“A company shouldn’t get addicted to being shiny, because shiny doesn’t last.” – Said Founder and CEO of Amazon Jeff Bezos

“A company shouldn’t get addicted to being shiny, because shiny doesn’t last.” – Said Founder and CEO of Amazon Jeff Bezos

Mad Hedge Technology Letter

December 19, 2018

Fiat Lux

Featured Trade:

(HOW TECH IS EATING INTO HEALTHCARE COSTS)

(VEEV), (CRM), (GSK), (AZN), (MRK), (NVS), (DBX), (OKTA), (TWLO)

It’s undeniable that American healthcare costs are a big part of a family’s monthly expenses.

Rising deductibles and out-of-network fees are a few of the out-of-pocket costs that can singe a hole in the average joes’ pocket.

It was only in 2016 when healthcare insurance costs eclipsed more than $10,000 a year per person, and over the past 12 months, 68% of people surveyed admitted that future healthcare costs would probably consume a larger part of their earnings.

The result is that healthcare companies are making money hand over fist.

Is there something that I deduce from this lucrative part of the economy that has the potential to feed into the tech sector?

The tidal wave of money spilling into the healthcare industry has also given impetus to these firms hoping to buttress their networks and IT with modern tech infrastructure to take advantage of the efficiencies on offer.

Building the best cloud services geared towards specific industries has been a winning formula and the generated momentum will continue into the next calendar year.

Prime models can be seen all over the tech ecosphere and they will be big winners of 2019.

One example is Twilio (TWLO) who has quietly risen the bar for communication cloud products.

A panoply of small companies can now offer professionalized email, text message, automated voice mail services amongst other services that do the work of 100 employees.

Recently, I touched on a cloud company named Okta (OKTA) responsible for managing the facilitation of passwords.

This identity management company was formed by a group of former Salesforce executives.

In my book, a Salesforce (CRM) credential is a golden stamp of approval for newly formed cloud-companies seeking to develop new cloud products in broad industries.

Why?

Salesforce’s client relationship management platform (CRM) is ubiquitous and the most popular enterprise software.

The way they develop their model is by launching and acquiring new e-commerce and marketing services - which lure in customers into its walled gardens.

Salesforce also applies its artificial intelligence platform Einstein to harness customer relationships and help businesses carry out decisions based on data alone instead of testosterone and emotion.

This all means that Salesforce executives have their finger on the pulse of the cloud landscape and know how to build a cloud business from scratch which is valuable.

They know what certain industries require to mushroom and can deploy resources in the quickest way possible while surrounding themselves by hordes of software engineers who can be poached for a certain fee.

The framework being in place is a massive bounty for these executives who just line up the dots then motor on to an industry confirmed by the data.

And remember that 99.9% of people do not have access to this proprietary data.

Consequently, they know more about corporate America than most Fortune 500 CEOs.

Marrying up the healthcare industry to the cloud was just a matter of time.

Veeva Systems (VEEV) is a cloud-computing company focused on pharmaceutical and life sciences industry applications.

Founder and CEO of Veeva Systems Peter Gassner cut his teeth at Salesforce serving as Senior Vice President of Technology.

His job was building the salesforce.com platform including product, marketing and developer relations.

Gassner has effectively transplanted the Salesforce platform model and applied it to the life sciences industry and has done a great job doing it.

The Veeva Commercial Cloud includes a CRM platform that aids drug company’s management of clients.

The Veeva Vault is a tool that tracks industry regulations, clinical trials, and recommends actionable habits in the cloud.

Veeva's CRM platform is powered by the Salesforce1 app development platform and is integrated into the broader Salesforce Marketing and Service Clouds.

The first mover advantage has offered all the low-hanging fruit for Veeva.

The lack of competition surely never lasts but the extra time to pad their lead is only a positive to its business model.

Veeva has already lured in some of the health industries biggest names such as GlaxoSmithKline (GSK), AstraZeneca (AZN), Merck & Co. (MRK), and Novartis (NVS).

These heavy hitters are meaningfully tied to its ecosystem, and it is safe to say that these relationships are only scratching the surface and have the potential to expand as Veeva installs more add-on tools into its platform.

The popularity shows up in the numbers with Veeva’s 3-year sales growth rate hovering around 30%.

Even better, the profitability of Veeva is indicative of the strength in its business model. They are simply at the right place at the right time to capture the momentum from the digital crossover in the healthcare industry.

Many similar names like Dropbox (DBX) are enormous loss-making enterprises but Veeva has shrugged off this stereotype that many cloud companies of its size can’t be profitable.

The effect of being strategically placed in a position to cherry pick the lucrative healthcare industry has also seeped into the strong profit margins of Veeva able to grow it to over 32%.

Touching more on the profitability, EPS has kicked into gear sequentially rising 80%, and the long-term outperformance is backed up with a 3-year EPS growth rate of 41%.

This cloud company is incredibly profitable for its size, and part of that is the absence of competition which increases pricing power.

Dropbox does not have that luxury of favorable pricing schemes which cripple profitability and leads to attrition and just as harmful – a price war.

Veeva’s forecasts for next year blew past Wall Street’s estimates and the company is modeling for EPS of $1.58 and revenue around $856 million in 2019.

Gassner has even publicly acknowledged that he expects 2019 revenue to come in between $1 billion and $1.1 billion which is a full year ahead of schedule.

The bullish guidance is a clue that the overall cloud story is alive and kicking, and there is absolutely no weakness whatsoever.

Making this story even more compelling is that in the last five years, profits are up six-fold, revenue is up four-fold, and the number of new products is up three-fold.

As we advance into 2019, I believe Veeva is a buy-on-the-dip candidate because of its favorable market position, rapidly expanding margins, and its low enterprise value of $11 billion which deems it, as I daresay, a lucrative buyout target for larger industry cloud players like Salesforce.

The tech industry has a habit of coming full circle become of its network effect of capital, talent, and management.

I would be interested in dipping my toe into any of Salesforce’s offspring because these models are built to scale and are waiting on the doorstep to seize revenue from industry migrating to digital.

Okta did it, and Veeva Systems made the leap of faith too, confirming that the Salesforce method is a path to untold profits for cloud-based software companies.

When the market can finally digest the macro rigmaroles, shares for this innovative and hyper-growth cloud company is set to take off.

“You must always be able to predict what's next and then have the flexibility to evolve.” – Said Founder and CEO of Salesforce Marc Benioff

Mad Hedge Technology Letter

December 18, 2018

Fiat Lux

Featured Trade:

(THE BIG TECHNOLOGY TRENDS OF 2019)

(MSFT), (AMZN), (BBY), (SONO), (ROKU), (ADBE), (AAPL), (BAC)

As an astute purveyor of technology, it is my job to share with you the upcoming tech trends of 2019.

Some might be easily discernable and some might be a headscratcher, but all must be tabbed up and considered in the current tech outlook that is unpredictable and fluctuating, to say the least.

Part of the moody tech sentiment has been influenced by a changeable macro landscape - the tech sector’s winter freeze was woefully volatile and unfairly capsized good companies with the bad.

There is no means to get around it – the administration's delicate situation as it relates to Beijing and the American tech sector is front and center, and any movement of tech stocks must carefully absorb the ongoings from this complicated relationship.

The number of obstacles that confront this sensitive situation means that the 90-day window granted to solve the trade quagmires appear too brief of a timeframe to really knock out every single disagreement on the table.

The uncertainty over trade policy has really ruffled some of tech’s strongest feathers such as America’s pride and joy Apple (AAPL).

Apple is a great long-term story, but it does not preside over many short-term positive catalysts that can resuscitate the stock.

Analysts' downgrade after downgrade has been most harrowing for the chip components that make up Apple and other consumer electronic devices such as televisions and tablets.

This scenario is expected to extend into 2019 with Bank of America Merrill Lynch (BAC) slashing their price target by nearly 30% on electronics retailer Best Buy (BBY) then sticking the fork in them by downgrading it to underperform.

The premise behind this downgrade was that Best Buy carved out 25% of revenue from television sales and even though Adobe (ADBE) analytics has calculated record online sales in the holiday season, the follow-through has largely been without television sales participating in the seasonal bonanza.

Piggybacking on this trope, I believe electronic device sales could be hard-pressed to eke out growth next year and are set up for a rude awakening.

Therefore, it is sensible to extrapolate this idea out and assume that smart hardware competing against the big boys such as smart speaker firm Sonos (SONO), who I urged readers to stay away at $16 in September, is set up for a painstaking 2019.

To reread the story, please click here.

The stock is now trading at $11 and a mix of weakening consumer device demand layered with the domination that is the Amazon Alexa has pushed up this company’s risk-reward levels to untold heights.

Rounding out the negatives is that content streaming platform Roku has also debuted its own version of a smart speaker.

Roku (ROKU) is one of my favorite long-time tech plays but has been dragged down by the broader trade war because a portion of its revenue is still captured by hardware such as the new speakers and Roku OTT boxes.

Differing from Apple, Roku earns most of their revenue from targeted ads on their proprietary platform, and this is its reason why most investors are in this stock that is set to capture a secular migratory wave of cord-cutters traversing to online streaming.

However, Roku TVs made by Chinese company TCL still draw in small portion of revenue and even though the China revenue is not as high on a relative basis as Apple’s 20%, the stock has floundered in the short-term.

If disruptors such as Roku can get hit savagely with a small portion of revenues from China, then I am convinced that any tech investor going into 2019 should stay away from hardware and hardware that is made in China.

The consensus is that the drawn-out trade war could become the X-factor in the 2020 election because the Chinese are willing to wait for the next guy on the carousel searching for a better deal.

If you thought Chinese supply chains had a tough time of it in 2018, then 2019 is poised to be even more treacherous.

What 2018 convincingly demonstrated was that the late economic price action is getting into later and later stages boding negative for tech stocks.

To construct a healthy tech portfolio going into 2019, the change in the tech partiality has made the pivot towards software much more important.

Investors need to mitigate Chinese supply chain risk and seek out domestic software plays.

That should be the playbook as tech investors are on pins and needles going into the new year.

The domestic economy is robust and tech investors should be attracted to top-quality cloud-based enterprise stocks that are profitable.

The FANG story collapsing in our face signaled to investors that it is time to cautiously consider whether to invest heavily into deep loss-maker tech growth stories.

A healthy rotation to premium quality tech with superior cash flow is one way to lock up stocks and slyly deflect the external factors shaking up the tech momentum.

PayPal (PYPL) is a stock that has large international exposure mainly in Europe, but none in China whose 3-year EPS growth rate is 26% and still driving sequential sales in the mid-20% range.

This is just one example of a stock that has the correct make-up in a harsh and brutal tech environment planted with invisible booby traps.

And the most tell-tale sign that the American economy is in for an all-out software frenzy is the number of head-spinning investments from big tech companies looking to expand their footprint into new talent spots around the country.

First, the farcical Amazon beauty pageant came to an end with the e-commerce giant announcing a three-part package deploying new operations in New York, Washington D.C., and Nashville as the next phase of digital growth ramps up.

Google (GOOGL) followed that up by plopping a software office in New York City devouring a huge chunk of the Chelsea neighborhood aimed at doubling the 7,000 employees already there.

Then it was Apple’s turn choreographing a significant investment in Austin, Texas that will cost them $1 billion along with juicing up operations in Seattle, San Diego, and Los Angeles.

They weren’t finished there and promised to double down its presence in Pittsburgh, New York and Boulder, Colorado over the next three years.

It’s clear that big tech has finally understood that it’s not invincible and milking the China supply chain for all its worth is now a taboo business practice that has bipartisan support firmly against it.

Like I said before, the trade war came 1-2 years too early for Apple, and these headline-grabbing talent investments in data centers and its staff underscore the sense of urgency to fully and comprehensively pivot towards a software and services company.

The transition has certainly been an excruciating process exposing the weak spots at a brilliant company at the worst possible time.

I blame CEO of Apple Tim Cook who is the operations expert in the building grappling with Apple overextending themselves in the Middle Kingdom that has come back to haunt him at night.

You would have thought that with the troves of big data on their hands, Apple’s consultants might have found a country allied with America to invest in such a massive supply chain.

This leads me to communicate with conviction that Microsoft (MSFT) is my favorite tech stock going into 2019 because it is the purest, scalable, high-quality software name with minimal hardware drag devoid of weak spots in its armor.

That was what the investment in GitHub for $7.5 billion was about, highlighting the value of owning the meeting place for coders, literally buying up a stash of over 28 million users and 57 million coding repositories in which 28 million are public.

Microsoft has also bought up six video game studios in 2018 attempting to capture a bigger piece of the pie for the video game market that has been throttled by Fortnite.

If the Microsoft baby gets thrown out with the bathwater, then the tech bear market is upon us in full force.

If you didn’t really believe content is king in 2018, then you will really feel the phenomenon further embedded into the economy and society in 2019.

Next year, almost all tech investments will result in more data centers and software engineers in the hope of pumping out the best content and data, whether it’s enterprise software, video games, or pure data storage.

In 2019, I am bullish on companies with a cloud-based bedrock able to grind out the best content in the world, backed by a strong balance sheet that dovetails nicely with a lack of China-based revenue exposure.

The uber-growth models could be taking a rest boding negatively for Uber, Lyft, and Airbnb who must convince a more skeptical tech audience with tighter purse strings as they inject yet another unique dimension into the tech world next year.

“Stone Age. Bronze Age. Iron Age. We define entire epics of humanity by the technology they use.” – Said Founder and CEO of Netflix Reed Hastings

Mad Hedge Technology Letter

December 17, 2018

Fiat Lux

Featured Trade:

(WHY TENCENT WILL REMAIN TRAPPED IN CHINA)

(TME), (SPOT), (IQ), (GOOGL), (FB)

So you thought that Tencent Music Entertainment (TME), the Spotify (SPOT) of China, going public at $13 a share on the New York Stock exchange would mean the music streaming giant would potentially tyrannize the Western music streaming market.

Relax, it will never happen, China’s personal data laws are analogous to Facebook’s (FB) lax data guidelines multiplied by a factor of 10.

There is no possible scenario in which a Chinese content service constructed at the magnitude of Tencent Music Entertainment Group would ever get the thumbs up from American regulators.

The ongoing trade war has effectively barred any Chinese capital’s ability to snap up key American technological firms, as well as stymieing any Chinese tech unicorns dishing out streaming content in participating in a monetary relationship with the American consumer.

In August, the Department of the Treasury which chairs the Committee on Foreign Investment in the United States (CFIUS) rolled out an expansionary pilot program widening CFIUS’ jurisdiction to review foreign non-controlling, non-passive investments in companies that produce, design, test, manufacture, fabricate, or develop “critical technologies” within certain industries deemed paramount to national security.

Even though the amendment does not specify China, it means China.

If you had a hunch that Tencent would take over the music streaming world, then the better question is to ask yourself if Tencent Entertainment is equipped to take over the Chinese streaming world and monetize the product efficiently.

What really is (TME)?

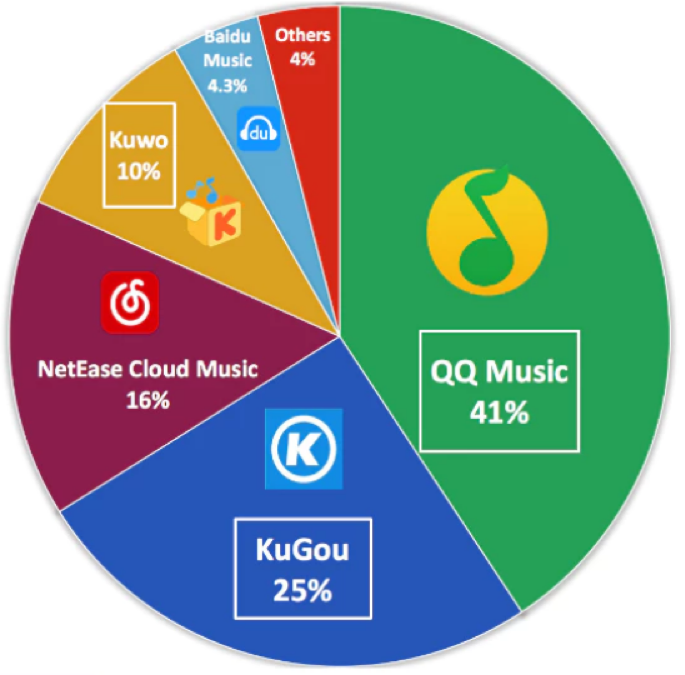

(TME) is the Tsar of Chinese music streaming with apps that allow users to stream music, sing karaoke, and watch musicians perform live. (TME) dominates this sphere of Chinese tech with a combined 800 million monthly active users.

(TME) is a concoction of services including QQ Music, Kugou, Kuwo, and karaoke app WeSing making up over 70% of the music streaming industry in China.

Its daily active users (DAUs) spend over 70 minutes per day on the platform and have inked exclusive deals with elite Western artists.

Tencent Music's revenue nearly doubled YOY to $2 billion during the first nine months of 2018, and its net income more than tripled to $394 million.

The social entertainment services aspect has been a massive revenue driver for them including income from virtual gifts on WeSing, a platform where fans gift virtual items to favorite singers, and sign up for premium memberships giving users access to exclusive concerts.

This collection of clever services mixed with social media has been successful, and the reason why it comprises 70% of total revenue.

Paid membership has grown 24% YOY to 9.9 million while paid users only make up 4.4% in China. This is a huge change in the tech climate from the past when Chinese netizens would never pay for internet content. This has allowed the average revenue per user (ARPU) to creep up to $17.22 per paid user.

The other 30% of revenue can be attributed to its ad-less music service which is not ad-less for free users.

So, in fact, the 30% of the business that mirrors Spotify is its Achilles heels echoing the painstaking task of monetizing pure music content.

No company has ever shown that a pure music streaming internet model can be profitable, the music streaming graveyard is littered with the failed attempts of companies from the past.

The unit registered a mere $1.24 in average revenue per paid user during the third quarter, paltry compared to (TME)’s social media products.

(TME)’s combination of social media and music entertainment weighted towards virtual gifts’ income is a weak business model in the west and would not extrapolate in the western world.

It is a supremely China model only unique to China and other Asian countries.

Therefore, I would point out that even if this arm of Tencent could migrate to America, management knows better than to put square pegs in round holes.

That being said, its potential in China is its long runway and most Chinese content companies haven’t been able to crack the western market.

The only types of Chinese companies that have had any remnant of success in the west are hardware companies and look what happened to telecommunication equipment companies Huawei and ZTE recently – taken out by the western regulatory sledgehammer.

It’s crystal clear that the Chinese understanding of personal data and IP regulation simply don’t marry up with western standards, and that is why I suggested that these two massive tech worlds are in for a hard splintering dividing these two competing models.

There has been some intense jawboning going on behind the scenes as Huawei, who is in the lead to develop 5G technology, still needs Qualcomm’s radio access technology to make 5G a reality.

The scenario of a hard fork between western and Chinese 5G becomes more real each passing day.

Part of Tencent Music’s ability to perform revolves around its swanky position installed in the center of the most popular chat app in China called WeChat.

Using this position as a fulcrum, Tencent Music plans to invest 40% of the capital raised from its IPO on expanding its music library, 30% on product development, 15% on marketing, and the last 15% on M&A.

For right now, there is an elevated emphasis on growing the number of paid users and converting its free users to premium subscriptions.

Ironically enough, Spotify has a 9% stake in Tencent Music and Tencent has a 7.5% holding in Spotify. Just by having stakes in each other is enough reason to avoid migrating into the same competitive markets with each other.

If you read between the lines, the stakes seem more a pledge of trading expertise in developing each other’s business as you see traces of each other in both unicorns.

Would I invest in Tencent Music?

One word – No.

There are almost 1,000 pending lawsuits alleging copyright infringement, not a huge surprise here.

Tencent concedes around 20% of the music content is not licensed.

Pouring fuel on the fire, a Tencent Music executive is also being sued by a seed investor claiming he was bullied into selling his stake ahead of its IPO.

There are question marks surrounding this company and that might have been part of the justification of tapping up the American public markets to prepare for this next stage of uncertainty.

As it is, Spotify cannot make money because of the elevated royalty costs eroding its business model, (TME) probably can if it steals most of its music, but that is a suicide mission waiting to happen.

Fortunately, Tencent is a hybrid mix of not only pure music streaming but of social media fused with music apps through gift giving gimmicks and karaoke-themed services.

These higher margin drivers are the reason why Tencent is profitable and Spotify is not, plus the giant scale of servicing 800 million Chinese users that give credence to the freemium model.

However, it’s entirely feasible that Tencent Music could use a good portion of the $1.1 billion from the IPO to battle the slew of pending lawsuits waiting around the corner.

Would you want to invest in a company that went public just to fund their legal defense?

Definitely not.

Look at its streaming cousin iQIYI (IQ), shares peaked over $40 in June after its IPO and have swan-dived ever since going down in a straight line and is trading around $17 today.

In general, most Chinese tech stocks have been collateral damage of a wider trade war pitting the maestros of crude geopolitical strategies against each other.

This year has not been kind to Chinese tech shares, and considering most of Tencent’s music library has been stolen, investors would be crazy to invest in this company.

I am surprised this company held up as well as it did on IPO day because the timing of the IPO couldn’t have been worse in a segment of tech that is awfully difficult to become profitable in a country whose economy is softening by the day in an insanely volatile stock market.

And to be honest, I would have stopped listening about this company after knowing they face pending lawsuits of up to 1000.

As for Spotify, yes, they are the industry leader in music streaming but investors need concrete proof they can become profitable. I like the direction of increasing operating margins, but that all goes to naught if it’s in a perpetual loss-making enterprise. I would sit out on both these stocks with a much negative bias towards its ticking time bomb Chinese music version.

Regulation and the trade war have taken a huge swath of tech off the gravy trade such as semiconductors, Google, social media, hardware, American tech who possess supply chains in China and I would smush in Chinese tech ADR’s on that list too.

Stay away like the plague.

“Life’s too short to hang out with people who aren’t resourceful.” Said Founder and CEO of Amazon Jeff Bezos