Mad Hedge Technology Letter

December 6, 2024

Fiat Lux

Featured Trade:

(A SHORT TERM TRADE)

(UBER), (GOOGL), (TSLA), (WRD)

Mad Hedge Technology Letter

December 6, 2024

Fiat Lux

Featured Trade:

(A SHORT TERM TRADE)

(UBER), (GOOGL), (TSLA), (WRD)

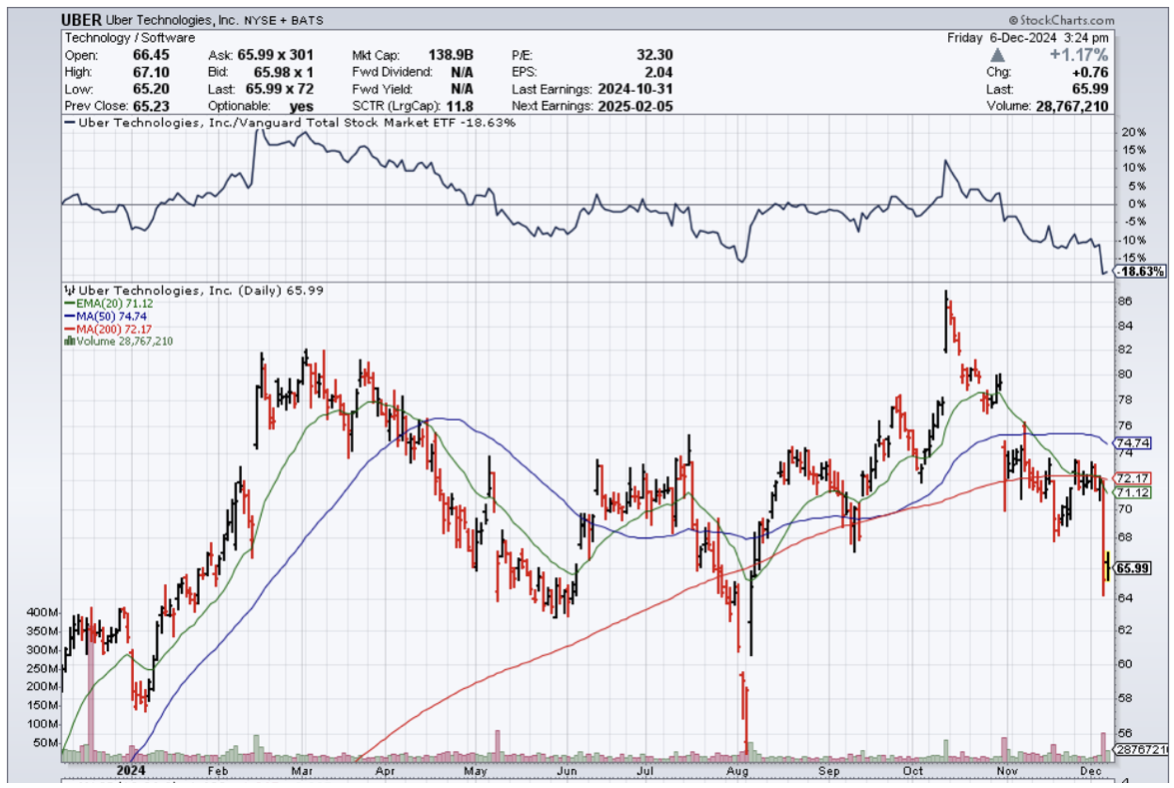

Uber’s (UBER) stock is almost 30% down from all-time high’s, and the stock was on a nice run from the lows of 2023 when the stock was trading around $25 per share.

There has been great optimism around the business, with revenge travel stoking a huge growth bump in the ride-sharing business.

Uber once burned through money like there was no tomorrow, but now it is a profitable business.

However, there are outsized risks just around the corner, and the stock has pulled back because the next risk might be existential.

They are running into one of the greatest innovators the world has ever seen.

Tesla (TSLA) and Elon Musk have made a lot of noise lately about self-driving robotaxis, and they do have their proprietary software with billions of driving hours of data.

Uber has nothing like this, and the more Elon Musk elbows out the competition about the self-driving technology, the more Uber’s share price sinks.

Uber is the tech company most affected if Musk successfully implements robo taxis as a main part of Tesla’s business.

By now, it is becoming quite apparent that EVs aren’t the holy grail of technology Musk is chasing after. It is merely a placeholder until he goes onto greater projects and technologies.

Sure, first, it would be rockets and space, but on Earth, Musk is after artificial intelligence through robots, and one of those applications would be self-driving automobiles.

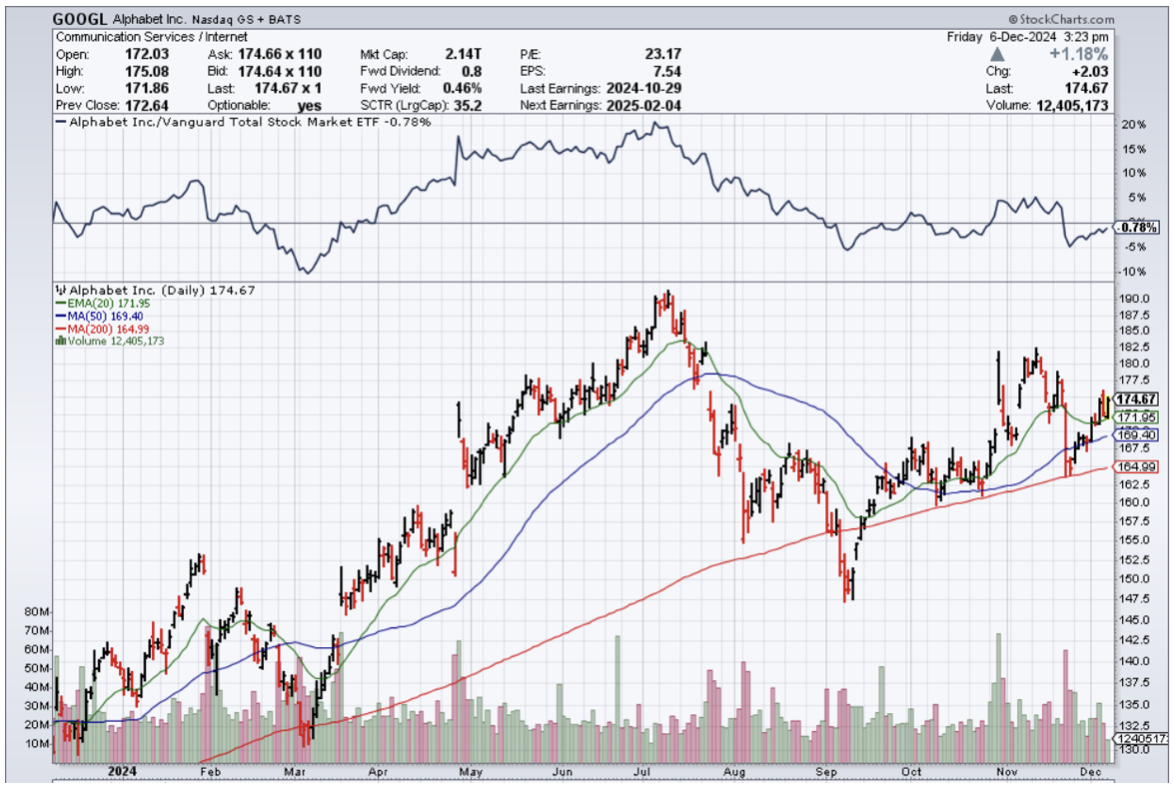

Google’s Waymo is another long-term investors in self-driving tech that will destroy Uber’s business model as well.

Uber just said it would partner with robotaxi maker WeRide (WRD) to launch ride-hailing in Abu Dhabi. Uber said it would be the first time AVs are available on the Uber platform outside of the US and that Abu Dhabi would be the largest commercial robotaxi service outside the US and China when it launches in 2025.

Waymo (GOOGL) lately said it would expand its robotaxi service to Miami, Florida.

Waymo has previously tested vehicles in Miami, the company said, a city that provided “challenging rainy conditions” for its driverless vehicles, and Uber’s stock crashed 10% on this news itself.

Waymo said it is already providing 150,000 trips per week in Phoenix, Los Angeles, San Francisco, and Austin.

Uber still has to pay for over 160 million month active riders to get shuttled around on its app, and when they are muscled out of the technology by Google and Tesla, it is not guaranteed they will be able to license this high level of proprietary technology from these big tech stalwarts.

If you are Google or Tesla, why ever involve Uber when you could pick up their riders for pennies on the dollar after Uber bankrupts itself because of the high cost of employing human drivers?

Long term looks quite grim for Uber, and I don’t believe there is a magical elixir for the self-driving software. They are too far behind.

The one hunch I have is that over the past year, Waymo and Tesla have made the concept of the masses taking self-driving technology as a real service closer and closer.

Each day, we inch closer, and the day of full implementation will be a death knell for Uber.

However, in the short term, I do believe Uber’s stock is oversold, and it could stage a bounce back in the short to mid-term.

Any dive into the high $50 range would be a great buying opportunity for a quick trade in Uber. I wouldn’t buy and hold for the long haul, there are better options.

Global Market Comments

September 27, 2024

Fiat Lux

Featured Trade:

(THE MAD HEDGE SEPTEMBER 17-19 SUMMIT REPLAYS ARE UP),

(SEPTEMBER 25 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (NVDA), (GLD), (SLV), (AGQ), (URA), (X), (PGE), (FDX), (V), (CEG), (NEE), (CCJ), (FSLR), (TLT), (WMT), (FCX), (UBER), (LYFT), (FXB), (T)

Below please find subscribers’ Q&A for the September 25 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe Nevada.

Q: The iShares 20+ Year Treasury Bond ETF (TLT) is not advancing like I had hoped. I’m not sure why the interest rate cuts have not impacted the 20-year maturity—is it too far out?

A: It’s not an issue of maturity; the fact is that the market has been discounting falling interest rates for six months, all the way back to March. It’s a classic “buy the rumor, sell the news” scenario. (TLT) rose $20 off the low this year, and once the rate cut actually happened, all the news was in. That is why I actually went short the TLT a couple of days ago, and that trade immediately started making money. Here’s the real problem: Fed futures are discounting 250 basis points in rate cuts by June of next year. If you don’t think we’re going to get 250 basis points in rate cuts, which is two 50 basis point rate cuts and five 25 basis point rate cuts, then the market is overbought for the short term and we’re selling short. That’s exactly what I did.

Q: Is it too late to buy Tesla (TSLA) and Nvidia (NVDA)?

A: No, it’s not, I think Tesla could hit $300 this year, and Nvidia could revisit $140. However, the more you wait, the more pain you have to take along the way. Nvidia did drop 40% off its high at one point this year, and Tesla dropped 80% off its high. The price of coming in late is pain, so be ready to take that pain or, even worse, to stop out.

Q: What is your take on Japan’s attempt to take over US Steel (X)?

A: Well, it’s entirely political. They definitely picked the wrong year to take a run at US steel because it’s headquartered in Pittsburgh, Pennsylvania, and neither political party can win their election without winning Pennsylvania. Nippon Steel is now 3x larger than US Steel (I covered the company for ten years when I lived in Japan.) It’s the steel factor Jimmy Doolittle bombed in the Pearl Harbor movie. US Steel is using 140-year-old technology—Open Hearth Technology—which hasn’t been updated since the Great Depression. Nippon Steel, meanwhile, is promising to scrap all of that and bring the Steel Industry into the 21st Century. All great ideas for Nippon Steel and their shareholders, but not so great for Unions; all of these takeovers always result in massive layoffs of Union workers. So, that is the issue. That’s where a large part of the added value comes from.

Q: What are the chances that interest rates drop to zero?

A: Zero. I don’t think we’ll ever see 0% interest rates again because people now understand the massive damage that causes to the economy and to savers. So, on the next interest rate cycle, we’ll go down maybe to 2% if we get a recession, but probably not much more than that.

Q: Is it a good time to buy FedEx Corp (FDX)?

A: Yes, it probably is. If there was one rule of trading this year, you buy everything on top of these monster selloffs that are caused by weak guidance. We did it on Palo Alto Networks (PANW) earlier this year—people made a fortune on that. FedEx just did the same thing, so yes, I’m looking very carefully at FedEx calls, call spreads, and LEAPS two years out.

Q: I recently saw a recommendation to buy California Utility Company PG&E (PGE) because of recent revenue gains. Should I take a look?

A: Absolutely, you should. PG&E has gone bankrupt twice in the last 25 years, and the current new management seems to know what they’re doing. They borrowed $20 billion to underground all the long-distance power lines in the state so they won’t be liable for any of these gigantic wildfires that caused the last bankruptcy. Also, you kind of want to own utilities when interest rates are falling because utilities are among the biggest borrowers in the country.

Q: Is Global X Uranium ETF (URA) a good proxy for Cameco Corp (CCJ)?

A: Yes, another one is Consolidation Energy Corp. (CEG), but they’ve all had absolutely astronomical moves ever since the announcement came out that Microsoft was reopening the Three Mile Island nuclear power plant. So, wait for a dip, but the thing is just going up every day right now.

Q: Is it time to buy iShares 20+ Year Treasury Bond ETF (TLT) LEAPS?

A: No, LEAPS territory was last year or the beginning of this year when we were in the $80s (and we issued a ton of (TLT) LEAPS last year.) LEAPS are what you do at market bottoms, not at new all-time highs or two-year highs. Remember, if LEAPS don’t work, they can go to zero, and you want to avoid the zero outcome as much as possible.

Q: Should I look at Visa Inc (V)?

A: Yes, this is another one of those poor guidance situations leading to 20% selloffs. In Visa’s case, they’re being sued by the US government for antitrust because they own 47% of the credit card market. So, I would maybe wait a little bit more, let the market fully digest that, and then Visa’s probably a really strong buy because they’re still growing at 15% a year and minting money like crazy.

Q: Do you see gold going to $3,000 next year?

A: Absolutely, yes, unless it goes to $3,000 this year, which raises a better question: what happens when gold hits $3,000? It goes to 4$,500, because Chinese savers have no other place to put their money except gold. The real estate has crashed and isn’t coming back, they don’t trust their own banks or currency—there really is nowhere else for them to put their own money. They don’t even buy gold miners, they just buy the gold metal and coins. So I think we could see much higher highs than gold, and I’m sticking to my longs.

Q: Will silver continue to lag?

A: No. In fact, in the last couple of weeks, silver has done a big catch-up that is happening because recession fears are going away. Even the soft-landing fears are starting to vaporize—we may have no landing at all. The economy may just keep going, and silver is far more sensitive to the economy than gold is; and that is all silver positive. When we get to the metals, you’ll see how much silver has actually caught up. Silver is probably the better buy here because it tends to outperform gold by two to one.

Q: Do you think the Japanese will cross 100 yen to the dollar in the near future?

A: No, but I think it may cross 100 to the dollar in two years. You’re looking at a permanently weak US dollar from now on. As long as we’re cutting interest rates faster than anyone else, our currency will be the weakest. Japan’s rates are at zero, so they’re not going to cut interest rates at all, which is why we've had this enormous move in the Japanese yen.

Q: Can you give me some good renewable energy stocks and reasons why they are good buys?

A: Well, my favorite renewables are the Canadian Uranium stock Cameco Corporation (CCJ), First Solar (FSLR), which has been the leading industrial-scale solar producer for a long time, and NextEra Energy (NEE), which is very heavily dependent on producing electric power from renewables and also have a 3% dividend.

Q: Why is the euro going up even though their economy is in such terrible shape?

A: Europe has much lower interest rates than the US, and therefore, much less ability to cut interest rates than the US; it is the interest rate cuts that are driving currencies down, and we are the world’s greatest interest rates cutter right now. So, that is why you’re getting outperformance of the euro (FXE).

Q: Financials have moved up over the last two weeks; what’s your take on year-end and beyond? Should I buy Goldman Sachs (GS), JP Morgan (JPM) and Morgan Stanley (MS)?

A: Yes on all three. They’re all big beneficiaries of falling interest rates, improving economies, declining default rates, and rising stock markets. So, you have a triple play on all three of those. I’d be buying the dips on all financials.

Q: When will the sell volatility come back?

A: When you get the Volatility Index ($VIX) over $30. That seems to be the sweet spot for selling volatility. We are now at $15.

Q: If the US sharply increases tariffs, what will be the impact on the economy?

A: It would basically amount to a 20% price increase on everything you buy—from clothes to electronic parts to everything else—and the stock market would crash. Probably 90% of the non-food items Walmart (WMT) sells is from China. That’s why they call it the Chinese embassy. Tariffs are a tremendous restraint of trade and never, ever work, except for targeted items like cars or solar panels. For instance, I am in favor of a 100% tariff on Chinese cars to keep them from demolishing our own car industry as they are currently doing in Europe.

Q: Do we expect commodities like copper (FCX) and foodstuffs to go up as rates are cut?

A: I do. They’re big beneficiaries of falling rates, but more importantly, they’re even bigger beneficiaries of a stimulated Chinese economy, and that’s why we see these monster moves over the last two days.

Q: If you had to invest in one rideshare company, would it be Lyft (LYFT) or Uber (UBER)?

A: Uber—they have far superior management, they’ll be the first into robo-taxis, and they are constantly evolving their model, with Lyft always struggling to catch up.

Q: How will antitrust regulation affect the Magnificent Seven?

A: The bottom line is it will double the value of the Magnificent Seven. If these companies are broken up, the individual parts are worth far more than the whole companies, and we saw this when we broke up AT&T (T) 50 years ago, and the resulting seven companies within a year had a combined market value that vastly exceeded the original AT&T. I actually participated in that deal when I was at Morgan Stanley (since I am 6’4” I was asked to carry the ballots from one floor to another). Expect the same to happen with the Magnificent Seven. They will be worth double or triple more.

Q: If China has a falling population, how will a stimulus program help?

A: Well, it will fill in for the 600 million consumers who were never born as a result of the one-child policy. Not many others are talking about this besides me, but the fact is that the current economic weakness comes entirely from the one-child policy, and there is no way out of that, so they are going to have to keep stimulating again and again, much like the US did through the pandemic.

Q: If you can buy gold and silver on the UK market in sterling, does that make more sense for a UK resident?

A: Yes, it does, since your home currency is in sterling. You will actually get a double play or a “hockey stick effect” because not only is gold going up against the US dollar, but sterling (FXB) is going up against the US dollar, so you’ll get a multiplied effect relative to the pound. We used to play this all day long in Europe in the 1970s and 1980s, back when you had individual currencies to trade and the euro hadn’t been invented yet.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Fishing in the High Sierras

Mad Hedge Technology Letter

September 25, 2024

Fiat Lux

Featured Trade:

(FROM 85 to 2,000 AI DATA CENTERS)

(ORCL), (NVDA)

Mad Hedge Technology Letter

September 23, 2024

Fiat Lux

Featured Trade:

(BE CAUTIOUS ABOUT STOCKS TIED TO GIG WORK)

(UBER)

I do believe companies heavily involved with gig workers will not experience a boon in the stock price in the near future.

Consumers are tapped out and there is not much more pricing power they can pass on to manufacture higher profits in the short run.

There is a chance the tide will rise with all boats, but I would wait this one out in gig work stocks.

As a cultural phenomenon, the gig economy is here to stay until they get muscled out by technology.

Americans are used to the 24-hour on-demand goods and services offered by gig workers.

The number one expense line item for these tech companies is labor.

They are actively working to try and reduce the burden.

I believe they are holding out until the vaunted robotaxi is green-lighted.

This change will crater labor expense to a pittance with most of the labor costs flowing towards the managers and executives.

It is the holy grail of the tech industry and we are rapidly approaching this inflection point.

These companies have come a long way.

In 2010, the smartphone application offered a new competitor to the taxicab industry by linking a paying passenger with a private driver using his or her own car.

The largest services are still focused on transportation. Uber and Lyft dominate the on-demand ride business.

Massive retailers like Walmart and Amazon joined in with their own on-demand platforms: Spark Driver and Amazon Flex.

Gig workers are recruited with the situation of flexible hours to earn additional income. However, as independent contractors, gig workers are not entitled to traditional employment benefits like health insurance, and they must take on additional occupational risks, equipment costs, and tax burdens.

In a 2024 economic impact report, Flex, a federal lobbying association supported by DoorDash, Grubhub, HopSkipDrive, Instacart, Lyft, Shipt, and Uber, estimated there were about 7.3 million “active drivers and delivery partners on major rideshare and delivery platforms” in 2022.

A 2022 report published by the consultancy McKinsey & Co. surveyed workers and estimated as many as 58 million Americans, or 36 percent of the U.S. workforce, did some gig work that year.

In its Securities and Exchange Commission filings, Uber describes the classification of its drivers as “employees, workers, or quasi-employees” as an “operational risk” to its business. The same document details the various legal and political challenges involved in maintaining independent contractor status.

Uber’s latest quarterly filing, published in August, said that if drivers win the reclassification through legal means or the passage of new laws, the company would incur significant expenses for compensating drivers and would pass its elevated costs onto riders. Uber also argues reclassification would limit its ability to find workers due to a loss of flexibility.

Uber is smart at attempting to root out the labor expenses. If robotaxis are integrated into the business model, the stock would increase by 500%.

In the meanwhile, workers forget ahead hoping to procure more benefits from Uber.

Uber is hell-bent on avoiding the financial toll of paying full-time workers and will indefinitely try to pin the label of independent contractor on its workers.

This existential threat will end up in courtrooms and Uber has good enough lawyers to stall out the lawsuits.

All eyes are on Tesla and Elon Musk to give insight into what the future of gig work and autonomous transportation looks like.

Uber knows it cannot maintain the status quo and something must be done to cut labor costs.

If that does happen, the stock will quadruple in short time.

As for the short-term, buy big dips in Uber stock.

Global Market Comments

June 4, 2024

Fiat Lux

Featured Trade:

(The Mad June traders & Investors Summit is ON!)

(THE BIGGEST “TELL” IN THE MARKET RIGHT NOW),

(GOOGL), (FRC), (PINS), (WORK), (UBER),

(ADSK), (WDAY), (SNE), (NVDA), (MSFT)

I am constantly looking for “tells” in the market, little nuggets of information that no one else notices, but give me a huge trading advantage.

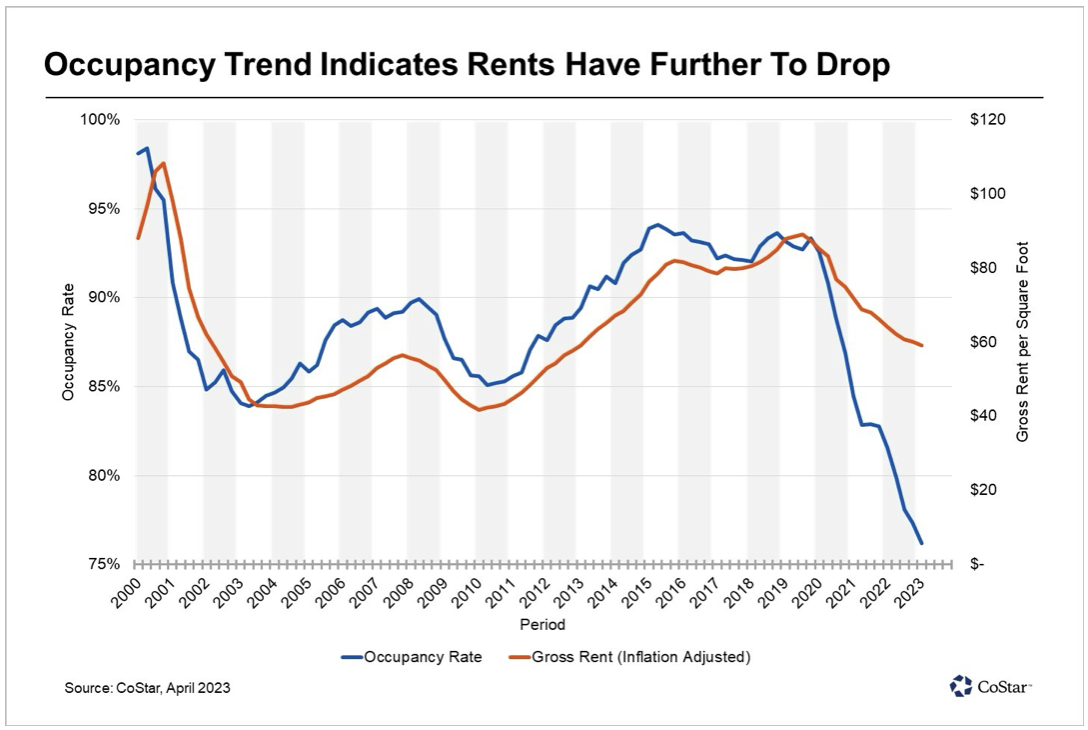

Well, there is a big one out there right now. The bottom feeders are pouring into San Francisco commercial real estate, taking advantage of valuations that sometimes reach negative numbers. Owners are walking away from buildings, mailing in the keys, and going into default rather than keeping up mortgage payments. What’s worse is refinancing at today’s lofty rates. That’s what you would expect with a 36% vacancy rate.

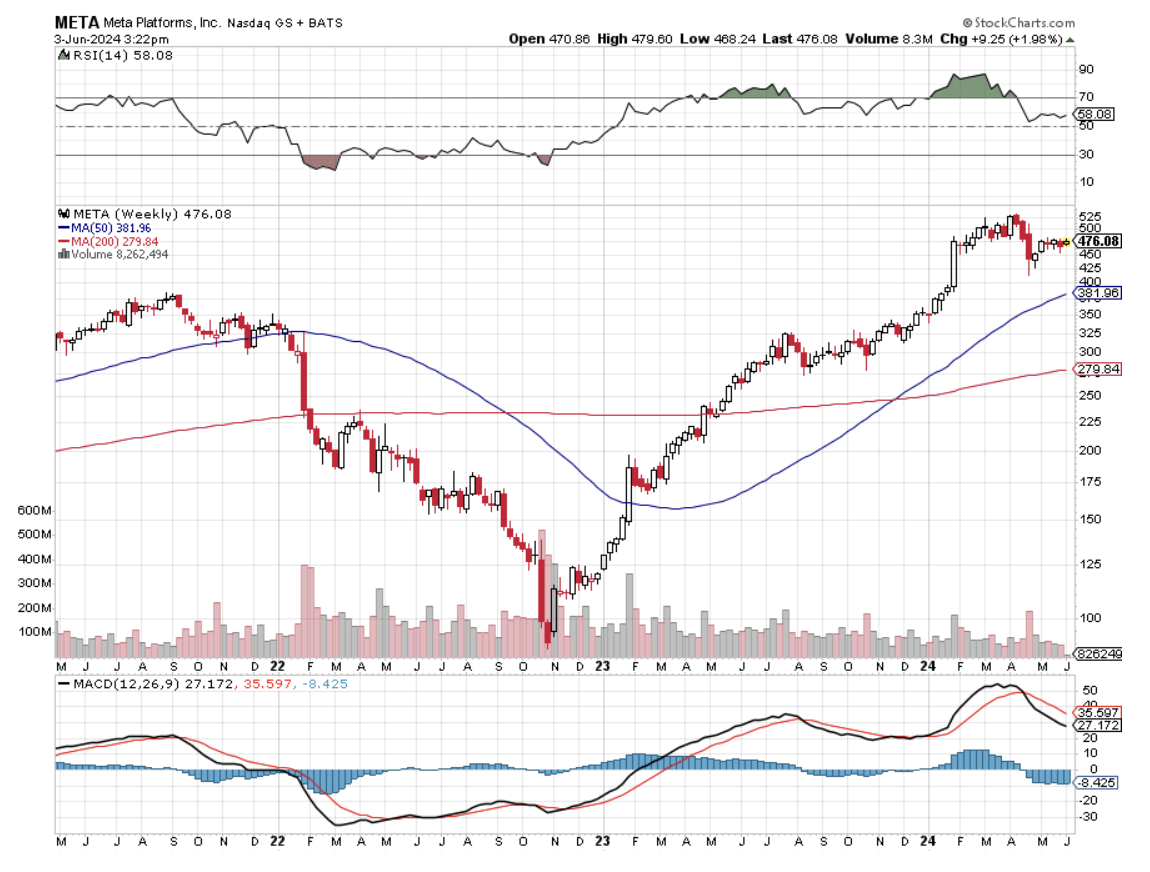

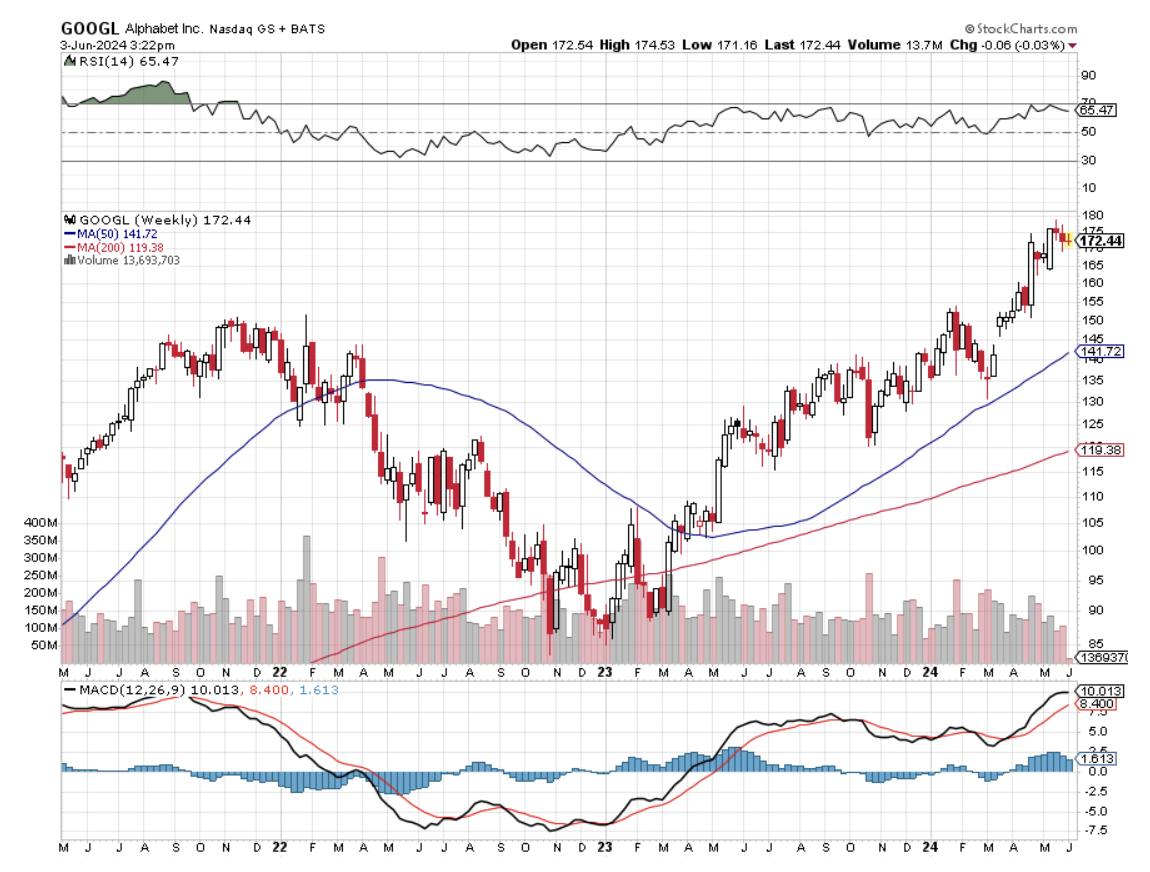

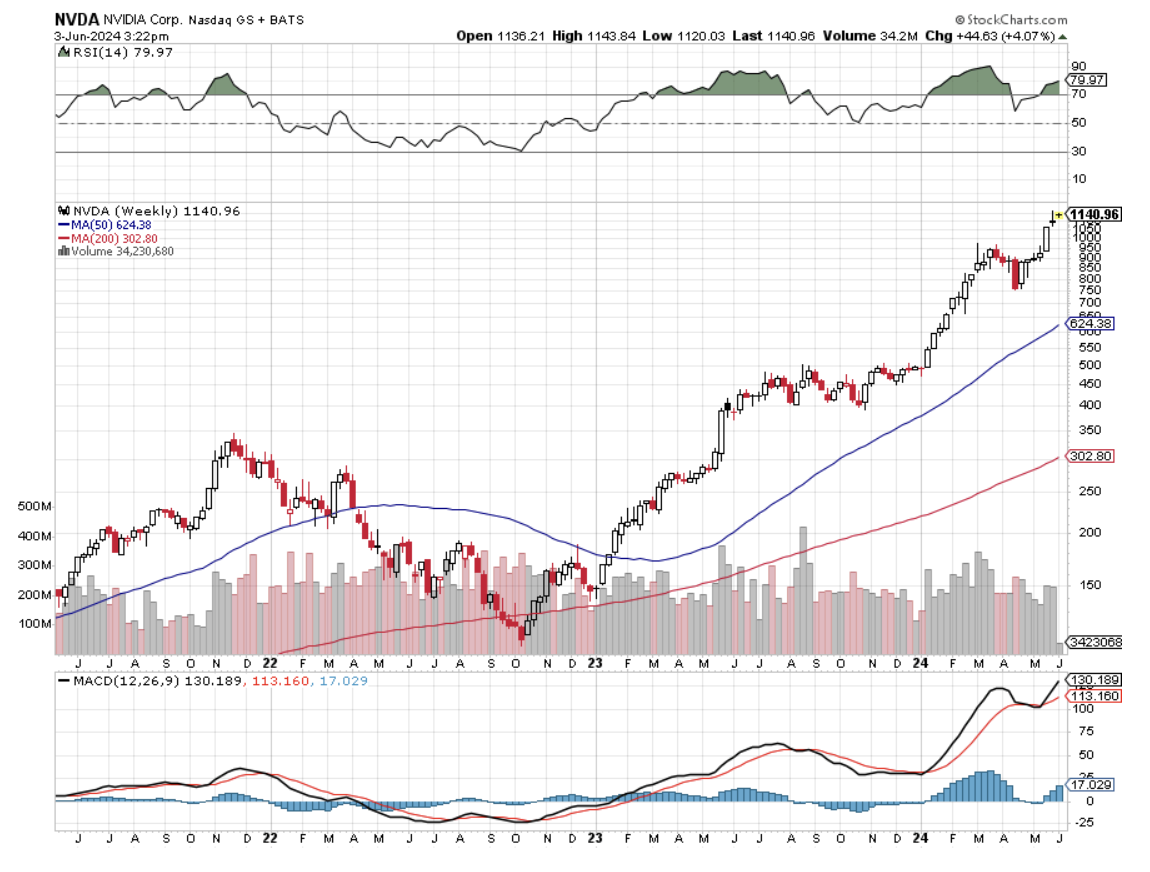

The message for you traders is loud and clear. You should be picking up the highest quality technology growth stocks on every substantial dip, such as Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta (META), and NVIDIA (NVDA). For they all know some things that you don’t. Their businesses are about to triple, if not quadruple over the coming decade thanks to AI. For every abandoned building out there are 200 new AI start-ups taking advantage of today’s bargain basement rates, and ALL of them use the services of the five companies above.

Technology stocks, which now account for an eye-popping 30% of stock market capitalization, will make up more than half of the market within ten years, much of that through stock price appreciation. And they are all racing to lock up the office space with which to do that….now.

San Francisco office rents reached a record pre-pandemic as the continued growth of tech — now turbocharged by nearly $100 billion in new capital raised in a series of initial public offerings — met a severe space crunch.

Asking rents rose to a staggering $84.16 per square foot annually for the newest and highest quality offices in the central business district, and citywide asking rents for such spaces, known as Class A, were up over 9% from the prior year. The citywide office vacancy rate was 5.5% in June, down from 7.4% a year ago.

In addition, local Bay Area home prices could get a turbocharger by the fall, when interest rates are expected to start falling.

San Francisco companies that have gone public continue to grow by leaps and bounds. Pinterest (PINS), Slack (WORK), and Uber (UBER) also signed office leases this year, with room for thousands of new employees.

Tech companies Autodesk (ADSK) and Glassdoor also signed deals at 50 Beale St. in the spring. In a sign of the city’s rapidly changing economy, old-line construction firm Bechtel and Blue Shield, the legacy health insurer, are both moving out of 50 Beale St. Sensor maker Samsara, software firm Workday (WDAY), and Sony’s (SNE) PlayStation video game division also expanded.

Globally, San Francisco has the seventh-highest rents in prime buildings. It’s still behind financial powerhouses Hong Kong, London, New York, Beijing, Tokyo, and New Delhi (San Francisco’s average office rents beat out New York.)

Only a handful of new office projects are being built, and future supply is further constrained by San Francisco’s Proposition M, which limits the amount of office space that can be approved each year. That is creating a steadily worsening structural shortage. Only two large office projects are under construction without tenant commitments.

Suddenly, it’s Not Crowded in San Francisco

Global Market Comments

February 20, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HOW THE CPI LIED),

(NVDA), (MSFT), (AMZN), (V), (PANW), (CCJ) (AAPL), (TSLA), (GOOGL), (MSFT), (AMZN), (META), (UBER), (UUP)