“We're very simple people at Apple. We focus on making the world's best products and enriching people's lives.” – Said CEO of Apple Tim Cook

“We're very simple people at Apple. We focus on making the world's best products and enriching people's lives.” – Said CEO of Apple Tim Cook

Mad Hedge Technology Letter

July 31, 2019

Fiat Lux

Featured Trade:

(TIME TO TAKE A BREAK WITH GOOGLE),

(GOOGL)

It’s time to take a breather.

That is after the 9% spike in Google shares.

The best way to describe results of late for Alphabet is a mixed bag for the company helmed by Sundar Pichai.

Things aren’t going bad but not great either.

I‘ll tell you why.

Alphabet undershot its top-line revenue by about $1.7 billion, a large miss that should disturb investors.

It’s definitely not the growth company it once was even though some elements of Alphabet are still growing profusely.

Nothing better epitomizes the state of Google’s ad cash cow with its cost-per-click on Google properties from Q2 2018 to Q2 2019 falling 11% showing that they are having a harder time charging customers for clicking their stuff.

But on the bright side, paid clicks on Google properties from Q2 2018 to Q2 2019 was up 28% demonstrating the attractiveness and stickiness of platforms such as YouTube and Google Search.

Two other bright spots were its in-house lineup of smartphones called the Pixel and cloud products, which helped this segment grow to $6.18 billion compared to $4.43 billion last year.

I am actually a huge fan of the Pixel lineup even though I go with an iPhone.

If I did own an Android, I’d choose the latest Pixel with the added bonus of the convenience of Google’s best in show software.

Google is coming out with their Pixel 4 later this fall.

Pichai has never dived into the finer numbers of the Google Cloud but he took the time to mention that its cloud division is now an $8 billion and growing business annually.

Alphabet plans to heavily hire an army of warm bodies tripling the cloud staff for their successful cloud unit which is poised to be a mainstay growth driver for Google.

Looking at the imminent future, there are a few bogies in the sky.

The Australian Competition and Consumer Commission is part of a growing chorus of domestic and international regulators looking to subdue Google’s big data businesses.

The best-case scenario is more fines in the billions of dollars and the worst case is shriveling access to certain lucrative end markets.

Alphabet has been hard hit by the trend of more stringent global data regulations, and this is just the beginning.

Facebook appears as if it's in a deeper quagmire with multiple regulatory commissions state side smelling blood in shark-infested waters.

There is part of the argument that these practices stem from Alphabet being too dominant and there is some truth in this.

They are literally gunning for the entire internet whether it be travel or eCommerce.

I would say from my experiences with Alphabet that they do push the threshold a tad bit far.

They probably do not need to preinstall YouTube and Google Chrome on Android Devices without the inability to delete them.

If you have tried to delete these apps from Android devices, you are stonewalled, but I do hold the view that users will naturally come to the conclusion these apps are utilities and would download them if not preinstalled in the first place.

Alphabet should be more comfortable in its expertise and leadership position.

After a rapid run-up in share appreciation, Alphabet is due for a short-term pullback which could materialize soon because of regulatory fears.

Traders should look at some short duration bear put spreads on Alphabet.

I am long-term bullish Alphabet.

“The right moral compass is trying hard to think about what customers want.” – Said CEO of Google Sundar Pichai

Mad Hedge Technology Letter

July 29, 2019

Fiat Lux

Featured Trade:

(THE RACE TO THE BOTTOM),

(SCHW), (FB), (SQ), (WMT), (AMZN), (FFIDX), (BOX)

Gone are the days of brokers shouting from the trading pits, a bygone era where pimple-faced traders cut their teeth rubbing shoulders with the journeymen of yore.

The stock brokerage industry is at an inflection point with the revolutionary online stock brokerage Robinhood on the verge of shaking up an industry that has needed shaking up for years.

A common thread revisited by this newsletter is the phenomenon of broker apps being low-quality tech.

A broker ultimately serves little or no value to the real players among the deal, usually extracting huge commissions.

Technology and now blockchain technology vie to completely remove this exorbitant layer from the business process.

Well, for the stock brokerage industry, that time is now.

Robinhood is an online stock brokerage company based in Menlo Park, Calif., trading an assortment of asset classes including equities, options, and cryptocurrencies.

So, what's the catch?

Robinhood does not charge commission.

That's right, you can invest up until the $500,000 threshold protected by the Securities Investor Protection Corporation (SIPC) and you can go along with your merry day trading for free.

The online brokerage industry has been getting away with murder for years.

They got comfortable and stopped innovating - the death knell of any company in 2019.

Effectively, high execution costs reaping massive profits were the norm for brokers, and nobody questioned this philosophy until Robinhood exposed the ugly truth - unreasonably high rates.

Peeking at a monthly chart of brokerage costs will make your stomach churn.

For instance, a trader frequently executing trades with an account of $100,000 would hand over $1836 in commission in 2017 if their account was with Fidelity.

On the cheaper side, Interactive Brokers would charge $854 for its brokerage services to habitual traders per month.

The outlier was Tradier, a start-up brokerage founded in 2014 using the powerful tool of an Application Programming Interface (API) which charged $213 per month to trade frequently.

An API is described as a software intermediary allowing two applications to communicate with each other.

This model helped cut costs for the online brokerage because Tradier did not have to focus its funds on the trading platform that was delegated to various third-party platforms.

Tradier is largely responsible for the aggregation of data and charts thus employing an army of developers to meet their end of the business.

This model is truly the democratization of the online brokerage industry, which has been coming for years.

Costs are cut to a minimum with equity trades at Tradier costing investors $3.49 per order and options contracts costing $0.35 per contract with a $9 options assignment and exercise fee.

Technology has defeated the traditionalist again.

More than 80% of Robinhood's accounts are owned by millennials – as expected.

Trading cryptocurrencies act as a gateway asset to springboard into other asset classes such as equities and derivative contracts.

Vlad Tenev, co-CEO of Robinhood, indicated that Robinhood will have to modify its radical business model to monetize more of the business in the future, but he is comfortable with the current business model.

But Tenev has already seen fruit borne with the likes of Robinhood applying fierce pressure to the legacy brokerages' pricing models.

The traditionalists are locked in a vicious pricing war with each other slashing their commission rates to stay competitive.

The longer the likes of Charles Schwab (SCHW) feel it necessary to charge $4.95, down from the January 2017 cost of $8.95, the better the chances are that Robinhood can build its account base rapidly.

Charles Schwab has more than 10 million accounts, only double the number of Robinhood, after being founded in 1971.

The 42-year head start over Robinhood has not produced the desired effect, and it is ill-prepared to battle these tech companies that enter the fray.

Robinhood has been able to add a million new accounts per year. If Charles Schwab relatively performed at the same rate, it would have 47 million accounts open today.

It doesn't and that is a problem because the company can be caught up to.

The age of specialization is upon us with full force, and customer demand requires care and diligence that never existed before.

Robinhood continues to enhance its offerings of various products adding Litecoin and Bitcoin Cash to the crypto lineup.

Only Bitcoin and Ethereum were offered before.

And there is one more outrageous thing I forgot to tell you.

Robinhood hopes to snatch away the traditional savings account by offering checking and savings accounts with an interest rate almost 30 times larger than most brick and mortar banks – 3%.

These accounts would have no minimum balances or no fees that nickel and dime customers.

The service will conveniently sit alongside its trading app and this move into the industry led by JP Morgan could start to derail Wall Street.

As with most FinTech start-ups, the roll-out of this new service was slightly botched because Robinhood failed to get the go-ahead from regulators concerning ensuring the accounts properly.

All this does is delay the inevitable and by spring 2019, potential customers should be earning 3% in Robinhood’s checking and savings account.

Sign me up!

"When something is important enough, you do it even if the odds are not in your favor." - said Tesla founder and CEO Elon Musk.

Mad Hedge Technology Letter

July 26, 2019

Fiat Lux

Featured Trade:

(WHY 3D PRINTING WILL BOOST THE AIRPLANE INDUSTRY),

(SSYS), (ETSY), (MSFT), (BA), (NFLX), (GE), (LMT)

If you need a new investment idea – here’s one.

3D printing.

Yes, the same 3D printing that was once considered a raging but hopeless fad.

A lot has changed since then.

Early adopters were largely cut down at the knees as they tried to traverse the rocky terrain from a niche market to going full out mainstream.

The teething pains echo bitcoin which was the fad of 2017, on the contrary, this technology it is built on is rock solid, yet the path to sustainability is littered with corpses.

Production complications and the lack of specialists in the industry meant that problems were rampant and nurturing an industry from scratch is harder than you think.

It is time to stand up and take notice of 3D printing, this time it is here to stay.

Certain tech companies love this technology.

Etsy (ETSY) e-commerce participants gravitate towards 3D printing because it gets firms from paper to the real world in a fraction of the time.

The cost of production doesn’t change whether you’re producing one item or a million because of the economies of scale.

The previous 3D printing bonanza was a frenzy and this corner of tech became known for the use of buzzwords representing the potential to reinvent the world.

With lofty expectations, there was a natural disappointment when outsiders understood growing pains were part of the critical evolution instead of a direct route to profits.

The initial goal was to democratize production which sounds eerily similar to bitcoins mantra of democratizing money.

The way to do this was to make it simple to produce whatever one wishes.

That would assume that the general public could pick up professional production 3D printing skills on arrival.

That was wishful thinking.

The truth was that applying 3D printers was time-draining and aggravating.

Issues cropped up like faulty first-generation hardware or software -problems that overwhelmed newbies.

Then if everything was going smoothly on that front, there was the larger issue of realizing it’s just a lot harder to design specific things than initially thought without a deep working knowledge of computer-aided software (CAD) design.

Most people know how to throw a football, but that doesn’t mean that most people can wake up one day in their pajamas and convince themselves they will be the next starting quarterback to lead an NFL team to the Super Bowl.

The high-quality 3D printing designs were reserved for authentic professionals that could put together complicated designs.

The move to compiling a comprehensive library will help spur on the 3D printing revolution while upping the foundational skill base.

Then there is the fact that 3D printing technology is a lot better now than it once was, and the printing technology has come down in price making it more affordable for the masses.

These trends will propel broad-based adoption and as the printing process standardizes, more products can rely on this technology from scratch.

The holy grail of 3D printing would be 3D printing on demand like Netflix (NFLX), but imagine this on-demand 3D printing would function to personalize a physical product on the spot.

Think of a hungry customer walking into a restaurant and not even looking at a menu because one sentence would be enough to trigger specific models in the database that could conjure up the design for the meal.

This would involve integrating artificial intelligence into 3D printing and the production process would quicken to minutes, even seconds.

At some point, crafting the perfect meal or designing a personalized Tuscan villa could take minutes.

The 3D printing industry is reaching an inflection point where the advancement of the technology, expertise, and an updated production process are brewing together at the perfect time.

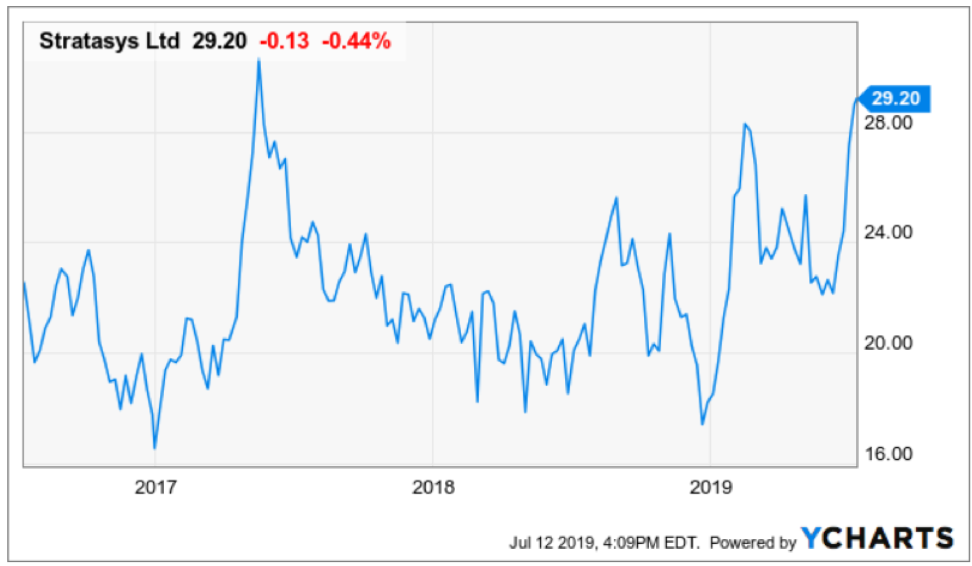

The company at the forefront of this phenomenon is Stratasys (SSYS).

Stratasys produces in-office prototypes and direct digital manufacturing systems for automotive, aerospace, industrial, recreational, electronic, medical and consumer products.

And when I talk about real pros who have the intellectual property to whip out a complex CAD-based 3D design, I am specifically talking about Stratasys who have been in this business since the industry was in infancy.

And if you add in the integration of cloud software, 3D printing would dovetail nicely with it.

All the elements are in place to fuel this industry into the mainstream.

Take for example airplanes made by Boeing (BA) and Airbus, 3D printer-designed parts comprise only 0.1% of the actual plane now.

It is estimated that 3D printed design parts could consist up to 20% of the overall plane.

These massive airline manufacturers like Boeing (BA) have profit margins of around 15% to 20%, and carving out more 3D printer-designed parts to integrate into the main design will boost profit margins to up to 50%.

The development of the 3D printing process into aerospace technology is happening fast with Boeing inking a five-year collaboration agreement with Swiss technology and engineering group Oerlikon to develop standard processes and materials for metal 3D printing.

Any combat pilot knows who Oerlikon is because they are famed for building ultra-highspeed machines to shoot down, you guessed it, airplanes and missiles.

They will collaborate to use the data resulting from their agreement to support the creation of a standard titanium 3D printing processes.

Only last November, GE announced that GE’s Aviation’s GEnx-2B aircraft engine for the Boeing 747-8 will apply a 3D printed bracket approved by the Federal Aviation Administration (FAA) for the engine, replacing a traditionally manufactured power door opening system (PDOS) bracket.

With the positive revelations that the (FAA) is supporting the adoption of 3D printing-based designs, GE is preparing to begin imminent mass production of the 3D printed brackets at its Auburn, Alabama facility.

Eric Gatlin, general manager of GE Aviation’s additive integrated product team gushed that “It’s the first project we took from design to production in less than ten months.”

Defense companies are also dipping their toe into the water with aerospace company Lockheed Martin (LMT), the world’s largest defense contractor, winning a $5.8 million contract with the Office of Naval Research to help further develop 3D printing for the aerospace industry.

They will partner up to investigate the use of artificial intelligence in training robots to independently oversee the 3D printing of complex aerospace components.

3D printed designs have the potential to crash the cost of making big-ticket items from cars to nuclear plants while substantially shortening the manufacturing process.

Further emphasis on cornering the North America aerospace market could cement this stock as a no-brainer buy of 2019 as the (FAA) embraces more of the technology opening up the addressable market for the active participants.

As it stands, Stratasys is the industry leader in this field, and placing best of breed tech companies into your portfolio will put you in better position to weather the squalls of the capricious tech sector.

The company is still relatively unknown even though it has been around for ages.

Stratasys is a company to put on your radar and remember this space as the 3D printing market blossoms.

It’s nonetheless still a speculative punt but a compelling part of the tech industry.

“Capitalism has worked very well. Anyone who wants to move to North Korea is welcome.” – Said Founder and Former CEO of Microsoft Bill Gates