Mad Hedge Technology Letter

June 7, 2018

Fiat Lux

Featured Trade:

(THE NEW TECHNOLOGY PLAY YOU'VE NEVER HEARD OF),

(GM), (UBER), (WMT), (GOOGL)

Mad Hedge Technology Letter

June 7, 2018

Fiat Lux

Featured Trade:

(THE NEW TECHNOLOGY PLAY YOU'VE NEVER HEARD OF),

(GM), (UBER), (WMT), (GOOGL)

Welcome to the new cutting-edge high-tech play - General Motors (GM).

The tectonic shifts permeating through the tech landscape seem like there is no end.

Another blockbuster announcement hit the airwaves melding together a brand-new partnership between SoftBank and GM's self-driving unit Cruise.

SoftBank invested an eye-popping $2.25 billion into Cruise for a 19.6% stake, adding to its scintillating arsenal of big data assets focusing on transportation including Uber, India's Ola, China's DiDi, and Southeast Asia's Grab.

GM disclosed it will divvy up a further $1.1 billion into the deal.

The Mad Hedge Technology Letter has been an astute follower of the autonomous driving technology race because the technology will be the next proprietary technology to change the world, creating enormous windfalls for the few involved.

The timeline commences later this year, when Waymo, a subsidiary of Alphabet (GOOGL), rolls out a robo-taxi commercial service.

General Motors is right on Waymo's heels rolling out its own commercial service "sometime in 2019."

This momentous investment by SoftBank solidifies (GM) as the No. 2 industry player going forward.

This is a huge victory.

The historic shift symbolizes the next gap up in the technology movement.

Tech stocks have been on a tear of late leaving other equities in the dust.

Waymo was the first mover and confidently never relinquished the top-dog position while avoiding any big disasters along the way.

The unparalleled success of Waymo's self-driving unit has led analysts to put a valuation figure ranging anywhere from $75 billion to $125 billion.

GM paid a measly $1 billion for Cruise in 2016, which is peanuts in today's thriving tech landscape.

Analysts estimated the valuation of Cruise at $4 billion just before the SoftBank investment. The almost 20% stake for $2.25 billion puts the new valuation number over $11 billion, three times more than analysts initially speculated.

Tech acquisitions have exploded in 2018 and show no signs of slowing down.

The hallmarks of Waymo's operation hinge on safety-first initiatives, which went a long way to upholding its industry leader position.

The safety-second attitude led Uber to attempt to short circuit its way to the top from a position of weakness to ill effect.

Uber's technology failed, and the result of the Phoenix, Arizona, casualty was a suspended operation.

Game over.

To stick the blade cleanly through the back, Uber CEO Dara Khosrowshahi revealed that talks are ongoing between Waymo and Uber to add Waymo's technology to Uber's broker app service.

This revelation is interesting considering Uber infuriated Waymo. It means Uber will effectively recede itself from competing with Waymo in self-driving technology.

The company doesn't need to anymore and it burns too much cash.

The protracted court ruling revealed Uber had stolen trade secrets using poached Waymo engineers.

This time, it really is the nail in the coffin for Uber's self-driving technology.

It will change strategy and refine its core app that made them famous in the first place.

The SoftBank investment into Cruise has clear synergies with Uber.

If Waymo refuses to go into bed with Uber, the natural logical step would be for the GM Cruise technology to be integrated with the Uber platform since they are both SoftBank investments.

SoftBank's management will clearly push for this arrangement. It makes no sense to use the Lyft platform with the GM Cruise division.

The tie up with GM Cruise was the catalyst for Uber seeking "talks" with Waymo, knowing very well if talks failed, a backup plan was hatched and would be able to partner up with Cruise's technology.

This is the luxury Uber has now since it is part of the SoftBank umbrella along with the GM Cruise division.

This nullifies the existential threat Uber was anxious about as it is guaranteed a certain slice of the pie leading to material future revenue stream post IPO.

The SoftBank investment is a stamp of approval for the quality of GM self-driving technology.

SoftBank only invests in the most innovative firms.

The conundrum with legacy car companies is that the bulk of revenue is reliant on selling combustion-engine cars that will soon become obsolete.

Any large commitment to R&D, unfocused on its main profits levers, hurt margins. Investors do not buy American car manufacturers that operate at a loss.

Therefore, legacy companies are penalized for spending on new businesses that could be hit or miss.

They stick with their bread and butter through thick and thin because that is what investors expect them to do. This was why Walmart (WMT) sold off when it acquired a stake in Flipkart.

A certain type of Walmart investor would be aghast at this unexpected new direction and amount of dollars drained.

In support of Walmart, CEO Doug McMillon has been positively vocal about the pivot to tech and e-commerce.

It should not be a surprise.

Old technology gets swept into the dustbin of history. Examples are legion.

Let me explain why.

The shift from horse-drawn carriages to the automobile was an equally jaw-dropping development at the time.

Not all horse-drawn carriage manufacturers were able to make the massive leap from creating simple horse-carriage passenger vehicles to automotive vehicles with combustion engines.

When Abraham Lincoln was transported to the Ford Theatre the night of his assassination, he was rolling in a Studebaker horse-drawn carriage.

Studebaker, which was established in 1852 with $68 of capital and a tool belt, was the only top-notch horse-drawn carriage manufacturer to make the gigantic shift from horse-drawn carriage builder to automotive producer.

The other players shriveled up and waved the white flag.

Studebaker actually manufactured both horse-drawn carriages and cars from 1902-1920.

The company mutated again during World War II making military vehicles, M29, M29C, and engines for B-17 bombers.

Financial mismanagement ruined the company. In 1963 it shuttered its South Bend, Indiana, factory and then went out of business by 1967, missing out on a chance to take on Uber and Waymo by about 55 years.

Such are the annals of history.

(GM) is the first American legacy car company to make the complicated transition from traditional American car producer to self-driving technology player.

And it could be the only one.

The deal will raise the price range for the Uber IPO planned for 2019. The (GM) cruise division will report financials separately from the rest of the (GM) balance sheet, which could be the precursor to spinning it out as its own company creating more shareholder value.

No matter how you dice this up, (GM) is the real deal. Investors voted with their feet causing the stock to explode skyward closing 13% higher on the news of the investment.

Buy (GM) on the next sell-off instead of chasing the bolted stallion out of the starting gate.

_________________________________________________________________________________________________

Quote of the Day

"Indian software engineers are the best in the world; even in Silicon Valley, the best software engineers are Indians," - said CEO of Softbank Masayoshi Son

Mad Hedge Technology Letter

June 4, 2018

Fiat Lux

Featured Trade:

(THE INNOVATOR'S DILEMMA),

(UBER), (WMT), (SNAP), (MSFT), (GOOGL), (AAPL), (GM), (IBM)

I must confess, innovation can't be taught.

You are innovative, or you aren't. Don't pretend otherwise.

Innovation drives companies to outperform.

The economic environment becomes more cutthroat by the day rendering complacent companies obsolete.

Top-quality innovation leading to outstanding entrepreneurship is a well-traversed theme transcending industries across the American economic landscape.

The reservoir of innovation in 2018 is primarily flowing from one narrow source - the tech sector.

This is the primary motive for many adjacent industries to incorporate tech expertise into existing and commonly ancient legacy systems.

Tech promises laggards a ride atop the gravy chain.

In many instances, these companies are grappling with existential threats from all directions.

The best example is Walmart (WMT), which effectively mutated into the next FANG with its majority stake in Indian e-commerce juggernaut Flipkart. This deal followed its purchase of Jet.com in 2016, which was its first foothold in the e-commerce world.

Traditional companies are becoming tech companies because of the ability to innovate all leads through the fingertips of talented coders.

When all roads lead to Rome, you will have to go through Rome.

The hunger for innovation has had major implications to the financial side of technology.

The story picks up from a recent report disclosing the 2017 remuneration of co-founder and CEO of Instagram competitor Snapchat (SNAP) Evan Spiegel.

The $637.8 million he received in 2017 was the third-highest annual compensation ever to be collected by a CEO.

Snapchat has tanked following its 2017 IPO and the main reason is Facebook is stealing its lunch and leaving Snap the crumbs on which to nibble.

Instagram, using a cunning strategy of cloning Snap's best features, single-handedly bludgeoned Snap's share price cutting it by half after the successfully launched IPO.

Snap has been an unequivocal sell on the rallies stock since the inception of the Mad Hedge Technology Letter and the disastrous redesign did no favors either.

My first risk off recommendation was Snapchat and at the time it was trading at $19. To revisit the story, please click here.

Microsoft (MSFT) is a great stock because it posts accelerated revenue and earnings, while Snapchat is a terrible company because it produces accelerated losses and lousy user growth.

A company almost 100 times smaller than Microsoft should not be struggling to grow.

It's a failure of epic proportions.

Small companies expand briskly because the law of numbers is leveraged in their favor and the tiniest bump of additional business has a larger effect on the bottom line.

As it stands, Snapchat lost $373 million in 2015, and followed that up with a disastrous $514 million loss in 2016, and a gigantic $3.45 billion loss in 2017.

Losses accelerated by 800% but annual revenue only doubled last year.

It was no shocker that the poor relative performance resulted in the sacking of 100 Snapchat developers.

Smart people would assume an annual salary of this magnitude (Spiegel's) would be the result of excellent performance.

Why else would a CEO get a lavish payout?

I'll explain.

The demand for tech knows no bounds.

In this environment, venture capitalists will pay up for brilliant ideas.

The problem is that brilliant ideas don't grow on trees.

The few cutting-edge ideas have stacks of money thrown at them.

In this sellers' market, founders can cherry-pick the best financing deal that will enrich them the quickest and empower them the most.

Multiple offers have become the norm just as with the Silicon Valley housing market.

The consequences are the premium for these brilliant ideas keeps rising and investors keep paying higher prices without a second thought.

Therefore, founders and CEOs are opting for the financial packages that offer them bulletproof voting shares, allowing the innovators to control operations to the very last detail.

The founders are responsible for leading innovation, and investors are offering glorious pay terms for this innovation because it can't be substituted. Low-quality tech has less of a premium because the technology can easily be rebranded and substituted.

Technology from the ground up is slowly being automated away leaving runaway valuations the norm.

Giving the keys to the Ferrari makes sense as tech companies formulate long-term strategies based on scale. And securing job security without the threat of an activist takeover offers peace of mind for CEOs who are focused on the daily grind.

Knowing their baby won't get stolen from the carriage goes a long way in tech land.

Venture capitalists are reticent about following through with proper governance because they do not want to alienate the innovators who could choose to stop innovating.

These investors also know that tech is the least regulated industry in the world, so it's better to turn a blind eye to cunning growth strategies that push the border of regulation.

The competition to fund these emerging tech companies is borderline criminal.

Uber declined a $3 billion investment by no other than the Oracle of Omaha Warren Buffett.

Buffett described himself as a "great admirer" of Uber CEO Dara Khosrowshahi.

Uber is one of the most unlikely Warren Buffett investments because it doesn't create anything and burns cash faster than a Kardashian.

Buffett's faith in Uber underscores the reliance on tech to fuel the stock market to new heights.

Buffett also admitted mistakes on missing out on Alphabet (GOOGL) and Apple (AAPL).

Rightly so.

Then add in the mix of SoftBank's $100 billion vision fund that just announced an upcoming sequel with another $100 billion vision fund.

Where is all this money flowing into?

Of the tech companies that went through an IPO last year backed by venture capitalist money, 67% relinquished superior voting rights to key founders, a rise of 54% since 2010.

Compare that to non-tech companies that only allow 10% to 15% of CEOs to institute a voting structure that will put them in charge indefinitely.

In many instances, the persona of these ultra-famous tech CEOs has taken on a life of its own.

Elon Musk, CEO of Tesla, is the most prominent example of a celebrity tech innovator milking every possible penny from his shareholders and is not shy about flaunting it.

News has it that Musk needs to go back to the well for another stage of financing later this year.

Don't worry, the money will be there in this climate.

Buffett's rejection was due to losing out to SoftBank, which beat out Buffett to invest in Uber.

SoftBank just announced a $3.35 billion investment into GM's (GM) autonomous driving unit called Cruise enhancing the best big data portfolio in the world.

At this pace, CEO of SoftBank Masayoshi Son will have a piece of every major big data company in the world.

This all bodes well for tech equities as the insatiable hunt for emerging, innovative tech spills over into daily equity market driving up the prices for all the top innovating public companies such as Salesforce, Amazon, Microsoft and Netflix.

Buffett, down on his luck after being shafted by Uber, picked up more Apple shares.

He sold all his IBM (IBM) shares after reading the Mad Hedge Technology Letter advising him to stay away from legacy companies.

Smart move, Warren. You can pick up the tab for our next lunch date.

If you have a few billion to throw around, expect multiple offers over the asking price for any high-grade tech innovation.

The going rate is shooting through the roof and you might NEVER be able to sack the founder.

Caveat emptor.

_________________________________________________________________________________________________

Quote of the Day

"We knew that Lyft was going to raise a ton of money. And we went (to their investors): 'Just so you know, we're going to be fund-raising after this, so before you decide whether you want to invest in them, just make sure you know that we are going to be fund-raising immediately after.' " - said former CEO and founder of Uber Travis Kalanick when asked how he copes with competition.

Mad Hedge Technology Letter

May 14, 2018

Fiat Lux

Featured Trade:

(MEET THE NEW FANG),

(AMZN), (WMT), (FB), (NFLX), (GOOGL), (UBER)

Yes, it's Wal-Mart (WMT).

No, I'm not making this recommendation because they let you park your RV in their parking lots at night for free.

And no, I'm not smoking California's biggest cash crop either (it's not grapes).

I predicted as much in my recent research piece, "Who Will Be the Next FANG?" by clicking here.

It is the dawn of a new era with the world absorbing yet another FANG to add to the list of Facebook (FB), Alphabet (GOOGL), Amazon (AMZN), and Netflix (NFLX).

As the tech world powers on to new heights, nothing can slow down these juggernauts.

Let's face it - companies are more lucrative when technical expertise is ramped up and infused into the business model.

Ground zero of the tech movement - Silicon Valley - has helped supercharge the economy and prodigious earnings' results support this thesis.

New innovations will fuel the next level up in the tech arm's race but more crucially, so will new geographical locations.

Instead of throwing a dart at a world map, the locations are a no-brainer because tech scavenger hunts orbit around one idiosyncrasy and that is scale.

Scalability is a sacred word in the tech world.

If a start-up cannot scale up, investors can't imagine future profits, entrepreneurs can't imagine growth, and funding dries up.

End of story.

For instance, Amazon's business model does not mesh kindly with pint-sized Iceland.

Not because Amazon discriminates against Iceland's culinary delicacy of sheep testicles but because the population is only around 330,000 people.

Scale equals success.

Indisputably, every country with an Amazon-esque business is being bid up because big tech firms know how to digitally monetize, effectively out-sourcing an incredibly profitable business model that has worked unabated for the developed world for the past decade or two.

The heightened awareness of existential survival is pitting foreign money against each other in far-flung places jostling for the same digital assets after a decade of cheap financing enriching tech companies.

Remember that first mover advantage leads to dominance in the datasphere because the volume of data is directly correlated to the bottom line.

Examples are rife around the world, for instance Amazon's $580 million purchase of Souq.com, described as the Amazon of the Middle East headquartered in Dubai and the biggest e-commerce site in the Arab world.

E-commerce commands a paltry 2% of sales in the region. That number is poised to explode as digital-savvy, tech Millennials reach peak consuming age and the migration to mobile erupts.

A preemptive strike is usually the most compelling strategy for large cap tech as it pushes out the smaller players, which lack the resources to compete.

Even the corporate offices of Walmart (WMT) in Bentonville, Arkansas, would wholeheartedly agree with me after doling out for its new toy.

Yes, Walmart acquired a 77% share in the Amazon of India, Flipkart, for $16 billion after the real Amazon failed to cut a deal with the most famous e-commerce unicorn in India.

This new development is a game changer.

India is a country that tech executives pinpoint as the future because of its massive population, economic growth, and economic potential foreign investors hope to tap up.

The International Monetary Fund (IMF) has anointed India as the fastest growing economy in 2018, and the 7.4% growth this year will follow with an even sturdier 7.8% in 2019.

Amazon has been well aware of India's ascent. Its CEO Jeff Bezos pledged to invest more than $5 billion in India and Amazon began its e-commerce operation in 2013.

Amazon's early entrance into the Indian e-commerce industry has paid off grabbing 31% of market share putting it in second place behind Flipkart's 40%, according to big data firms.

The Indian e-commerce space was $20 billion in 2017, and by 2019, expect that number to grow to $35 billion.

Walmart CEO Doug McMillon noted that by 2026, the Indian e-commerce industry will surpass $200 billion. When it comes to clothing and fashion, Flipkart has a 70% share in India.

Even more valuable than the economic growth is the new pipeline of tech talent that will help Walmart compete with Amazon.

The Trump administration's crackdown on H-1B visas that Silicon Valley utilizes to bring developers to American shores has forced American tech companies to implement a work-around.

Essentially, the only difference now will be that the past recipients of H-1B visas will be sitting in an air-conditioned office in Bengaluru, India, until the visa documents come through.

Flipkart has a deep pipeline into the best engineering schools in India and the staff of more than 30,000 employees work on Indian wage levels.

This deal is one of the biggest talent grabs of tech developers the world has ever seen. And this group has the know-how of building an Amazon-style digital marketplace platform from zero.

The Flipkart investment comes after Walmart's purchase of Jet.com, an e-commerce company based in Hoboken, New Jersey.

The $3.3 billion purchase of Jet.com in 2016 was the beginning of Walmart's digital strategy, and it has come a long way in a very short time.

Walmart is now a vaunted member of the FANG group and has a new army of developers to back up this claim.

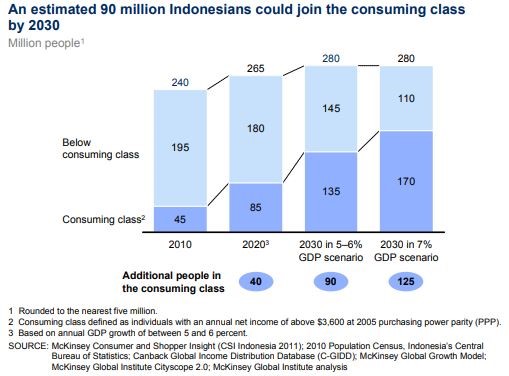

Glancing at the opportunities to scale, Indonesia is clearly the runner-up behind India.

Indonesia has been tagged as a tech new battleground with a population of 260 million in 2016 and growing.

The country has a medium age of 28, meaning this young population could turn into a reliable source of new tech developers who traditionally are young and digital natives.

Economic prosperity has been welcomed with open arms to this tropical island nation. It is poised to become the seventh largest economy by 2030, up from its rank of No. 16 today, creating a burgeoning middle class with newfangled discretionary spending.

The rural migration to urban environments will add another 90 million people living in Indonesian cities by 2030, while Internet access is growing by 20% each year in Indonesia.

Goldman Sachs recently issued a note to investors citing Indonesia's unbridled potential.

Capital is pouring into Indonesia at a breakneck speed with Alibaba investing $1.1 billion into Tokopedia, the Amazon of Indonesia.

Companies are coming to the stark realization that the domestic low hanging fruits have been picked, and aging developed countries are turning to undeveloped regions of growth to advance business objectives.

This is why South East Asia has been bombarded with an onslaught of Japanese, Korean, and Chinese investments and not only in the tech sector.

The Far East powerhouse countries are battling each other in Southeast Asia for consumer goods, infrastructure, high speed trains, and of course technology.

Uber just sold its Southeast Asian ride-sharing asset Grab to China's DiDi Chuxing and SoftBank for $2 billion.

The Southeast Asian region is one of the hottest places to make a deal because of a lack of FANG occupancy.

Walmart sold off on the Flipkart news because of the potential impairment to margins, but this move is a long-term positive for Walmart shareholders.

Flipkart does not turn a profit and Walmart is still solely judged by earnings. Unfortunately, it does not receive the same license to focus on growth like Tesla, Amazon, and Netflix.

However, I have a hunch that down the road, investors will agree this move by Walmart's McMillon was as shrewd as can be.

Like the colonial powers of yore, India and Southeast Asia are likely to be divvied up.

American companies already own more than 70% of market share in India e-commerce.

India is the biggest democracy in Asia and a staunch ally of the United States.

India's frosty relationship with China due to border spats and communist origins will stunt China's ability to take over and expand in India.

However, Southeast Asian countries are more likely to go the way of Cambodia, which is reliant on Chinese money to fund new initiatives, hamstrung by Chinese debt up to its eyeballs, and acquiesced political capital to the Mandarins.

Chinese investment's path of least resistance is Southeast Asia. This progression will be facilitated by the sizable Chinese expat population that resides in Indonesia, Vietnam, Thailand, Philippines, Myanmar, Laos and Cambodia.

Long-term shareholders of Amazon and Walmart will be rewarded. However, expect a few more Indians walking around Bentonville, Seattle, and Hoboken.

_________________________________________________________________________________________________

Quote of the Day

"My life is now a constant assessment of whether what's happening in real life is more entertaining than what's happening on my phone." - said television host Damien Fahey.

Mad Hedge Technology Letter

May 1, 2018

Fiat Lux

Featured Trade:

(AMAZON KILLS IT AGAIN),

(AMZN), (WMT), (FB), (TGT), (GOOGL)

Jeff Bezos is a god.

Well, not quite but he is turning into one after Amazon delivered a mythical earnings report that left Amazon haters in awe.

The Amazon bears patiently waiting for the day of reckoning will have to wait longer as Amazon smashed earnings expectations by a magnitude of two or three.

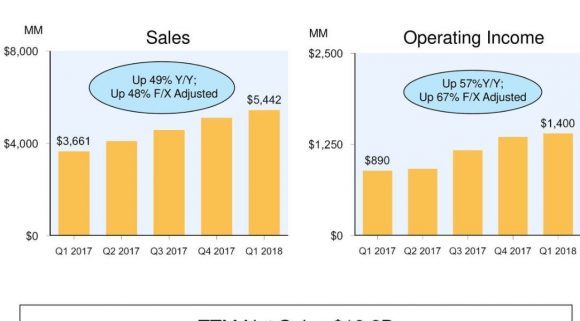

Amazon had a lot riding on the most recent earnings report after racing to new highs in mid-March.

The brief macro-correction then gave investors yet another entry point into one of the best companies of our generation that is still up more than 30% this year.

Amazon Web Services (AWS) revenue reaccelerated from its 42% growth last year to a high octane 49% YOY and made up a disproportionate 73% of Amazon's operating income.

Amazon is heavily reliant on the AWS segment to carry it through feast or famine.

According to Jeff Bezos, its critically acclaimed cloud segments' outstanding results originate from the "seven-year head start before like-minded competition."

This reaffirms the benefit of first-mover advantage with which large cap tech is obsessed.

There is room for other companies in the cloud space, with the cloud industry expanding 20% in 2018 to $186 billion.

Therefore, expanding by 20% is the bare bones minimum to be considered relevant.

Amazon has positioned itself to funnel in the most dollars that migrate toward the cloud as the industries pioneer and best of breed.

After the latest earnings report, Amazon is in pole position to become the first publicly traded $1 trillion company.

This latest quarter wrapped up its 62nd consecutive quarter of 20% plus growth.

And the commentary coming out of the earnings reports makes it almost certain that Amazon will capture more market share.

There were a few bombshells dropped that were unequivocal positives for investors.

First, Amazon has become the third player in digital ad industry with the duopoly of Google search and Facebook.

Amazon revved up its digital ad revenue by 139% QOQ to a substantial $2.03 billion per quarter business.

This business is particularly appetizing because of its high margins and will help alleviate tight margins on the e-commerce side.

Amazon's digital ad business is by far the fastest growth lever in its portfolio. It will ramp up this side of the business whose main function is to match consumers with suitable products that consumers otherwise would miss out on in a standard Amazon search.

The extraordinary numbers support the notion that the hoopla of Washington regulation is all bark and no bite.

Facebook also delivered a prodigious quarter for the ages amid testimony and public backlash that resulted in immaterial damage to top- and bottom-line numbers.

The second bombshell announced was the change in pricing to prime members. Amazon upped its annual prime membership to $119 from $99.

This additional $20 price hike, or 20% on 100 million prime members, will swell revenue by an extra $2 billion of incremental revenue.

In total, Amazon will accrue a bonus of 4% of revenue by this price change.

Amazon has a high fixed-cost business, and slightly tweaking prices will create a huge windfall with the revenue almost entirely flowing down to the bottom line in the form of pure profit.

Many industry analysts claim that Amazon has the best management team in the industry and explicate this company as an "Internet staple."

More than 100 million products are delivered with free shipping for Amazon prime customers. This is starkly higher than the 20 million products shipped for free in 2014.

Amazon does everything in its power to offer a unique and efficient experience for customers.

The customer satisfaction reveals itself by the rock-bottom churn rate.

Amazon prime at an annual cost of $119 is such a value that no analysts even dared to ask Amazon CFO Brian Olsavsky if consumers would take issue with the rise in price.

Investors and strangers alike assume that broad-based reoccurring revenue from annual prime membership is a given.

In an era of mass-scrutinization, Amazon's earnings call seemed like a celebration of the mythical achievements that are changing consumer behavior by the day.

The lack of inquiry was justifiable this time because the one major shortcoming suddenly remedied itself.

Amazon's doubters frequently attack the lack of margin growth because its business model is first and foremost a land grab for market share ignoring any remnants of margin stability.

Now that Amazon's digital ad business has sprouted up, the margin story, starting from a miniscule base, will go from weakness to an unrelenting success.

Amazon started with its ultra-thin margin e-commerce business that made an operating loss of $160 billion in 2017.

Cranking up a shiny, high margin business will be hard for the other FANGs to compete with as they gyrate toward other businesses that have lower margins than Amazon's digital ad segment.

This is a horrible time to start fighting Amazon in price wars as the paradigm shift to quantitative tightening has made the cost of capital demonstrably pricier.

Operating margins almost doubled from 2% to 3.8% on $51 billion of quarterly sales.

This is a huge deal.

Amazon has been continuously harangued for "not making money." Well, that era is over.

Profits, and not only revenue, will start accelerating and Amazon will become the closest thing to a perfect company.

The years and years of plowing cheap capital back into fulfillment center and e-commerce activity gave Amazon a stained reputation for years.

However, as Amazon turns the screws and uses its foundational leverage to capture additional profits, the other FANGs will be forced down the same path ruining operating margins for the other big players.

Amazon telegraphed its quest for market share strategy to investors years ago, and investors understand they are paying for growth and growth only.

That will change now that profits have become a real part of its arsenal.

There is no doubt that Amazon will deploy its profits back into expanding its company because Jeff Bezos knows that if he can grow Amazon's top-line number, investors will follow suit.

Also, spending means improving the products, and Amazon has never hesitated to spend big.

The move into digital ad growth is a warning shot to Facebook and Google. Amazon will mobilize its workforce to take on other business, and anything that is high margin is fair game.

The future looks bleak for retail competitors Walmart and Target, as the contents of the earnings report reaffirms Amazon's unrelenting assault on the retail sector, which is systematically being dissected by Amazon for fun.

Google search and Facebook are in Amazon's crosshairs. Staving off this monster will be hard to do in the long run.

Amazon has a clear path to further market gains, and operating margins are almost at a tipping point.

Revenue is poised to re-accelerate because of the reignition of AWS to a higher growth trajectory.

Shoring up operating margins through a burgeoning digital ad division will only be a boon to earnings in the future.

Amazon is one of the best companies in the world, and any weakness in the stock should be bought and held forever.

_________________________________________________________________________________________________

Quote of the Day

"I do not fear computers. I fear a lack of them," - said writer Isaac Asimov.

Global Market Comments

April 26, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 13, 2018, PHILADELPHIA, PA, GLOBAL STRATEGY LUNCHEON)

(WHY CONSUMER STAPLES ARE DYING),

(XLP), (PG), (KO), (PEP), (PM), (WMT), (AMZN),

(WHY YOUR OTHER INVESTMENT NEWSLETTER IS SO DANGEROUS)

Mad Hedge Technology Letter

April 2, 2018

Fiat Lux

Featured Trade:

(WHY THERE WILL NEVER BE AN ANTITRUST CASE AGAINST AMAZON)

(AMZN), (WMT), (MSFT), (FB), (DBX), (NFLX)