Mad Hedge Technology Letter

June 19, 2019

Fiat Lux

Featured Trade:

(FREELANCING TO THE TUNE OF THE GIG ECONOMY)

(FVRR), (LYFT), (UBER), (UPWK)

Mad Hedge Technology Letter

June 19, 2019

Fiat Lux

Featured Trade:

(FREELANCING TO THE TUNE OF THE GIG ECONOMY)

(FVRR), (LYFT), (UBER), (UPWK)

The company who exploits workers in the gig economy, Fiverr International Ltd. (FVRR), went public and is a terrible long-term buy and hold for investors.

I’ll tell you exactly why you should stay away from it like the plague.

Take a look at one of the sad side effects of the tech industry – 58% of full-time gig workers said they would have a hard time finding $400 to cover an emergency bill compared to 38% of people who don’t work in the gig economy.

The large discrepancy indicates that the informal economy is far more destabilized from Silicon Valley than investors care to admit.

And in many cases, the brutal economic conditions don’t underline the lack of upward mobility too.

While some are drawn to flexible roles, the gig-economy has faced condemnation, particularly because it has enabled companies to marginalize workers as contractors rather than employees who would be entitled to benefits and wage protections.

What about the risks of Washington smushing their business models?

Fiverr confesses that policy changes could destroy their business model if the ability to designate their workers as contractors is banned.

The freelance model could also become less attractive if it means higher regulatory risk or even higher perceived regulatory risk.

Another stain on Fiverr’s reputation is that, like many other tech companies of its ilk, it is loss-making.

Fiverr posted a net loss for 2018 of $36.1 million, compared to a net loss of $19.3 million in the prior year.

The lack of profitability is absorbed for the ultimate goal of gouging a total addressable market within the U.S. of $100 billion.

Fiverr's $82.5 million in trailing revenue is less than a third of fellow freelance platform operator Upwork (UPWK) at $263.1 million.

Uber (UBER) and Lyft (LYFT), ridesharing services, are considerably larger than that as Uber and Lyft command trailing top-line results of $11.8 billion and $2.5 billion, respectively.

Revenue expanded 45% last year and this year 42% annualized through the first three months of 2019.

Fiverr is growing faster than Upwork with just a 16% top-line gain in the first quarter and Uber which decelerated to a 20% increase in the same reporting period.

But all three gig-economy players still trail behind Lyft with its first-quarter revenue surge of 95%.

None of these companies are currently profitable.

Is it worth it to pay a premium for cash burners?

Fiverr, Upwork, Uber, and Lyft are fetching between six- and nine-times trailing revenue.

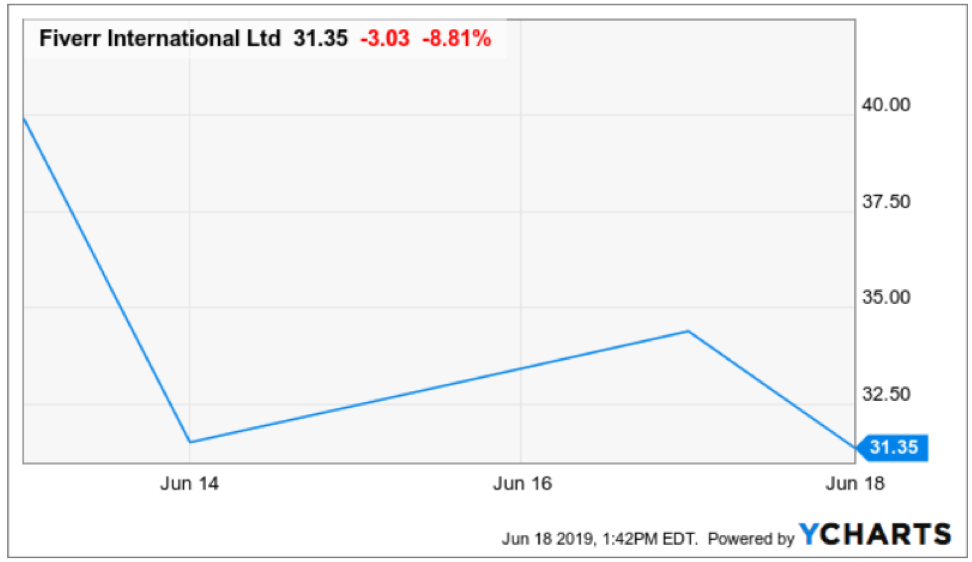

Fiverr shares are 50% above its IPO price after just two days of trading and is somewhat misleading but mister market is always right.

Lyft and Uber have been losers this year after going public and the jury is out to whether they are really worth a long-term duration trade.

It can be argued that Uber is a better bet long-term bet because of a bold aerial service that could eventually unlock massive value, but I would say its current model is somewhat underwhelming and could be called a fancy taxi service.

The best type of tech companies right now are software companies insulated from the turmoil of the trade war.

If you are interested in pure software companies, there are a handful of names out there that fit the bill, but if you are looking at a company attempting to crowbar itself into the idea of a software company then Fiverr is it.

That unflattering description is entirely justified as well.

Don’t forget they have real competition in the marketplace to supply freelance jobs in Upwork who has a bigger market share.

These type of broker apps do not have much pricing power and their only sell is the prospect of scaling as fast as possible meaning a volume play.

I can honestly ask, why buy Fiverr when there is a much better option out there?

The success of Fiverr is reliant on maintaining and expanding the scale of operations to generate a sufficient amount of revenue to offset the associated fixed and variable costs.

In my eyes, growing the number of users to benefit from the scale might happen after it does not exist anymore.

Investors must really ask themselves if gig workers will even be around in 8-10 years.

Why is that?

The gig economy is a battle down to zero and as tech companies become more sophisticated with expanding their artificial intelligence capabilities, it will remove the demand for gig economy taking away a huge swath of the addressable market with it.

This stock is a bet against artificial intelligence and the application of it, and if anyone has been reading this newsletter, they know it would be akin to throwing your hard-earned money down the toilet.

Specifically speaking, every cornerstone industry from national defense, consumer products, the trappings of Wall Street, industrial production, robotics, autonomous driving technology, and transportation is moving full speed ahead with implementing and harnessing artificial intelligence.

The technology isn’t quite there yet and humans are just a quick stop-gap until the optimal technology can be achieved.

Then it will be arrivederci to the human element, stripped away like my innocence in high school.

This is a bet on the upward trajectory of gig economy workers and the fate of them and that is a bad gamble to make long-term.

“10 to 20 years out, driving your car will be viewed as equivalently immoral as smoking cigarettes around other people is today.” – Said American Venture Capitalist Marc Andreessen

Mad Hedge Technology Letter

June 17, 2019

Fiat Lux

Featured Trade:

(THE FLIGHT PATH OF UBER)

(UBER)

If you want a bull out of the gate type technology stock, those are few and far between at this point in the late economic cycle.

There's another deep-lying value out there and a company who promises the stars and the moon is Uber who announced some eye-opening developments.

Uber Elevate, a division of Uber developing urban flight ridesharing, will have to hold on to its ridesharing business serviced by combustion engine-based cars for quite a while before the company can literally take flight.

This is the type of investment that used to only be reserved for venture capitalists, but Uber going public has given the average American a chance at staking out and holding one of the most controversial yet forward-thinking tech companies in the world.

If Uber can get this up and running, the underlying stock promises to become a ten bagger.

The United States-based subsidiary of the Embraer, EmbraerX, focuses on the development of disruptive businesses.

EmbraerX fundamental pillar is the formation of the future experience of air transport users.

Last week turned heads by debuting a small electric-powered vertical takeoff and landing (eVTOL) vehicle that should transform the future for Uber and other ridesharing companies.

The annual Uber Elevate conference in Washington, D.C. offered a glimmer of hope for Uber Elevate, the company is hellbent on realizing the holy grail of ridesharing transport transforming into autonomous flying vehicles.

A business model concocted with this input would pay dividends for a company who is doling out subsidies to gas-guzzling drivers on the road to service.

Yes, this is the future, but the future is here sooner than you think.

The EmbraerX eVTOL will only be able to handle a few passengers from the get-go.

Unfortunately, autonomous piloting will integrate into the process slowly.

The goal is for the vehicle to be absolutely autonomous according to the manufacturer aligning with Uber’s much-prophesized aim of going fully autonomous.

Dreams aside, there appear to be many technical issues with executing this transformation such as how will a new generation of flying Ubers prevent nonstop collisions above a city?

Uber has buddied up with an army of air traffic controllers, academics, pilots and industry experts to study this issue, while EmbraerX has proposed a pragmatic, simple and robust urban air space design to allow more aircraft to operate in urban environments.

Uber’s flying division plans on rolling out their service by 2023 which is an ambitious target, to say the least.

EmbraerX is partnering up with Uber to try and make this happen.

The locations of Los Angeles and Dallas have been pinpointed as places they plan to demonstrate flight capabilities next year.

The timeline is excruciating tight if Uber plans to get all their ducks in a row and make this a reality.

Uber has toyed with other launch locations such as Brazil, France, and India.

Other aircraft manufacturers are in the mix as well allowing Uber to diversify the risk in case EmbraerX can’t deliver the goods.

Similar air products are being crafted by Aurora Flight Sciences, a Boeing subsidiary, Bell and Karen Aircraft, and a Slovenian manufacturer named Pipistrel Vertical Solutions.

The entire premise behind the aerial ridesharing involves delivering a network of airports.

It will not morph into a door to-door service because a lack of capabilities on last mile deliverability that gas-based cars possess.

The concept of skyports or skystations have been bandied around and will theoretically force passengers to find their way to these launch stations to take advantage of aerial capabilities.

Uber could deliver a 2-1 service with road-based cars delivering the passengers to the sky stations all through the Uber app and a receiving a windfall of 100% of the transport revenues.

Uber is collaborating with renowned architectural and engineering firms on that piece of the project to solve complex challenges.

The sky stations must be built around commercial and retail hubs making this problem even more frustrating because the lack of infrastructure and crowded nature of these tight spaces means this project absolutely cannot fail.

Can you imagine a failed blighted sky port hanging above the retail and tourist mecca of Times Square in Manhattan?

Then there is the issue of these sky ports being monumental eye sores ruining picturesque skylines that many people hold dear to their heart.

The San Francisco skyline and the property owners with panoramic views would lose enormous property value if they were holed up next to an Uber aerial flight route.

The company has brainstormed around building on top of existing under-utilized urban structures like parking garages or even big box malls.

Some of the designers see them as providing not just takeoff and landing platforms for eVTOL vehicles, but an all-inclusive mix of retail, entertainment, and commercial with fitness clubs, supermarkets, and fine dining integrated into the concept similar to Tokyo subway stations.

In terms of time, the benefits would be compelling with flights able to cut commutes down from 2 hours to 15 minutes.

This type of time savings is applicable to megacities such as New York and the San Francisco Bay Area where many employees reside in outer suburbs to only commute into the heart of the city with their cars.

Shared flights would mitigate traffic on the ground giving a 3D solution to the massive traffic problem megacities face.

Meanwhile, as a way of dipping its toe into the waters of urban aerial transportation, Uber is due to launch a new service in New York City on July 9 that relies on an existing technology: helicopters.

The new Uber Copter service is by way of the Uber app allowing customers to call for helicopter rides between lower Manhattan and JFK Airport, pegged at a price of about $250 per person.

Times will be reserved for the afternoon rush hours on weekdays – and only for Platinum and Diamond members of the Uber Rewards loyalty program.

Newark-based HeliFlite will operate this part of Uber offering 5 seats per helicopter.

This test roll-out will give Uber valuable insight into the pitfalls of running an aerial transport network and long-term feasibility of it.

What does this mean for Uber?

Part of accessing the public markets was to supercharge their Uber Elevate division.

It is happening.

The company will be able to access the debt market to fund its deep-lying value divisions much like Google’s autonomous driving division Waymo has been financed by its parent company Alphabet.

Regulatory headwinds still represent a doozy of a thorn in its side.

There is a real chance of Uber Elevate being ready before the government is ready to allow them to flood the sky with aircrafts, and a 2-year delay suddenly grounding the planes with shareholders footing the costs will sap the momentum.

Facebook has grown uncontrollably for over a decade and the government still can’t get their finger out and figure out what to do.

A decade hiatus would be catastrophic for Uber Elevate as flight crashes have a more graphic consequence than personal data being hijacked.

I give Uber a 40% chance of creating a full-fledged, up and running aerial ridesharing service by 2023.

“As we move over to more of a mobile device-centric world... I think the interaction model with devices is going to be much more voice-based.” – Said CEO of Uber Dara Khosrowshahi

Mad Hedge Technology Letter

June 13, 2019

Fiat Lux

Featured Trade:

(THE TRADE WAR MOVES DOWN MARKET)

(DOCU), (PSTG), (ZUO), (MSFT), (PYPL), (ADBE)

To understand the consequences of the global trade war, just take a look at the second-tier software companies.

There has been softness in the latest earnings reports and guidance signaling a lukewarm upcoming summer.

The best-case scenario is the likes of DocuSign (DOCU) and Zuora (ZUO) rallying into the end of the year.

That is hardly a given considering the global turmoil has shifted supply chains in every which way as well as denting overall demand.

Cloud-based companies have seen meaningful weakness this earnings season, even some of them absorbing heavy losses in the wake of their quarterly results, but analysts aren’t ready to write off this industry yet.

Referencing the latest industry survey, 20 software companies reported results in the last month, and of those, only six saw a positive response in their stock prices.

DocuSign and Pure Storage (PSTG) were among names that got clobbered, along with cloud-computing plays like Cloudera Inc., Nutanix Inc., Box Inc., and Pivotal Software Inc.

The current malaise in software is due to higher valuations and macroeconomic issues which subsequently elevates uncertainty.

There is no reason to go hysterical over this, and in no way, shape, or form, does this signal an imminent implosion of cloud companies, any incremental caution may be reversible if macro indicators and sentiment rebound.

And this rebound can be swift once all the stars align together.

Adding to the comfort is that some of the sharp drawdowns were company-specific reasons.

MongoDB Inc. or Zscaler Inc., were coming off strong year-to-date advances in their shares and it was time to take profits before the next upward explosion.

Cybersecurity company Zscaler, is appropriately accounting for outperformance and have already been crushing higher than normal expectations.

DocuSign eclipsed expectations on some metrics but disappointed on others, such as billings growth.

This disappointing miss punished the company with a drop of 15% in the pre-market session, as DocuSign grew sales by 27%, a lower rate than in previous quarters.

Management blamed the poor performance to an elongated sales cycle.

Bulls were hoping for a beat-and-raise quarter and instead got in-line numbers with some soft spots around the periphery.

Investors aren’t in a charitable mood and the sensitive mood around geopolitics has made investors more agitated with a shorter leash.

There was a tone of a broader deceleration in software demand prompting stronger names to get comingled together, but the bulk of this negative price action has been overdone.

Even further down the pecking order, results from smaller cloud firms have pointed to more fundamental issues, and these stocks have emerged as a particularly weak sub-sector.

A number of these companies reigned in their forecasts, a trend that has buttressed analyst caution over the group.

Considering that many companies have labored and there exist clear narrative similarities, it’s hard not to surmise that some real systemic pains in infrastructure exist.

Many in the industry are acutely aware of the growing chorus of companies blaming competition or poor sales execution.

Lower growth rates are effectively the predominant reason for lower stock prices in this group of cloud companies.

On the flipside of this weaker cloud growth are the heavy hitters who are throwing around their weight getting through largely unscathed.

If any of these bigger cloud companies can fuse together a business model with no China exposure, then shares are likely stable to upward trending.

A company like Adobe (ADBE) is a perfect company to look at with an unpretentious yet steady growth rate and wildly successful products.

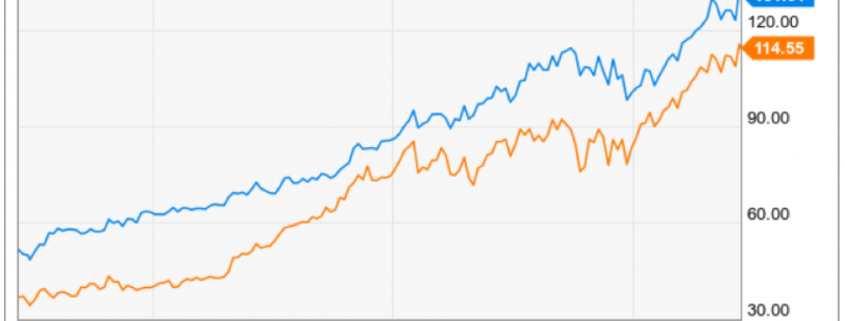

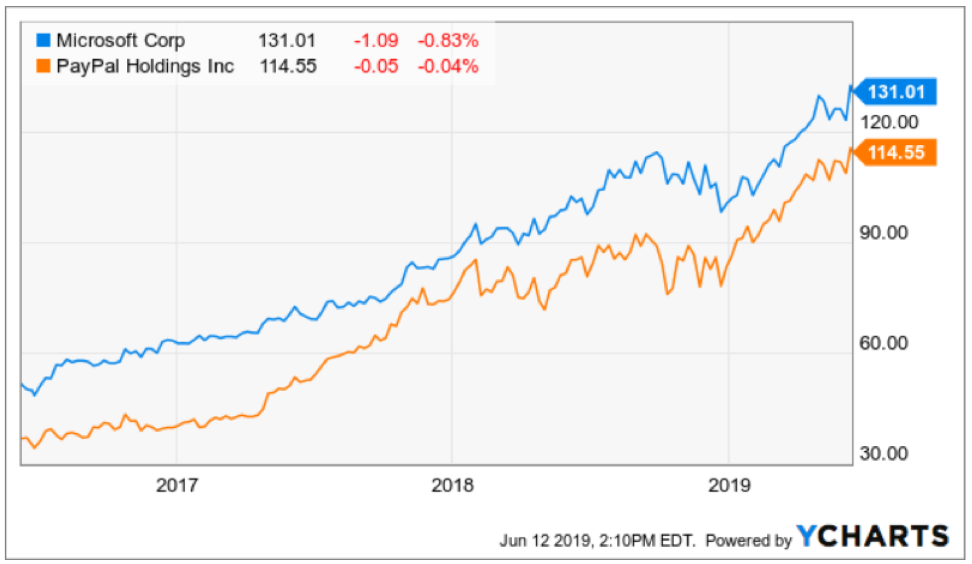

If we were to look at more growth-based companies with larger scale, then PayPal (PYPL) and Microsoft (MSFT) epitomize the type of cloud companies that are thriving in this environment and if geopolitics subsides, take on another 10% in sales.

Not only is the weather hot in the summer, but the anti-trust regulators are turning up the heat on certain tech companies on anti-trust concerns.

This could be a time to wait out those stocks and there could be another move to the upside if regulation is weaker than expected.

“There are two kinds of companies, those that work to try to charge more and those that work to charge less. We will be the second.” – Said Founder and CEO of Amazon Jeff Bezos

Mad Hedge Technology Letter

June 12, 2019

Fiat Lux

Featured Trade:

(STITCHING YOUR WAY TO PROFITS)

(SFIX)