Mad Hedge Technology Letter

November 28, 2022

Fiat Lux

Featured Trade:

(US ECOMMERCE HOLDING UP)

(CPI), (TWTR), (BNPL)

Mad Hedge Technology Letter

November 28, 2022

Fiat Lux

Featured Trade:

(US ECOMMERCE HOLDING UP)

(CPI), (TWTR), (BNPL)

Black Friday and the ecommerce season hit us with a bang and we are embracing it.

How has it gone so far?

We’ve broken numerous records offering positive news for the US economy and the corresponding tech sector.

Ecommerce sales grew 2.3% year-over-year on Black Friday.

The US economy continues to be the cleanest shirt in the laundry hamper.

There’s been some doubt whether the US consumer can hold up during the holiday season amid unrelenting price increases on just about anything and everything throughout 2022.

It’s looking good so far.

The numbers vindicate the amazing US online economy with consumers spending a record $9.12 billion online shopping during Black Friday this year.

Another nice bullet point to add to the success of the ecommerce holiday season is the particular items that were purchased which drastically favored tech items.

Popular items included gaming consoles, drones, Apple MacBooks, Dyson products and toys like Fortnite, Roblox, and Bluey.

Thanksgiving was also a major success this year with sales expanding by 2.9%.

The strength of the US consumer is exactly why I believe the biggest upside surprise to next year’s tech story is the economy not succumbing to a painful recession as early as we first thought.

Consumer sentiment has decreased somewhat because of the associated headwinds that have caused discretionary budgets to tighten like higher shelter prices and energy costs.

Yet, the US consumer stays resilient.

This year, Cyber Monday is expected to drive $11.2 billion in spending, up 5.1% year-over-year.

The cons to the latest news are that the US consumer is going deeper into debt to make these holiday purchases.

Buy Now Pay Later payments increased by 78% compared with the past week, and Buy Now Pay Later revenue is up 81% year-over-year.

The runway will eventually run out for the BNPL model because consumers won’t be able to make payments if they overextend themselves.

Another issue that could crop up is if BNPL makes it costlier to borrow money to finance purchases instead of a 0% interest borrowing plan.

That will definitely dent the volume of ecommerce sales.

Then there is the issue of not just the nominal numbers, but the real numbers.

Inflation measured by the CPI index is 7.7% but sales growth was 2.3% for Black Friday.

In real terms, real growth is negative 5.4% year-over-year.

There is a high likelihood that the US consumer is spending an extra 2.3% on products, but receiving significantly less in value for what they pay for.

Many products are being made with less quality and in smaller sizes or are being discontinued altogether.

Effectively, the American consumer is spending an extra 2.3% but getting back -5.4% in relative value, but tech corporations can and will claim victory for growing ecommerce sales.

This type of data offers insight into why American GDP is barely growing with full employment.

Usually, full employment would suggest stronger GDP growth.

To extrapolate more, the data suggest that the efficiency per worker in the US is declining and stark examples can be found at companies such as Twitter.

Twitter runs better as a product, management, staff, and service after firing 75% of staff.

All in all, nominal tech ecommerce numbers performed well enough, but such hidden downsides in the report give a bitter aftertaste.

This could mean we are range bound in the short term for tech shares.

There was nothing in these numbers that would make me want to bid up tech shares going into yearend unless a bullish external macro event suddenly takes place.

Mad Hedge Technology Letter

October 21, 2022

Fiat Lux

Featured Trade:

(A SMART WAY OUT)

(TWTR), (TSLA), (SNAP)

In a crazy turn of events, the US government is considering a national security review of Elon Musk’s Twitter (TWTR) takeover deal.

The review could potentially block the deal, saving Musk $44 billion.

I would say that Musk has been playing up this angle for quite some time.

It’s no coincidence that he started meddling in the Russian-Ukraine dialogue just recently.

Hatching a plan to tick off the US government enough for them to decide a perceived pro-Putin supporter cannot control the reigns of the biggest public discourse forum in the world would signify a massive victory for Musk.

We know Twitter isn’t worth $44 billion.

Snap issued terrible earnings which meant the new valuation of SNAP went from $19 billion to $13 billion company in one day.

Things are so bad at SNAP that they chose to not offer guidance for the 2nd straight quarter.

Musk has also voiced how he plans to reinstate former US President Donald Trump and fire 75% of the Twitter staff on the first day on the job.

He is doing his best to “achieve” a national security review which is executed by the Committee on Foreign Investment in the US (CFIUS).

CFIUS carries out security reviews if a "transaction threatens to impair the national security of the United States," according to federal regulations.

It’s also not a shocker that Musk recently threatened to stop supplying the Starlink satellite service to Ukraine.

If Musk is perceived to not be working for Ukraine, in the political world today, this means he can be labeled a pro-Russian, pro-Putin, anti-democratic, anti-American figure worthy of tech deals getting banned.

Ironically enough, he does the dirty work for the Chinese Communist Party because he operates a gigafactory in Shanghai which produces the most Tesla’s per factory.

Musk later backed down from his threat to stop deploying Starlink and agreed to continue to suffer losses operating the service.

Musk has been providing the service for free but has said SpaceX loses $20 million a month servicing Ukraine.

I must say that Musk has a serious pathway to wriggle himself out of this $44 billion deal.

If the deal is blocked, Twitter would be valued at around $15 billion-$20 billion range, possibly $25 billion is a stretch.

It would be a devastating blow for the Twitter management and shareholders.

Management would need to change instantly because of the brand damage and loss of credibility. Musk has attacked the management and staff at Twitter non-stop throughout this process.

A major restructuring is in the cards no matter what.

Job morale at the firm is at an all-time low as Twitter employees experience depression through a threat of possible termination upon Musk’s purchase.

The fiasco is essentially what Musk wanted in the first place and I could argue that the free PR he is receiving is worth at least $100 billion from start to finish.

Musk understands the more digital footprints he plants all around the internet, the richest man in the world will get many articles published about him. Just do a Google search of Musk and he’s everywhere.

Whether it is about spaceships or social media, Musk has launched himself front and center into almost every discourse including sensitive geopolitics to solving world hunger. He even said one time he wants to buy soccer club Manchester United.

About social media tech stocks, this is highly negative news for the valuations of other social media stocks like Meta (META), but this is great news for Tesla stock if Musk doesn’t need to sell Tesla stock to pay for the Twitter deal.

Musk still needs another $10 billion in financing to cover the balance of the deal to finish the deal.

Global Market Comments

October 10, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or EATING YOUR SEED CORN),

(SPY), (TLT), (PANW), BRKB), (JPM), (MS), (V),

(USO), (MU), (RIVN), (TWTR), (TSLA)

You know that 10% downside risk I talked about? In other words, you may have to eat a handful of your seed corn.

We may have to eat into some of that 10% this week. With the September Consumer Price Index out on Thursday, and the big bank earnings are out Friday, there is more than a little concern about the coming trading week.

That’s why all my remaining positions are structured to handle a 10% correction or more and still expire at their maximum profit point in nine trading days.

Even in the worst-case Armageddon scenario, which we are unlikely to get, the S&P 500 is likely to fall below 3,000, or 627.90 points or 17.25% from here.

That’s what you pay me for and that’s what you are getting.

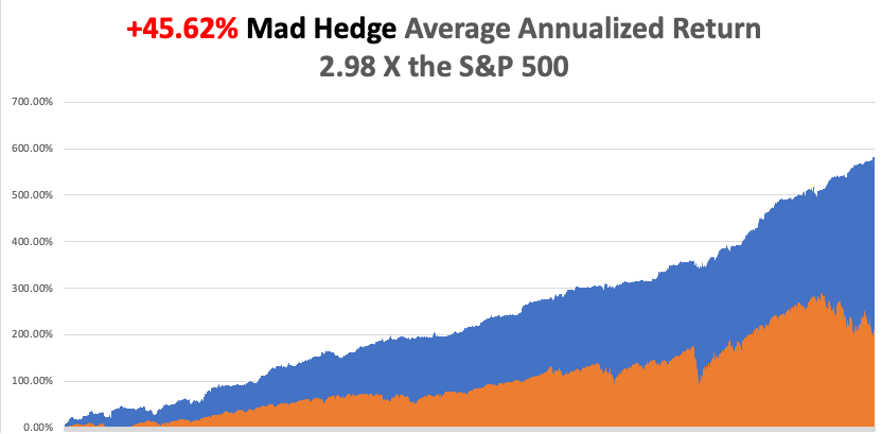

I shot out of the gate with an impressive +3.25% gain so far in October. My 2022 year-to-date performance ballooned to +72.93%, a new high. The Dow Average is down -19.3% so far in 2022 or a gob-smacking -7,000 points. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +81.35%.

That brings my 14-year total return to +585.49%, some 3.03 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +45.62%, easily the highest in the industry.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago.

I used last week’s extreme volatility to rearrange positions, adding longs in Morgan Stanley (MS), JP Morgan (JPM), and Visa (V). That takes me to 80% long, 20% short, and 0% cash. I wisely rolled down the strikes on my Tesla position from $230-$240 to $200-$210. I covered one short in the S&P 500 (SPY). All of my options positions expire in only nine trading days.

I know that you’re probably getting boatloads of advice the sell all your stocks now, sell your house, and head for those generous 5% short term interest rates, and 8% in junk. Even I went 100% cash….in December last year. The problem is that these other gurus are giving you advice that is only a year late with perfect 20/20 hindsight.

To bail now, you risk giving up on the 100% gains in years to come. If I’m wrong, you lose 10%, if I’m right, you get a double or more. Sounds like a pretty good bet to me.

People always want to know how I pick market bottoms, something I have been doing since the Dow Average was at a miniscule $753.

The lower the market is, the less aggressive the Fed is going to be

Every single input into the Consumer Price Index is now turning down sharply, especially rents and housing costs, meaning we can expect a blockbuster decline when the next report comes out on October 13

We now have two outsiders doing the Fed’s job for it, the British economy, which is clearly collapsing, and a strong US dollar that is rapidly shrinking the foreign revenues of our multinationals, like big tech.

Capitulation indicators, occasionally spotted here and there, are now coming in volleys, the Volatility Index at $35, the (VIX) curve inversion, the RSI below 30, the ten-year US Treasury yield hit 4.0% and then instantly backed off, the British pound plunged to $1.03, and we saw absolutely massive retail selling in September.

The froth is now out of all tech stocks.

All of this brings forward the last Fed hike in interest rates and the next bull market in stocks. If the last Fed rate hike is two months away on December 14, then the reasons to sell stocks are disappearing like the last sands in an hourglass.

In my mere half century in the market, every time the CPI starts to fall, stock market “V” bottoms and begins classic “rip your face off’ rallies as the shorts panic to cover. It happened in 1970, 1974, 1980, 1990, and 2009. It will happen again in 2022. The market will smell that inflation is done, the Fed is done, and volatility becomes a distant memory.

And I hate to be so obvious, but if you sell in May, what do you do in October? You buy with both hands. Just do it on the right day. That could get you a 10% to 20% move by yearend. The S&P 500 earnings multiple has collapsed by eight points in nine months and that is too far, too fast.

How do midterm years perform? October is the best month of the year followed by November. Of the entire 16-month presidential election cycle, the coming first quarter of 2023 is the best of the entire lot.

Nonfarm Payroll Falls Short at 263.000 in September. The headline unemployment rate matched a 2022 low at 3.5%. The long-term unemployment rate, the U-6 also matched this year’s low at 6.7%. The report keeps the Fed on its current interest raising schedule. Stocks, bonds, and gold sold off 500-points.

JOLTS Drops Sharply, from an expected 11.0 million to only 10.05 million. This is the job openings report from the Department of Labor. It’s one of the sharpest declines in history. The jobs market is finally starting to deteriorate, which is just what the Fed wanted. Factory Orders for August were unchanged.

OPEC+ Cuts Quotas by 2 million, and production by 1 million, in one of the largest reductions in history. It’s an effort to maintain oil prices at current prices in the face of falling demand from a global recession. The Arabs are not your friends. It’s also a slap in the face of the anti-oil posture, pro-climate posture of the Biden administration, which responded with a further release of 10 million barrels from the Strategic Petroleum Reserve. Energy stocks soar across the board. Don’t get caught standing when the music stops playing. Avoid (USO).

Why Did Russia Blow Up Their Own Pipeline? International analysts are puzzled by Putin’s latest hostile move. Is this a prelude to limited nuclear war in Ukraine? My view is that Putin expects to be deposed soon and wants to make it difficult for the next government to resume relations with Europe. Others argue that the true motivation is to enable Nordstream to file a $10 billion insurance claim. Good luck collecting on that one.

Advanced Micro Devices Bombs on weak PC sales and supply chain problems, taking the stock down 5% aftermarket. Profit margins were cut. The news could take the stock down to new lows, which didn’t really participate in this week’s monster rally. The rest of the tech sector sold off in sympathy.

Tesla Breaks Production Records in Q3, manufacturing 365,000 EVs and delivering 365,000, a record high. Sales prices have risen three times this year, while commodity costs have fallen dramatically, widening profit margins. This is the most volatile stock in the market, with one 52% correction so far this year, and another 23% correction in recent weeks. It’s the reason we just saw a “buy the rumor, sell the news” type correction that took us to the bottom of a three-month range.

Another factor is that now that big tech is rallying again, people are rotating out of Tesla, which held up well in Q3. Below here, long term Tesla bulls like my friend Ron Baron, Cathie Wood, and I start adding to big positions. With OPEC+ threatening a million barrel a day production cut, taking crude up 6%, oil alternative Tesla should be rising.

Elon Musk Pays Full Price for Twitter at $54.20 a share, completely caving on pending litigation. Wall Street consensus is that the company is worth $15 a share. It may be years before we learn what’s really going on here, leaving many scratching their heads, including me. Tesla (TSLA) plunged $15 on the news, killing off a nascent rally. The distraction of management time will be huge. Avoid (TWTR).

Rivian Raises 2025 Production Goal, from 20,000 to 25,000, after a better-than-expected 7,363 third quarter. Mass production is reaching the sweet spot for the next Tesla. The company is planning a $5 billion investment in non-union Georgia. Buy (RIVN) on dips, sell short puts and buy LEAPS.

Micron Technology to Invest $100 Billion in New York Plant. It’s all part of a retreat from China and paring war risk in Taiwan. Massive government subsidies from the Chips Act helped. Biden also expanded restrictions on the export of key semiconductor manufacturing equipment, America’s crown jewels. It means more expensive buy safer supplied chips for US industry. Buy (MU) on dips.

Hurricane Ian to Cost Insurers $63 Billion, and deaths, and the federal government may be on the hook for more. The storm double-dipped, cutting a wide swath across Florida and the Carolinas. Some 95% of the costs are carried by foreign insurers through the reinsurance market. There are too many billionaire mansions on the beach which are fully insured. This paves the way for major rate increases by insurance companies, which is why Warren Buffet loves the insurance business. Many thanks to the many foreign Mad Hedge subscribers who expressed sympathy over the storm losses.

My Ten-Year View

When we come out the other side of pandemic and the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With oil in a sharp downtrend and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, October 10, no data of note is released.

On Tuesday, October 11 at 7:00 AM, the 6:00 AM, the NFIB Business Optimism Index for September is released.

On Wednesday, October 12 at 8:30 AM, Producer Price Index for September is published. At 11:00 AM, the FOMC minutes from the last Fed meeting is released.

On Thursday, October 13 at 8:30 AM, Weekly Jobless Claims are announced. We also get the blockbuster Consumer Price Index.

On Friday, October 14 at 8.30 AM, US Retail Sales for September is disclosed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, with the 35th anniversary of the October 19, 1987 crash coming up, when shares dove 22.6% in one day, I thought I’d part with a few memories.

I was in Paris visiting Morgan Stanley’s top banking clients, who then were making a major splash in Japanese equity warrants, my particular area of expertise.

When we walked into our last appointment, I casually asked how the market was doing (Paris is six hours ahead of New York). We were told the Dow Average was down a record 300 points.

Stunned, I immediately asked for a private conference room so I could call the equity trading desk in New York to buy some stock.

A woman answered the phone, and when I said I wanted to buy, she burst into tears and threw the handset down on the floor. Redialing found all Transatlantic lines jammed.

I never bought my stock, nor found out who picked up the phone. I grabbed a taxi to Charles de Gaulle airport and flew my twin Cessna as fast as the turbocharged engines could take me back to London, breaking every known air traffic control rule.

By the time I got back, the Dow had closed down a staggering 512 points, taking the Dow average down to $1,738.74. Then I learned that George Soros asked us to bid on a $250 million blind portfolio of US stocks after the close. He said he had also solicited bids from Goldman Sachs, Merrill Lynch, JP Morgan, and Solomon Brothers, and would call us back if we won.

We bid 10% below the final closing prices for the lot. Ten minutes later he called us back and told us we won the auction. How much did the others bid? He told us that we were the only ones who bid at all!

Then you heard that great sucking sound. Oops!

What has never been disclosed to the public is that after the close, Morgan Stanley received a margin call from the exchange for $100 million, as volatility had gone through the roof, as did every firm on Wall Street.

We ordered JP Morgan to send the money from our account immediately. Then they lost it! After some harsh words at the top, it was found. That’s when I discovered the wonderful world of Fed wire numbers.

The next morning, the Dow continued its plunge, but after an hour managed a U-turn, and launched on a monster rally that lasted for the rest of the year. We made $75 million on that one trade from Soros.

It was the worst investment decision I have seen in the markets in 53 years, executed by its most brilliant player. Go figure. Maybe it was George’s risk control discipline kicking in?

At the end of the month, we then took a $75 million hit on our share of the British Petroleum privatization, because Prime Minister Margaret Thatcher refused to postpone the issue, believing that the banks had already made too much money.

That gave Morgan Stanley’s equity division a break-even P&L for the month of October 1987, the worst in market history. Even now, I refuse to gas up at a BP station on the very rare occasions I am driving an internal combustion engine.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

October 5, 2022

Fiat Lux

Featured Trade:

(THE DEAL GOES THROUGH)

(TWTR), (TSLA)

I believe there are still more twists and turns in the Elon Musk chasing after his favorite social media platform saga.

It’s getting a little out of hand now.

It seems like it’s the story that will never burn out, yet it gives us deep insight into the state of the tech industry.

It could be just a giant ploy to buy Twitter (TWTR) shares on the open market by Musk as it traded all the way down to $35 per share in July.

Musk could have feigned problematic to drag the price of shares down and scoop them up on the cheap to bring down the cost basis of the sale.

This could be the reason why Musk has offered to conclude a $44 billion acquisition of Twitter in a dramatic turn of events.

The SpaceX Chief had written to Twitter yesterday offering to close the deal at the original price of $54.20 a share.

Musk had been set for a courtroom duel with Twitter with multiple legal commentators warning he had a slim chance of succeeding in his attempt to scrap the deal.

On the surface, it certainly does appear as if Musk has been pacified and content with pushing the deal through.

However, the caveat, funding must be secured for this to go through and since the interest rate environment has turned from bad to atrocious, the other question that must be asked is whether banks can provide the necessary funding at exorbitant rates.

Musk is already thinking 5 steps ahead tweeting that the acquisition could be an “accelerant” to “creating X, the everything app”, adding the process would be accelerated by up to five years without giving further details.

Musk’s initial argument in reneging on his offer to buy the company was that it had miscounted the number of spam or bot accounts on its platform.

An “everything app” could mean something similar to China’s WeChat.

A super app in which you can do everything from paying the gas bill, to ordering pizza, and even finding a new girlfriend.

No doubt if the deal goes through, Twitter and Tesla will be inextricably linked with services of each on both.

Getting down to the nuts and bolts, Twitter is a great technology asset and one that is highly scarce.

It’s the center of conversation for anyone who is of high visibility.

Although I believe the price Musk is paying is way too high and $25 billion seems more appropriate, Musk is a victim of his own brinkmanship.

I also believe that a sharp recession that we could experience in 2023 was the real reason for securing the deal now and not later.

If Tesla’s stock tanks in 2023, it would be cringe-worthy to sell stock at depressed prices to fund a Twitter deal.

Musk saw a clear path to financing this deal and that is the clincher. It also bodes ill for tech stocks in 2023 if Musk thinks he needs to cash in now before they head lower as the Fed raises rates aggressively.

However, something tells me this deal will still get dragged out.

Mad Hedge Technology Letter

July 13, 2022

Fiat Lux

Featured Trade:

(HOT INFLATION NUMBER BODES POORLY FOR TECH STOCKS)

(LYFT), (UBER), (AMZN), (SHOP), (GOOGL), (SNAP), (META), (TWTR), (MELI), (EXPE), (TRIP)

Fed swaps now fully price in 150 basis points of hikes over the next two meetings after awful inflation numbers came in showing inflation heading in the wrong direction.

The 9.1% inflation print was an acceleration of the 8.6% which was what we got last time.

I don’t want to beat a dead horse, but inflation accelerating and beating the expectations of 8.8%, is paramount to the trajectory of tech shares.

The awful number also underscores the magnitude of policy mistakes that the U.S. Fed Central Bank has overseen.

This is the only thing that matters because macro liquidity drives the trajectory of equities in the short term.

These clowns aren’t serious about tackling inflation, as I said a few times already and this proves it!

Itty bitty rate rises won’t stamp out 9.1% inflation and in fact, encourages it.

The Fed would need to raise the Fed Funds rate by 7.35% to 9.1% immediately from the current 1.75% for the real inflation rate to be non-inflationary.

According to the official Fed website, the Fed targets 2% inflation because they call this level “healthy.”

By their own measure, to achieve this 2% inflation, they would still need to raise rates by 5.35% immediately, but they absolutely won’t because Powell simply has no interest in doing his job, period.

These core expenses skyrocketing is why I keep and kept mentioning that Americans have less money to splurge on tech gadgets and software and again, this inflation report validates my thesis.

Think about pitiful tech stocks that didn’t work in bull markets like ride chauffeurs Lyft (LYFT) and Uber (UBER), I fully expect these companies to perform terribly over the next 6 months amid a rising rate backdrop.

Not only are they growth tech, but their business is directly tied to energy prices.

They are the poster boys for the pain tech companies will feel from hyperinflation.

The outlook is quite poor for technology in the short term, and we are still waiting to form a bottom. It will come back but we need a capitulation.

The accelerated rate of inflation means that we push back the big recovery in tech stocks.

Ecommerce stocks will suffer like Amazon (AMZN), Shopify (SHOP), and MercadoLibre (MELI) because of the decline in discretional spending for the consumer.

Digital ad giants like Google (GOOGL), Snap (SNAP), Meta (META), and Twitter (TWTR) will need to reckon with smaller ad budgets from 3rd party ad purchasers as companies cut back on marketing spend.

Don’t need to increase marketing spend when people have no money to spend on products.

Travel tech stocks like Expedia (EXPE) and Tripadvisor (TRIP) can expect summer to mark peak travel as Americans get more concerned about food and oil budgets after the summer of travel revenge from the arbitrary lockdowns.

It also means there will be a meaningful next leg down for tech stocks as many CFOs are now furiously crunching the new revenue and margin downgrades to reflect this heightened risk.

The new re-rating isn’t reflected yet in tech shares.

It’s already been a few months on the trot where many analysts say this is the top, they have been inaccurate every time.

Even if it is the top, inflation will stay higher for longer and stagflation is the consensus for 2023.

The clowns at the Fed not doing their job means that economic cycles will be shorter and a great deal more volatile because the smoothing effect of moderated inflation is now stripped out of calculations. This effectively means a contracted boom-bust trajectory for tech stocks which is unequivocally what we are seeing in market behavior.