“Our industry does not respect tradition - it only respects innovation.” – Said current CEO of Microsoft Satya Nadella

“Our industry does not respect tradition - it only respects innovation.” – Said current CEO of Microsoft Satya Nadella

Mad Hedge Technology Letter

September 18, 2019

Fiat Lux

Featured Trade:

(WHY YOU SHOULD AVOID CHINESE TECH IPOS LIKE THE PLAGUE)

(TSLA), (BIDU), (NIO)

Millennials usually stick with the stocks that they know.

That’s all fine until it takes a bite out of their wallet.

Some of these decisions based on the products that represent this generation have been stock market disasters of late.

Sadly, many Millennials were too young to catch the ride up for Tesla.

Many older generations got into the stock at $20, $40 and $100 and rode the elevator up with an ultra low-cost basis.

I can’t say the same for Millennials as many came of age and finally had the money to splurge for shares after the stock had plateaued.

This was a cringe-worthy lesson that just because a company has a great product doesn’t always mean the stock is just as great.

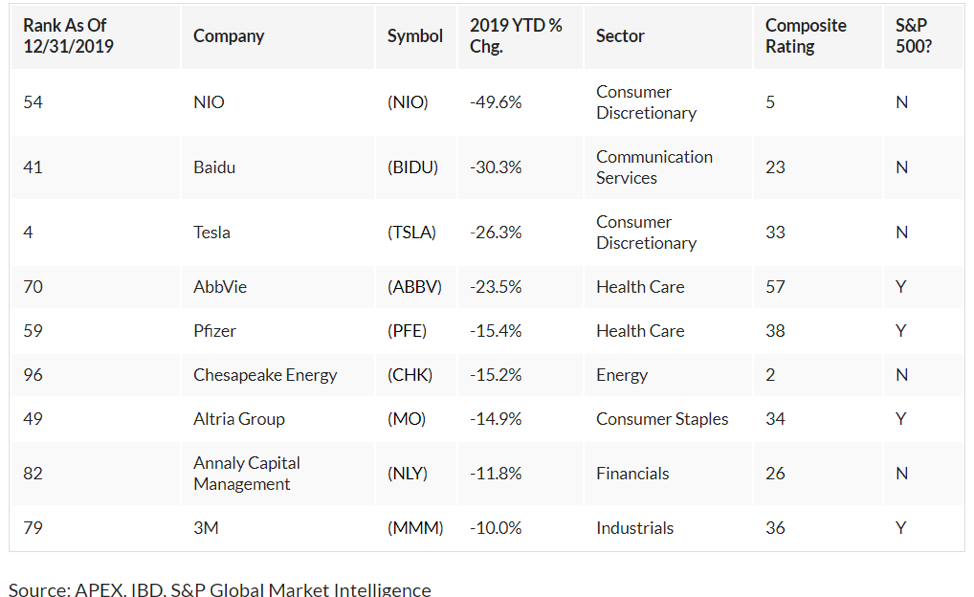

Electric Vehicles (EV) are front and center of the Millennial consciousness and that also meant that many scooped up NIO which is the Chinese version of Tesla.

After peaking at $10 in March, the stock is now trading at $3.

Many Chinese IPOs that go public in New York are of a pump-and-dump mentality as they shower the public with losses.

In fact, many Chinese IPOs only have the goal of going public without the goal of doing much more after that.

NIO has yet to be found out completely, but the Chinese economy is hurting and the Chinese consumer has reigned back the purse strings as times become lean.

As we head into a global slow down, electric car companies that lose boatloads of money will be in the firing line for value revaluations.

In fact, I would urge any reader to steer clear of any Chinese company traded on the public markets because of opaque financials that are intentionally obfuscated.

Baidu is another favorite of the Millennial generation pigeonholed as the “Google search of China.”

That moniker is an impressive catchphrase but it doesn’t do much to rejuvenate the large loss in market share that Baidu has ceded to Alibaba and WeChat platforms.

Baidu has lost its mojo and is bleeding usership and it will be hard to reverse it as Baidu never evolved with the changing trends of Chinese consumers.

Baidu peaked in April 2018, at $250 and is now trading at less than $108 and the slide isn’t over yet as Baidu has no adequate response to the domination of the other Chinese tech behemoths.

Yes, many tech trends have legs and are secular shifts that have major ramifications to the global economy.

But the devil is in the details and peels back the layers to be aware of developments such as CEO of Tesla Elon Musk building an American Gigafactory in Shanghai at the worse time in economic history as a legitimate canary in the coal mine.

As robust as the Chinese consumer has been, the latest contagion of African swine flu that culled a major amount of Chinese pigs has raised the price of pork by over 45%.

Chinese consumers are hyper-aware of these economic developments in the year of the pig.

After a massive ride up in Chinese tech shares and electric car story that took many investors breath away, we are at the beginning of a meaningful revaluation that will change the narrative moving forward.

Timing is everything in this game.

“I don't care about revenue.” – Said Founder of Alibaba Jack Ma

Mad Hedge Technology Letter

September 16, 2019

Fiat Lux

Featured Trade:

(GILLETTE’S MARKETING FLUB)

(PG)

The pitfalls of getting it wrong can bring you tears.

Proctor and Gamble (PG) got a taste of precisely that.

We underestimate the power of digital marketing and how it can make or break a company’s fortune.

Even many small businesses rely on media platforms such as YouTube, Patreon, Snapchat, Twitter and so on to disseminate their message and nurture their brands.

But what if it goes badly wrong?

The story of personal grooming brand Gillette is a stark warning for companies to stay in their lanes and not reach too far when it comes to their digital marketing campaigns.

Once companies start diving into delicate social issues, they risk alienating half or more of their targeted audience.

In January, Gillette debuted a short film in part of continuing their woke campaign with a self-titled phrase called “toxic masculinity.”

To see the short video please, click here.

Gillette’s underlying message suggested that men in general pose a deep problem in society.

Their self-coined phrase “toxic masculinity” rolls through clips of portraying a young boy being bullied by other boys, sexual harassment, catcalling, and a man speaking over a woman in a meeting highlighting the disappointment in the male gender.

Instantly, the backlash from Gillette’s core demographic, men who shave, were heard from in full force with many shouting from the rooftops for a boycott on Gillette’s and even Procter and Gamble’s products.

Gillette didn’t blink and doubled down on their woke campaign rolling out a “fat acceptance” ad.

They did not stop there and tripled down distributing an ad depicting a father's first time teaching his female-to-male transgender child how to shave.

Gillette were defiant in their beliefs and felt an obligation to dip into social discourse and take a stand for what they think is the right message to sell razors.

Just a mere seven months after Gillette’s social justice campaign began, Gillette's parent company Procter & Gamble took an eye-popping $8 billion write-down citing a painful charge for Gillette’s personal grooming division.

The company would have produced net profits without this ghastly charge.

Granted that Gillette was already having a tough time selling more razors as a combination of trends and demographics decrease the volume of male shaving, but the exacerbation of underperformance was purely due to the revolt against the digital marketing campaign which drove away their core customer.

Gillette’s excuse was currency fluctuations and increasing competition but that can in no way explain the giant uptick in customer deterioration.

Management’s strategy of profiting from woke capitalism on the back of the #MeToo movement blew up in their face and many men chose to respond with their wallets.

This also represents the viral nature of digital marketing in 2019 and it really works both ways.

It also indicates how powerful these tech platforms are as the cradle of human discourse and underscores how reliant even the largest of corporations are on digital marketing through the likes of Instagram, Facebook, Google, Amazon and the who’s who of Silicon Valley.

“A squirrel dying in front of your house may be more relevant to your interests right now than people dying in Africa.”

Mad Hedge Technology Letter

September 13, 2019

Fiat Lux

Featured Trade:

(ANOTHER VIEW OF THE ANTITRUST ASSAULT)

(FB), (APPL), (GOOGL)

When will CEO of Apple Tim Cook get fired?

I feel like a broken record.

Another product show comes and goes with him STILL selling a bunch of iPhones.

He is the most uncreative CEO that exists in a company where the utmost creativity is demanded.

He is starting to make a mockery and drag Apple’s reputation through the mud.

I believe that Apple is on a suicide mission ruining its brand that took founder Steve Jobs decades to craft.

What we got was the iPhone 11 Pro with three cameras on the back, is Cook going to be around for iPhone 15 or 16?

The world and the people that can afford an iPhone are already tapped out with iPhones, iPods, iPads, and devices.

These same consumers won’t buy 5 iPhones to use at the same time.

The Apple Watch Series 5 with an always-on display has been a nice bump in revenue but that’s it, just a nice bump and will never go viral.

Since Cook is having problems selling $1,000 Apple devices, he has chosen to sacrifice margin and go down market.

How Steve Jobs would be turning in his grave if he heard that!

The new Apple+ video streaming service will debut in November at a price of just $5 per month–or free for a year with the purchase of any of Apple's phones, computers, tablets, or set-top boxes.

Viewers will have access to just a dozen or so made-for-Apple+ shows that Apple is producing.

Sounds quite pitiful if you compare it with Netflix.

I understand that Cook is spurning revenue in the short run with low prices but to what end?

If Cook brings back the same playbook of selling the next iPhone, at some point, he will be blustered by shareholders who finally come to the same conclusion as me.

The lower margin business will be the catalyst to Cook’s firing once Apple’s margins go down the toilet.

At some point, he will have to come up with the product that will reinvent the world and my bet is he will utterly fall flat on his face.

We are talking about the CEO of Apple here and not the boss of some local car repair shop.

Apple will sell the new iPhone 11 for $700 instead of $750 and this decision will bring the average selling price (ASP)’s down.

Let’s welcome their new business in switching out old iPhones, another damning development in this company that used to be the most exciting business in the world.

Apple will also roll out a trade-in initiative that offers current iPhone owners money in credits for handing over their old phone when they buy a new one.

A two-year old iPhone X is worth up to $400 and an iPhone 7 fetches $150.

The trade-in program is a desperate reaction to falling iPhone sales.

If the company hired a visionary like Twitter’s Jack Dorsey or Tesla’s Elon Musk, Apple shares would trade twice as high than the $225 today and wouldn’t have gone flat for the past year.

In Cook’s defense, the sequel to Steve Job’s main act was going to be a rough one to match in success and potency and it is clear that Cook is in over his head.

It’s odd that I am the only one that sees it.

“Anything can change, because the smartphone revolution is still in the early stages.” – Said CEO of Apple Tim Cook