Mad Hedge Technology Letter

January 7, 2019

Fiat Lux

Featured Trade:

(NOT TOO GOOD TO BE TRUE),

(SCHW), (FB), (SQ), (WMT), (AMZN), (FFIDX), (BOX)

Mad Hedge Technology Letter

January 7, 2019

Fiat Lux

Featured Trade:

(NOT TOO GOOD TO BE TRUE),

(SCHW), (FB), (SQ), (WMT), (AMZN), (FFIDX), (BOX)

It seems time after time, entire industries get flipped on their heads without notice.

The modern-day hyper-acceleration of technology is creating tectonic shifts in the economy that only some can truly understand.

There is the good, the bad, and the ugly.

The functionality of technology has helped enhance our daily lives infinitely, yet there is a dark side of technology that has reared its ugly head threatening the future existence of mankind.

One industry next in line to be smashed to bits will have the effect of unimaginably reshaping Wall Street as we know it.

Gone are the days of brokers shouting from the trading pits, a bygone era where pimple-faced traders cut their teeth rubbing shoulders with the journeymen of yore.

The stock brokerage industry is at an inflection point with the revolutionary online stock brokerage Robinhood on the verge of shaking up an industry that has needed shaking up for years.

A common thread revisited by this newsletter is the phenomenon of broker apps being low-quality tech.

These apps can be built by a pimple-faced freshman college student in his dorm.

A broker ultimately serves little or no value to the real players among the deal, usually extracting huge commissions.

Technology and now blockchain technology vie to completely remove this exorbitant layer from the business process.

Well, for the stock brokerage industry, that time is now.

Robinhood is an online stock brokerage company based in Menlo Park, Calif., trading an assortment of asset classes including equities, options, and cryptocurrencies.

So, what's the catch?

Robinhood does not charge commission.

That's right, you can invest up until the $500,000 threshold protected by the Securities Investor Protection Corporation (SIPC) and you can go along with your merry day trading for free.

The online brokerage industry has been getting away with murder for years.

How did the online brokers get away with this in a technological climate where industries such as the transportation sector are being flipped on their head?

They got comfortable and stopped innovating - the death knell of any company.

Effectively, high execution costs reaping massive profits were the norm for brokers, and nobody questioned this philosophy until Robinhood exposed the ugly truth - unreasonably high rates.

Peeking at a monthly chart of brokerage costs will make your stomach churn.

For instance, a trader frequently executing trades with an account of $100,000 would hand over $1836 in commission in 2017 if their account was with Fidelity.

On the cheaper side, Interactive Brokers would charge $854 for its brokerage services to habitual traders per month.

The outlier was Tradier, a start-up brokerage founded in 2014 using the powerful tool of an API (Application Programming Interface) which charged $213 per month to trade frequently.

An API is described as a software intermediary allowing two applications to communicate with each other.

This model helped cut costs for the online brokerage because Tradier did not have to focus its funds on the trading platform that was delegated to various third-party platforms.

Tradier is largely responsible for the aggregation of data and charts thus employing an army of developers to meet their end of the business.

This model is truly the democratization of the online brokerage industry, which has been coming for years.

Costs are cut to a minimum with equity trades at Tradier costing investors $3.49 per order and options contracts costing $0.35 per contract with a $9 options assignment and exercise fee.

Technology has defeated the traditionalist again.

Day traders will tell you their largest worry is keeping a lid on execution costs.

Volume traders plan their strategies according to bare bones commission.

Marrying technology with online brokerages has the deflation effect that Amazon (AMZN) deftly took advantage of perfection.

Brokerages do not pay higher costs for an incremental bump in trading volume. Costs are mainly fixed.

If you hold a trading account in one of these legacy brokers charging an arm and a leg to trade with them, jump ship and join the revolution.

So how does Robinhood generate revenue if the broker trades for free?

Hawk ads? No.

They are not rogue ad sellers such as Facebook (FB).

The plethora of accounts opened with Robinhood earn interest, and Robinhood collects the earned interest as revenue.

Also, Robinhood has one paid service for sale.

Robinhood Gold is a subscription allowing traders to use margin. The margin accounts will set traders back $10 per month adding up to $120 per year, and they won't be charged interest on the funds.

This is peanuts compared to what other traditional brokerages are charging clients for margin account interest.

This is also a data grab with the proprietary data building up profusely turning into a potential Masayoshi Son SoftBank Vision fund acquisition.

Robinhood has almost registered a staggering 6 million accounts since 2013 – a staggering feat for an unknown and the momentum is palpable.

The meteoric rise of Robinhood coincided with the explosion of the price of bitcoin breaching the $20,000 level.

This price surge inspired a whole generation of millennials to get off the sofa and start trading cryptocurrencies.

More than 80% of Robinhood's accounts are owned by millennials – as expected.

Trading cryptocurrencies act as a gateway asset to springboard into other asset classes such as equities and derivative contracts.

Vlad Tenev, co-CEO of Robinhood, indicated that Robinhood will have to modify its radical business model to monetize more of the business in the future, but he is comfortable with the current business model.

But Tenev has already seen fruit borne with the likes of Robinhood applying fierce pressure to the legacy brokerages' pricing models.

The traditionalists are locked in a vicious pricing war with each other slashing their commission rates to stay competitive.

The longer the likes of Charles Schwab (SCHW) feel it necessary to charge $4.95, down from the January 2017 cost of $8.95, the better the chances are that Robinhood can build its account base rapidly.

Charles Schwab has more than 10 million accounts, only double the number of Robinhood, after being founded in 1971.

The 42-year head start over Robinhood has not produced the desired effect, and it is ill-prepared to battle these tech companies that enter the fray.

Robinhood has been able to add a million new accounts per year. If Charles Schwab relatively performed at the same rate, it would have 47 million accounts open today.

It doesn't and that is a problem because the company can be caught up to.

The lack of urgency to combat the tech threat is astounding. Companies such as Walmart (WMT) have taken the initiative to transform the narrative with great success.

The race to zero is a grim reality for the Fidelities (FFIDX) of the world, and adopting a Robinhood approach will be the playbook going forward.

Brokerages and a slew of other industries are turning into a legion of top-level developers fighting tooth and nail to stay relevant.

The transportation industry has grappled with this harsh reality lately, but the economy is on the cusp of many other industries digitizing to the extreme.

My guess is that Robinhood starts rolling out a slew of subscription services catering toward specific investors.

The age of specialization is upon us with full force, and customer demand requires care and diligence that never existed before.

Robinhood continues to enhance its offerings of various products adding Litecoin and Bitcoin Cash to the crypto lineup.

Only Bitcoin and Ethereum were offered before.

And there is one more outrageous thing I forget to tell you.

Robinhood is in the midst of going after traditional savings accounts by offering checking and savings accounts offering an interest rate almost 30 times larger than most brick and mortar banks – 3%.

These accounts would have no minimum balances or no fees that nickel and dime customers.

The service will conveniently sit alongside its trading app and this move into the industry led by JP Morgan could start to derail Wall Street.

As with most FinTech start-ups, the roll-out of this new service was slightly botched because Robinhood failed to get the go-ahead from regulators concerning ensuring the accounts properly.

All this does is delay the inevitable and by spring 2019, potential customers should be earning 3% in Robinhood’s checking and savings account.

Sign me up!

The company is not without headline investors boasting the likes of Andreessen Horowitz, the venture capitalist firm based in Menlo Park, Calif., Box (BOX) CEO Aaron Levie, and hip-hop mogul Snoop Dogg.

Expect Robinhood to pile the funds into improving the technology, data accuracy while offering more hybrid products.

The enhancements will attract another wave of adopters spawning another wave of panic from the legacy brokers.

All of this explains how Robinhood snapped up 6 million users and almost a $6 billion valuation in only 5 years – if the Batman of FinTech innovation is Square (SQ) then Robinhood is seriously the Robin of innovation at the same time.

To visit the pricing information at Robinhood, please click here.

"When something is important enough, you do it even if the odds are not in your favor." - said Tesla founder and CEO Elon Musk.

Mad Hedge Technology Letter

January 3, 2019

Fiat Lux

Featured Trade:

(HOW TO TAKE OVER THE WORLD),

(SFTBY), (BABA), (NVDA)

The wild west of the data wars is spawning into an all-out, gunslinging shoot-out with a winner-takes-all mentality.

This slugfest is reminiscent of the unregulated 19th-century American oil barons whose clout and complete control of the supply of oil fueled the industrial revolution that drove America's economy to the top of the global food chain.

Yes, data has become the oil of the 21st century. It is the oxygen of the next leg of the Internet revolution.

And there is one man moving early to stake out the premium real estate of our futures: SoftBank's Masayoshi Son.

His $100 billion SoftBank Vision Fund is not only creating waves in Silicon Valley but tidal waves.

Many countries, such as Iran, Saudi Arabia, and Russia, still rely on petroleum for the lion's share of government revenues. Saudi Arabia is attempting to wean themselves from the reliance on oil, but teething pains are sprouting up everywhere.

The choreographed killing of former Saudi Arabian dissident Jamal Khashoggi at a Saudi Arabian Embassy in Turkey will have many unintended consequences to the future economy further delaying the supposed pivot to a legitimate knowledge economy.

Oil prices crashing offers less financial support to make this pivot even possible.

Even though oil is still integral to the growth of the global economy, there is a new sheriff in town: big data.

Cut it up any way you want, data is simply information, the "zeros" and "ones" that make up the digital world. The information that commands mouthwatering premiums these days can be unraveled by computers.

Computer-deciphered data can show behavioral and consumer trends in stark daylight, helping companies ferret out business strategies that are proving immensely powerful.

There is an exponential hockey stick effect going on here. As the quantity of data accumulates, the more valuable it becomes.

The types of data being collected are personal data, transactional data, web data, and sensor data used for IoT (Internet of Things) products.

Who is the major player vacuuming up this data?

Masayoshi Son, the CEO of SoftBank (SFTBY), is an ethnic Korean who grew up in a small village in Japan. He transferred to Serramonte High School on the San Francisco Peninsula as a bustling youth and graduated in three weeks.

He was and still is that brilliant.

Son ventured on to UC Berkeley majoring in economics and computer science. He is one of the most dynamic people in the world and has amassed personal wealth of around $25 billion.

A few of his brilliant preemptive strikes were seed-investing in Yahoo, creating Yahoo Japan, and a $20 million for a stake in Alibaba (BABA) in 1999. These investments increased more than 100-fold in value.

Son is on a mission to own or control assets that are the linchpin to global growth nourished by Artificial Intelligence in selective industries such as transportation, food, work, medicine, and finance.

The solid anchor that ties all these firms together is the massive hordes of harvested data which are central to directing how future automated robots and machines perform.

His goal envisions the construction of responsive robots that will emerge as the cash cow in 2045. The construction, utilization, and high performance of these machines will be the key to his vision.

Instead of splurging for premium human data, investors will be competing for the best performing robots and the data derived from them. Accurate human data will provide the springboard to the machine data these robots will generate.

After the first generation of robots endows us with their first batch of data, all human data will be irrelevant. Human information is the test case on which robots are founded.

Once the first cohort of robot data comes to market, the second generation of robots will be derived off the first generation of robots.

Humans and the data generated from us will become irrelevant.

Once you marry the treasure trove of data with A.I., the results will enter the realm of today's science fiction. Imagine being the first CEO to bring functional robots to mass market and how valuable that first tranche of robot data would represent.

Priceless.

Son is positioning himself to organically engineer the highest-grade robots catalyzing the next gap up in global competition.

This year, Son is on a global treasure hunt to meld together the most precise "big data" he requires to build his robot squadron that will take over the world.

The fight these days is acquiring the oxygen to power these non-human contraptions. Without pure oxygen, i.e. massive amounts of data, engineers will create faulty, error-prone robots that underperform and are less valuable.

Looking at the amalgam of companies in which Son has bet on, it is difficult to decipher any rhyme or reason. That is until you find the commonality of big data.

Son invested $200 million in "Plenty" in July 2017, a company developing indoor farms. If indoor farm data is not diverse enough, then how about the $300 million he showered on the San Francisco dog-walking app called "Wag."

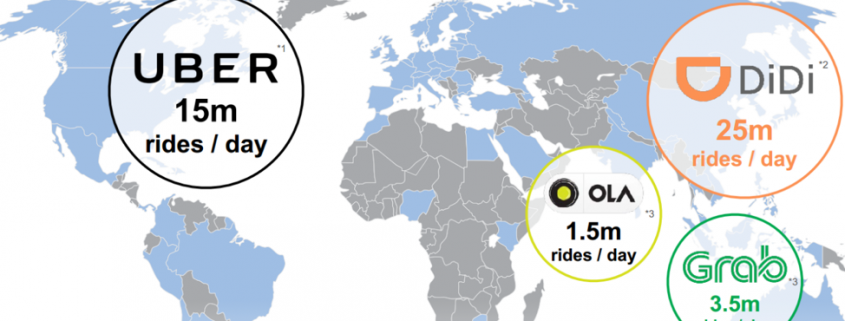

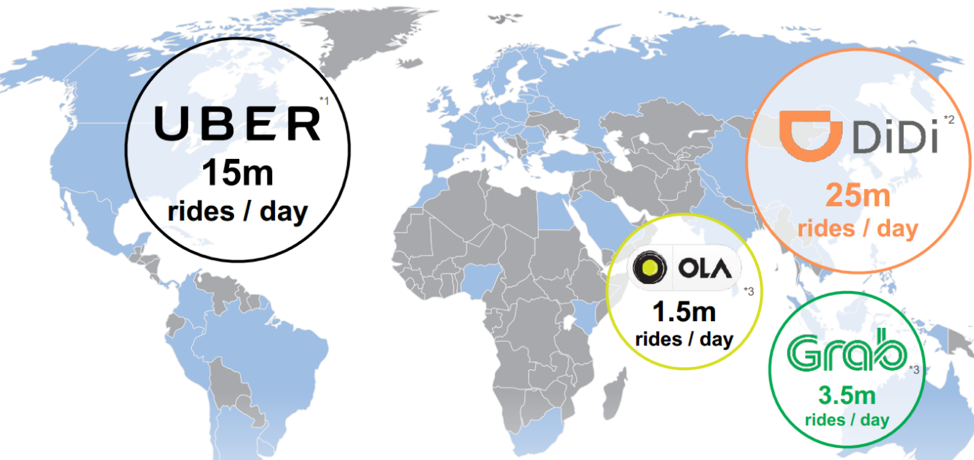

The biggest holding in the SoftBank Vision Fund is Uber. For those without an Internet connection, Uber is ubiquitously known as a ride-sharing company that shuttles passengers from spot A to spot B.

Sweetening the deal was a substantial discount the Vision Fund received on a private placement of Uber shares. Uber is now worth about $70 billion and may someday become a FANG in its own right.

Supplementing this transaction is the custom online map app Mapbox, founded as a competitor to Google Maps. Some of Mapbox's partners include Snapchat, Lonely Planet, and The Weather Channel.

Vision Fund's second largest position is ARM Holdings which is an English semiconductor chip company that has carved out a large segment of the Android and laptop market.

It produces simple CPUs (central processing units) and much more advanced GPUs (graphics processing units) that are placed in smartphones, TVs, tablets, and computers.

Son has shelled out $8.2 billion through the SoftBank Vision Fund already, and the remaining 75% stake is owned by parent company SoftBank Group. ARM is one of the shining beacons of European tech and SoftBank has pegged its future to its success.

There are even whispers of a second $100 billion vision fund lurking around the corner.

Unsurprisingly, Nvidia (NVDA) is the third-largest weighting, and the $5 billion SoftBank investment into Nvidia (NVDA) represents a 4.9% stake in the company. The Nvidia commitment is logical considering ARM licenses its chip designs to Nvidia.

As autonomous vehicles will be one of the first benefactors from the cross-pollination between big data and automation, these investments completely justify Son's long-term vision.

Son has also snapped up other ride-sharing entities such as Didi Chuxing in China, Ola in India, Grab in Southeast Asia, and 99 in Brazil.

Some 31% of the global population is without Internet connectivity. Thus, Son bought OneWeb which pioneers low-cost, high-quality satellites striving to grant Internet access for the people still without access. This maneuver will surely see his net data load increase.

In many of the Mad Hedge Technology Letters, we often offer readers the creme de la creme of public stock symbols, but this time it is different.

First, the major holdings in the SoftBank vision fund, aside from Nvidia, are privately held companies that do not trade on any stock market.

However, it is very important to watch what he buys as it gives insights into the best-performing, fastest-growing sub-sectors of technology and a comprehensive barometer or tech risk appetite from higher echelon VCs.

Or you could just buy SoftBank itself whose shares have doubled over the past two years.

Giving further color to the backstory, not all is doom and gloom for Saudi Arabia as they have invested heavily into the Vision Fund giving Son a key source of financing.

Son’s relationship with the Saudis is important to spearheading a 2nd Vision Fund which he hopes to deploy shortly.

Readers must not forget that 40% of the $100 billion constitutes debt and must be serviced forcing Son to supercharge the growth of the companies he purchases to maintenance his monthly debt bills.

Son won't just flip these companies for a 30% or 50% profit. Tenfold, or hundred-fold gains are the order of the day and that is exactly what he has been successful at.

In reality, Son's ultimate goal is to leach out the future aggregate data spewing from his underlying portfolio and cross-pollinate it with A.I. and automation to revolutionize the world while becoming the richest man in the world.

As 5G is literally on our doorstep, Son, large tech firms, China, and the rest of the VC universe are jockeying with each other and staunchly positioning themselves accordingly for the next 30, 40 and 50 years.

Welcome to the future and good luck.

"It would take enormous expertise for Amazon to win in every category. Do you think McDonald's could be number one in hamburgers, seafood, and Chinese food?" - said SoftBank CEO Masayoshi Son.

Mad Hedge Technology Letter

January 2, 2019

Fiat Lux

Featured Trade:

(THE FANGS' PATH TO ONLINE BANKING),

(SQ), (V), (MA), (AXP), (JPM)

Yu'e Bao or "leftover treasure" in English has caught the attention of more than 400 million Chinese investors.

This money market fund has exponentially grown into a $250 billion fund by the end of 2017, and is now the largest money market fund in the world!

This product isn't offered by Bank of China or another giant state-owned bank or financial enterprise, but Alibaba's (BABA) Ant Financial (gotta love those Chinese names).

Assets under management are up 100% YOY and it now accounts for a quarter of China's money-market mutual fund industry in just one fund.

These inflows coincide with the sudden migration into mobile payments. Common folks are comfortable with investing their life savings in these short-term instruments with a too-big-to-fail, larger-than-life firm such as Alibaba.

Yu'e Bao derives its funds from Alipay users, Alibaba's digital third-party platform, that allows consumers to pay for everything in life from theater tickets to utility bills.

Service is unified on a holistic graphic interface. Users can easily divert cash into this fund with a few screen taps on their app. Yu'e Bao's ROI offers a seven-day annualized yield of 4.02%, down from the introductory annualized rate of 6.9% around the launch in 2013.

Yu'e Bao's short-term yield outmuscles the 1.5% interest rate on one-year Chinese bank deposits and the 3.6% yield on 10-year Chinese government debt.

Weak banking regulation has spawned a mammoth FinTech (financial technology) industry in the Middle Kingdom. Only one yuan (16 cents) is enough to create an account and considerable retail flow has rushed in.

China has catapulted ahead of the rest of the world emerging as the leader of global FinTech innovation. The pace, sophistication, and scale of development of China's FinTech have surpassed the level in any other of the developed countries.

The country's digital metamorphosis has enhanced e-commerce, payment systems, and connected logistical services. The Chinese discretionary spender for the past decade has been the deepest and most reliable lever of global growth.

Mobile third-party payments in China, 90% cornered by Tencent's WeChat and Alibaba's Alipay, are estimated to reach a lofty $6 trillion in revenue by 2019, more than 50 times that of the U.S.

These omnipresent payment systems are now deeply embedded into the fabric of Chinese society. It's common to witness homeless people on Shanghai subways waving around a scannable image for WeChat or Alipay money transfers instead of asking for physical cash.

Even in rural farmlands, shabby convenience stores prioritize digital currency and sometimes don't accept paper currency at all. Yes, China is beating the U.S. to a cashless society.

Digitization is changing the competitive balance, and global banks must embrace large-scale disruption caused by big tech platforms.

Banks in China regard these companies as potential collaborators resulting in a net positive long-term infusion of enhanced products and services.

Agreements have been forged between the Bank of China and Tencent, and the China Construction Bank has linked up with Alibaba.

China has incorporated the technical power of A.I. (artificial intelligence) and machine learning into its FinTech platforms at every opportunity. Robo-advisors are also making inroads creating a bespoke financial program for the individual.

This trend has so far failed to go viral in America where individuals still prefer plastic cards or even paper cash. E-commerce clocked in a paltry 9.1% of total U.S. retail sales in the third quarter of 2017.

Even though most of us have our heads buried deep in our smartphone virtual world, Americans are still programmed to whip out debit or credit cards at every opportunity.

Chinese who visit America carp endlessly about America's archaic payment system.

Ultimately, American payment systems are ripe for digital disruption.

The American consumer will ultimately cause severe damage to MasterCard (MA), Visa (V), and American Express (AXP) which are happy with the current status quo.

The lack of innovation in the US FinTech sector is a failure in the otherwise fabulous technological leadership of the US. American smartphones should already be a fertile digital wallet, not just a niche market.

Savvy Jack Dorsey even invented a firm based on this inefficiency exploiting the lack of proficiency in domestic FinTech with Square (SQ).

And a vital reason the stock has gone parabolic this year is because of the brisk execution and the long runway ahead in this industry.

American big tech will gradually utilize China's FinTech model and extrapolate it with "American personality." It is much more of a two-way street now than before with cutting-edge ideas flowing both ways.

The next leg up after digital wallet penetration of FinTech is money market funds on tech platforms. In effect, the Chinese innovation of this industry has allowed more variations of potential financing for the ambitious Chinese, and the same trends will gradually appear on Yankee shores.

Ironically enough, Amazon's (AMZN) land grab strategy is more prevalent in China as artificially low financing and juicier scale justify this strategy.

The scaling premium also explains why corporate China's early adopter advantage is so effective because not many countries boast a 1.3-billion-person consumer market.

Soon, Americans will wake up to the reality that American FinTech must advance or foreign firms will rush in.

Mediocrity is not good enough.

iPhones and Android consumers could direct savings into tech money market funds with compounding yield all on a single digital platform.

Tech companies could deploy some of the repatriated cash to invest in some fledgling FinTech expertise to smoothly execute this new endeavor.

Consequently, a successfully created money market fund on a tech platform would enlarge the already substantial cash hoard these firms possess. Not only will the large tech companies flourish, but the big will get absolutely massive.

The determining factor is financial regulation. Capitol Hill has drawn a large swath of mighty Silicon Valley tech titans to testify because they are stepping on too many toes lately.

A scheme to hijack the digital payments market and dominate the mutual fund industry will cause unyielding push back in Washington especially when the Amazon death star continues pillaging select industries of their choosing and eliminating brick-and-mortar jobs by the millions.

J.P. Morgan (JPM) which has the largest institutional money market fund in the country and retail stalwarts such as BlackRock and Vanguard will be sweating profusely too if mega tech starts probing around its turf.

Alibaba is also coming for its bacon with the failed purchase of payment transfer service MoneyGram International (MGI) temporarily shutting out Jack Ma from a foothold in the American payment system industry.

And if the Chinese aren't let in, there will be others sniffing around for the bacon, too.

The momentum for these financial instruments is robust as FinTech integrates deeper into consumer life. The global cash glut from a decade of cheap financing is causing profit-hungry investors to starve for high-yield vehicles.

The stability and clean balance sheets of tech giants give them ample chance to successfully execute. So, why can't they also become banks? Would you buy an Apple, Amazon, or Google money market fund if they offered a 4% to 7% annualized yield?

I believe most Americans would.

"If you're gonna make connections which are innovative... you have to not have the same bag of experiences as everyone else does," - said the former co-founder of Apple, Steve Jobs.

Mad Hedge Technology Letter

December 31, 2018

Fiat Lux

Featured Trade:

(NEWSPAPERS REALLY KNOW WHO YOU ARE),

(TPCO), (AMZN), (FB), (GOOGL), (USPS), (SFTBY)