Mad Hedge Technology Letter

May 13, 2019

Fiat Lux

Featured Trade:

(THE TIDAL WAVE OF EUROPEAN EV SUPPLY)

(TSLA)

Mad Hedge Technology Letter

May 13, 2019

Fiat Lux

Featured Trade:

(THE TIDAL WAVE OF EUROPEAN EV SUPPLY)

(TSLA)

It’s not Volkswagen’s first attempt at an all-electric car, but it’s certainly the most crucial attempt in their long history.

There have been iterations such as the e-Golf and other pure-electric vehicles before.

This time around, VW will debut the ID.3 and its new MEB platform.

The newest architecture for electric vehicles will be the lynchpin for several models across all of VW Group’s brands.

According to VW, “The architecture is aimed to consolidate electronic controls and reduce the number of microprocessors, advance the application of new driver-assistance technology and somewhat alter the way cars are built.”

The German company has committed $48 billion in car battery supplies too and plans to run 16 factories to build electric cars by the end of 2022.

At the lowest rung, there’ll be a battery expected to get around 205 miles and this ID.3 will be priced at under 30,000 euro ($33,650) before any subsidies or incentives.

In the middle, there’ll be an ID.3 capable of roughly 261 miles on a full charge which could mushroom into the most popular battery size.

Lastly, there’ll be a 342-mile battery option.

VW is certainly betting big on EVs along with its other in-house brands.

In March, VW announced it plans to launch 70 battery electric vehicles over the next decade and sell 22 million of them.

Previously, VW had said it would sell 15 million battery-electric vehicles by 2025.

The previous plan called for 25% of its global sales to be all-electric by 2025.

VW in-house brands are cranking up launches of new all-electric models.

Audi has started with the e-tron SUV and Porsche’s Taycan goes on sale in September.

VW brand’s I.D. and I.D. Crozz will appear next year while its subsidiaries like Skoda and SEAT are also going electric.

VW is not without its problems.

The recent charge by the European Union (EU) that it colluded with other German manufacturers to limit advances in clean emissions technology was another management misstep.

And the EU provides another challenge to all European carmakers with its harsh rules for 2020 fuel efficiency.

Recent research showed that it could cost VW up to 10 billion euros ($11.3 billion) in fines if it is unable to reduce its current fleet average of 123 grams per kilometer.

Cars like VW’s Audi e-tron offer zero reasons for consumers to buy, costing upwards of 70% more than conventionally powered equivalent vehicles.

The efficiency of the Audi is poor compared with Tesla models and the e-tron’s 95kWh battery offered a range of 2.5 miles per kWh, while the Tesla Model X managed 3.25 miles and the long-range Model 3, 4.13 miles.

Costs should come down substantially for vehicles deploying the MEB platform.

Theoretically, it’s the MEB platform that will serve further electric models going forward.

Yet, it’s highly possible the market is being overly optimistic that VW can deliver on its EV strategy and targets, which is the underlying thesis of the bull story.

VW’s lack of transformative structural improvements and its difficulties in making value-accretive strategic decisions that could unlock shareholder value means multiple upgrades in share price is less than probable.

Volkswagen is offering a Tesla style pre-booking to those who purchase an ID.3 and the possibility of charging electric power at no cost for the first year up to a maximum of 2,000 kWh at all public charging points connected to the Volkswagen charging app WeCharge and using the pan-European rapid charging network IONITY.

The ID.3 is to be delivered to customers in carbon-neutral form.

Production of the ID.3 1ST is to start as planned at the end of 2019 and the first vehicles will be delivered in mid-2020.

With its electric offensive, the Volkswagen brand plans to become the world's number one by 2025.

Mercedes is getting in on the act as well with the EQC Edition 1886 aiming to deliver 292 miles per charge and, with an output of 402 horsepower.

The metrics indicate that it will pose a direct threat to both Tesla's older Model X and upcoming Model Y.

The new Mercedes isn’t attacking the low-end of the market where Volkswagen hopes to apply pressure by offering the base version at 71,281 euros, or just short of $80,000, slightly less expensive than the e-tron quattro in Europe.

The new product from Mercedes qualifies for Germany's 4,000-euro federal tax incentive for EVs.

Ultimately, the avalanche of supply from the European high-end carmakers will heap more pressure on Tesla’s Elon Musk to deliver outperformance.

The entire pivot to EVs is predicated on millennials picking up the demand slack and buying into this story when the Baby Boomer generation did not.

By then, the stringent requirements from government and regulators in tackling climate change by itself might offer a massive customer base to tap into EVs whether they like it or not.

EVs have come a long way since the Chevy Bolt, but it’s far from certain that the Europeans will destroy Tesla, but the new developments will sap German demand for Tesla’s car with a domestic alternative.

“It's OK to have your eggs in one basket as long as you control what happens to that basket.” – Said Founder and CEO of Tesla Elon Musk

Mad Hedge Technology Letter

May 9, 2019

Fiat Lux

Featured Trade:

(APEX LEGENDS TO THE RESCUE)

(EA)

Fortnite roiled the video gaming industry last year reinventing the landscape with its freemium model that is available on every platform.

Its in-game add-on revenue strategy is the new model going forward and the first major video game studio to adapt to the new status quo is Electronics Arts Inc. (EA).

The successful earnings report by a newly minted super growth driver and Fortnite competitor called Apex Legends.

Apex Legends copied Fortnite with its 'Battle Royale' format incurring outsized user growth.

Overall, EA’s player base grew to more than 500 million active player accounts in 2019.

This was driven by engagement in the top franchises and live services on major platforms, the game-changing introduction of new IP, including the free-to-play game Apex Legends, offering reach to new audiences around the world is the crux behind short-term bullish momentum in the stock.

Other releases such as "Star Wars Jedi: Fallen Order" will provide another boost to sales momentum as well.

The sports side of the company is also working miracles in a year where both FIFA 18, including World Cup content and FIFA 19 with the UEFA Champions League, had more than 45 million unique players in total playing FIFA games on console and PC.

More than 100 million players engaged with EA’s FIFA franchises on mobile and PC free-to-play during the year as well.

Given investor paralysis across the video game space about revenue stability, competitive moat, and changing revenue models, the predictability and stability of sports demonstrates the breadth of EA’s asset.

Apex Legends is the fastest-growing new game in the history of EA quickly reaching a milestone 50 million players and millions more have continued to participate.

It has also helped EA accumulate new player audiences as nearly 30% of Apex Legends players are new to EA.

The plan for Apex Legends is to deliver this massive global community with a long-term live service, including new seasons with more robust Battle Pass content, new legends and exciting evolutions to the in-game environment.

EA is collaborating aggressively to bring the game to more players in more markets and platforms around the world, including Korea, to take advantage of an opportunity in the market and self-publish Apex Legends via Origin.

EA expects $300 million to $400 million in net bookings for Apex Legends in the fiscal year that ends next March, though that projection doesn’t take into account potential contributions from a mobile version of the game or a version for the Chinese market.

Annual targets were met with GAAP net revenue for the fiscal year registering $4.95 billion delivering EPS of $3.33.

These results enabled EA to deliver an operating cash flow of $1.55 billion and return over $1 billion to shareholders, about 83% of free cash flow, through the ongoing share repurchase program.

The prior quarter was a robust one with EA beating on the top and bottom line.

EA easily beat on the top line with GAAP net revenue for the quarter coming in at $1.24 billion, shattering guidance by $75 million.

Turning to the key catalysts of this quarter, net bookings were $1.36 billion, well above guidance of $1.17 billion, and up from $1.26 billion last year.

To reiterate, the beat was driven by Apex Legends and the outperformance in the blockbuster sports titles.

Digital net bookings were $1.19 billion, up 14% on the year-ago period, driven by strong digital sales of Apex Legends and Anthem.

Digital net bookings represented 75% of the business on a trailing 12-month basis, a new record compared to 68% in the prior year.

Live services net bookings were up 24% to $845 million, primarily driven by Apex Legends.

Live services at EA delivered its best year on record with FIFA and Madden Ultimate Teams both closed the year very strongly.

The gaming environment shows no let up in dollar terms, expect the gaming software market to grow 7% over the calendar year, with mobile up 12%, console up 4% and PC flat.

Estimates for 2020 is for net revenues of $5.4 billion, and cost of revenue of $1.3 billion and EPS of $8.56.

Gaming is still a hot part of tech and after 2018 that crushed Fortnite competition, EA should hold its own with Apex Legends and the strength of its sports franchises.

Shares are up over 20% this year and have more room to the upside.

“Capitalism has worked very well. Anyone who wants to move to North Korea is welcome.” – Said Co-Founder and Former CEO of Microsoft Bill Gates

Mad Hedge Technology Letter

May 8, 2019

Fiat Lux

Featured Trade:

(ELBOWED OUT OF THE WAY BY APPLE)

(SPOT), (AAPL)

I have turned bearish on online music streaming platform Spotify (SPOT) who have grumbled to EU about the charges they must pay Apple for selling through the Apple (AAPL) app store.

The charge reduces to 15% after 1 year but initially start at 30%.

These are the perils of not possessing your own proprietary platform, needing to jump through hoops to receive access to the lucrative North American market.

3rd party companies must oblige and pay the commissions or seek business elsewhere.

If the situation were the other way around, Spotify would charge Apple.

I hardly feel bad for Spotify, but Apple doubling down on the services story spells trouble for Spotify.

If they think competition is brutal now, Apple is certain to make life harder to sell through the Apple store when actively promoting a direct competitor through Apple music.

Much of the gloss is being rubbed off of Spotify who are trying harder these days just to tread water.

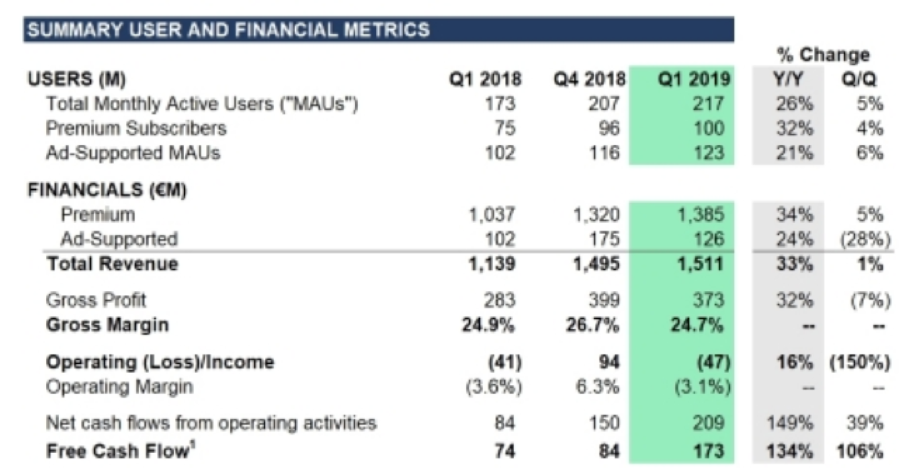

The company reported total Q1 revenue of $1.69 billion (€1.511 billion), eclipsing analysts’ expectations of $1.64 billion.

That was the good, now some of the bad.

Spotify posted a net loss of $158 million (€142 million), versus a net loss of €169 million ($189 million) in the year-earlier period.

The net loss of 88 cents per share (€0.79) missed consensus EPS of 39 cents (€0.35), a wayward miss that epitomizes the inherent problems with this unprofitable business model.

The numbers revealed that Spotify was overextending itself to acquire incremental revenue and is unable to generate the high-quality growth that tech companies relish.

According to Spotify, Q1 headwinds consisted of “significantly increased operating expenses” and much of that has to do with the exorbitant royalty expenses doled out to the music industry.

When a company goes the route of cheap tricks like nonsensical promotions to boost revenue, there is a material risk that customers won’t retain subscription at higher price points after the promotions drop off.

The EPS miss was horrid, but Spotify did deliver on its growth estimates delivering 26% YOY growth in Monthly Active Users (MAUs) to 217 million, slightly lower than the midpoint of the company’s guidance range of 215-220 million MAU.

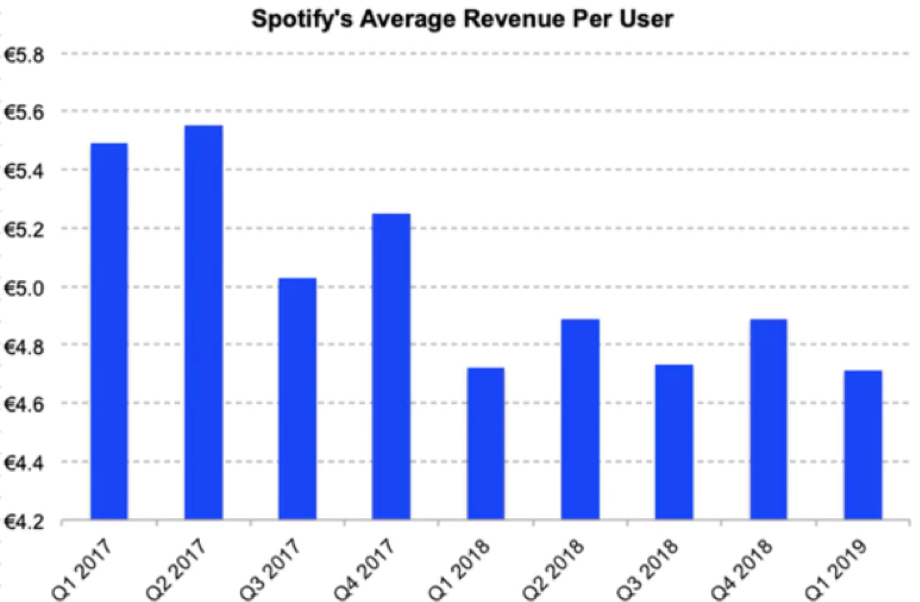

Another cavity emitting pain from the mouth was Average Revenue Per User (ARPU) of only EUR4.71, roughly flat from the prior year.

Spotify has experienced a deceleration in ARPU due to shifts in product and geographic mix.

The company believes the downward pressure on ARPU has moderated and now hopes ARPU declines through the remainder of the year to be in the low single digits.

The inability to accelerate the ARPU tells us that the product’s viability in the lucrative North American market could be waning and thawing out North American revenue drivers won’t automatically guarantee a renaissance in higher ARPU.

This could be the new normal with the company presiding over lower ARPU and a big part of that stems from its penetration into lower-income countries such as India.

In February, Spotify launched its service in India and has racked up over 2 million users in the country. The company’s global market footprint now impressively spans 79 countries.

Spotify’s key areas of growth during the quarter were measurement and programmatic revenues.

Measurement-related revenues doubled from 20% to 40% of total ad revenues year-over-year.

Programmatic and Self-Serve grew 53% from last year and now account for 26% of total ad-supported revenue.

Premium subscribers increased 32% year-over-year to 100 million, reaching the high end of the 97-100 million guidance.

The outperformance was aided by a better than plan promotion in the US and Canada and continued expansion in Family Plan.

For next quarter, Spotify expects revenue to grow 18-35% YOY to EUR1.51 billion to EUR1.71 billion.

Total MAUs are expected to increase 23-27% year-over-year with the premium segment boosted by 29-34% to EUR107-110 million.

“Competition is really not a big factor for us,” CEO Daniel Ek who chimed in on the earnings call.

This couldn’t be further from the truth with Spotify unhappy that Apple is charging them 30% commission to sell from the Apple app store which all boils down to stifling the competition.

Apple has made it clear to investors that ramping up service growth is one of the key pillars to Apple’s story, and music will be a cornerstone of the service transformation.

Competition will heat up creating a more fractious relationship between Apple and penetrating the Android users won’t cut it.

Spotify still hasn’t offered investors an intriguing way to put the kibosh on royalty expenses and in the near future, Spotify will need to prove they can increase margins which I believe they won’t.

My bet is that operating margins are squeezed, cash burn increases, EPS goes further south and the stock show softness in the near-term.

“Spotify is a platform: it could be expanded to other types of content.” – Said CEO of Spotify Daniel Ek

Mad Hedge Technology Letter

May 7, 2019

Fiat Lux

Featured Trade:

(THE LURKING DANGERS BEHIND FACEBOOK)

(FB), (WFC), (NFLX)