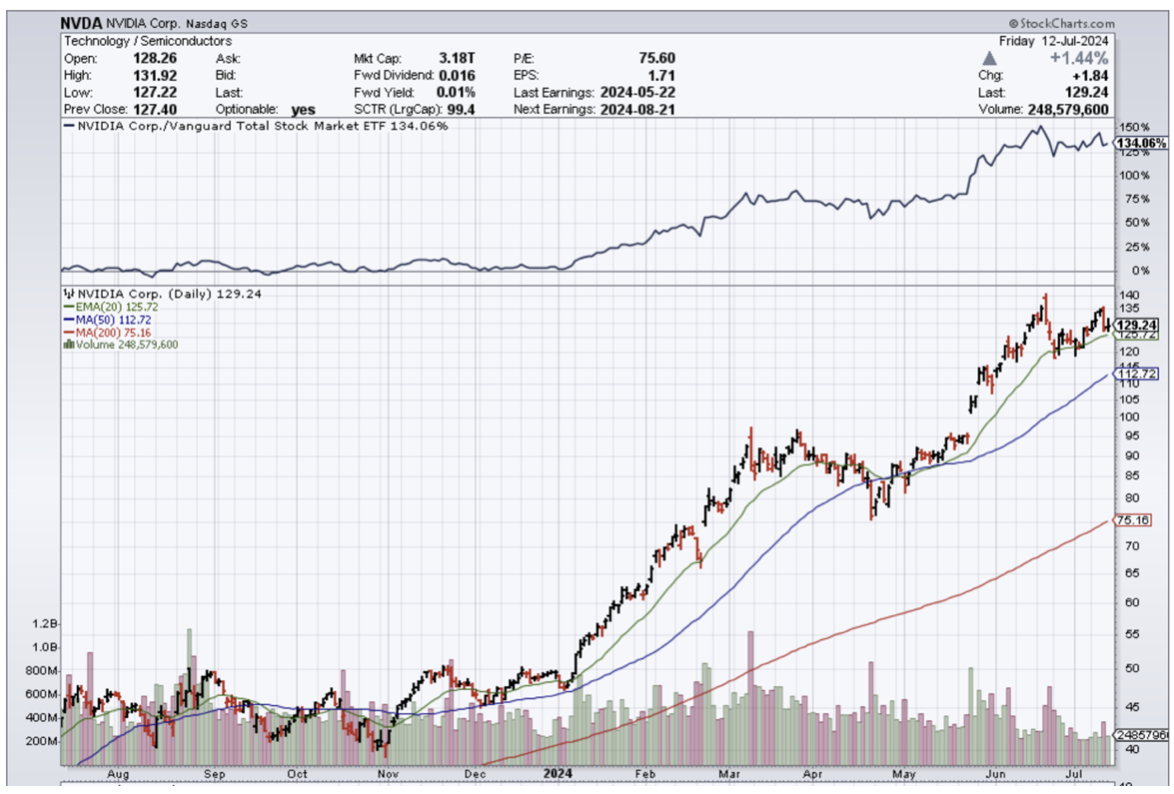

The stock market as well might have been organized by the Italians last week with the doubling of volatility and extreme moves up and down. Some 500 Dow points suddenly became a round lot, up and down. Tesla down $40? NVIDIA off 25%? Instantly, last month’s heroes became this month’s goats. It was a long time coming.

The Great Rotation, ignited by the July 11 Consumer Price Index shrinkage lives on. We are only two weeks into a reallocation of capital that could go on for months. Tech has nine months of torrid outperformance to take a break from. Interest sensitives have years of underperformance to catch up on.

Using a fund manager’s parlance, markets are simply moving from Tech to interest sensitives, growth to value, expensive to cheap, and from overbought to ignored.

A great “tell” of future share price performance is how they deliver in down markets. Last week, the Magnificent Seven (TSLA), (NVDA), got pummeled on the bad days. Interest sensitives like my (CCI), (IBKR), industrials (DE), (CAT), (BRK/B), precious metals (GLD), (SLV), and Housing (DHI) barely moved or rose.

Sector timing is everything in the stock market and those who followed me into these positions were richly rewarded. My performance hit a new all-time high every day last week.

Only the industrial metals have not been reading from the same sheet of music. Copper, (FCX), (COPX), Iron Ore (BHP), Platinum (PPLT), Silver (SLV), uranium (CCJ), and Palladium (PALL) have all suffered poor months.

You can blame China, which has yet to restart its sagging economy. I blame that on 40 years of the Middle Kingdom’s one-child policy, which is only now yielding its bitter fruit. That means 40 years of missing Chinese consumers, which started hitting the economy five years ago.

And who knows how many people they lost during the pandemic (the Chinese vaccine, Sinovac, was found to be only 30% effective). This is not a short-term fix. You can’t suddenly change the number of people born 40 years ago.

I warned Beijing 50 years ago that the one-child policy would end in disaster. You can’t beat the math. The leadership back then only saw the alternative, a Chinese population today of 1.8 billion instead of the 1.4 billion we have. But they ignored my advice.

It is the story of my life.

Eventually, US and European growth will make up for the lost Chinese demand, but that may take a while. Avoid all Chinese plays like a bad dish of egg foo young. They’re never going back to the 13% growth of the 2000’s.

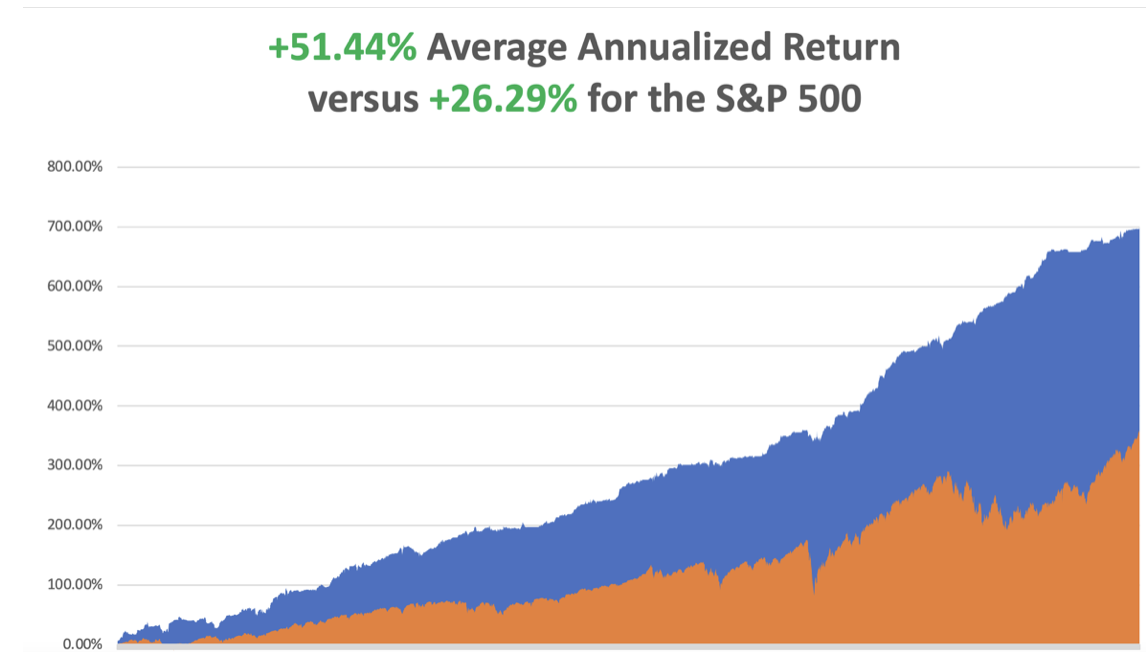

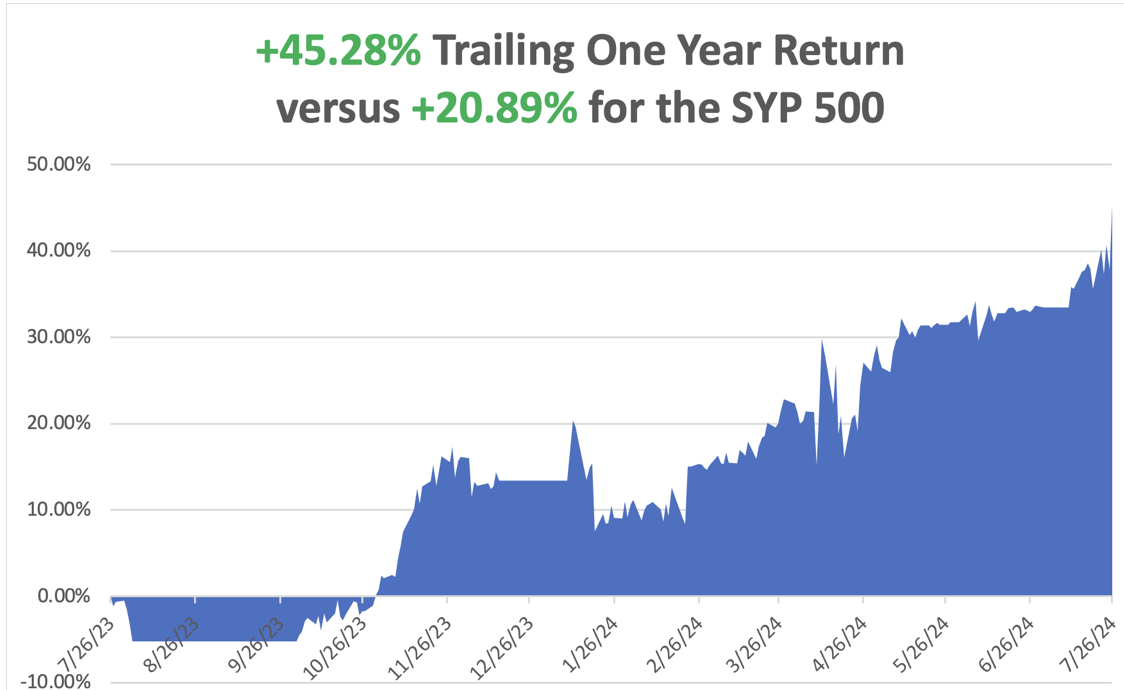

So far in July, we are up a stratospheric +11.82%. My 2024 year-to-date performance is at +31.84%. The S&P 500 (SPY) is up +14.05% so far in 2024. My trailing one-year return reached +xx.

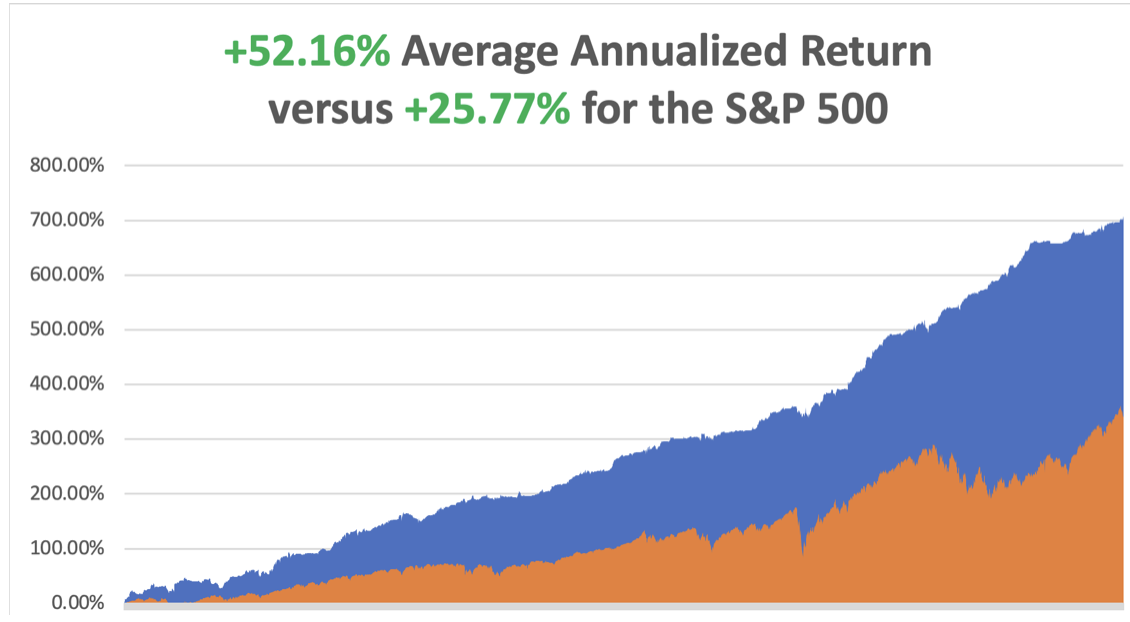

That brings my 16-year total return to +xx. My average annualized return has recovered to +708.47.

I used the market collapse to take a profit in my shorts in (NVDA) and (TSLA). Then on the first rally in these names, I slapped new shorts right back on. I used monster rallies to take profits in (JPM) and (CCI). I added new longs in interest sensitives like (CAT), (DHI), and (SLV). This is in addition to existing longs in (GLD), (BRK/B), and (DE), which I will likely run into the August 16 option expiration.

That will take my year-to-date performance up to an eye-popping 43.77% by mid-August.

Some 63 of my 70 round trips were profitable in 2023. Some 45 of 53 trades have been profitable so far in 2024, and several of those losses were break-even. That is a success rate of 84.91%.

Try beating that anywhere.

One of the great joys of hiking around Zermatt is that you meet happy people from all over the world. The other morning, I was walking up to Mount Gornergrat when I ran into two elementary school teachers from Nagoya, Japan. After recovering from the shock that I spoke Japanese I told them a story about when I first arrived in Japan in 1974.

Toyota Motors (TM) hired me to teach English to a group of future American branch sales managers. A Toyota Century limo picked me up at the Nagoya train station and drove me up to a training facility in the mountains. As we approached the building, I witnessed 20 or so men in dark suits, white shirts, and thin ties lined up. One by one they took a baseball bat and savagely beat a dummy that lay prostrate on the grass before them.

I asked the driver what the heck they were doing. He answered that they were beating the competition. A decade later, Japan had seized 44% of the US car market, with Toyota taking the largest share.

I like to think that a superior product did that and not my language instruction abilities.

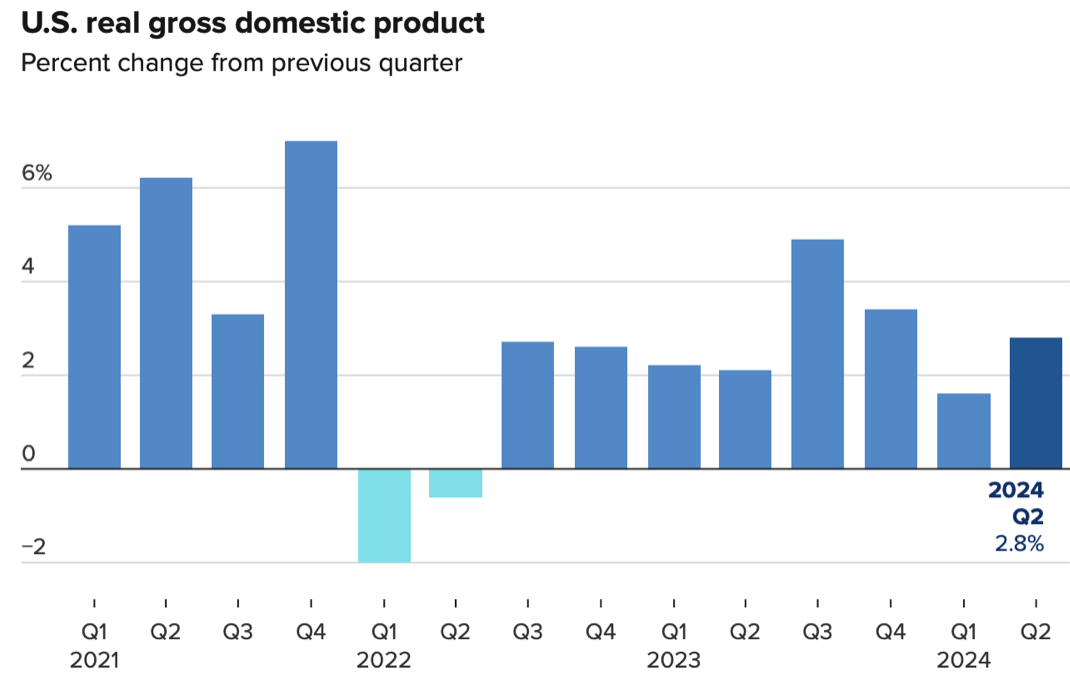

US Q2 GDP Pops, up 2.8% versus 2.1% expected. The US still has the strongest major economy in the world. Consumer spending helped propel the growth number higher, as did contributions from private inventory investment and nonresidential fixed investment. Goldilocks Lives!

Personal Consumption Expenditure Drops, a key inflation indication for the Fed, up only 0.1%in June and 2.5% YOY. Core inflation, which excludes food and energy, showed a monthly increase of 0.2% and 2.6% on the year, both also in line with expectations. Personal income rose just 0.2%, below the 0.4% estimate. Spending increased 0.3%, meeting the forecast, while the personal savings rate decreased to 3.4%.

Leveraged NVIDIA Bets Cause Market Turmoil. Great when (NVDA) is rocketing, not so much when it is crashing, with (NVDA) plunging 25.7% in a month. (NVDA) is now the largest holding in 500 traded ETF’s. I already made a nice chunk of money on an (NVDA) and will go back for another bight on the smallest rally.

The US Treasury Knocks Out a Blockbuster Auction, shifting $180 Billion worth of 7 ear paper, taking yields down 5 basis points. Foreign demand was huge. Bonds are trading like interest rates are going to be cut. Stock rallied an impressive 800 points the next day.

Durable Goods Get Slammed, down 6.6% versus an expected +0.6% in June. More juice for the interest rate cut camp.

Tesla Bombs, with big earnings and sales disappointments, taking the stock down 15%. Thank goodness we were short going into this. The EV maker put off its Mexico factory until after the November election. Adjusted earnings fell to 52 cents per share in the three months ended in June, missing estimates for the fourth consecutive quarter. Tesla will now unveil robotaxis on Oct. 10, and the cars shown will only be prototypes. Cover your Tesla Shorts near max profit.

Home Sales Dive, in June, off 5.4%. Inventory jumped 23.4% from a year ago to 1.32 million units at the end of June, coming off record lows but still just a 4.1-month supply. The median price of an existing home sold in June was $426,900, an increase of 4.1% year over year.

Oil Glut to continue into 2025, thanks to massive tax subsidies creating overproduction. Morgan Stanley said it expects OPEC and non-OPEC supply to grow by about 2.5 million barrels per day next year, well ahead of demand growth. Refinery runs are set to reach a peak in August this year, and unlikely to return to that level until July 2025, it said. Avoid all energy plays until they bottom.

Homebuilders Catch on Fire, with the prospect of falling interest rates. The US has a structural shortage of 10 million homes with 5 million Millennial buyers. Homebuilders have been underbuilding since the 2008 Great Financial Crisis, seeking to emphasize profits and share buybacks over to development land purchases. Buy (DHI), (LEN), (PMH), (KBH) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, July 29 at 9:30 AM EST, the Dallas Fed Manufacturing Index is out.

On Tuesday, July 30 at 9:30 AM, the JOLTS Job Openings Report is published. The Federal Reserve Open Market Committee (FOMC) meeting begins

On Wednesday, July 31 at 2:00 PM, Jay Powell announced the Fed’s interest rate decision.

On Thursday, August 1 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, August 2 at 8:30 AM, the July Nonfarm Payroll Report is released. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I am reminded as to why you never want to fly with Major John Thomas

When you make millions of dollars for your clients, you get a lot of pretty interesting invitations. $5,000 cases of wine, lunches on superyachts, free tickets to the Olympics, and dates with movie stars (Hi, Cybil!).

So it was in that spirit that I made my way down to the beachside community of Oxnard, California just north of famed Malibu to meet long-term Mad Hedge follower, Richard Zeiler.

Richard is a man after my own heart, plowing his investment profits into vintage aircraft, specifically a 1929 Travel Air D-4-D.

At the height of the Roaring Twenties (which by the way we are now repeating), flappers danced the night away doing the Charleston and the bathtub gin flowed like water. Anything was possible, and the stock market soared.

In 1925, Clyde Cessna, Lloyd Strearman, and Walter Beech got together and founded the Travel Air Manufacturing Company in Wichita, Kansas. Their first order was to build ten biplanes to carry the US mail for $125,000.

The plane proved hugely successful, and Travel Air eventually manufactured 1,800 planes, making it the first large-scale general aviation plane built in the US. Then, in 1929, the stock market crashed, the Great Depression ensued, aircraft orders collapsed, and Travel Air disappeared in the waves of mergers and bankruptcies that followed.

A decade later, WWII broke out and Wichita produced the tens of thousands of the small planes used to train the pilots who won the war. They flew B-17 and B-25 bombers and P51 Mustangs, all of which I’ve flown myself. The name Travel Air was consigned to the history books.

Enter my friend Richard Zeiler. Richard started flying support missions during the Vietnam War and retired 20 years later as an Army Lieutenant Colonel. A successful investor, he was able to pursue his first love, restoring vintage aircraft.

Starting with a broken down 1929 Travel Air D4D wreck, he spent years begging, borrowing, and trading parts he found on the Internet and at air shows. Eventually, he bought 20 Travel Air airframes just to make one whole airplane, including the one used in the 1930 Academy Award-winning WWI movie “Hells Angels.”

By 2018, he returned it to pristine flying condition. The modernized plane has a 300 hp engine, carries 62 gallons of fuel, and can fly 550 miles in five hours, which is far longer than my own bladder range.

Richard then spent years attending air shows, producing movies, and even scattering the ashes of loved ones over the Pacific Ocean. He also made the 50-hour round trip to the annual air show in Oshkosh, Wisconsin. I have volunteered to copilot on a future trip.

Richard now claims over 5,000 hours flying tailwheel aircraft, probably more than anyone else in the world. Believe it or not, I am also one of the few living tailwheel-qualified pilots in the country left. Yes, antiques are flying antiques!

As for me, my flying career also goes back to the Vietnam era as well. As a war correspondent in Laos and Cambodia, I used to hold Swiss-made Pilatus Porter airplanes straight and level while my Air America pilot friend was looking for drop zones on the map, dodging bullets all the way.

I later obtained a proper British commercial pilot license over the bucolic English countryside, trained by a retired Battle of Britain Spitfire pilot. His favorite trick was to turn off the fuel and tell me that a German Messerschmidt had just shot out my engine and that I had to land immediately. He only turned the gas back on at 200 feet when my approach looked good. We did this more than 200 times.

By the time I moved back to the States and converted to a US commercial license, the FAA examiner was amazed at how well I could do emergency landings. Later, I added additional licenses for instrument flying, night flying, and aerobatics.

Thanks to the largesse of Morgan Stanley during the 1980’s, I had my own private twin-engine Cessna 421 in Europe for ten years at their expense where I clocked another 2,000 hours of flying time. That job had me landing on private golf courses so I could sell stocks to the Arab Prince owners. By 1990, I knew every landing strip in Europe and the Persian Gulf like the back of my hand.

So, when the first Gulf War broke out the following year, the US Marine Corps came calling at my London home. They asked if I wanted to serve my country and I answered, “Hell, yes!” So, they drafted me as a combat pilot to fly support missions in Saudi Arabia.

I only got shot down once and escaped with a crushed L5 disk. It turns out that I crash better than anyone else I know. That’s important because they don’t let you practice crashing in flight school. It’s too expensive.

My last few flying years have been more sedentary, flying as a volunteer spotter pilot in a Cessna-172 for Cal Fire during the state’s runaway wildfires. As long as you stay upwind there’s no smoke. The problem is that these days, there is almost nowhere in California that isn’t smokey. By the way, there are 2,000 other pilots on the volunteer list.

Eventually, I flew over 50 prewar and vintage aircraft, everything from a 1932 De Havilland Tiger Moth to a Russian MiG 29 fighter.

It was a clear, balmy day when I was escorted to the Travel Air’s hanger at Oxnard Airport. I carefully prechecked the aircraft and rotated the prop to circulate oil through the engine before firing it up. That reduced the wear and tear on the moving parts.

As they teach you in flight school, it is better to be on the ground wishing you could fly than being in the air wishing you were on the ground!

I donned my leather flying helmet, plugged in my headphones, received a clearance from the tower, and was good to go. I put on max power and was airborne in less than 100 yards. How do you tell if a pilot is happy? He has engine oil all over his teeth. After all, these are open-cockpit planes.

I made for the Malibu coast and thought it would be fun to buzz the local surfers at wave top level. I got a lot of cheers in return from my fellow thrill seekers.

After a half hour of low flying over elegant sailboats and looking for whales, I flew over the cornfields and flower farms of remote Ventura County and returned to Oxnard. I haven’t flown in a biplane in a while and that second wing really put up some drag. So, I had to give a burst of power on short finals to make the numbers. A taxi back to the hangar and my work there was done.

There are old pilots and there are bold pilots, but there are no old, bold pilots. I can attest to that.

Richard’s goal is to establish a new Southern California aviation museum at Oxnard airport. He created a non-profit 501 (3)(c), the Travel Air Aircraft Company, Inc. to achieve that goal, which has a very responsible and well-known board of directors. He has already assembled three other 1929 and 1930 Travel Air biplanes as part of the display.

The museum’s goal is to provide education, job training, restoration, maintenance, sightseeing rides, film production, and special events. All donations are tax-deductible. To make a donation please email the president of the museum, my friend Richard Conrad at

rconrad6110@gmail.com

Who knows, you might even get a ride in a nearly 100-year-old aircraft as part of a donation.

To watch the video of my joyride please click here.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Where I Go My Kids Go

Global Market Comments

July 25, 2024

Fiat Lux

Featured Trade:

(AUGUST 5 VILNIUS LITHUANIA STRATEGY LUNCHEON)

(A NOTE ON OPTIONS ASSIGNED OR CALLED AWAY)

(TLT), (TSLA)

Global Market Comments

July 24, 2024

Fiat Lux

Featured Trade:

(WHAT AI CAN AND CAN’T DO FOR YOU)

(AAPL), (GOOGL), (AMZN), (AMZN), (TSLA), (NVDA), (MU)

Mad Hedge Technology Letter

July 22, 2024

Fiat Lux

Featured Trade:

(THE EV CONUNDRUM)

(TSLA), (RIVN), (TOYOTA)

Sometimes tech trends start and stop and then start again.

It certainly feels that way for the EV industry when the Chairman of Toyota Akio Toyoda threw a damp towel on the progress of EVs taking over the world.

The Japanese Chairman told the world that he thought EVs would never account for more than a third of the market and that consumers should not be forced to buy them.

These ideas definitely go against the grain of the liberal democratic order.

Listen to the bureaucrats in Brussels and the left-wing establishment in Washington and it almost seems as if they want to ban oil and gas products.

Of course, the ban is certainly hyperbole, but the green movement towards lithium battery-powered cars has become quite political and partisan.

Akio Toyoda, chairman of the world’s biggest carmaker by sales, said that electric vehicles (EVs) should not be developed to the exclusion of other technologies such as the hybrid and hydrogen-powered cars that his company has focused on.

He said he believed battery EVs will only secure a maximum of 30% of the market – less than double their current share in the UK – with the remaining 70% taken by fuel cell EVs, hybrids, and hydrogen cars.

Mr. Toyoda argued that electric cars’ appeal is limited because one billion people in the world still live without electricity, while they are also expensive and need charging infrastructure to operate.

The chairman also pointed to Toyota’s recent announcement that it was working on a new combustion engine, saying it was important to give engine factory workers a role in the green transition.

Koji Sato, the car maker’s chief executive, last year promised Toyota would sell 1.5 million battery EVs a year by 2026, and 3.5 million by 2030.

Tesla, the world’s biggest EV producer on an annual basis, reported 1.8 million deliveries last year.

Mr. Toyoda’s two cents come after electric car sales have slowed in the Western world slowed in 2024.

I am of the notion that in the short term, all the low-hanging fruit has been plucked by the EV buyers.

To find the next incremental buyer, it won’t be impossible, but that same type of excitement won’t exist.

The truth is that many consumers are still tied to the combustible engine.

On a recent trip to Japan, almost no local drove an EV and I witnessed almost no charging points.

If one of the biggest economies in the world isn’t convinced, then there is still a lot of work to do and I don’t believe that the Japanese will give up gas-powered engines so quickly.

In the short term, the demand weakness in EVs bodes ill for EV stocks like Tesla or Rivian.

Throw in the fact that EVs aren’t cheap and the cost of living crisis is forcing consumers to migrate to necessities which unfortunately doesn’t include a brand new Tesla.

Stay away from EV stocks in the short term and pile into the AI narrative.

Mad Hedge Technology Letter

July 15, 2024

Fiat Lux

Featured Trade:

(AI AND IMPROVED WORKFORCE EFFICIENCY IS HERE TO STAY)

(TSLA)

Students hoping to become bankers shouldn’t study finance, they should dive into AI programming.

This is the big takeaway from how investment banks are run these days.

Gone are the moments when finance degrees were the hottest commodity, now it is all about generative AI.

Artificial intelligence (AI) could replace the equivalent of 300 million full-time jobs, a report by investment bank Goldman Sachs says.

It could replace a quarter of work tasks in the US and Europe but may also mean new jobs and a productivity boom.

And it could eventually increase the total annual value of goods and services produced globally by 7%.

Generative AI, able to create content indistinguishable from human work, is "a major advancement", the report says.

Silicon Valley is keen to promote investment in AI not only in the United States but in a way that will ultimately drive productivity gains across the global economy.

The report notes AI's impact will vary across different sectors - 46% of tasks in administrative and 44% in legal professions could be automated but only 6% in construction and 4% in maintenance, it says.

Journalists will therefore face more competition, which would drive down wages unless we see a very significant increase in the demand for such work.

Consider the introduction of GPS technology and platforms like Uber (UBER). Suddenly, knowing all the streets in London had much less value - and so incumbent drivers experienced large wage cuts in response, of around 10% according to our research.

The result was lower wages, not fewer drivers.

Over the next few years, generative AI is likely to have similar effects on a broader set of creative tasks.

According to research cited by the report, 60% of workers are in occupations that did not exist in 1940.

However, other research suggests technological change since the 1980s has displaced workers faster than it has created jobs.

Nobody understands how the technology will evolve or how firms will integrate it into how they work.

Lower wages and higher output are a perfect recipe for higher technology share prices and that is exactly what we will get.

Currently, we are experiencing a mild pullback from the AI mania, but that is simply because it got too far ahead of its skis.

I am quite impressed by the price action in a stock like Tesla (TSLA) which executed a major cut to their global workforce to trim costs.

The staff cut of 10% could result in exactly what I mentioned in more output for less pay, but in terms of hiring more workers, they have decided to force less workers to do more.

This type of management decision increases efficiency because it forces workers to work smarter.

It’s certain they will be a major investor in AI chips to outfit their EV cars, and much of this corporate tech business is a feedback loops involving synergies with businesses overlapping.

Tech as a whole is not in trouble, but individual companies will find an imbalanced treatment of their stock.

The AI pixie dust is still strong as many readers bought the shallow dip in Nvidia.

I do believe in the AI hype, and a lot of the price action is skewed toward just a handful of AI stocks.

My advice is to buy AI stocks on the dip and this increased efficiency will certainly filter down into the top and bottom lines.

Global Market Comments

July 15, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SEA CHANGE), (BB RATED BANKS LOANS), and (RESCUING THE USS POTOMAC),

(TLT), (JNK), (SLRN), (BRLN), (BKLN), (FFRHX), (WES), (CCI), (GLD), (DE), (BRK/B), (TSLA), (NVDA).

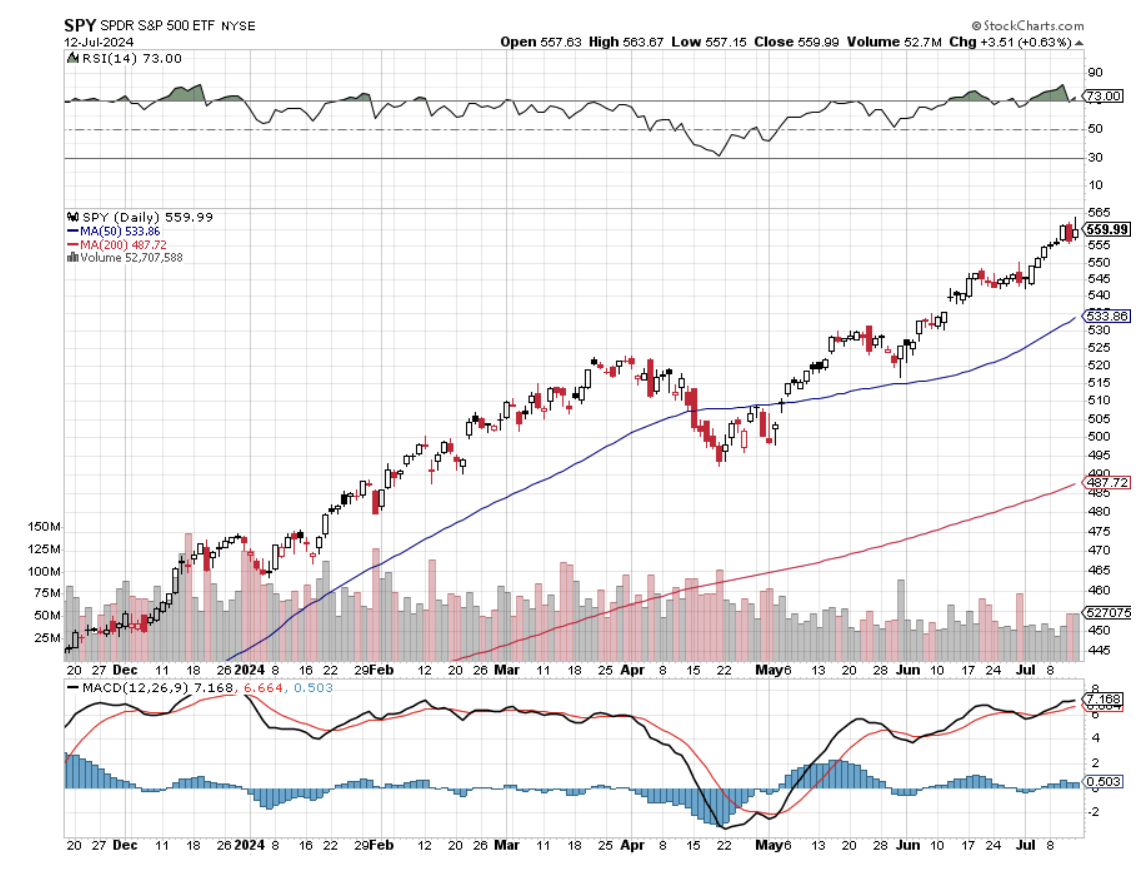

I believe there was a major sea change in the markets last week, which has taken the economy from inflation to deflation. All asset classes performed as they should, with some extreme moves. It is now time to focus on the 493 of the S&P 500 and let the Magnificent Seven take a long-needed rest.

Not only does this pave the way for a Fed interest rate cut in September, but several more to follow. This opens the floodgates for the (TLT) to rise above $100 by yearend, and maybe even to $110. Remember the old high for bonds is $166. Higher beta fixed-income plays will rise much more.

Stocks will keep rising but with different leadership from dozens of interest-sensitive sectors, including real estate, their suppliers, industrials, precious metals, financials, energy, and outright value plays long left in the doghouse. If you can’t grasp these new trends, your portfolio will be out to sea shortly. An S&P 500 of 6,000 looks like a pretty safe bet by yearend.

That brings to the fore investment in fixed-income securities. There are two ways to make money on a fixed income. Coupon interest rates are still at historically high levels. And as rates fall, fixed-income prices rise, opening the door to capital gains, which could reach 10%-20% in the coming year.

The fixed-income market at $100 trillion is double the size of the stock market. And there are many more bond listings than stock ones. So the number of possible investments is almost endless. I shall give you a brief overview of some of the more interesting subsectors.

US Government bonds – are the gold standard with a guaranteed return. But you pay for the extra security with lower rates; the current ten-year US Treasury bond yield is 4.20%, much lower than the present 90-day T-bill of 5.21%. The easiest way to buy these is through the (TLT). The 30-year government bond should be avoided as the extra 0.14% in yield doesn’t adequately compensate you for the extra 20 years of risk

Junk Bonds – Also known as “high yield” bonds have always been misnamed. The default rates never remotely approached the levels that justified their high yields, not even during the financial crisis, as my old friend former junk bond king Michael Milliken has amply proven. The (JNK) is currently yielding 6.59% and has the potential for larger capital gains than government bonds.

Master Limited Partnerships – These are partnerships granted generous tax benefits with the goal of producing oil. They issue annual Form K-1’s to include with your tax return. Dividends are deferred until the MLP’s investment reaches the end of its useful life, which can be decades. MLPs used to be a huge industry with dozens of listed companies.

When the price of oil went to negative numbers during the pandemic, most of them got wiped out. Because of this rocky past, there are a handful of large, well-capitalized MLPs with extremely high yields. One is Western Midstream Partners (WES) with a 9.20% yield. Energy Transfer Partners (ET) pay a 7.96% yield.

These yields will remain safe as long as oil prices are stable or rising, as I expect in a long-term global economic recovery. Take oil back to zero again in another pandemic and these returns will get turned on their head.

With the normalizing of interest rates, it's time to normalize investment strategies as well. That means bringing back the old 60/40 strategy where one half of the portfolio ensures the other, with a modern twist. You can put 60% of your assets in stocks, with half on technology and half on domestic cyclicals.

The other 40% should be allocated to some mix of the above fixed-income investments guaranteeing annual high returns. It is not a bad strategy for mature investors, especially if they would rather be on a golf course instead of spending all day in front of a screen picking bottoms and tops for stocks, like Millennials.

Here’s where to get a Safe 8.48% Yield, BB-rated bank loans, which will soar in value with even just one quarter-point rate cut. BB bank loans are very low risk, and they have a spread that’s about 290 basis points above the overnight Fed rate. How does one buy such an animal? The actual bank loans themselves are made by lending institutions to companies. These loans aren’t made accessible to individual investors who want to make a play for yield. Rather, large institutional investors snap them up and add them to their fixed-income portfolios. The top ticker symbols are (SLRN), (BRLN), (BKLN), and (FFRHX). Check them out.

So far in July, we are up +2.17%. My 2024 year-to-date performance is at +22.19%. The S&P 500 (SPY) is up +17.40% so far in 2024. My trailing one-year return reached +37.07.

That brings my 16-year total return to +698.82%. My average annualized return has recovered to +51.44%.

I used the blockbuster CPI Report last week to jump off my 100% cash position and piled on six new positions. Those included interest rate-sensitive longs in (CCI), (GLD), (DE), (BRK/B), and shorts in big tech leaders (TSLA) and (NVDA).

Some 63 of my 70 round trips were profitable in 2023. Some 35 of 44 trades have been profitable so far in 2024, and several of those losses were really break-even.

Nonfarm Payroll Report Comes in Weak for June at 206,000. The Headline Unemployment rate rose to a three-year high at 4.1%. All interest rate plays rocketed as a September interest rate comes back on the table. If the Fed doesn’t cut soon, we are going into recession. Buy (TLT) on dips.

Fed Governor Jay Powell Warns of Recession Risks if interest rate cuts don’t take place soon, spiking all markets. Powell is showing his cards for the next few Fed Meetings. Buy all interest rates plays like (TLT), (JNK), (NLY), and (CCI).

CPI comes in Negative. The writing is not only on the wall right now, it’s blasting us with great neon lights. That was the message this morning from the Consumer Price Index, which this morning delivered a gob-smacking 0.1% DECLINE in June. We are now in deflation and the YOY inflation rate is now down to only 3.0%. As a result, a Fed interest rate cut of 25 basis points is now a certainty in September and more will follow. All falling interest rate plays in the stock market are in play. Rising rate plays could be the trade for the rest of 2024.

PPI Rises 0.2%, with Wholesale Prices coming in as expected. The producer price index is now up 2.6% year over year. The inflation pictures goes back to mixed. Stocks rallied with big tech recovering about half of yesterday’s losses.

Consumer Sentiment at a Three-Year Low at 66.0%, down from 68.5 as the economic slide continues, according to the University of Michigan. It’s another pre-recession indicator.

Bank Earnings Beat and the stocks are rising in expectation of falling interest rates, with (JPM), (BAC), and (C) reporting. Wells Fargo (WFC) Bombed again. Buy banks on dips which have been on a tear all day.

Tesla Delays Robotaxi Day, past its original August 8 target to probably October, tanking the shares by 11%. The date propelled the massive 50% rally in the hares over the past month. Musk is always overly aggressive on his targets. Sell calls against existing (TSLA) stock positions.

Apple Expects 10% Rise in iPhone Shipments in 2024, after a bumpy 2023, counting on AI features to fuel demand for the iPhone 16. Apple is now the newly discovered AI stock. Buy (AAPL) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, July 15 at 9:30 AM EST, Feder Governor Jay Powell speaks. He has lately been leaning dovish.

On Tuesday, July 16 at 9:30 AM, Retail Sales are published.

On Wednesday, July 17 at 9:30 AM, Building Permits are out.

On Thursday, July 18 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, July 19 at 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I usually get a request to fund some charity about once a day. I ignore them because they usually enrich the fundraisers more than the potential beneficiaries. But one request seemed to hit all my soft spots at once.

Would I be interested in financing the refit of the USS Potomac (AG-25), Franklin Delano Roosevelt’s presidential yacht?

I had just sold my oil and gas business for an outrageous profit and had some free time on my hands so I said, “Hell Yes,” but only if I get to drive. The trick was to raise the necessary $5 million without it costing me any money.

To say that the Potomac had fallen on hard times was an understatement.

When Roosevelt entered the White House in 1932, he inherited the presidential yacht of Herbert Hoover, the USS Sequoia. But the Sequoia was entirely made of wood, which Roosevelt had a lifelong fear of. When he was a young child, he nearly perished when a wooden ship caught fire and sank, he was passed to a lifeboat by a devoted nanny.

Roosevelt settled on the 165-foot USS Electra, launched from the Manitowoc Shipyard in Wisconsin, whose lines he greatly admired. The government had ordered 34 of these cutters to fight rum runners across the Great Lakes during Prohibition. Deliveries began just as the ban on alcohol ended.

Some $60,000 was poured into the ship to bring it up to presidential standards and it was made wheelchair accessible with an elevator, which FDR operated himself with ropes. The ship became the “floating White House,” and numerous political deals were hammered out on its decks. Some noted guests included King George VI of England, Queen Elizabeth, and Winston Churchill.

During WWII Roosevelt hosted his weekly “fireside chats” on the ship’s short-wave radio. The concern was that the Germans would attempt to block transmissions if the broadcast came from the White House.

After Roosevelt’s death, the Potomac was decommissioned and sold off by Harry Truman, who favored the much more substantial 243-foot USS Williamsburg. The Potomac became a Dept of Fisheries enforcement boat until 1960 and then was used as a ferry to Puerto Rico until 1962.

An attempt was made to sail it through the Panama Canal to the 1962 World’s Fair in Seattle, but it broke down on the way in Long Beach, CA. In 1964 Elvis Presley bought the Potomac so it could be auctioned off to raise money for St. Jude Children’s Research Hospital. It sold for $65,000. It then disappeared from maritime registration in 1970. At one point, there was an attempt to turn it into a floating disco.

In 1980, a US Coast Guard cutter spotted a suspicious radar return 20 miles off the coast of San Francisco. It turned out to be the Potomac loaded to the gunnels with bales of illicit marijuana from Mexico. The Coast Guard seized the ship and towed it to the Treasure Island naval base under the Bay Bridge. By now, the 50-year-old ship was leaking badly. The marijuana bales soaked up the seawater and the ship became so heavy it sank at its moorings.

Then a long rescue effort began. Not wanting to get blamed for the sinking of a presidential yacht on its watch, the Navy raised the Potomac at its own expense, about $10 million, putting its heavy lift crane to use. It was then sold to the City of Oakland, CA for a paltry $15,000.

The troubled ship was placed on a barge and floated upriver to Stockton, CA, which had a large but underutilized unionized maritime repair business. The government subsidies started raining down from the skies and a down to the rivets restoration began. Two rebuilt WWII tugboat engines replaced the old, exhausted ones. A nationwide search was launched to recover artifacts from FDR’s time on the ship. The Potomac returned to the seas in 1993.

I came on the scene in 2007 when the ship was due for a second refit. The foundation that now owned the ship needed $5 million. So, I did a deal with National Public Radio for free advertising in exchange for a few hundred dinner cruise tickets. NPR then held a contest to auction off tickets and kept the cash (what was the name of FDR’s dog? Fala!).

I also negotiated landing rights at the Pier One San Francisco Ferry Terminal, which involved negotiating with a half dozen unions, unheard of in San Francisco maritime circles. Every cruise sold out over two years, selling 2,500 tickets. To keep everyone well-lubricated, I became the largest Bay Area buyer of wine for those years. I still have a free T-shirt from every winery in Napa Valley.

It turned out to be the most successful fundraiser in the history of NPR and the Potomac. We easily got the $5 million and then some. The ship received a new coat of white paint, new rigging, modern navigation gear, and more period artifacts. I obtained my captain’s license and learned how to command a former Coast Guard cutter.

It was a win-win-win.

I was trained by a retired US Navy nuclear submarine commander, who was a real expert at navigating a now thin-hulled 73-year-old ship in San Francisco’s crowded bay waters. We were only licensed to cruise up to the Golden Gate Bridge and not beyond, as the ship was so old.

The inaugural cruise was the social event of the year in San Francisco with everyone wearing period Depression-era dress. It was attended by FDR’s grandson, James Roosevelt III, a Bay area attorney who was a dead ringer for his grandfather. I mercilessly grilled him for unpublished historical anecdotes. A handful of still-living Roosevelt cabinet members also came, as well as many WWII veterans.

As we approached the Golden Gate Bridge, some poor soul jumped off and the Coast Guard asked us to perform search and rescue until they could get a ship on station. Nobody was ever found. It certainly made for an eventful first cruise.

Of the original 34 cutters constructed, only four remain. The other three make up the Circle Line tour boats that sail around Manhattan several times a day.

Last summer, I boarded the Potomac for the first time in 14 years for a pleasant afternoon cruise with some guests from Australia. Some of the older crew recognized me and saluted. In the cabin, I noticed a brass urn oddly out of place. It contained the ashes of the sub-commander who had trained me all those years ago.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Captain Thomas at the Helm