Mad Hedge Biotech & Healthcare Letter

April 20, 2021

Fiat Lux

FEATURED TRADE:

(A DEPENDABLE BUT UNDERVALUED HEALTHCARE STOCK)

(UNH), (ANTM), (CI), (HUM), (CNC), (CHNG)

Mad Hedge Biotech & Healthcare Letter

April 20, 2021

Fiat Lux

FEATURED TRADE:

(A DEPENDABLE BUT UNDERVALUED HEALTHCARE STOCK)

(UNH), (ANTM), (CI), (HUM), (CNC), (CHNG)

The ongoing seesaw fights in the stock market are causing too much drama that cunning investors can—and definitely should—steer clear from.

Instead of fretting over speculative and risky investments, it’s better off staying with tested and proven big-name companies that will remain solid buys for the years to come and continue to deliver positive results despite periods of uncertainty.

Among the huge names in the healthcare industry, United Health (UNH) is a strong contender that meets the criteria.

After almost a decade of delivering high returns, which shows off fast-rising earnings expectations, it’s interesting to see that the market has recently backed away from this blue-chip stock.

Nonetheless, the market’s skittishness offers an opening for investors looking to buy in the dip a company that pays dividends and promises to steadily boost your savings in the years to come.

Founded way back in 1974, UNH has become a top name in the healthcare industry, landing in seventh place on the Fortune 500 list.

To date, UNH has four main divisions handling its over 50 million members both in the US and across the globe: its private health insurance business UnitedHealthcare, its pharmacy benefits segment OptumRx, its healthcare services provider branch OptumHealth, and its analytics platform OptumInsight.

UNH has a market capitalization of $354 billion.

In comparison, the closest competitor is Anthem (ANTM), with $87.93 billion. In terms of market cap, the two are followed by Cigna (CI) with $85 billion, Humana (HUM) with $53.81 billion, and Centene (CNC) with $36.19 billion.

Amid the financial crisis brought about by the pandemic, UNH still reported a 6.2% jump in its revenue in 2020 to reach $257.1 billion.

The company’s most prominent growth driver is its Optum line, and UNH is making sure that this division continues to grow.

One of the most indicative moves towards that direction is UNH’s $7.8 billion acquisition announcement of technology and data analytics company Change Healthcare (CHNG), which should be completed by the second quarter of 2021.

In the agreement, UNH is offering Change Healthcare $25.75 for its shares, representing a premium of roughly 41% above the latter’s stock price.

UNH plans to merge Change Healthcare’s operation into OptumInsight, which currently handles hospital systems health plans, life sciences companies, and even governments.

In the first nine months of 2020 alone, OptumInsight generated over $1.9 billion, contributing to roughly 11% of UNH’s total bottom line.

The combination of these two will all but guarantee that UNH’s possession of the biggest and most powerful platform in the entire healthcare industry, with the acquisition projected to add approximately $470 million to the company’s adjusted earnings in 2022.

The decision to acquire Change Healthcare is part of the string of M&A deals executed by UNH to stay ahead of the game.

In 2019, it bought two companies to expand its operations: the DaVita Medical Group for $4.3 billion and Equian for $3.2 billion. Prior to these, UNH splurged on a $12.8 billion acquisition of Catamaran in 2015.

For 2021, UNH projects its earnings to increase, estimating its per-share profits to be somewhere between $16.90 and $17.40—and that estimate already took into consideration the headwinds involving COVID-19 that could still weigh on the company’s bottom line.

While this may appear optimistic, the truth is, generating strong results isn’t a novel accomplishment for UNH.

In the past three years, the company reported a net income of $10 billion or higher, with net margins recorded at 5% above its revenue.

Over the course of the last 12 months, UNH stock has climbed 24%, beating the S&P 500, which rose 18% during the same period. It also offers a decent dividend of 1.5%, which is admittedly slightly lower than the S&P 500 average at 1.6%.

Overall, UNH is a safe stock that you will not have to anxiously watch over and can hold in your portfolio for years.

More importantly, this company remains undervalued and still shows a lot of room for growth.

So if you’re a value investor looking with an interest in the insurance and healthcare services industry, then this market leader is a sustainable addition to your portfolio.

Mad Hedge Biotech & Healthcare Letter

January 7, 2021

Fiat Lux

FEATURED TRADE:

(LEFTOVER STOCKS RIPE FOR THE PICKING)

(ANTM), (UNH), (CVS), (TDOC)

One of the key things to remember in choosing companies to invest in is their long-term prospects. With these firmly in place, compounding can practically do most of the heavy lifting in the years to come.

Sure. It’s easy to be blinded by hot growth businesses these days—ones that seemingly promise unabated growth forever or those with cheap valuations but with no definitive growth prospects.

That is, you need to find businesses with not only promising prospects but are also trading at reasonable valuations. This requires a delicate balancing act.

With that balance in mind, one of the most obvious trends that fits the bill is to capitalize on the aging populations across the world.

As people age, it will drive higher demand for a myriad of healthcare services and the sector that responds most to this trend is the medical insurance segment.

Among the companies in this industry, I find Anthem (ANTM), UnitedHealth (UNH), and CVS Health (CVS) to bring the most bang for your buck.

While these companies are as fun to talk about as an actuarial table, they offer predictable cash flows and long-term prospects at reasonably priced valuations.

Let’s take Anthem for example.

From a valuation point of view, Anthem has traded hands at roughly 11.5 times its trailing earnings. More impressively, those earnings are estimated to increase by approximately 14.5% clip over the next five years.

That’s a reasonable, if not really cheap, price to pay for a company that’s well-positioned for what the future is expected to bring.

The aging population will also swell the ranks of UnitedHealth, being the largest health insurer in the country with over 14 million members in its Medicare programs.

Among the three, I find CVS the most intriguing.

The problem with this business is that people generally believe it’s only a pharmacy company. The truth is, it’s only one facet of CVS’ business, and, surprisingly, that’s its least profitable sector to date.

During the first six months of 2020, the total revenues of CVS went up 5% year over year to $132 billion.

Meanwhile, revenues of its pharmacy services sector grew by 2% compared to the same period in 2019 while its retails segment increased by 3%.

Notably, the biggest gainer is its healthcare benefits segment with a 6% jump year over year in revenues.

During these six months, CVS increased its medical memberships by 134,000 individuals to add Medicare and Medicaid insurance products.

On top of these, CVS reported that it had administered almost 2 million tests for COVID-19 in July—a number that continued to grow as the pandemic progressed throughout 2020.

Taking cue from the success of companies like Teladoc (TDOC), CVS also invested heavily in telehealth services.

In its second quarter earnings report, the company recorded a 15% increase in the number of its HealthHUB visits for regular members and Aetna cardholders.

This 2021, CVS plans to boost its digital health services by adding more segments like a behavioral support unit.

Overall, CVS has been performing better than its peers despite the pandemic thanks to its efforts on transforming itself into a more affordable healthcare benefits provider.

In fact, the company raked in $4.9 billion in profits in July 2020 alone—a whopping 48% jump from its performance in the previous year over the same period.

Most importantly, CVS is offering a dividend of $0.50 per share. Although the company hasn’t exactly raised this since 2017, it remains a preferable yield of 3.54%. This is way better than the average 1.8% payout from the S&P 500.

Despite all these, CVS is still one of the unpopular stocks among investors today.

All three companies have managed to still make a notable profit and fared relatively well despite the pandemic.

They are also underpriced, trading at roughly 14 times earnings or even less. On top of these, each pays dividends and offers an ROE of at least 11%.

Keep in mind that aging is an unstoppable and undeniable trend.

You’ve heard about the large number of Baby Boomers hitting retirement age, with the last of the roughly 72 million from that generation in the US alone turning 65 by 2030.

By 2034, older adults will outnumber children aged 18 and under. That has never happened in American history.

This isn’t a unique case in the US either.

The same is happening in Europe, where 1 of 5 people is already at least 65 years old. Asia is also expected to experience the same thing within the decade, particularly in South Korea and Singapore.

All three stocks, Anthem, UnitedHealth, and CVS offer reasonable opportunities at their current prices. They actually fit the textbook definition of value stocks. Hence, buying and holding these stocks is one of the most straightforward strategies over the next decade and beyond.

To put it simply, this only means one thing. For investors of these medical insurance stocks, time is literally on your side.

Although late to the party, giant biopharmaceutical company AbbVie (ABBV) is now going all-out on its coronavirus disease (COVID-19) treatment program.

The Illinois-based company, which has a market capitalization of $162.95 billion, aims to come up with a treatment that can block the SARS-CoV-2 coronavirus that causes COVID-19. The drug is currently dubbed 47D11.

AbbVie is working on this cure alongside Netherlands’ Erasmus Medical Center and Utrecht University as well as China’s bio-therapeutics developer Harbour BioMed.

It’s worth noting that AbbVie isn’t the first company to use this approach.

Earlier this year, Regeneron (REGN) announced a similar strategy to beat COVID-19. Its experimental cure, called REGN-COV2, is an antibody cocktail composed of two to three proteins working together to fight off the virus. The company plans to start clinical trials sometime this month.

Aside from AbbVie and Regeneron, Eli Lilly (LLY) is also utilizing the same technology.

In fact, the Indiana-based biotechnology leader already started dosing actual patients with COVID-19 with its experimental treatment, LY-CoV555.

Eli Lilly’s drug was actually developed using the antibodies collected from one of the first patients in the US to recover from the disease.

Using the same approach to find a COVID-19 cure isn’t the only thing Regeneron and AbbVie have in common, though.

To bulk up its oncology pipeline, AbbVie forged a partnership with Danish biotechnology company Genmab (GMAB) earlier this month.

Interestingly, Genmab is the same company behind the clinical progress of the bispecific antibody treatments of both Regeneron and Roche Holding (RHHBY).

AbbVie and Genmab agreed to collaborate on bispecific antibody development to come up with treatments that can target cancer cells and strengthen immune cells. The three drugs included in the deal are epcoritamab (DuoBody-CD3xCD20), DuoHexaBody-CD37, and DuoBody-CD3x5T4.

Aside from the three candidates already lined up, the two companies are also ironing out details on four additional cancer treatments.

The deal is estimated to be worth almost $4 billion, with AbbVie paying $750 million upfront.

On top of that, Genmab will also be entitled to get potential payments of up to $3.15 billion in milestone payments. The four potential cancer treatments could also entitle Genmab with an additional $2 billion.

Since bispecific antibodies are hailed as the “next-generation cancer therapy,” this market continues to attract big names in the industry.

So far, the list of companies working on bispecific antibodies includes Amgen (AMGN), Johnson & Johnson (JNJ), Novartis (NVS), GlaxoSmithKline (GSK), Merck (MRK), AstraZeneca (AZN), and Sanofi (SNY).

Aside from improving its oncology lineup, Abbvie has shown more creativity in diversifying its products.

Throughout the years, AbbVie had been considered as a strictly pharmaceutical company in the past. However, its recent purchase of Allergan set off a series of decisions that showcased the company’s plan to expand its portfolio.

With AbbVie’s revenue reaching $33.3 billion in 2019, several experts disagreed with the company’s decision to buy Allergan (AGN).

However, the move is estimated to add roughly $50 billion to the company’s annual revenue and help AbbVie’s bottom line.

One of the biggest products added to AbbVie’s portfolio is Botox, which has been long-regarded as Allergan’s prized cash cow.

In fact, this widely popular injectible raked in $1.02 billion in sales for Allergan in the fourth quarter of 2019 alone. Another promising product is the dermal filler Juvederm, which brought in $347.3 million in the same period.

Despite the excitement from the newly formed partnerships, a lot of investors remain apprehensive over AbbVie’s future.

These fears are rooted in the doomsday countdown for the company’s blockbuster rheumatoid arthritis drug Humira — and for good reason.

In its 2020 first quarter report, AbbVie recorded $8.6 billion in revenue, indicating a 10.1% jump year over year.

From this, Humira contributed nearly 58% despite the growing number of biosimilar rivals in Europe. In fact, Humira sales reached $4.7 billion, showing a 14.5% climb from the same period last year.

In 2019, experts predicted that Humira is poised to overtake Pfizer’s (PFE) Lipitor as the top-selling drug of all time by 2024.

AbbVie’s rheumatoid arthritis drug is estimated to reach a whopping $240 billion in sales in the next four years.

As expected, biosimilar competition, led by Amgen, has been licking their chops to get a piece of the action for years now, and they would do everything to dethrone AbbVie from its top spot in the autoimmune diseases sector.

Hence, AbbVie implemented two strategies to address this issue.

The first is forestalling the inevitable. In a recent court victory, AbbVie secured patent exclusivity for Humira until 2023.

Although this only leaves AbbVie with three short years to deal with the problem, it’s sufficient period for the company to execute its second plan: “Humira on steroids.”

Since Humira’s patent exclusivity has been a sore issue for AbbVie for years, the company decided to solve it by creating a stronger version of the drug.

The new antibody treatment, called ABBV-3373, is said to be more effective than Humira.

If all goes well in its clinical trials, then this “new Humira” can very well be AbbVie’s next megablockbuster and main moneymaker after 2023.

Humira isn’t the only big seller in AbbVie’s lineup.

Other blockbusters include cancer drug Imbruvica, which recorded $1.2 billion in revenue in the first quarter, up by 20.6% compared to the same period last year. Another cancer drug, Venclexta, is also performing well, bringing in $317 million in net revenue.

AbbVie has been boosting its next-generation treatments as well.

So far, two more Humira-like drugs stand out --severe plaque psoriasis medication Skyrizi and rheumatoid arthritis treatment Rinvoq.

Skyrizi’s annual sales are projected to grow from $1 billion to hit $4.4 billion by 2025, with the numbers going higher than $7.4 billion in the following years.

Rinvoq is expected to bring in $3.7 billion in sales by 2025 and increasing to reach $5.9 billion after that.

Right now, AbbVie appears to be oddly cheap as its shares are trading at only 9 times its expected earnings this year. This is possibly due to the anxiety over the loss of Humira’s patent exclusivity by 2023.

As AbbVie has shown in the past months, it has solid plans on how to deal with the impending loss. Its acquisition of Allergan, partnership with Genmab, and development of the “next Humira” all prove that claim.

Mad Hedge Biotech & Healthcare Letter

June 16, 2020

Fiat Lux

Featured Trade:

(THE ONE BRIGHT STAR IN THE HEALTHCARE INDUSTRY),

(ANTM), (TDOC), (CVS), (HUM), (CNC), (UNH)

The COVID-19 crisis has yanked the rug from under companies across all industries, and among the businesses that experienced a completely altered landscape these days is the health insurance industry. Imagine a business where sales increase fourfold overnight, but the customers can’t pay.

With the unemployment rate rising to historic levels since the pandemic hit, more people are dropping off commercial coverage rolls. Visits to the doctors and other elective procedures have been postponed indefinitely. Even political talks on healthcare reforms appear to be tabled until 2021.

Overnight, some doctors at country hospitals have seen workloads double and the suicide rate soar, while those in private practice are essentially unemployed.

While healthcare stocks are understandably struggling to survive, there are standouts that managed to take the blow without crumbling to ruins.

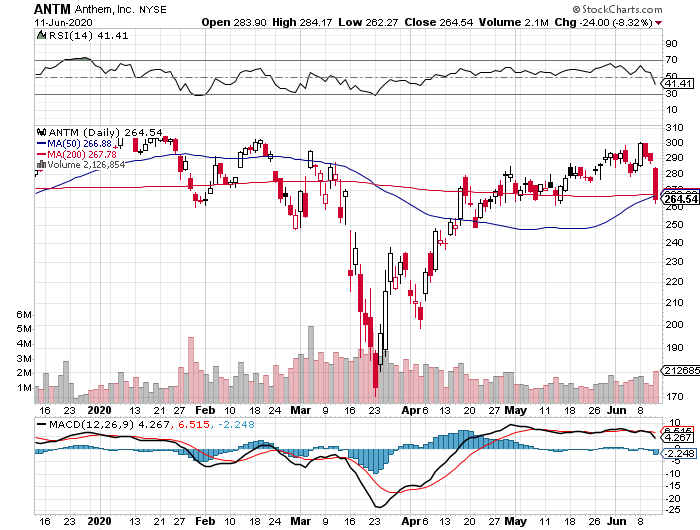

One of them is Anthem (ANTM).

With a market capitalization of $75.78 billion, Anthem is one of the biggest health insurers in the United States today.

Recently, the company wielded its power to offer $2.5 billion worth of premium credits as a form of financial assistance to its members during the pandemic.

This comes in the form of cost-share waivers, extensions for their virtual care coverage, and even assistance for struggling employers to help in maintaining the healthcare of their own employees.

While a lot of companies have been rapidly downgrading 2020 guidance due to the pandemic, Anthem updated its 2020 forecasts to reflect an increase in its adjusted net income from $19.44 per share to an eye-popping $22.30.

This indicates that Anthem has extra bandwidth for growth primarily thanks to its stable revenue stream, increasing membership, and solid earnings.

In its first quarter report for 2020, Anthem’s operating revenues jumped by 20.7% year over year to reach $29.4 billion, with profits from its IngenioRx launch.

As for its net income in the said period, Anthem raked in $1.52 billion or roughly $5.94 per share compared to $5.91 per share in 2019.

Anthem even increased its dividend by 19% in January.

However, it’s Anthem’s cash flow that continues to impress. From 2019 up until the first quarter of this year, Anthem’s cash flow surged by 58% year over year.

One of the main factors that boost the growth of a health insurance company is membership, and Anthem managed to tick off that box as well in the first quarter.

Anthem’s medical enrollment climbed to 42.1 million members, showing off a 3.2% increase year over year. With backing from government business enrollment as well as commercial and specialty businesses, this number is expected to climb higher this year.

Even Anthem’s inorganic growth ventures promise great results, with acquisitions and collaborations continuously boosting the Medicare Advantage growth of the company.

A good example is its acquisition of the Medicaid members in Missouri and Nebraska via WellCare Health at the beginning of 2020. This led to 849,000 lives added to its government business enrollment since 2019.

Meanwhile, its acquisition of AmeriBen added 452,000 members to its commercial and specialty business sector.

Anthem’s takeover of Beacon Health, which is the biggest independent behavioral health firm in the US, serves to further strengthen its position in this sector. This move added roughly 300,000 Medicaid members under Anthem’s coverage.

In terms of adapting to the needs of its members during the pandemic, Anthem is making more aggressive moves to promote its telehealth services.

Although this sector is currently widely associated with Teladoc Health (TDOC), which has a market capitalization of $12.93 billion, the rest of the league is catching up quick.

Since the average cost per telehealth session is roughly $100 less compared to fees paid in visits to the doctor’s office, this is definitely a platform-managed care providers are looking into.

According to Anthem, its telehealth app recorded over 170,000 new downloads since the COVID-19 crisis started.

It also reported a 250% surge in the demand for its virtual care services.

Anthem isn’t the only health insurer joining the telehealth fray. CVS Health (CVS), Humana (HUM), Centene (CNC), and even industry leader UnitedHealth Group (UNH) has been looking into the service.

In this period of uncertainty, choosing a stable company with a robust outlook and sold at a reasonable price is always a wise investment.

With Anthem’s profits projected to grow by roughly 47% over the next years, this company’s future offers security to its investors. Its impressive cash flow also plays a significant role in its higher share valuation.

Mad Hedge Biotech & Healthcare Letter

June 11, 2020

Fiat Lux

Featured Trade:

(THE BIOTECH MERGER BOOM ACCELERATES)

(AZN), (GILD), (BMY), (ABBV), (AGN), (TAK), (CI), (SNY), (JNJ), (UNH), (RHHBY), (LLY)

Nothing can ever be absolutely shocking in the biotechnology and healthcare world.

I’ll admit though that the reports on AstraZeneca’s (AZN) interest in acquiring Gilead Sciences (GILD) surprised me.

The two companies touched base last month on a potential acquisition deal.

If this rumor turns into a reality, then we’re looking at what could be the biggest healthcare deal to date.

That’s saying something considering the massive mergers we’ve seen in the past years.

So far, the biggest biotechnology and healthcare deal is the $87.6 billion acquisition of Celgene (CELG) by Bristol-Myers Squibb (BMY) in 2019.

In the same year, AbbVie (ABBV) acquired Allergan (AGN) for a whopping $83.8 billion, making it the third biggest deal in the healthcare sector to date.

The year 2018 paved the way for two more massive deals in the form of Takeda’s (TAK) $81 billion acquisition of Shire, which ranks fourth overall, and Cigna’s (CI) $68.4 billion deal with Express Scripts (ESRX) in seventh place.

Fifth on the list is by Sanofi’s (SNY) $73.5 billion deal with Aventis in 2004.

Although it has been two decades since it happened, the $72.5 billion merger of Glaxo and SmithKline Beecham in 2000 still counts as one of the biggest deals in the industry. This agreement gave birth to GlaxoSmithKline (GSK).

Prior to Bristol-Myers Squibb and Celgene deal, it was Pfizer’s (PFE) $87.3 billion acquisition of Warner-Lambert in 1999 that topped the list.

AstraZeneca’s current market capitalization is roughly $140 billion. Meanwhile, Gilead Science’s market cap stands at approximately $96 billion.

With all these in mind, the AstraZeneca-Gilead Sciences merger is estimated to reach roughly $250 billion on top of the significant synergies expected throughout the years.

If these two health industry heavyweights merge, then their newly formed company would become the third biggest healthcare company in the world behind Johnson & Johnson (JNJ), which has a market cap of $384.55 billion, and UnitedHealth Group (UNH) with $293.85 billion.

Looking at this potential merger in the context of the coronavirus race, it’s safe to say that the combined efforts of AstraZeneca and Gilead would create a COVID-19 titan.

AstraZeneca’s partnership with the University of Oxford resulted in a COVID-19 vaccine candidate that was recently selected as one of the top five candidates worthy of US government support through Trump’s Operation Warp Speed program.

Meanwhile, Gilead’s antiviral medication Remdesivir has been constantly hailed as the standard of care for COVID-19 treatment since the pandemic broke.

The drug which was previously marketed as an HIV medication is now expected to generate $2 billion in sales as a COVID-19 treatment in 2020 alone.

In 2022, Remdesivir is estimated to rake in roughly $7.7 billion in sales. After that, the antiviral drug is projected to generate annual sales somewhere between $6 billion and $7 billion.

Although everything is hypothetical, let’s take a quick look at where each company stands at the moment outside their COVID-19 efforts.

AstraZeneca has been a consistent strong stock market performer throughout the years.

In the first quarter of 2020, sales improved in practically all of AstraZeneca’s territories. Although it has a diversified portfolio of drugs and a robust pipeline, the company’s hottest segment is its oncology business.

A good example of this is non-small cell lung cancer treatment Tagrisso, which is starting to live up to expectations as the next mega-blockbuster for AstraZeneca.

The cancer drug’s first quarter sales reached an impressive $982 million, showing off a 56% jump year over year.

This is promising considering that its competitors include Roche’s (RHHBY) Tarceva and Eli Lilly’s (LLY) Cyramza.

As for its 2020 revenue forecast, AstraZeneca is reported to rake in $25 billion, from which it will generate approximately $7.5 billion in operating profit.

On the other hand, Gilead also has an impressive portfolio that it can bring to the table.

In the first quarter of 2020, the company earned $5.47 billion in revenue compared to the $5.20 billion it generated in the same period last year.

Despite the decline in its hepatitis products from $790 million in the first quarter of 2019 to $729 in the same period of 2020, Gilead’s HIV line made up for the loss by bringing in over $4 billion in sales compared to the $3.6 billion it earned last year.

Not only that, some of Gilead’s other candidates are exciting.

For example, rheumatoid arthritis drug Filgotinib is expected to become another blockbuster and generate $5 billion in revenue annually.

Meanwhile, the anti-tumor treatment Magrolimab is estimated to rake in $3 billion in peak sales.

With the company’s older drugs still capable of generating strong revenue and its new candidates showing their potential for revenue expansion, Gilead can be assured of a continued cash flow well into the 2030s.

Regardless of whether this rumored mega-merger pushes through, both Gilead and AstraZeneca are attractive stocks worthy of their premium valuations.

Global Market Comments

March 5, 2020

Fiat Lux

SPECIAL MARKET BOTTOM ISSUE

Featured Trade:

(FRIDAY, APRIL 17 SAN FRANCISCO STRATEGY LUNCHEON),

(A LEAP PORTFOLIO TO BUY AT THE BOTTOM),

(TEN LONG-TERM BIOTECH & HEALTHCARE LEAPS TO BUY AT THE BOTTOM)

(UNH), (HUM), (AMGN), (BIIB), (JNJ), (PFE), (BMY)