Mad Hedge Technology Letter

December 24, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Mad Hedge Technology Letter

December 24, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape or form.

Microsoft's (MSFT) pivot to its Azure enterprise business has sent its stock skyward, and it is poised to rake in more than $100 billion in cloud revenue over the next 10 years.

Microsoft's share of the cloud market rose from 10% to 13% and is catching up to Amazon Web Services (AWS).

Amazon leads the cloud industry it created and the 49% growth in cloud sales from 42% in Q3 2017 is a welcome sign that Amazon is not tripping up.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes 73% to Amazon's total operating income.

Total revenue for just the AWS division is an annual $5.5 billion business and would operate as a healthy stand-alone tech company if need be.

Cloud revenue is even starting to account for a noticeable share of Apple's (AAPL) earnings, which has previously bet the ranch on hardware products.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day. If you work in Silicon Valley you can triple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations. Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that's where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them telecommute. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees. According to a recent survey, 79% of respondents already work outside of their office some of the time, while another 60% would switch jobs if offered this flexibility.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

Global Market Comments

December 11, 2018

Fiat Lux

Featured Trade:

(JOHN THOMAS TV INTERVIEW Q&A)

(TLT), (FB), (USO), (GE), (PYPL), (SQ), (HD), (UUP), (FXE), (FXY)

Mad Hedge Technology Letter

December 10, 2018

Fiat Lux

Featured Trade:

(IT’S ALL ABOUT THE CLOUD)

(OKTA), (ZS), (DOCU), (INTU)

This is no Potemkin village!

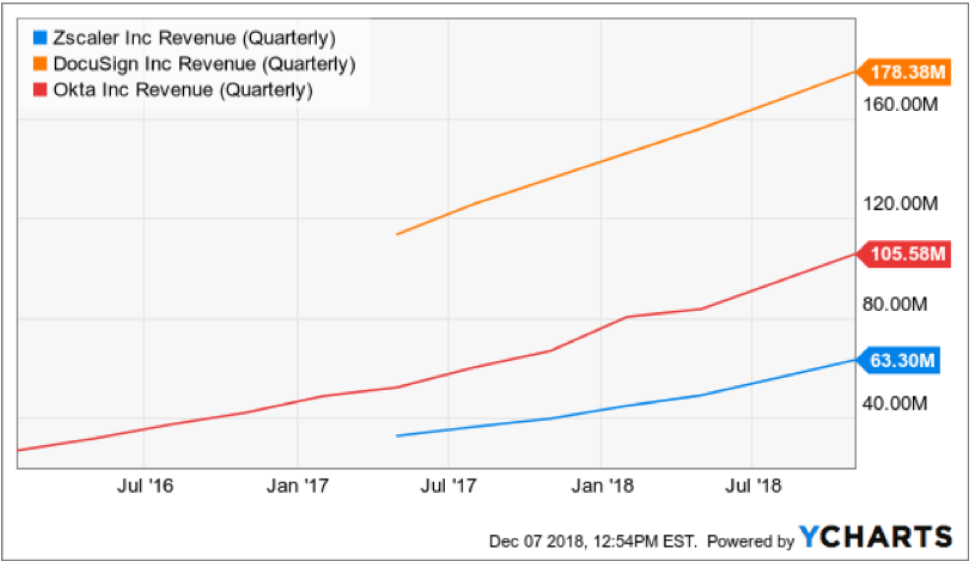

That was my reaction when I examined the earnings reports from second-tier cloud companies Okta (OKTA), Zscaler (ZS), and DocuSign (DOCU).

Cloud companies aren’t going away anytime soon, please singe that into your memory.

Even during a winter Nasdaq (QQQ) swoon, software companies are delivering great earnings.

Ironically enough, the three aforementioned security-based cloud companies come at a time when global tech security is the laser-like focus of contentious geopolitics.

There isn’t a hotter topic circulating the gossip networks these days.

Okta is the best in show for identity management – a snazzy term for managing employees’ passwords.

Okta’s products are built on top of the Amazon Web Services cloud.

Coincidentally, Okta was erected in 2009 by a team of former Salesforce (CRM) executives. Salesforce is one of my favorite cloud-based software companies, offering a blueprint for success to other up-and-coming software companies.

Current Okta CEO and founder Todd McKinnon previously served as the Senior Vice President of Engineering at Salesforce.

Other founders include Okta COO Freddy Kerrest who also walked the corridors of Salesforce.

I can tell you that you could do much worse than starting a new software company with a collection of Salesforce upper echelon talent.

This all-star team is behind the insatiable growth of Okta whose revenue has grown over 600% since establishing itself.

Somewhere along the way at Salesforce, this veteran team became acutely aware of a lack of password security and the dire need for it.

This gang of brothers took it upon themselves to spin out of their former lives and develop this specialized cloud product.

Comparing with Intuit (INTU), the finance and accounting software company, readers can lucidly comprehend the superior growth trajectory of Okta.

I am not tarring Intuit as a bad tech company, it rather does justice to the growth model at Okta.

Okta was forecasted to grow between 43%-45% YOY in the previous quarter and shredded any remnant of doubt by posting 58% YOY of revenue growth.

Last quarter was also Okta’s first profitable quarter as a public company.

Customer expansion was another bright highlight with Okta adding 42% YOY.

Specific relationships that drove the bottom line was America’s second-largest traditional supermarket chain and parent of Safeway, Albertsons, Okta became responsible for their passwords on Albertsons’ e-commerce and loyalty programs.

Other relationships that gained traction were other blockbuster names such as the Transportation Security Administration, Sonoco, LendingClub, and Hertz.

The record third quarter also saw gross margin expansion from 68.4% to 71.9%.

CEO of Okta Todd McKinnon briefly summed up the firm’s outlook by gushing that Okta is “well positioned to further benefit from tailwinds as organizations continue their move to the cloud while digitally transforming and securing their businesses.”

McKinnon stole the words right out of my mouth.

Cloud-based software companies will be outsized winners in 2019 as investors start nitpicking more of which tech to own and which tech to dispose of.

This year spawned a massive divergence between tech who has legs and tech who will be dragged down to the depths of the ocean floor by the heavy weight of regulation, overwhelming competition, or just flat out poor management or inferior product development.

In mid-2018, the FANG shared up moves in unison, Facebook zigged and so did Amazon and friends, then they gleefully zagged together.

That trade unceremoniously fell apart swiftly when macro headwinds applied extreme pressure to each unique model.

Suddenly, the FANGs weren’t best pals anymore and the weaknesses became painfully exposed glaringly to the outside world.

Look for the FANG stocks to experience additional divergence as we moved forward because the low-hanging fruit has been picked and only the strong will excel 2019.

Before the recent turbulence, big tech stocks were assumed as one trade and that is done and dusted.

An exciting new chapter to the tech world and the fierce competition it breeds await with the much-praised unicorns of Uber, Lyft, Airbnb, and Slack going public next year.

As for Okta, analysts expected the company to guide to around a 45% YOY growth rate next year, but management took the liberty to forecast a more audacious revenue growth rate of 53% YOY to a tad below $400 million.

Okta’s management has gone out on a limb predicting revenue to surpass $500 million and maintain an annual growth rate of over 30% for the next five years.

Future revenue has a one-way ticket to $1 billion – quite impressive when you consider 2015 revenue came in at $41 million.

Another growth stock performing amid a tempestuous broader market is digital signature cloud company DocuSign.

The company expansion withstood any supposed softness to its business model outperforming expectations.

DocuSign improved on their 2nd quarter growth rate of 33% and sequentially accelerated to 37% last quarter.

Management jacked up revenue expectations to just under $700 million next year, almost three times the annual revenue of 2015.

The disappointing price action neglecting DocuSign’s bright performances is a sign of the current times.

Catching a horrid downdraft from its 2018 peak of $65 is a swift kick in the groin, but it sadly epitomizes the broader malaise whipsawing market volatility like a bull at a rodeo.

The price action is rare for a company displaying accelerating revenue growth with exciting revenue prospects.

Zscaler echoed the same positive sentiment recording a quarter to remember nudging up sales by a robust 59% easily beating forecasts.

Management geared towards premium-priced bundles spiking gross margin massaging the bottom line.

Next year’s annual guidance was nothing short of spectacular with management believing the company will crack $270 million of total revenue compared to analysts conservatively modeling $259 million in 2019.

Zscaler is still labeled a minnow in the larger landscape of the cyber security market and is the smallest of the three firms written about today, but that is gradually moving up the totem pole as the firm’s hyper-growth model is kicking into gear.

Gartner research estimates that the global information security market will eclipse $124 billion in 2019 offering many players an enlarging piece of the pie.

It is justifiable to bake in that Zscaler's prospects will outrun any broader weakness that tries to crimp the stock’s unfettered momentum.

With a current market capitalization slightly north of $5 billion, the growth potential may justify a premium valuation.

Investors fervently applauded the quarterly results elevating the stock 12% on the positive news.

Zscaler is now convinced it can spearhead consistent profitability and positive cash flow by 2020.

It’s hard not to see them decimate their own in-house projections.

These three shining stars of the cloud revolution are not papering over cracks of a dying model, they are front and center of a cohort leading the digital economy and the underlying outperformance backs up this premise.

Unfortunately, even if a company goes gangbusters, they could still be vulnerable to outside forces which are lamentably unavoidable.

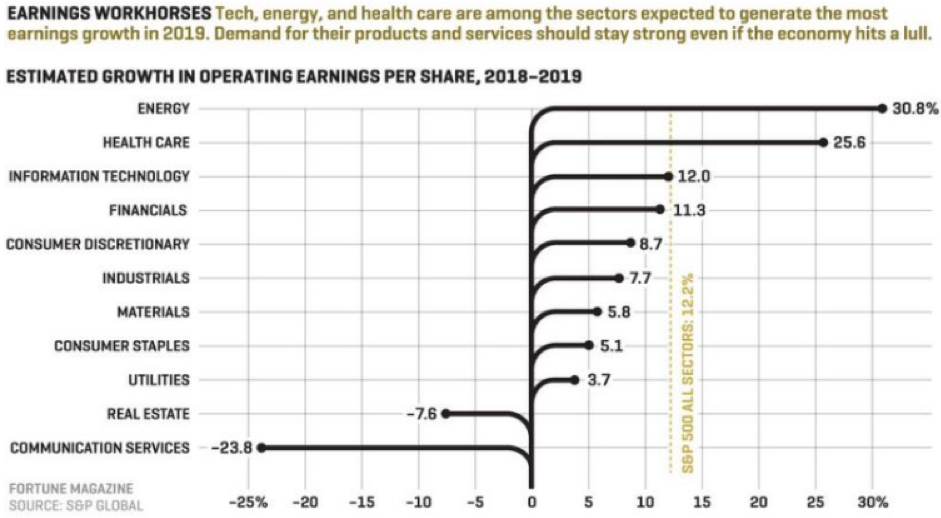

A report published by S&P Global shows the tech industry growing earnings by 12% in 2019, only trailing health care and energy.

This is a great sign of things to come next year.

The demand for quality cloud products of this ilk is one theme that will perpetuate.

The American economy is on the verge of a whole slew of analog companies from other sectors traversing single file into the sweet spot of the data-dependent tech taxonomy clamoring for hybrid specialized offerings.

It is safe to say burgeoning cloud-based software companies with annual revenue of less than half a billion dollars are not only primed to take advantage of the digital migration phenomenon irrespective of the machinations in Washington or the fluctuations of treasury yields, but will post attractive financials numbers because of the law of large numbers that makes small companies’ results look better than they are on a percentage basis.

Mad Hedge Technology Letter

October 23, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Mad Hedge Technology Letter

July 2, 2018

Fiat Lux

Featured Trade:

(THE CLOUD FOR DUMMIES)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape or form.

Microsoft's (MSFT) pivot to its Azure enterprise business has sent its stock skyward, and it is poised to rake in more than $100 billion in cloud revenue over the next 10 years.

Microsoft's share of the cloud market rose from 10% to 13% and is catching up to Amazon Web Services (AWS).

Amazon leads the cloud industry it created, and the 49% growth in cloud sales from the 42% in Q3 2017 is a welcome sign that Amazon is not tripping up.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes 73% to Amazon's total operating income.

Total revenue for just the AWS division is an annual $5.5 billion business and would operate as a healthy stand-alone tech company if need be.

Cloud revenue is even starting to account for a noticeable share of Apple's (AAPL) earnings, which has previously bet the ranch on hardware products.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day. If you work in Silicon Valley you can triple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations. Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that's where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy remember that the original Department of Defense packet switching design was intended to make the system atomic bomb proof.

As a user you can access any single server at any one time anywhere in the world. These servers are owned, maintained and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at anytime from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Today's employees want to have a better work/life balance and this goal can be best achieved through letting them telecommute. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees. According to a recent survey, 79% of respondents already work outside of their office some of the time, while another 60% would switch jobs if offered this flexibility.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document, so they can stay on top of real-time changes, which can help businesses to better manage work flow, regardless of geographical location.

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

_________________________________________________________________________________________________

Quote of the Day

"Life is not fair; get used to it," said founder of Microsoft Bill Gates.

Mad Hedge Technology Letter

June 11, 2018

Fiat Lux

Featured Trade:

(HERE ARE SOME GREAT SECOND-TIER CLOUD PLAYS TO SALT AWAY),

(DOCU), (ZUO), (ZS), (MSFT), (AMZN)

The year of the cloud has been one of the most successful themes for the Mad Hedge Technology Letter since inception and rightly so.

The heavy hitters are knocking it out of the park with the top gangbuster firms facing no impediment to success.

As these firms crack on, it seems there is not a day that passes by where Amazon (AMZN) or Microsoft (MSFT) do not close up 1% for the day.

If you are feeling nervous and believe the top cloud plays are getting too frothy for your taste, even though they are not, it is time to look at alternative parts of the cloud ecosphere that could tickle your fancy.

The second-tier cloud companies focusing on a particular niche of the market is the perfect place to identify companies that are growing at higher rates than the top cloud companies in terms of revenue expansion.

Amazon, because of its sheer size, will find it harder to double its revenue in the same amount of time as cloud companies with annual revenue of just a few hundred million dollars.

Zscaler (ZS) is a cloud security company that I advised readers to buy on April,16, at $29 and after a blowout quarterly report the stock touched the $42 handle intraday.

This company is a solid buy, especially in light of the General Data Protection Regulation (GDPR) and a newfound, broad-based emphasis on Internet security that will usher in a new injection of cloud security spending.

Zscaler CEO Jay Chaudhry delivered a glorious quarterly performance and the only direction this company is going is up.

All told, Zscaler processes in excess of 45 billion Internet requests per day during peak periods.

It detects and blocks more than 100 million daily threats while performing more than 120,000 unique daily security updates.

The end result is far superior security than traditional outlets. That's the whole point.

The cloud security company was able to inspire business to a 49% YOY pace of growth and calculated billings were up 73% YOY to $54.7 million.

The quarter's success didn't stop there with operating margins gaining 9% YOY helping Zscaler go cash free positive for the quarter.

The type of security products it offers is part of an annual $17.7 billion market and rapidly expanding.

Firms are incentivized to adopt these products because reduced cost on bandwidth and lower network equipment costs benefit the bottom line.

A mobile dominant world is fast approaching, and Zscaler has positioned itself perfectly to take advantage of the new pipeline of business coming its way.

The slew of new signed contracts reinforces this trend.

The most prominent deals were with a Fortune 500 medical equipment company that purchased a bundle including a Cloud Firewall, Sandbox and Data Loss Prevention for 40,000 users.

It followed that up with a deal with a European bank that added the business bundle with SSL inspection and data loss prevention (DLP) for more than 70,000 users driven by the business moving to Office 365.

Zscaler kept going strong with another Fortune 500 tech company joining its lineup, integrating the transformation bundle for 20,000 employees and contractors just six months ago,

They were thrilled with the products, leading them to buy an additional 25,000 seats and now have all 45,000 employees served by Zscaler.

A global 500 IT services and products company in Asia went for the entry level professional bundle covering10,000 users in Q2.

It expanded the next quarter with the same bundle for more than 130,000 users domestically.

Forecasted revenue is expected to be in the range of $184 million to $185 million, substantially larger than the $126 million of revenue in 2017.

Once annual revenues start eclipsing the several billion-dollar mark, growth becomes tougher to grind out.

Zscaler is headed by an old hand and understands the market in detail.

The firm will be in a growth sweet spot for the foreseeable future. Subscribers who do not mind taking on the added risk could expect these investments to pay off many times over.

Another niche cloud company Zuora (ZUO) is performing briskly.

I recommended this stock the same day as Zscaler when it was trading at $20.50. The stock is up big, rocketing to $28.50 at the time of this writing.

Zuora is a company focused on software that helps companies manage their subscriptions business, which has been all the rage for tech companies.

The software as a service (SaaS) model has become the de-facto standard to bill for tech services, and Zuora helps automate and execute.

First quarter revenue surged 60% to $51.7 million.

Zuora's retention rate of 110% increased to 112%, demonstrating that existing customers buy premium add-ons and stick around in its ecosystem.

Zuora increased the numbers of clients with an active contract value greater than $100,000 by 6% to 441, resulting in a net add of 26.

Zscaler and Zuora are around the same size and could experience similar bullish price trajectories in the stock going forward.

DocuSign (DOCU), a digital signature software company, is another niche player whose services have been valuable in the business environment.

Instead of scrawling out your name with a quill and ink, clicking to sign makes the process faster than ever.

The stickiness of its services led Forbes to anoint DocuSign as the fourth best cloud company on the Forbes Cloud 100 list in 2017.

Last year saw DocuSign blow past the half a billion-number bringing in revenue of $518 million, up 36% YOY.

The lion's share of its business comes from its subscription business carving out $484 million in 2017, passing the $348 million in 2016.

DocuSign set an IPO price range between $24 to $26 in April 2018, and the stock has more than doubled to $58 today.

Do not fight against the cloud; embrace it like your lovable pet dog. There is no reason to short these stocks because chances are likely you will get badly burned on these ultimate buy on the dip stocks.

However, DocuSign has seldom even dipped, even in the face of a trade war, crushing dip buyers' dreams.

It has gone up in a straight line.

Only once since its late April IPO has there been a pullback of more than $1.50, and that happened in mid-May when the stock went from $45.50 to $43.

Remember, the trend is your friend.

Zscaler's 37% bump to its share prices after the earnings beat is why you want to get into this stock.

The moves up are legendary.

Zuora's earnings beat earned them a not-too-shabby 20% one-day return as well.

No matter how well Amazon does, there is no 37% up move in one day unless it finds the cure for cancer in a single pill form.

As Amazon and Microsoft grow stronger, so does the appetite for these niche cloud services.

The tide will lift all boats and choosing either a dinghy or a luxury yacht will stand you in good stead.

_________________________________________________________________________________________________

Quote of the Day

"I don't care about revenues," - said Cofounder and Executive Chairman of Alibaba Jack Ma.