Global Market Comments

March 2, 2022

Fiat Lux

Featured Trade:

(TESTIMONIAL)

(HOW TO BUY A SOLAR SYSTEM),

(SPWR), (TSLA)

Global Market Comments

March 2, 2022

Fiat Lux

Featured Trade:

(TESTIMONIAL)

(HOW TO BUY A SOLAR SYSTEM),

(SPWR), (TSLA)

Global Market Comments

February 28, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or FAREWELL THE PEACE DIVIDEND),

(SPY), (TLT), (TBT), (TSLA), (AAPL)

Remember that great bull market of the Dotcom Boom? Most investors believe it was the result of combining a new Internet, cheap PCs, and the Mosaic Application which made it all work together.

But to Wall Street types usually blind to geopolitics, there was another important factor: The peace dividend paid out by the end of the Cold War. The end result was 30 years of less defense spending, lower taxes, and higher profits for corporate America.

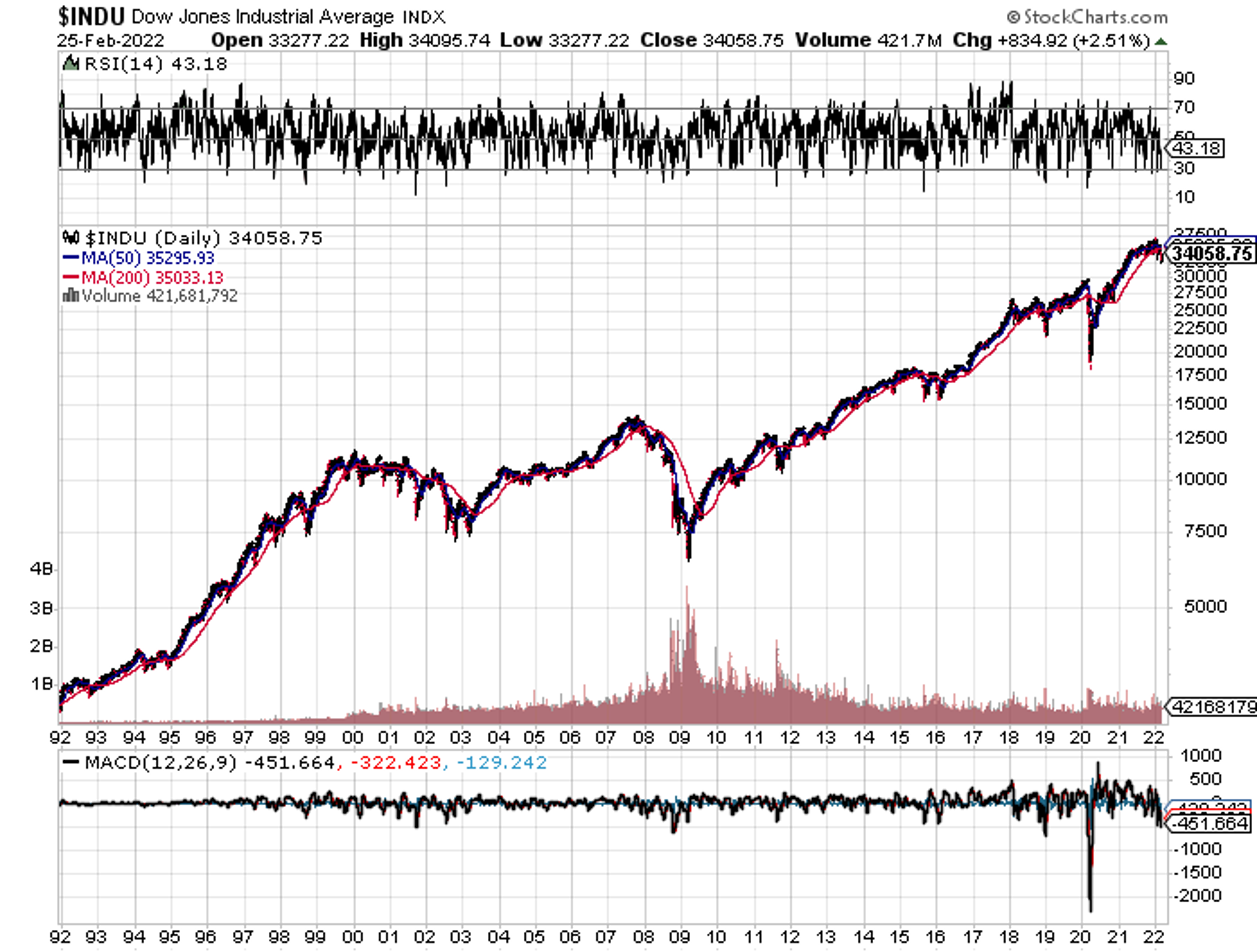

The numbers are pretty compelling. Since the Soviet Union collapsed in 1991, the Dow Average has risen from $2,875 to $34,000, a gain of 12 times. That averages out to an incredible 40% a year. Individual stocks like Monster Beverage (MNST), Tractor Supply (TSCO), and Altria (MO) appreciated a thousandfold or more.

So what happens if the Cold War resumes? Do we have to pay the money back?

In part, yes.

Not that you have to have to write a check anytime soon. But you will have to pay in the form of higher taxes for more defense spending, slower economic growth, fewer corporate profits, and a more modestly appreciating stock market. And that great multiplier of growth, globalization, just suffered a dagger through its heart.

While we have just seen one of the greatest short-covering rallies of all time, $1,800 points or 5.6% in two days, don’t think you’re back on Easy Street yet. A worst-case scenario full-scale Russian invasion of the Ukraine is in the price. So, it's back to focusing on runaway inflation and the certain multiple Fed interest rate hikes to fight it once again.

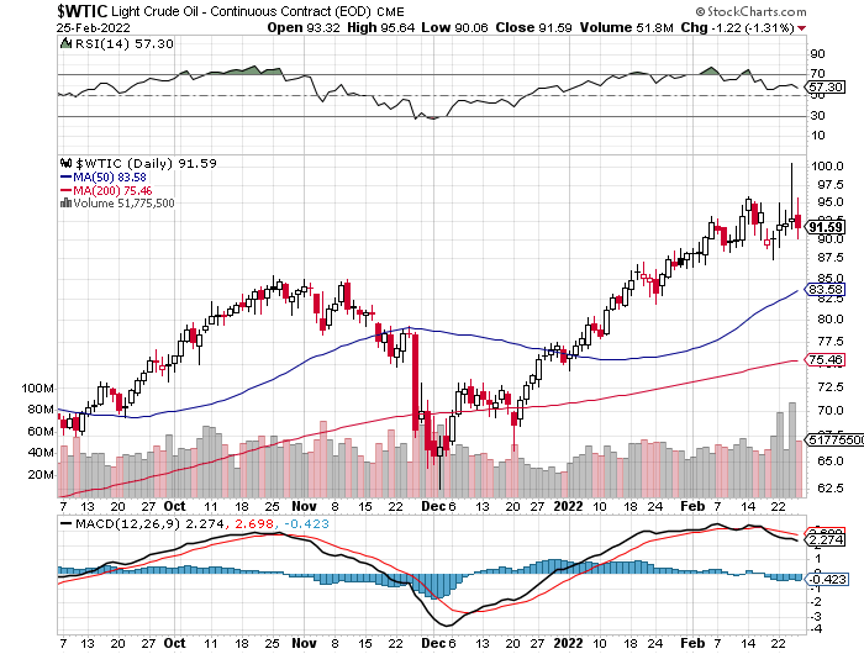

And guess what? Wars are inflationary. We are already seeing surges in the price of energy, wheat, and nonferrous metals.

So, I think I’ll stick to the short side for the time being. After all, it’s worked pretty well so far in 2022. You’ll still need to maintain some discipline here, only selling rallies.

If the US acts fast, there is an opportunity here for it to create a second War in Afghanistan for Russia. It’s certainly trying. As I write this, there are already long convoys of NATO trucks that carry ammunition and antitank missiles into the Ukraine. If you remember, it was its loss of the first one that led to the demise of the Soviet Union. I think Putin has bit off more than he expected.

For those who are maintaining core long-term portfolios, which are most of you, writing, or selling short front month out-of-the-money call options against your positions is a great idea. It will reduce your risk, lower your average cost, reduce your volatility, and bring in some extra income. Option volatilities are still high, so you can earn a pretty penny with such a strategy.

And if in case we return to happy days again, you will be taken out of your positions at higher prices with bigger profits and will think you have died and gone to Heaven.

What is the other smart trade here? If you have any energy exposure whatsoever this is a generational opportunity to get rid of it. The best-case golden scenario has happened. Even if oil goes to $125 short term, your energy stocks won’t go much higher from here.

If Russia and Saudi Arabia are trying to exit the energy business, maybe you should too.

There has been a lot of speculation about Putin’s timing of his invasion of the Ukraine. The winter, oil inventory shortages, and NATO’s half-century of underinvestment in defense were all factors.

But the most important one is being completely ignored. Putin has to unload his country’s energy resources before they become worthless, which I reckon will happen in about 20 years.

That means in two decades, some 70% of Russia’s total government revenues vaporize. The invasion of the Ukraine allows Putin to get rid of more energy faster at higher prices right now.

As my old friend, Dr. Armand Hammer used to say, “Everything boils down to oil.” (click here for the link).

Without energy, Russia has little to offer the world but a few metals and a lot of unregulated hackers. You see the same motivation in Saudi Arabia’s massive investment in alternative energy in California. And yes, they really did try to buy all of Tesla three years ago (TSLA) before the shares rose fivefold.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

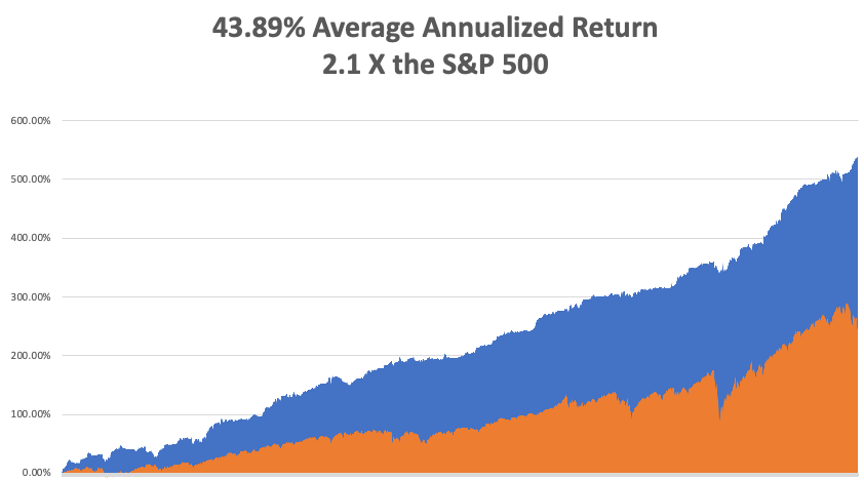

With near-record volatility fading fast, my February month-to-date performance rocketed to a blistering 10.51%. It turned out to be a great month to play from the short side in size. My 2022 year-to-date performance ended at 25.10%. The Dow Average is down -6.1% so far in 2022. It is the great outperformance on an index since Mad Hedge Fund Trader started 14 years ago.

I went into the Russian invasion with 90% cash, expecting trouble. I stopped out of a long in Apple (AAPL) in a day for a small loss. The next trade I added was another short in bonds, followed quickly by a new long in Tesla (TSLA) ($700 a share? Really?). Within hours the stock was up $100!

That brings my 13-year total return to 537.66%, some 2.00 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 43.89%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 79 million and rising quickly and deaths topping 950,000, which you can find here.

On Monday, February 28 at 8:00 AM EST, the president delivers the State of the Union Speech

On Tuesday, March 1 at 8:30 AM, the ISM Manufacturing Index for February is out.

On Wednesday, March 2 at 5:15 AM, the ADP Private Employment Index is released.

On Thursday, March 3 at 8:30 AM, Weekly Jobless Claims are published.

On Friday, March 4 at 8:30 AM, the February Nonfarm Payroll Report is Published. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, I’m not supposed to be alive right now. In fact, the betting in my extended family is that I would never make it past 30. But here I am 40 years after my “sell by” date and I’m having the last laugh.

There were times when it was a close-run thing. Breaking my neck in a 70 mile per hour head-on collision in Sweden in 1968 didn’t exactly help my odds. Nor did watching a land mine blow up the guy in front of me in Cambodia in 1975, showering me head to toe with shrapnel and bone fragments.

After crashing three airplanes in Italy, Austria, and France, the European Union Aviation Safety Agency certainly wishes I died at a much earlier age. So, no doubt did the tourists at the top of the Eifel Tower one day in 1987, who I just missed hitting by 100 feet (yes, I was the Black Baron).

When I was in high school, the same group of four boys met every day at recess. We were all in the same Boy Scout Troop and became lifelong friends. Since I had been to over 50 countries by the age of 16, I was considered the wild man of the bunch, the risk-taker, always willing to roll the dice. The rest lived vicariously through me. But I was also the lucky one.

For a start, I was not among the 22 from my school who died in Vietnam, 11 officers and 11 draftees. Their names are all on the Vietnam Memorial Wall in Washington DC. My work for the Atomic Energy Commission at the Nuclear Test Site gave me a lifetime draft exception on national security grounds.

But I went anyway, on my own dime, to see who was telling the truth. It turned out no one was.

The other three boys in my group played it safe, pursuing conventional careers and never took any risks.

David Wilson was the first to go. He managed a hotel in Park City, Utah for a national chain. When he was hiking in the Rocky Mountains one day, a storm blew in and he went over a cliff. They didn’t find his body for a week.

Paul Blaine went on to USC and law school. In his mid-fifties, he lost a crucial case and shot himself at his desk at his Newport Bay office. I later learned he had been fighting a lifetime battle against depression. We never knew.

Robert Sandiford spent his entire career working as a computer programmer for the city of Los Angeles. By the time he retired at 65, he was managing 40 people. He pursued his dream to buy a large RV, drive it to Alaska, and play his banjo in a series of blue grass festivals.

Robert was unfamiliar with driving such a large vehicle. Around midnight, he was driving north on Interstate 5 near Modesto, CA when he passed a semi. When he pulled back into the slow lane, he clipped the front of the truck on cruise control with a driver half asleep. The truck pierced a propane tank on the RV, blowing up both vehicles. Robert, his wife Elise, and the truck driver were all burned to death.

At least, this was the speculation by the California Highway Patrol. Robert and Elise went missing for months. We thought that maybe his RV had broken down somewhere on the Alaskan Highway and family members went there to look for him. It was only after the Los Angeles County Coroner discovered some dental records that we learned the truth.

When the bones were returned, the family had them cremated and we scattered the ashes in the Pacific Ocean off Catalina Island where we used to camp as scouts.

I have been rewarded for risk taking for my entire life, so I keep at it. Similarly, I have seen others punished for risk avoidance, as happened to all my friends. The same applies to my trading as well. The price of doing nothing is far greater than doing something, and being aggressive offers the greatest reward of all.

This summer, I am scheduled to fly an 80-year-old Supermarine Spitfire fighter aircraft over the white cliffs of Dover, of Battle of Britain fame. I am spending my evenings memorizing the 1940 operations manual just to be safe, as I always do with new aircraft.

A 70-year-old flying an 80-year-old plane, what could go wrong with that?

Oh, and I am learning the banjo too.

I’ll send you the videos.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

That’s a Heck of a Dividend

Global Market Comments

February 18, 2022

Fiat Lux

Featured Trades:

(FEBRUARY 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(NVDA), (MSFT), (VIX), (ROM), (TSLA), (GOOGL), (TLT), (TBT), (IWM), (QQQ), (FCX)

Below please find subscribers’ Q&A for the February 16 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, Nevada.

Q: Is it a mistake to try to be nimble with the ProShares UltraShort 20+ Year Treasury ETF (TBT), or is it better just to hold it through the rest of the year?

A: You should do both; have a core long position which you keep through the end of the year, and you also have a second position that you trade. A good example is how I just took profits on the short iShares 20+ Year Treasury bond ETF (TLT) even though it had a month to run because we had 91.67% of the profit in hand. So, when you get way in the money and still have a lot of time duration left, there’s no point in continuing with these put spreads to catch the last 5 or 10% in the position. The risk/reward is no good.

Q: The iShares 20+ Year Treasury bond ETF (TLT) seems washed out.

A: There is a risk of that, which is why I went long the (TLT) $127-$130 March vertical bull call spread. I think even if we get down to $130, it will take us at least a month to get down that far. There will be several short-covering rallies along the way that we can run out the clock with, and I think even my 3/$127-$130 should expire at max profit.

Q: Should we buy puts or spreads?

A: When you get the CBOE Volatility Index (VIX) over 30, it’s only because you get a very sharp collapse in stocks, and there you’re looking at very deep in the money call spreads— 10-20% in the money can still make you $1,000 or $2,000 a month. And if you get extreme selloffs with (VIX) up to $40, then you’re really looking for long-term LEAPS, one-year call spreads on your favorite stocks, like Tesla (TSLA), NVIDIA (NVDA), and Microsoft (MSFT), and so on.

Q: Is it time to enter Tesla (TSLA) now?

A: I’m waiting for one more final selloff—if we get that, we could get back into the low 800s or even the 700s in Tesla. That's the figure I’m hanging on for, and that's where you get into Tesla LEAPS because Tesla is clearly expanding beyond just the electric car business. SpaceX is now worth $100 billion dollars, and the boring company could be worth just as much if they get more contracts for building underground mass transit. There is also Solar City to consider plus some other stuff they haven’t even announced yet.

Q: What are your thoughts on Google (GOOGL)?

A: The 20 to 1 split is in the price already. But any selloff and I would go back into there with call spreads because Google is a fantastic company and a legal monopoly which I love owning.

Q: What about the ProShares Ultra Technology ETF (ROM)?

A: Yes, I’m watching very closely. It had a huge dive in January, then made back nearly half its losses. So again, I'm waiting for another dip to go back into (ROM) with lots of leverage.

Q: Do we get Volatility Index (VIX) over $30 within 2 months?

A: Yes, I think we probably will. We’re pretty close to it now; we got up to $26 this morning. So yes, I’d be a buyer of that.

Q: Is a (TLT) $128-$131 call spread for March still ok?

A: Yes, I kind of like that. I don’t think we’ll get down below $131 in four weeks, and at the very least we’ll get one rally of several points, and that’ll be your chance to get out of that position.

Q: Is it too early for (TLT) LEAPS?

A: No, it’s too late for TLT LEAPS. You should have been doing put LEAPS in November, and everybody who did that got profits of nearly 100% on that position. I don’t see a call side LEAPS in TLT for at least 5 to 10 years when interest rates get up over 6% on 10 year US Treasury bonds. We are a long way from a (TLT) call LEAP.

Q: Are we at a Bitcoin bottom?

A: Possibly, 50/50 chance we go back and retest the lows. We’ll just have to see how Bitcoin behaves in a rising interest rates scenario because ever since Bitcoin was invented, interest rates have been falling. Rising rates are a new thing for Bitcoin and no one knows what that will look like.

Q: When will you update your long-term portfolio?

A: Soon; things have been kind of busy issuing 30 trade alerts a month.

Q: How high will the ProShares UltraShort 20+ Year Treasury bond fund (TBT) go?

A: Looking for $26 from current levels, so yes, much higher to go. And we have a double in three months on (TBT) at the $28 level.

Q: If one believes in the war in Ukraine happening soon, what companies or sectors do you invest in for the short term?

A: None; if we actually do get a war, everything gets absolutely slaughtered, and then you’re looking for the buy. And that will be buys in tech especially. I don’t think there’s going to be a war in Ukraine, but the only things that go up in a Ukraine war scenario are energy stocks (USO), oil companies, and so on.

Q: Do you like China EV stocks?

A: No, I don’t. I visited BYD Motors 15 years ago and they just don’t have the technology, the battery lengths are poor, and they tend to catch on fire. They have never been able to reach American quality standards on any of their cars, not only the EVs but also the conventional internal combustion engines as well..

Q: Which index will outperform in the second half, the Invesco QQQ Trust (QQQ) or iShares Russell 2000 ETF (IWM)?

A: I vote (QQQ). I think we have a technology-led bull market in the second half, and the Russel will be lagging.

Q: What’s better, copper or copper miners?

A: You always go for the miners like Freeport McMoRan (FCX)—they will outperform the physical metal by at least three or four to one, to the upside. That’s also true with gold miners and other derivative plays; the miners always outperform the metals.

Q: What is a bond vigilante?

A: That is a term we heard from the ‘70s and ‘80s when you would get enormous selling of bonds on even the slightest negative piece of economic data or inflation data. They called the bond traders the bond vigilantes because they just crushed the bond market for the slightest transgression on the inflation/economic front. And they are back, by the way, hugely punishing the market as we have seen ($20 points in two months is a lot of punishment) on even the slightest increase in inflation.

Q: Do you have a yearend price for Freeport McMoRan (FCX)?

A: Over $50—just rallied from $30 in September.

Q: Isn’t inflation wildly understated?

A: Yes, you can find individual items that are up 30 or 50%, but the inflation calculation is actually based on 105 different items, and some of them are going down in price. For example, you had an enormous increase in used car prices in December, but they actually went down last month. So, whenever you get a basket this big, eight groups of 80,000 items, you get smaller moves. As anyone will tell you who trades baskets of stocks against the individual stocks, the same mathematical effect happens in the calculation. And while it is being wildly understated now, it’ll be wildly overstated in a few months when we get back to the 3% level, which I am expecting.

Q: What is your TLT prediction after the next 3 or 4 interest rate hikes?

A: Remember, the interest rate hikes only affect the overnight rate. TLT is a 10 to 20-year basket of bonds, so they don’t trade one for one. We may reach a bottom by the end of the year in the (TLT) somewhere in the $120s, but it’s not going to 100 this year and it’s not going to zero like some people are predicting.

Q: The inflation measure is a joke.

A: Yes, it has always been a joke. Any collection of data among 330 million people is going to be inaccurate, late, and have huge lags—but you trade the data you have, not what you wish you had, and that is the real world. I've been trading economic data for 50 years and that is my conclusion.

Q: Martial Law was declared in Canada— is there anything to trade off of that news?

A: No; even a major international event only gets a stock market reaction of usually one day or two at the most. Whatever’s happening on a bridge in Canada, nobody here really cares.

Q: Are you doing a cruise?

A: Yes, I’m doing a Norwegian cruise. Just go to the lunches section on the madhedgefundtrader.com website, and you can still buy tickets. We would love to have you for lunch on the Queen Victoria, a Norwegian Fjord cruise. We’re coming up to payment time on the tickets.

Q: Will there be earnings disappointment in April?

A: Yes, the year-on-year comparisons are going to be difficult. That will be another problem for the market in the spring in addition to the Fed.

Q: What happens with the FOMC out today at 2:00?

A: It will show a heightened fear of inflation and a greater urgency to raise interest rates.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

1932 De Havilland Tiger Moth

Global Market Comments

February 15, 2022

Fiat Lux

Featured Trades:

(HOW TO HANDLE THE FRIDAY, FEBRUARY 18 OPTIONS EXPIRATION),

(TLT), (SPY), (BRKB), (TSLA), (MSFT), (AMZN)

Happy and newly enriched followers of the Mad Hedge Fund Trader Alert Service have the good fortune to own a record ten deep in-the-money options positions that expire on Friday, February 18 at the stock market close in three days.

I have to admit that I traded like a Wildman this month, pedal to the metal, and 100% invested. This will take our 2022 year-to-date performance to over 24%. I like to think that is the end result of my 53 years investment in researching trading strategies.

Sometimes overconfidence works.

It is therefore time to explain to the newbies how to best maximize their profits.

These involve the:

Risk On

World is Getting Better

(TLT) 2/$149-$152 put spread 10.00%

(TLT) 2/$147-$150 put spread 10.00%

(TLT) 3/$150-$153 put spread 10.00%

(BRKB) 2/$270-$280 call spread 10.00%

(TSLA) 2/$600-$650 call spread 10.00%

Risk Off

World is Getting Worse

(MSFT) 2/$340-$350 put spread -10.00%

(SPY) 2/$465-$475 put spread -10.00%

(SPY) 3/$470-$480 put spread -10.00%

(AMZN) 2/$3400-$3500 put spread -10.00%

(TLT) 3/$127-$130 call spread -10.00%

Total Net Position 0.00%

Total Aggregate Position 100.00%

Provided that we don’t have another 2,000-point move down in the market in the next three days, these positions should expire at their maximum profit points.

So far, so good.

I’ll do the math for you on our deepest in-the-money position, the Tesla (TSLA) February 18 $600-$650 vertical bull call spread, which 50% in the money from its lower strike price which I almost certainly will run into expiration. Your profit can be calculated as follows:

Profit: $50.00 expiration value - $43.00 cost = $7.00 net profit

(2 contacts X 100 contracts per option X $7.00 profit per option)

= $1,400 or 16.28% in 15 trading days.

Many of you have already emailed me asking what to do with these winning positions.

The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck, and pat yourself on the back for a job well done.

You don’t have to do anything.

Your broker (are they still called that?) will automatically use your long position to cover your short position, canceling out the total holdings.

The entire profit will be credited to your account on Monday morning February 21 and the margin freed up.

Some firms charge you a modest $10 or $15 fee for performing this service.

If you don’t see the cash show up in your account on Monday, get on the blower immediately and make your broker find it.

Although the expiration process is now supposed to be fully automated, occasionally machines do make mistakes. Better to sort out any confusion before losses ensue.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. You can probably unload them pennies below their maximum expiration value.

Keep in mind that the liquidity in the options market understandably disappears, and the spreads substantially widen, when a security has only hours, or minutes until expiration on Friday, February 18. So, if you plan to exit, do so well before the final expiration at the Friday market close.

This is known in the trade as the “expiration risk.”

One way or the other, I’m sure you’ll do OK, as long as I am looking over your shoulder, as I will be, always. Think of me as your trading guardian angel.

I am going to hang back and wait for good entry points before jumping back in. It’s all about keeping that “Buy low, sell high” thing going.

I’m looking to cherry-pick my new positions going into the next month-end.

Take your winnings and go out and buy yourself a well-earned dinner. Just make sure it’s take-out. I want you to stick around.

Well done, and on to the next trade.

You Can’t Do Enough Research

Global Market Comments

February 9, 2022

Fiat Lux

Featured Trades:

(WHY TESLA IS TAKING OVER THE WORLD)

(TSLA), (GM), (TM)

(TESTIMONIAL)

It was another typical Elon Musk earnings call.

Tesla is evolving into the world’s preeminent robotics and AI company.

It is building the largest neural network in history, which means all the Tesla’s ever made are talking to each other, some four million by the end of this year.

When the US goes all electric in a decade, the size of the power grid is going to triple (buy copper), or else brownouts and outages will become constant. Every home in the country is going to need solar roofs to meet the demand.

Demand for cars is the greatest Tesla has ever seen, far beyond their ability to produce them, and Q1 is the slow quarter for the auto industry. I just tried to buy a new Model X and the waiting list is one year. In fact, I can sell my existing 2018 Model X on eBay for more than I paid for it….new.

Elon never fails to amaze.

As for the stock, you have to get used to the idea that the world’s greatest company has annual 45% drawdowns. That’s how Tesla has always traded. It's either going to zero or infinity, depending on who you talk to.

My decade target is still $10,000 per share. We just had a $420, 35% pullback, so we may take one more run at the lows before we go to new Highs. But I have only been trading Tesla shares for 11 years. What do I know?

I’ll never forget my first tour of the Fremont factory in 2010, right after they bought it for stock from Toyota (TM) out of the General Motors (GM) bankruptcy (Toyota owned half). Tesla then occupied only a tiny corner of the gigantic 50,000 square foot space.

But you know what? There were virtually no humans on the assembly line, just a long row of red German-made robots. There was just the occasional guy shooting oil into automatic joints.

It was a vision into the future.

I knew I was on the right track when the salesman told me that the customer who just preceded me for a Tesla Model X P100D SUV was the Golden Bay Warriors star basketball player, Steph Currie.

Well, if it’s good enough for Steph, then it’s good enough for me.

So, when I received a call from Elon Musk’s office to test the company’s self-driving technology embedded in their new vehicles for readers of the Diary of a Mad Hedge Fund Trader.

I did, and prepare to have your mind blown!

I was driving at 80 MPH on CA-24, a windy eight-lane freeway that snakes its way through the East San Francisco Bay Area mountains. Suddenly the salesman reached over a flicked a lever twice on the left side of the driving column.

The car took over!

There it was, winding and turning along every curve, perfectly centered in the lane. As much as I hated to admit it, the car drove better than I ever could. It does especially well at night or in fog, a valuable asset for senior citizens whose night vision is fading fast.

All that was required was for me to touch the steering wheel every minute to prove that I was not sleeping.

The cars do especially well in rush hour driving, as it is adept at stop-and-go traffic. You can just sit there and work on your laptop, read a book, call some customers, or watch a movie on the built-in 5G WIFI HD TV.

When we returned to the garage the car really showed off. When we passed a parking space, another button was pushed, and we perfectly backed 90 degrees into a parking space, measuring and calculating all the way.

The range is 300 miles, which I can recharge at home at night from a standard 220-volt socket in my garage in seven hours. When driving to Lake Tahoe, I can stop halfway at get a full charge in 30 minutes at a Tesla supercharging station.

The new chargers operate at a blazing 400 miles per hour. That’s enough time to walk to the subway next door and get a couple of sandwiches.

The chassis can rise as high as eight inches off the ground so it can function as a true SUV.

The “ludicrous mode,” a $12,000 option, take you from 0 to 60

mph in 2.9. However, even a standard Tesla can accelerate so fast that it will make the average passenger carsick.

Here’s the buzzkill.

Tesla absolutely charges through the nose for extras.

The 22-inch wheels, the third row of seats to get you to seven passengers, the premium sound, the leather seats, and the self-driving software can easily run you $30,000-$40,000.

A $750 tow hitch will accommodate a ski or back rack on the back. There is a $1,000 delivery charge, even if you pick it up at the Fremont factory.

It’s easy to see how you can jump from an $84,990 base price to a total cost of $162,500, including taxes, for the ultra-luxury Performance model, as I did.

As for “drop dead’ curb appeal, nothing beats the Model X. When I first started driving Tesla’s I used to get applause at stoplights. It took a while to realize they were cheering the car, not me.

Even after driving one of these for 11 years, I still get notes with phone numbers from young women asking for rides. And they don’t even offer that as an option!

My original split-adjusted cost for my Tesla shares is $3.30.

It’s still true that if you buy the shares, you get the car for free.

I got three.

Thank You, Elon!

Mad Hedge Bitcoin Letter

February 8, 2022

Fiat Lux

Featured Trade:

(BITCOIN MOMENTUM PICKS UP)

(BTC), (ETH), (TSLA)