Global Market Comments

October 26, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MIXED MESSAGES)

(SPY), (TLT), (UUP), (FCX)

Global Market Comments

October 26, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MIXED MESSAGES)

(SPY), (TLT), (UUP), (FCX)

It was definitely a week of mixed messages in the stock market.

Is Covid-19 going to disappear by itself shortly, or is it the worst thing since the black plague?

Are we going to get a $2 trillion stimulus package out of Washington, or not?

Are stocks too expensive, or still cheap?

We are being told the answers to these questions loud and clear, we just can’t hear them.

For this election looks to set all records on turnout. Every city in the country is seeing lines of voters snaking around the block waiting 2-8 hours. But which way are they voting? Are there hoards of hidden Biden voters coming out of the woodwork, or Trump ones? We won’t know the result for eight more days.

In the meantime, the markets bide their time.

Which raises one last question: how low can stocks fall over the next seven trading days?

In the meantime, some asset classes aren’t willing to sit on their hands any longer. Interest rates have started to rise, hitting a four-month high. This has knocked 15 points off of bond (TLT) prices. Yet, contrary to expectations, the US dollar is hugging a multiyear low (UUP), while commodity prices (FCX) soar.

All of this spell a record economic recovery in 2021. All that remains is for stock prices to play catch-up.

The word is that there is over $1 trillion sitting on the stock market ready to dive in the day after the election, possibly tacking on at least 10% to the major indexes by yearend. There could be one hell of a post-election celebration, no matter who wins.

Baby Boomers are unloading stocks to Gen Xers mostly, but Millennials as well. Of course, they have all the money, with a 53% ownership of all stocks, compared to 27% for Gen Xer’s and a mere 3% for Millennials. The Greatest Generation, born before 1946, have been shrinking their share ownership since 1990 and own only 17% of the total now. A coming jump in capital gains taxes will accelerate the process.

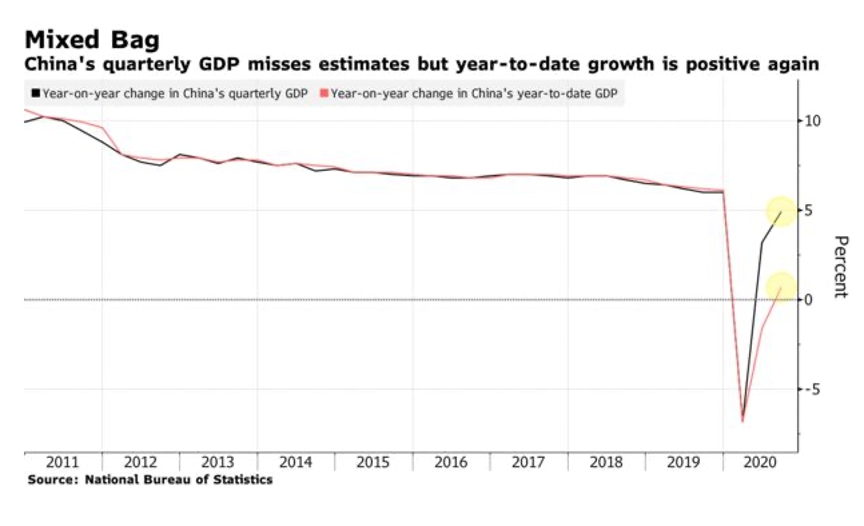

China’s Economy soared by 4.9%, in Q3 YOY with the pandemic in the rear-view mirror. First into the Coronavirus brings first out. Retail sales are through the roof and industrial production and business investment is accelerating.

Goldman Sachs says a Blue Wave will increase spending and boost the stock market. Total one-party control of the government eliminates the haggling that we are currently seeing in Washington and will deliver more Covid-19 aid faster. It should more than offset the ill effects of tax increases.

Beware of the coming Tax Loss Selling. A Biden win could unleash a torrent of selling as investors rush to beat an increase in the capital gains tax. That’s when you buy.

US Housing Permits blow the roof off at 1.553 million, up a staggering 22% YOY and a 13-year high. I wondered why I was suddenly getting a lot of flat tires on the freeway. They’re caused by nails and screws falling off the back up pickup trucks on the way to jobs. The long-term structural housing shortage continues. 30-year money at 2.75% makes a big difference.

Tesla generates a record profit for the fifth consecutive quarter in a row. The company is relying on its China factory to hit its 2020 target of 500,000 million units. Again, $397 million in regulatory credits drive earnings, payments from other carmakers who are lagging on electric car production. Gross margins rose 250 basis points to 23.5%. S&P 500 listing here we come! Next target $2,500!

Weekly Jobless Claims dropped to 787,000, better, but still horrible. California is finally reporting again.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Global Trading Dispatch hit a new all-time high last week by staying 100% in cash. I was just as grateful for having no positions on the up 600-point days as I was on the down 600-point days. Safe to say that I will be an increasingly more aggressive buyer on ever smaller dips and a seller on bigger rallies. October has now reached to a welcome 1.89% profit.

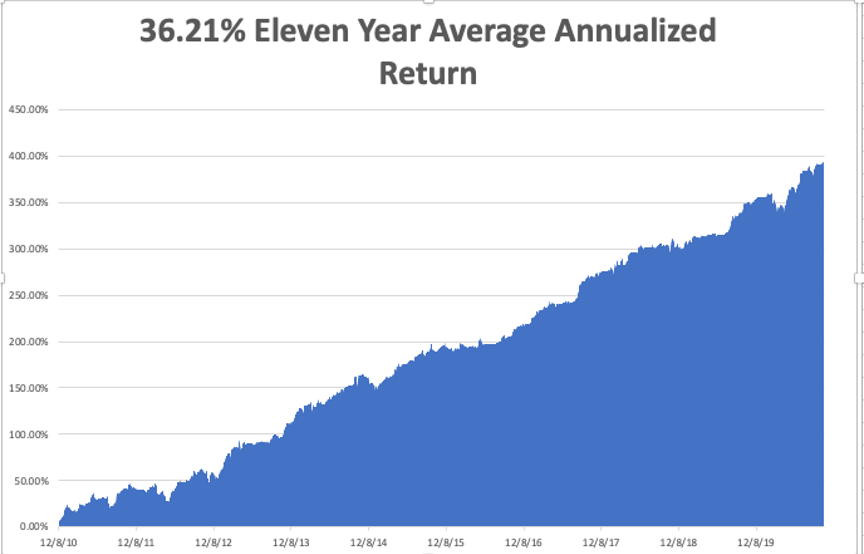

That keeps our 2020 year-to-date performance at a blistering +36.29%, versus a LOSS of -0.57% for the Dow Average. That takes my eleven year average annualized performance back to +36.21%. My 11 year total return stood at new all-time high at +392.30%. My trailing one year return appreciated to +42.86%.

The coming week will be a dull one on the data front. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, now at 225,239, which you can find here.

On Monday, October 26 at 10:00 AM EST, New Home Sales are published. Ely Lilly (LLY) and Merck (MRK) report earnings.

On Tuesday, October 27 at 9:00 AM EST, the S&P Case Shiller Home Price Index for August is released. Microsoft (MSFT) and Pfizer (PFE) report earnings.

On Wednesday, October 28, at 2:00 PM EST, the EIA Cushing Crude Oil Stocks are out. Boeing (BA) and Visa (V) report earnings.

On Thursday, October 29 at 8:30 AM EST, the Weekly Jobless Claims are announced. At the same time, we get the first read on Q3 GDP. Alphabet (GOOGL) and Amazon (AMZN) report earnings.

On Friday, October 30, at 8:30 AM, Personal Income for September is printed. Exxon (XOM) reports earnings. At 2:00 PM we learn the Baker-Hughes Rig Count.

As for me, I’ll be charging up every electronic device I have as the San Francisco Bay Area is expected to suffer a complete power blackout for the next three days. PG&E is shutting off the juice because winds are expected to reach 70 miles per hour and it hasn’t raised in six months.

I won’t be affected because I am totally off the grid with my own solar and battery network. You can easily find me because mine will be the only house in the mountains with the lights on.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 28, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or DID THE ELECTION OR COVID JUST HIT THE STOCK MARKET?),

(SPY), (TLT), (GLD), (TSLA), (UUP)

Did the election finally hit the stock market? It could have been both or neither.

Certainly, the passing of Supreme Court Justice Ruth Bader Ginsberg was worth 1,000 points, and maybe more. It may open the door to a period in politics that is uncertain at best or become violent at worst.

But the Coronavirus is making a comeback too. The US topped 7 million cases and 200,000 deaths, more than any other country in the world. The president’s new pandemic advisor, Scott Atlas, seems to be advocating a “herd immunity” approach. If so, 53% of the population will get the disease causing a total of 3 million deaths. The pandemic will continue for years.

New cases are spiking in Europe. The UK, which was on the verge of ordering workers back to their offices is now going back to a total shutdown. That augers for a second big wave in the US as kids go back to school and universities reopen.

With the S&P 500 now down 1% on the year, 2020 basically never happened. We saw a whole lot of volatility with no net movement. It makes my own 34.50% profit this year look stellar by comparison.

With the twin challenges of Covid-19 and the election lower lows for the market beckon. The one-year charts show that a “head and shoulders” top is in place for the (SPY), so my downside target at the 200-day moving average stands. That would be 3,074 for the (SPX) and $84 for Apple (AAPL).

There is a chance that the Fed could intervene in the stock market one more time right before the election if the markets resume the cascading falls of the spring. If that happens, buyers will return in hoards. My view is that this is but another dip in a long-term bull market that started in 2009 and may run all the way to 2030. You especially want to load the boat with Apple again.

However, the mystery of why technology stocks are so expensive remains. Let me take another shot at this.

From a technology point of view, we have just completely skipped the 2020s and are already in 2030. A year ago, would you have ever imagined that all of the country’s children would now be going to school online or that you’d be sending your business suits to the Good Will?

Stock markets have yet to price in the 2030 level of technology and profit, so the stocks will keep going up. Maybe we are already at 2023 or 2025 prices. I’ll let you know when I find out.

Volatility rocketed last week, and stocks collapsed. Any chance of further Covid-19 economic stimulus this year has just been demolished. If you were worried about the presidential election eroding confidence in the market before, now you have to be positively suicidal.

Any doubts about traders going into cash before the election have been vaporized. A 4-4 Supreme Court now makes an election outcome uncertain, no matter what the actual vote. Price that into your dividend discount model!

US Corona Deaths topped 200,000, weighing heavily on the economy and the election. There is no sign that the death rate is slowing, possibly reaching 400,000 by yearend. I went out to dinner last weekend and one-third of all businesses were boarded up, with no sign of reopening, ever.

Twelve IPOs to hit last week. This is in the wake of the Snowflake (SNOW) deal last week that tripled off its initial price talk. Apparently, there is an extreme shortage of high-growth large cap technology stocks and Silicon Valley is more than happy to meet that demand. Flooding the market like this ends up killing the goose that laid the golden eggs and is a common signal of market tops. Existing stock holdings have to be sold to buy new ones, taking markets south.

The economy slows as stimulus hopes fade as confirmed by last week’s economic data. US Consumer Sentiment dove in August, while Weekly Jobless Claims hover just below a Great Recessionary one million. The pandemic remains the dominant economic issue unless you live online.

The NASDAQ whale continues to sell, as Softbank (SFTBY) continues to unwind its massive technology long options positions. Last week, it was Adobe (ADBE), Salesforce (CRM), and Facebook (FB) that got hit. We won’t know if they made money on these for months, but they certainly put the final spike top in for the technology bubble.

The biggest debt increase in history occurred, with Federal government borrowing up an eye-popping 59% YOY. Sell every rally in the (TLT). It’s just a matter of time before a flood of new issuance destroys this market. We are sowing the seeds for the next financial crisis. The government was running record deficits BEFORE the pandemic even started.

Existing Home Sales soared in August, up 2.4% MOM to 6 million units, the hottest since 2006. Prices are up a huge 11.4% YOY. Homes over $1 million increased by 44% YOY as both work and school move home. Properties sit only 22 days on the market to sell, a record low.

Elon Musk promised a $25,000 car in three years, fully autonomous with long range and no maintenance for the life of the vehicle. The lifetime cost would be half of conventional gasoline-powered cars. That was the outcome of Battery Day in Fremont, CA, attended by hundreds of devotees safely enclosed in Teslas who honked instead of clap. It is all the result of dozens of revolutionary design and manufacturing improvements currently in the works, like moving from lithium to raw silicon for batteries. If so, General Motors (GM) and Ford (F) have had it.

A US dollar crash is imminent, says my old Morgan Stanley colleague Steven Roach. The double dip recession is here inviting even lower interest rates. The current account deficit soared to record highs in Q2. Buy the Aussie (FXA), Euro (FXE), and yen (FXY) on this dip.

Investors pull $25 billion from Equity funds last week as a new wave of nervousness hit the market. It’s the third largest weekly outflow in history. Everyone and his brother is trying to get out before the election. Pick your conspiracy theory as to what could go wrong.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch stayed level at just short of an all-time high this week. I dumped my last two positions at the Monday morning opening as I could see the 1,000-point drop coming from a mile off, going to a rare 100% cash position.

The risk/reward in the market now is terrible. I believe we have to test the 200-day moving averages before it is safe to go back in with the indexes and single stocks.

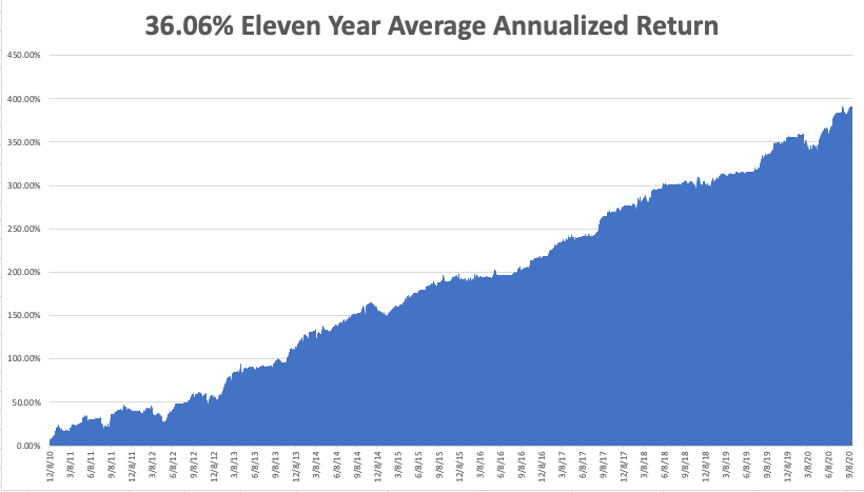

That takes our 2020 year-to-date back up to a blistering 34.50%, versus a loss of 7.00% for the Dow Average. September stands at a nosebleed 7.95%. That takes my eleven-year average annualized performance back to 36.06%. My 11-year total return returned to another new all-time high at 390.41%. My trailing one-year return popped back up to 54.09%.

The coming week is a big one for jobs data. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, now at 203,000, which you can find here.

On Monday, September 28 at 10:30 AM EST, the Dallas Fed Manufacturing Index is released.

On Tuesday, September 29 at 9:00 AM EST, the S&P Case Shiller National Home Price Index for July is announced.

On Wednesday, September 30, at 8:15 AM EST, the ADP Private Employment Report is printed. At 8:30 AM EST, the final figure for US Q2 GDP is disclosed. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out.

change.

On Thursday, October 1 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, October 2 at 8:30 AM EST, the all-important September Nonfarm Payroll Report is out. At 2:00 PM The Bakers Hughes Rig Count is released.

As for me, we have another superheating of the climate in store this weekend, with San Francisco Bay Area temperatures expected to top 100 degrees. The fires are out now, but high winds are coming so PG&E is expected to cut off electric power once again.

I’ll be fine with my solar and battery back-up. The Tesla power management software knows in advance when this is going to happen and automatically goes into maximum storage mode. But just to be safe and to keep the trade alerts coming, I am charging up the car and every battery I own.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 21, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE’S THE BLACK SWAN FOR 2020),

(SPY), (INDU), (TSLA), (JPM), (TLT), (C),

(V), (GLD), (AAPL), (AMZN), (UUP)

I had the pleasure of meeting Supreme Court Justice Ruth Bader Ginsberg only last year. She was funny, a great storyteller, and smart as a tack. If she disagreed with you, she pounced like a lion with a prescient one-liner.

She was also a goldmine of historical anecdotes about American history over the past 60 years, recalling incidents seen from her front-row seat as if they had happened yesterday.

She was also frail and rail-thin as if a faint breeze could knock her over at any time. Contracting cancer five times will do this to a person. Assistants helped her walk.

Her unexpected passing is now on the verge of creating a new financial crisis. Any chance of passing further stimulus in the US congress has just turned to ashes. The focus in Washington has turned entirely to the Supreme Court for the rest of 2020.

As a result, tens of thousands more small business will go under, millions of families will be thrown out on to the street, and the Great Depression will drag on. There is nothing left to spike the punch bowl with.

The Dow Average on Monday morning will open down 1,000 points, led by Tesla (TSLA) and the big technology stocks. US Treasury bonds (TLT) will rocket $5. The US dollar (UUP) will soar on a flight to safety bid.

Traders were already cutting positions and scaling back risk to duck the coming turmoil of the presidential election. We are also trying to front-run a yearend stock selloff prompted by a Biden rise in the capital gains tax from 21% to 40%.

That’s a bit of a moot point as 75% of stock ownership is owned by tax-exempt funds. The remaining 25% is most tied up in institutions that duck the tax by never selling or are embedded on corporate cross ownerships which never change.

Now we have uncertainty with a turbocharger, with gasoline poured in the air intake (pilot talk).

With Democrats refighting the battle of the Alamo, I doubt that Trump can ram through a third Supreme Court nomination. Remember how the last one went, for Brett Cavanaugh? Filibusters alone could delay proceeding by a month. These are NOT developments that make stocks go up.

If Trump succeeds, it may be a pyrrhic victory, costing Republicans at least five Senate seats, losing a majority, and increasing the margin of a presidential loss. If retired astronaut wins the Senate in Arizona on November 3, only two Republicans need to fold to make a Supreme Court nomination impossible.

It’s not like the stock market was in such great shape going into this, the biggest black swan of 2020. The market is being flooded with high priced initial public offerings, some 12 in the coming week alone. Apparently, there is an extreme shortage of high growth large-cap technology stocks and Silicon Valley is more than happy to meet that demand.

Cloud storage player Snowflake (SNOW) saw price talk at $70, an IPO of $120, and a first-day peak of $275. This created $70 billion in market value with the stroke of a key.

Of course, flooding the market like this ends up killing the goose thay laid the golden eggs and is a common signal of market tops. Existing stock holdings have to be sold to buy new ones, taking markets south.

We have already seen the 30-day and 50-day moving averages broken, and sights are clearing set on the 200-day. They would take us to a full top to bottom correction in the indexes of 20%. That would take the S&P 500 from $3,600 to $3,000, The Dow Average from $26,298 to $24,000, and Apple from $137 to $84.

If the Volatility Index (VIX) goes over $50, I’ll start sending out lists of very low risk, high return two-year options LEAPS like I did last time.

The Fed says no interest rate hike until 2023 and promises to heat up the economy even more than previously. The long-term average 2% inflation target I reaffirmed. Jay sees a net shrinkage of the US GDP this year ay 3.7%. Since governor Jay Powell promised to run the economy hot weeks ago, ten-year US treasury bonds have only eked out a paltry rise to 72 basis points.

The market isn’t buying it. It’s tough to beat ever hyper-accelerating technology that crushes prices. Still, I’ll keep selling short bond rallies because it’s just a matter of time before the government crushes the market with massive over-issuance. Sell every rally in the (TLT). The Fed put lives! Buy stocks on dips.

Election chaos is starting to price in, with the US dollar (UUP) getting an undeserved bid in a flight to safety trade and stock down 1,000 points from the week’s high. All sorts of Armageddon scenarios are making the rounds now and traders are pulling out of the market to protect hard-earned profits. For details watch the final season of House of Cards, where martial law is declared in Ohio to reverse an election outcome. No kidding!

Citigroup announced a surprise $900 million loss. I can’t wait for the excuse for this surprise, out-of-the-blue “operational error.' It’s most likely an expensive hack. It’s the kind of black swan that can hit you any time if you are a short-term trader. Long term investors should be buying the dip in (C).

China’s Retail Sales rise for the first time in 2020, up 0.5% in August. First into the pandemic, first out. Keeping Corona deaths to 4,000 was also a big help. It’s proof that economies CAN recover post-COVID-19. Buy China on dips (BABA), (BIDU). Stocks there will enjoy a huge post-election rally once the trade war winds down.

US Consumer Sentiment hits six-month high, up from a 75 estimate to 78.9. The University of Michigan report is proof that those who have money are spending it. Another green shoot. Didn’t help stocks today though.

Oil collapsed 15% on the dimming outlook for the global economy. Not even massive well shutdowns caused by this week’s hurricane could boost prices. Avoid all energy plays like the plague.

Morgan Stanley says the trading boom won’t last forever, says my former employer coming off of a record quarter. Too much of a good thing won’t last forever. Make hay while the sun shines.

The value rotation is on, with large scale selling of technology stocks and the chasing of banks and other recovery plays. It’s been a long time coming and could well persist until the end of the year. The option expiration at the close on Friday was exacerbating all moves, which is why I dumped my last two tech positions days prior. It’s too early to buy tech again on dips. Wait for a pre-election meltdown.

Copper hit a new four-year high as traders bet on an accelerating recovery in the global economy. My favorite, Freeport McMoRan, the world’s largest copper producer and a long time Mad Hedge subscriber is soaring, up 257% from the market lows. China, which is done with the Coronavirus and whose economy is recovering rapidly, has returned as a major buyer of the red metal. Keep buying (FCX) on dips.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch clocked its third blockbuster week in a row. I cashed in on my winnings with longs in (JPM), (TLT), (V), (GLD), (AAPL), and (AMZN), rang the cash register with shorts in (TLT) and (SPY), and booked a small loss in a long in (C). This took my cash position from 0% to 80% and I am looking to go to 100% in the coming week. The risk/reward in the market now is terrible.

Notice that I am shifting my longs away from tech and toward domestic recovery plays.

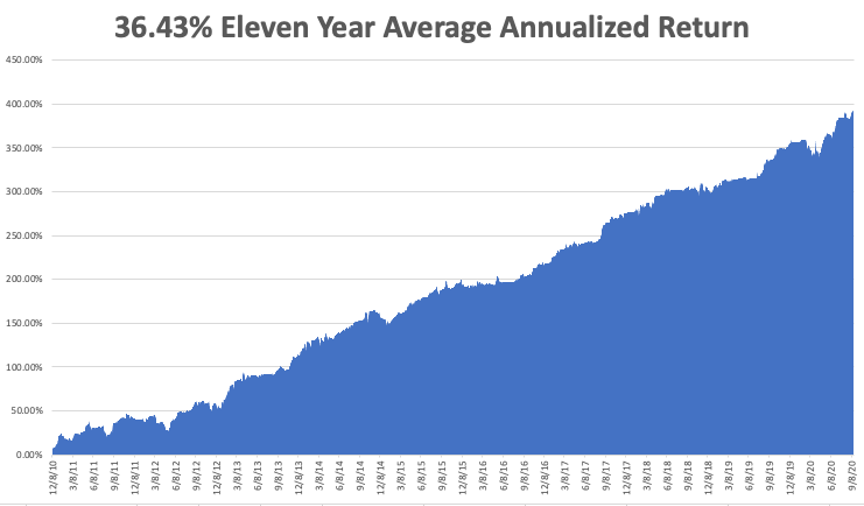

That takes our 2020 year-to-date back up to a blistering 35.74%, versus -2.93% for the Dow Average. September stands at a nosebleed 9.19%. That takes my eleven-year average annualized performance back to 36.43%. My 11-year total return is back for another new all-time high at 392.12%. My trailing one-year return popped back up to 54.87%.

The coming week is a big one for housing data. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, September 21 at 8:30 AM EST, the Chicago Fed National Activity Index is out.

On Tuesday, September 22 at 10:00 AM EST, Existing Home Sales for July are released.

On Wednesday, September 23 at 9:00 AM EST, the US Home Price Index for July is printed. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out.

change.

On Thursday, September 24 at 8:30 AM EST, the Weekly Jobless Claims are announced. At 10:00 AM the all-important Existing Home Sales for July are published.

On Friday, September 25, at 8:30 AM EST, US Durable Goods Sales for August are disclosed. At 2:00 PM The Bakers Hughes Rig Count is released.

As for me, I’ll climb up on the roof this weekend and clean the ash from my 59 solar panels. The fallout from the nearby raging forest fires has been so extreme that it has cut my solar output by 25%.

It’s not just me. Over a million homes in California have the same problem, putting a serious dent in the state’s electricity production.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

August 18, 2020

Fiat Lux

Featured Trade:

(HOW TO HEDGE YOUR CURRENCY RISK),

(FXA), (UUP),

Let’s say you absolutely love a stock but despise the currency of the country it comes from.

The United States comes to mind.

The US Federal Reserve has announced they don’t expect to raise interest rates for three years. The US government is running record budget deficits. Debt to GDP is now at the highest level since WWII.

That means the greenback is about to become the weakest currency in the world. Look at the ten-year chart below and you’ll see that a major double bottom for the Aussie may be taking place.

Most American technology stocks are likely to gain 30% or more over the next two years. However, it’s entirely possible that the US dollar declines by 30% or more against the Australian (FXA) and Canadian (FXC) dollars during the same period. Making 30% and then losing 30% leaves you with precisely zero profit.

There is a way to avoid this dilemma that would vex Solomon. Simply hedge out your currency risk. I’ll use the example of the Australian dollar, as we have recently had a large influx of new subscribers from the land down under.

Let’s say you want to buy AUS$100,000 worth of Apple (AAPL), the world’s most widely owned stock.

Since Apple is listed on the New York Stock Exchange, its shares are denominated in US dollars. When you buy Apple in Australia, your local broker will automatically buy the US dollars for your account to settle this trade in the US, taking out a small commission along the way. You are now long US dollars, thus creating a currency risk.

Getting rid of this currency risk is quite simple. You need to offset your US dollar long with a US dollar short of equal value. Long dollars/short dollars give the Australian investor a currency-neutral position. The US dollar can go to hell in a handbasket and you won’t care.

There are several financial instruments with which you can do this. Buying Invesco Currency Shares Australian Dollar Trust ETF (FXA) is the easiest. This ETF invests 100% of its assets in long Australian dollar/short US dollar futures and overnight cash positions.

I’ll do the math for you on the final hedged position assuming that the Australian dollar is worth 70 US cents.

BUY AUS$100,000 long US dollars X US$0.70 cents/dollar = US$70,000.

US$70,000/$210 per share for Apple = 333 Apple shares

BUY US$70,000/$70 (FXA) price = US$1,000 shares of the (FXA)

Thus, by owning AUS$100,000 shares of Apple shares and 1,000 shares of the (FXA) you have completely removed the currency risk in owning Apple. You have, in effect, turned Apple into an Australian dollar-denominated stock. Apple can rise, the US dollar will fall, and you will make twice as much money in Australian dollars.

There are a few problems with this precise trade. The liquidity in the (FXA) is not great, especially during US trading hours. Understandably, the bulk of Aussie liquidity takes place during Australian business hours.

There are other instruments with which you can hedge out the currency risk of Apple, or any other US dollar-denominated investment.

You can take out your own short dollar position in the futures market. You can ask your bank to create a short position in the US dollar in the cash market. Or, you can simply ask your broker to hedge out your US dollar currency risk, for which they will charge you another small commission.

Hedging out currency risk not only is free, the market will pay you to do it. That’s because Australian dollar overnight interest rates at 1.00% are lower than US dollar overnight interest rates at 2.50%. By shorting Aussie against the buck, you get to keep this 1.50% interest differential.

You don’t have to be Australian to want your Apple shares denominated in Australian dollars. In fact, hedge funds do this all day long. They pursue a strategy of keeping their long position in the world’s strongest securities (Apple), and their shorts positions in the world’s weakest securities (the US dollar). This, by the way, is also the strategy of the Mad Hedge Fund Trader. It’s called “global long/short macro.”

The better ones often make money on both sides of the equation, with the longs rising and the shorts falling. You can do the same in your own personal online trading platform.

I should urge a word of caution here. What happens if you hedge out your US dollar risk, and the dollar continues to appreciate? Then you will get none of the gains from that appreciation and will end up losing money in Australian dollars if Apple shares remain unchanged.

In the worst case, if both Apple and the Aussie could go down, this accelerates your losses. So, currency hedging can be a double-edged sword. Yes, this may be irrational given the fundamentals of the Aussie and Apple. But as any experienced long term trader will tell you, “Markets can remain irrational longer than you can remain liquid.”

Many thanks to John Maynard Keynes.

Global Market Comments

July 17, 2020

Fiat Lux

Featured Trade:

(JULY 15 BIWEEKLY STRATEGY WEBINAR Q&A),

(EEM), (GLD), (GDX), (NEM), (GOLD), (UUP), (FXA), (FXE), (FXY), (AMZN), (AAPL), (GOOGL), (FB), (BIDU), (TLT), (TBT), (IBB), (ROM)

Below please find subscribers’ Q&A for the July 15 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Lake Tahoe, NV with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Do you expect foreign equities to begin to outperform US equities sometime soon?

A: I expect them to outperform imminently simply because Europe did their shutdown properly, a total shutdown, and got rid of the virus, so their economy and schools are opening. We did a partial shutdown, some states did not shut down at all, and as a result, the epidemic is on fire here, and our shutdown will have to last an extra six months to a year. So that means you’ll probably want to be rotating out of US stocks and into emerging stocks, and the (EEM) is the ETF to go with there.

Q: Would you buy gold LEAPS at this point?

A: Normally, I say only buy LEAPS on capitulation selloffs like we had in March. We actually put out 25 LEAP recommendations on the long side in tech and biotech in March and they all proved spectacular winners. However, at this point, gold is just short of an all-time high; if you break the high you could get a $500 or $1,000 move very quickly to the upside. If you want to do LEAPS, I would go out one year, I would go fairly close to the money, something like a $200-$210 LEAP in the (GLD) ETF. Your much bigger bang, by the way, would be to do LEAPS on the individual stocks; go 10% or 20% out of the money, you might make 100%-200% on those and the stocks to do there would be Newmont Mining (NEM) and Barrick Gold (GOLD).

Q: Would the US or any other country consider backing their currency with gold?

A: Absolutely not. We went off the gold standard in 1972 for a reason. That’s because they're not making it anymore; there isn't enough gold to support growth in a global economy. On the other hand, a supply of paper is unlimited, and that's why we've had such terrific economic growth since we’ve gone off the gold standard.

Q: I’m seeing some really great deals in energy. Should I get involved?

A: Absolutely not. Don’t confuse “gone down a lot” with “cheap.” We think the oil business is long term going out of business. It can't compete with alternatives and electric cars; the economics for investing in a non-scalable energy form just are not there. It’s like asking an analog adding machine to compete with a computer.

Q: Is it too late to sell the US dollar or the Invesco DB US Dollar Index Bullish Fund ETF (UUP)?

A: No, we’re only in the very early stages of the collapse of the US dollar, so you want to be buying all of the nondollar ETFs like the Australian dollar (FXA), the euro (FXE), and the Japanese yen (FXY). Massive over issuance of currency will destroy its value, that’s one of the seminal lessons of currency markets. The US is not immune to that.

Q: Biotech is getting overheated here—should I buy the rumor, sell the news?

A: We’re also just in the opening stages of the biotech golden age. Even if they cure corona tomorrow, there are another 100 diseases they will cure over the next 10 years using all of the new advanced technology that has just been developed, like gene editing, monoclonal antibodies, and quantum computers. It’s another reason to subscribe to the Mad Hedge Biotech and Healthcare Letter for $1,500 a year (click here).

Q: I see Bill Gross is bullish on value stocks—would you go with that view?

A: No, leave the value stocks for Bill Gross. He's semi-retired and hasn’t been as good on the stock market lately as he used to be, as much as he is a dear friend. This is a chasing-a-winner type market. I would wait for value stocks. You could die a long horrible death by the time value stocks turn around so I would avoid them. Go for earnings growth, that’s the only thing that counts in the future.

Q: What would you recommend as a portfolio starter?

A: I would recommend 100% cash. I know you don’t want to hear that you should keep cash if you just bought an expensive trade alert service, but the fact is the risk now is the highest it’s been in years. I only add new trade at market sweet spots, and you don’t get those every day of the year. I will send you an alert if I see a low-risk high-return trade. Wait for the summer correction—that will set up another bet-the-ranch opportunity. Don’t worry about trade alerts, we’ll be doing about 400 of them this year, but they do tend to come in bunches at market bottoms and market tops.

Q: Do American companies have much of a chance against Chinese tech?

A: The US has an overwhelming lead, which will probably increase at an exponential rate. I think the threat of Chinese tech is vastly overstated by the administration. They needed an enemy to protect us from to stick around. The reality is that the US is so far ahead it’s unbelievable; that’s the reason they steal our technology. And they only have leads in very specific areas, such as surveillance of large populations. I wouldn’t worry too much about tech—if the Chinese really had a lead on tech, would Amazon (AMZN), Apple (AAPL), Alphabet (GOOGL), Facebook (FB) all be going to new highs every day, while Baidu (BIDU) lagged?

Q: Should we close out the Regeneron call spread?

A: At this point, we’re so far in the money I would just wait two more days and it will expire at its maximum $10 value, and you can avoid all the fees. You’ll end up making $1,600 or 16.28% 15 trading days.

Q: Presidential candidate Joe Biden has just had a huge surge in the polls in battleground states. Will he be damaging to the market?

A: No, ever since he started his rise in the polls, the stock market has been rising almost every day, and that’s even after announcing in advance that he’s going to raise corporate taxes from 21% to 28%. He’s also going to eliminate the carried interest, which should have been eliminated a long time ago. I imagine there will be some super punitive Roosevelt style 90% tax on net taxable income over a billion dollars—a real billionaire’s punishment tax, as they’ve basically made all the money for the last 30 years. The stock market is voting with confidence for the future Biden government, who am I to disagree? The market is always right.

Q: Will gold hit a new high?

A: Yes, I think we will have a new high in a couple of weeks. That's why I said it’s a rare case when you actually buy LEAPS in a rising market, especially if you go one or two years out. Guess where gold will be in two years? My bet is $3,000, so a $200/$210 LEAP in the (GLD) could bring in a 1,000% return, The overwhelming fundamentals are in favor of gold. I'll keep hammering away at that in the newsletter.

Q: I only trade stocks; how can I take advantage of your recommendations?

A: First of all, buy the stocks. Second, you can buy stocks on margin, which gives you double exposure. Third, there are many 2X ETFs on the stocks or sectors we recommend, like the (TBT), which you can also trade in a stock account. For example, for biotech, you can get your exposure there through the (IBB), and through tech, you can buy the 2X (ROM); but I wouldn’t buy it today because it is too high. In fact, only about 25% of our followers do options, the rest trade stocks or use it to manage their own long-term portfolios.

Q: Will we hit 0% yielding US Treasuries (TLT)?

A: Probably not, that move is behind us. We got down to a 31 basis points yield at the lows. Now, massive oversupply from the US government will be the primary factor dictating Treasury prices, and that means going down a lot.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader