Mad Hedge Technology Letter

May 9, 2018

Fiat Lux

Featured Trade:

(HERE'S THE TOP STOCK IN THE MARKET TO BUY TODAY),

(MSFT), (AMZN), (AAPL), (APTV), (QCOM), (FB)

Mad Hedge Technology Letter

May 9, 2018

Fiat Lux

Featured Trade:

(HERE'S THE TOP STOCK IN THE MARKET TO BUY TODAY),

(MSFT), (AMZN), (AAPL), (APTV), (QCOM), (FB)

When the CEO of Microsoft, Satya Nadella, sits down for a candid interview, I move mountains then cross heaven and hell to listen to him, and you should, too.

Microsoft is at the top of my list as a conviction buy.

Nadella is one of the great CEOs of our time and was able to complete Microsoft's makeover after Steve Ballmer's insipid tenure at the helm.

Microsoft's Build conference is the perfect platform for Nadella to share his wisdom about the company, industry, and changes going forward.

In an age where tech CEOs thrive off of smoke and mirrors, Nadella was succinct conveying the concept of trust as the secret sauce that will help tech's digital footprint expand into new territories.

Trust infused products through the cloud and A.I. will be the perfect archetype of future tech that will encourage accelerated adoption rates.

A.I. was the message of the day at the Build conference. Nadella used the term A.I. 14 times and the word cloud four times when interviewed.

It was fitting that Microsoft wowed the audience with a sparkly, new-fangled demo.

The demo put on by Microsoft in conjunction with Amazon's (AMZN) Alexa showed smart-assistants working in collaboration.

Microsoft showed how it is possible to use a PC Windows desktop to order an Uber car through Amazon's Alexa.

This technology is very powerful and is a work-around for the "walled garden" problem where big companies are closing off their systems only to proprietary software and products limiting upside potential.

The ability to collaborate with multiple A.I. smart systems will generate a whole new layer of business catering toward the communication and business developments among A.I. systems.

Nadella also offered extended examples of A.I. applications, for instance, the capability of detecting cracks in an oil pipeline and running recognition software through a drone using a Qualcomm (QCOM) manufactured camera to monitor the state of containers.

Trusting A.I. will expedite the usage of A.I. business applications, and the companies diverting capital into A.I. enhancement will reap from what they sow.

The knock-on effect is that university A.I. staff members are being poached faster than a breakfast egg. There is a bidding war going on as we speak from both sides of the Pacific.

Facebook is opening new A.I. research centers in Seattle and Pittsburgh.

Previously, A.I. was a buzzword and companies would trot out a visually stimulating display with pizzazz. But that is all changing with A.I. swiftly moving into the backbone of all business operations.

Ottomatika, a company that develops software for autonomous cars acquired by Aptiv (APTV), was entirely a Carnegie Mellon University (CMU) in-house project that was picked up by Aptiv for commercial applications.

In one fell swoop, (CMU) lost a whole team of leading A.I. researchers.

Microsoft is a premium stock because it straddles both sides of the fence.

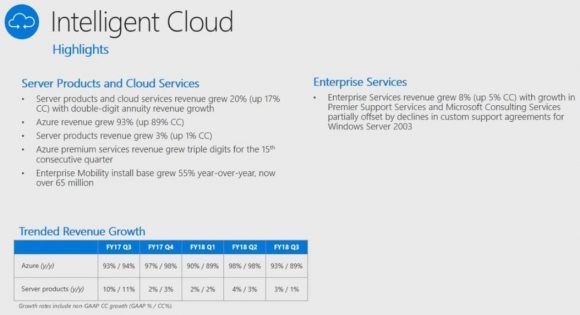

On one side, it's an uber growth company with Microsoft Azure growing 93% YOY satisfying investors requirement for insatiable growth.

On the other hand, Microsoft is robustly lucrative profiting $21.20 billion in 2017, and would be a Warren Buffett-type of cash flow reliant stock even though he has smothered any inkling of buying Microsoft shares because of his close relationship with co-founder Bill Gates.

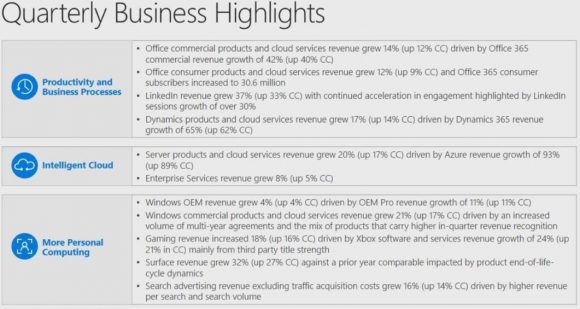

Even Microsoft's legacy product Microsoft Office 365 is a gangbuster segment swelling 42% YOY.

This contrasts with other legacy companies that are attempting to wean themselves from their own outdated products.

Office 365 products are still embedded in daily life, and I am using it now to type this story.

On the technical side of it, Microsoft is beefing up its developer tools.

Microsoft will integrate Kubernetes, an open-source system for automating deployment, into the Azure as well as upping its Azure Bot Service adding 100 new features.

There are more than 300,000 developers who operate the Azure Bot Service alone.

The slew of upgrades for developers will enhance the power of Microsoft's software and ecosystem.

The overarching theme to the Build conference is the integration of A.I. into real life business applications and the importance of the cloud.

Now the Cloud.

Nadella reaffirmed Microsoft's position in the cloud wars characterizing the current environment as a duo of Amazon and Microsoft with Google trailing behind.

Microsoft has the potential to nick Amazon's position as the industry's cloud leader because of the unique set of products it can combine with the cloud.

Most of the world utilizes a mix of PC-based hardware, using Microsoft's software and operating system, supplemented by an Android-based smartphone.

As expected, Microsoft, Alphabet (GOOGL), and Amazon are spending a pretty penny advancing their cloud business.

Microsoft spends more than $1 billion per month on Azure cloud data centers.

This number now surpasses the entire annual Microsoft R&D budget.

In the interview, Nadella cited that Microsoft now has 50 domestic data centers.

Amazon habitually holds between 50,000 to 80,000 servers at each data center. Extrapolate the lower range of the number with 50 data centers and Microsoft could have at least 2.5 million servers working for its data needs.

The barriers of entry have never been higher in the cloud industry because the costs are spiraling out of control.

Few people have billions upon billions to make this business work at the appropriate scale.

Tom Keane, head of Global Infrastructure at Microsoft Azure, recently said that Azure meets 58 compliance requirements set forth by the federal government, industry, and local players.

Azure is the first cloud that satisfies the Defense Federal Acquisition Regulation Supplement criteria for contractors to handle Department of Defense work.

Regulation has emerged as one of the controversial issues of 2018, and this did not get lost in the shuffle.

The trust comment was clearly a thinly veiled swipe against Facebook's (FB) much frowned upon business model, making it commonplace these days for prominent CEOs to distance themselves from Mark Zuckerberg's creation.

Protecting a company's image and reputation is paramount in the new rigid era of big data.

Nadella's anti-Facebook rhetoric continued by noting the auction-based pricing standards are "funky," explaining the model is counterintuitive. His reason was that as demand increases, the price should drop and not rise.

Apple (AAPL) CEO Tim Cook has largely been negative about Facebook's tactics. The fury is justified when you consider Apple and Microsoft hustle industriously to develop software and hardware products while Facebook manipulates user data to profit from collected data. A nice shortcut if there ever was one.

It's clear that Apple and Microsoft have no interest in giving third parties access to personal data because the leadership understands it is a slippery slope to go down and unsustainable.

Nadella's emphasis on tech ethics is a breath of fresh air and the data Microsoft accumulates is used to improve the cloud and software products rather than pedal to mercenaries.

The companies that have staying power create proprietary products that cannot be replicated.

Microsoft's assortment of software products acts as the perfect gateway into the cloud and is a moat widening tool.

A.I. and the cloud are all you need to know, and Microsoft is at the heart of this revolutionary movement.

Any weakness of Microsoft's shares into the low-90s is a screaming buy.

_________________________________________________________________________________________________

Quote of the Day

"Innovation has nothing to do with how many R&D dollars you have. When Apple came up with the Mac, IBM was spending at least 100 times more on R&D. It's not about money. It's about the people you have, how you're led, and how much you get it." - said Apple cofounder Steve Jobs.

Mad Hedge Technology Letter

May 8, 2018

Fiat Lux

Featured Trade:

(BUFFETT GOES ALL IN WITH APPLE),

(SNAP), (WDC), (GOOGL), (AMZN),

(CRM), (RHT), (HPQ), (FB), (AAPL)

Not every stock comes with Warren Buffett's confession that he would like to own 100% of it. But, of course that stock would have to be a tech stock.

As it stands, the Oracle of Omaha owns 5% of Apple (AAPL), and his confession is still a bold statement for someone who seldom forays outside his comfort zone.

Buffett also continues to concede that he "missed" Google (GOOGL) and Amazon (AMZN).

What a revelation!

The outflow of superlatives invading the airwaves is indicative of the strength technology has assumed in the bull market.

The tech sector has been coping with obstacles such as higher interest rates, trade wars, data regulation, IP chaos, and the globalization backlash.

However, the tech companies have come through unscathed and hungry for more.

Their power is not contained to one industry, and techs' capabilities have been spilling over into other sectors digitizing legacy industries.

Every CEO is cognizant that enhancing a product means blending the right amount of tech to suit its needs.

It is not halcyon times in all of tech land either.

There have been some companies that have faltered or were naturally cannibalized by other tech companies that disrupt business.

Times are ruthless and this is just the beginning.

There will be winners and losers as with most other secular paradigm shifts.

Particularly, there are two types of losers that investors need to avoid like the plague.

The first is the prototypical tech company hawking legacy products such as Western Digital Corp. (WDC) that I have been banging on the table telling investors not to buy the stock.

The lion's share of revenue is still in the antiquated hard drive business that has a one-way ticket to obsolescence.

Yes, they are turning around product mixes to factor in its pivot to solid state drives (SSD), but they are late to the game and deservedly punished for it.

Compare WDC to companies that have completed the transition from legacy reliance to the cloud, and it is simple to understand that companies such as Microsoft, which struggled for years to turn around with CEO Satya Nadella, finally can claim victory.

The problem with WDC is the stock's price action performs miserably because the company is tagged as an ongoing turnaround story.

On the other hand, headliner cloud plays experience breathtaking gaps up due to the strength of the cloud such as Amazon (AMZN), Red Hat (RHT), and Salesforce (CRM), just to name a few.

To pour fuel on the fire, speculative reports citing NAND chip price "softening" beat down the stock into submission.

Effectively, legacy companies become sell the rallies type of stocks.

Transforming a legacy company into a high-octane cloud company is perilous to say the least. Jeff Bezos recently gloated that Amazon Web Service's (AWS) seven-year head start is all investors need to know about the cloud. There is some merit to his statement.

Examples are rife with bad executive decisions by legacy companies such as HP Inc. (HPQ), another legacy tech company that makes computers and hardware. It ventured out to buy Palm for $1.2 billion plus debt after a bidding war with legacy competitor Dell in 2010.

In 1996, the Palm PDA (Personal Digital Assistant) was the first smart phone on the market that predated BlackBerry's smart phone with the full keyboard made by RIM (Research in Motion).

The demise of Palm emerged from a hodgepodge of mismanagement, failed spin-offs, misplaced mergers, and resource wastefulness even with the preeminent technology of its time.

(HPQ)'s stab at the smartphone market resulted in purchasing Palm. However, after heavy selling pressure in its shares, HP shut down this division and sold off the remaining technology to Chinese electronics company TCL Corporation.

The sad truth is many transformations fail at step one, and there is no guarantee a newly absorbed business will perform as expected.

RIM, now changed to BlackBerry (BB), soon found out how it felt to be Palm when Steve Jobs dropped the first iPhone on the market, and the world has never been the same.

(BB) gradually morphed into an autonomous vehicle technology company after the writing was on the wall.

The other types of losers are companies with inferior business models such as Snapchat (SNAP), which I have written about extensively from the bearish side.

In an age where disruptors are being disrupted by other disruptors, CEOs must live in fear that their business will get undercut and hijacked at any time.

Instagram, a subsidiary of Facebook (FB), has permanently borrowed numerous features from Snapchat. Its Instagram "stories" feature is now used by more than 300 million daily users.

Snapchat is serving as Instagram's guinea pig while CEO Evan Spiegel finds an alternative way to survive against Facebook's unlimited resources.

Both are in the game of selling ads and nobody does it better than Facebook and Alphabet or has the degree of scale.

The recent redesign was met with a chorus of universal boos. The 60 minutes I spent testing the new design reconfirmed my fears that the new design was an unmitigated washout.

In short, Snap's redesign seemed like a different app and became incredibly difficult to use.

Compounding the deteriorating situation, Snapchat laid off 120 engineers due to sub-par performance and withheld last year's performance bonuses even though co-founder Evan Spiegel received $637 million in 2017.

The latest earnings report was a catastrophe.

Daily active user (DAU) growth, the most sought out metric for Snapchat, failed to deliver the goods. The street expected 194.2 million DAU and Snap reported 191 million. A miss of 3.2 million users and a deceleration of growth QOQ.

Remember that Snapchat is substantially smaller than Instagram and should have no problems surpassing expectations on a smaller scale, thus investors voted with their feet and bailed on the stock after the catatonic performance last quarter.

Instagram is six times larger with more than 800 million users as of the end of 2017.

Top line fell short of expectations and average revenue per user (ARPU) dropped to $1.21, far less than the expected $1.27.

The less than stellar redesign faced a rebellion from long-term Snapchat disciples. More than 1.2 million Snap diehards signed a petition hoping to revert back to the old interface, and its updated ratings in Apple's app store has fallen to 1.6 stars out of 5.

Then the perpetual question of why would advertisers want to pay for Snapchat digital ads when they earn more by buying Instagram ads?

This remains unsolved and appears unsolvable.

Snapchat is befuddled by the pecking order and the company is on a train to nowhere.

To hammer the nail in the coffin, Snapchat announced to investors that it expects revenue to "decelerate substantially" next quarter.

In an era where technology companies will lead the economy and stock market, and has an outsized influence in politics and culture, not all tech companies are one-foot tap-ins.

Investors need to separate the wheat from the chaff or risk losing their shirt.

_________________________________________________________________________________________________

Quote of the Day

"We have to stop optimizing for programmers and start optimizing for users." - said American software developer Jeff Atwood

Mad Hedge Technology Letter

May 7, 2018

Fiat Lux

Featured Trade:

(WARREN BUFFET BOARDS THE APPLE TRAIN),

(AAPL), (AMZN), (BABA), (JD), (TSM)

I have never been one to argue with the Oracle of Omaha Warren Buffet. The founding subscriber to the Diary of a Mad Hedge Fund Trader has been a follower of many of my Trade Alerts, including Bank of America (BAC), Burlington Northern (he bought the whole company), and American Express (AXP). But I could never get him into technology stocks.

Now, at last, you can add Apple (AAPL) to that list.

You know all of those panicky investors unloading Apple stock just over $150 apparently believing that the company's product cycle and innovation were at an end? That was Warren doing the buying.

Too bad I couldn't get him interested in the stock when Steve Jobs was still alive. Knowing Steve, maybe that was the reason he stayed away.

Still, I tried.

Still, looking at Apple's earnings this week, better late than never.

The analysts covering tech stocks are making a mockery of their work.

They are continually left to lick their wounds after a slew of inaccurate claims that will empty investors pockets faster than the speed of light.

Granted, Apple had the weakest position of the vaunted FANG group going into earnings because of a lack of a direct cloud play and the stale iPhone narrative.

However, Apple is still a force to be reckoned with and they proved the bears horribly wrong delivering an extraordinary performance in Q1 2018.

Katy L. Huberty, a tech analyst from Morgan Stanley, downgraded Apple citing weak demand in China. This was after Taiwan Semiconductor (TSM) released tepid future guidance, stoking fear into investors causing a short-term dip in shares for chip related stocks and Apple.

The first two months of the year saw a barrage of downgrades from KeyBanc, Bernstein, and BMO capital. It is the same story over and over again.

Analysts do their best to character assassinate Apple on the run up to earnings every time. This ritual has embarrassed the analyst community. I don't think I'll ever believe another analyst again.

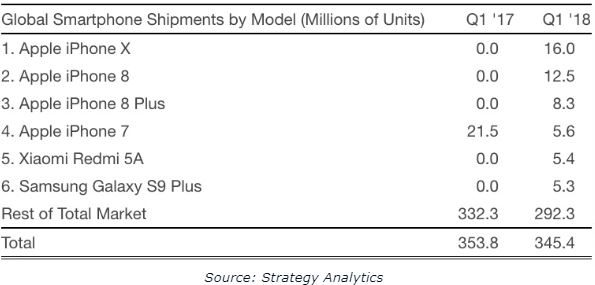

The iPhone X was the World's best-selling smartphone the last two quarters according to big data firm Strategy Analytics because it is the best smartphone in the World.

This logic might be too difficult for Wall Street analysts to comprehend with their hodgepodge of random data points that lead them to the wrong conclusions.

Apple has delivered earning beats on 20 of the last 21 quarters. The guidance was even on the high side of the range and the report was demonstrably better than expectations.

Services is now a material part of the company, blowing past estimates of $8.39 billion posting $9.19 billion in sales. This makes up 15% of the total revenue, and Apple will seek to solidify this segment going forward.

Apple will make a lot of headway if services become 25% of revenue. The optimal method to boost earnings is to develop a revolutionary product or extract additional incremental revenue from existing subscribers. Apple is going with the latter as the low hanging fruit is always easiest to pick.

The timing couldn't be more perfect for Apple. The World is on the cusp of new tech regulation that could lower margins and veering into a reoccurring subscription model is the perfect way to insulate themselves while growing the business.

The potential to increase the incremental revenue from China is strong because most of the iPhone earners in China originate from Tier 1 cities like Beijing and Shanghai and have the disposable income to pay for Apple's cocktail of services.

To dismiss the Chinese consumer is dangerous. Just look at the growth targets being smashed by Alibaba (BABA) and JD.com (JD) each quarter.

Japan and China contributed 20% growth to Apple's top line mainly due to the adoption of Apple Pay at many train and bus stations.

iPhone unit sales missed estimates by 340,000, but the analysts' bearish sentiment led many investors to believe the shortfall would be an unmitigated disaster.

The Average Selling Price (ASP) of $728 remained healthy as Apple has largely avoided the deterioration in margins that analysts routinely use as a pinata.

Apple continues to be the preeminent profit creator in the tech industry. They pocketed almost $50 billion in net profit in 2017. Public companies are in the business of making profits and returning capital to shareholders, and Apple does that better than anyone.

Apple's stock has been unfairly sabotaged by analysts and it almost seems they want the stock to capitulate and buy it for their own personal accounts.

Compare that to Amazon (AMZN) whose annual sales amounted to almost $180 billion but only $3 billion in net profit.

The market is penalizing Apple for a lack of a cash burn, land grab business. It is not Amazon and does not want to be Amazon. That is what the market pays for now.

It is ironic that Apple are penalized for making so much cash. They even hit an all-time high at $183 in a hazardous macro environment.

Saving the best for last, CEO Tim Cook pulled out his "trump" card. Apple announced an altruistic capital allocation program of $100 billion, the largest of any company in history. The dividend was hiked a further 16%.

Apple has given back $275 billion to shareholders since 2012 and this number should surpass $300 billion by 2019.

The unbridled expectations that Apple need to revolutionize the world with something better than an iPhone has reached the tipping point. Investors alike need to understand this is one company. And this company is doing very well.

Steve Jobs made an indelible impact on Silicon Valley, America, and the World. Tim Cook is not Steve Jobs. He will never be Steve Jobs.

Tim Cook is a safe pair of hands that knows how to captain this large ship.

Apple is turning into a service business and is still in the good graces of the Chinese communist government. If you consider that business attached to the iOS operating system has provided employment to a staggering five million local Chinese people. Creating problems for Apple as part of any widened trade war would create a huge loss to the Chinese economy.

I suspect that moving forward, Apple will increase operational margins due to a bigger contribution from the services segment which will dislodge the reliance on iPhone unit sales.

Buy Apple after the next atrocious analyst call and mini selloff.

"It has become appallingly obvious that our technology has exceeded our humanity." Said Albert Einstein.

Mad Hedge Technology Letter

May 4, 2018

Fiat Lux

SPECIAL SPACE X ISSUE

Featured Trade:

(WILL SPACE X BE YOUR NEXT TEN-BAGGER?)

(EBAY), (TSLA), (SCTY), (BA), (LMT)

I am constantly on the lookout for ten baggers, stocks that have the potential to rise tenfold over the long term.

Look at the great long-term track records compiled by the most outstanding money managers, and they always have a handful of these that account for the bulk of their outperformance, or alpha, as it is known in the industry.

I've found another live one for you.

Elon Musk's Space X is so forcefully pushing forward rocket technology that he is setting up one of the great investment opportunities of the century.

In the past decade his start up has accomplished more breakthroughs in advanced rocket technology than seen in the last half century, since the golden age of the Apollo space program.

As a result, we are now on the threshold of another great leap forward into space. Musk's ultimate goal is to make mankind an "interplanetary species".

There is only one catch.

Space X is not yet a public company, being owned by a handful of fortunate insiders and venture capital firms. But you should get a shot at the brass ring someday.

The rocket launch and satellite industry is the biggest business you have never heard of, accounting for $200 billion a year in sales globally. This is probably because there are no pure stock market plays.

Only two major companies are public, Boeing (BA) and Lockheed Martin (LMT), and their rocket businesses are overwhelmed by other aerospace lines.

The high value added product here is satellite design and construction, with rocket launches completing the job.

Once dominated by the US, the market for launches has long since been ceded to foreign competitors. The business is now captured by Europe (the Arianne 5), China (the Long March 5), and Russia (the Angara A5).

Until recently, American rocket makers were unable to compete because decades of generous government contracts enabled costs to spiral wildly out of control.

Whenever I move from the private to the governmental sphere, I am always horrified by the gross indifference to costs. This is the world of the $10,000 coffee maker and the $20,000 toilet seat.

Until 2010, there was only a single US company building rockets, the United Launch Alliance (ULA), a joint venture of Boeing and Lockheed Martin. ULA builds the aging Delta IV and Atlas V rockets.

The vehicles are launched from Cape Canaveral, Florida and Vandenberg Air Force Base in California, one of which I had the privilege to witness. They look like huge roman candles that just keep on going, until they disappear into the blackness of space.

Enter Space X.

Extreme entrepreneur Elon Musk has shown a keen interest in space travel throughout his life. The sale of his interest in PayPal, his invention, to Ebay (EBAY) in 2002 for $165 million, gave him the means to do something about it.

He then discovered Tom Mueller, a childhood rocket genius from remote Idaho who built the largest ever amateur liquid fueled vehicle, with 13,000 pounds of thrust. Musk teamed up with Mueller to found Space X in 2002.

A decade of grinding hard work, bold experimentation, and heart rending testing ensued, made vastly more difficult by the 2008 Great Recession.

Space X's Falcon 9 first flew in June, 2010, and successfully orbited earth. In December, 2010 it launched the Dragon space capsule and recovered it at sea. It was the first private company ever to accomplish this feat.

Dragon successfully docked with the International Space Station (ISS) in May, 2012. NASA has since provided $440 million to Space X for further Dragon development.

The result was the launch of the Dragon V2 (no doubt another historical reference) in May, 2014, large enough to carry seven astronauts.

Then Musk really upped his game by successfully pulling off the first ever landing of a booster rocket on a platform at sea in April, 2016. This is crucial for his plan to dramatically cutting the cost of space travel.

Commit all these names to memory. You are going to hear a lot about them.

Musk's spectacular success with Space X can be traced to several different innovations.

He has taken the Silicon Valley hyper competitive ethos and financial model and applied it to the aerospace industry, the home of the bloated bureaucracy, the no bid contract, and the agonizingly long time frame.

For example, his initial avionics budget for the early Falcon 1 rocket was $10,000, and was spent on off-the-shelf consumer electronics. It turns out that their quality had improved so much in recent years they met military standards.

But no one ever bothered to test them. $10,000 wouldn't have covered the food at the design meetings at Boeing or Lockheed-Martin, which would have stretched over years.

Similarly, Musk sent out the specs for a third party valve actuator no more complicated than a garage door opener, and a $120,000, one-year bid came back. He ended up building it in house for $3,000. Musk now tries to build as many parts in house as possible, giving it additional design and competitive advantages.

This tightwad, full speed ahead and damn the torpedoes philosophy overrides every part that goes into Space X rockets.

Amazingly, the company is using 3-D printers to make rocket parts, instead of having each one custom made.

Machines guided by computers carve rocket engines out of a single block of inconel nickel-chromium super alloy, foregoing the need for conventional welding, a frequent cause of engine failures.

Space X is using every launch to simultaneously test dozens of new parts on every flight, a huge cost saver that involves extra risks that NASA would never take. It also uses parts that are interchangeable of all its rocket types, another substantial cost saver.

Space X has effectively combined three nine engine Falcon 9 rockets to create the 27 engine Falcon Heavy, the world's largest operational rocket. It has a load capacity of a staggering 53 metric tons, the same as a fully loaded Boeing 737 can carry. It has half the thrust of the gargantuan Saturn V moon rocket that last flew in 1973.

Musk is able to capture synergies among his three companies not available to any competitor. Space X gets the manufacturing efficiency of a mass production car maker.

Tesla Motors has access to the futuristic space age technology of a rocket maker. Solar City (SCTY) provides cheap solar energy to all of the above.

And herein lies the play.

As a result of all these efforts, Space X today can deliver what ULA does for 76% less money with vastly superior technology and capability. Specifically, its Falcon Heavy can deliver a 116,600 pound payload into low earth orbit for only $90 million, compared to the $380 million price tag for a ULA Delta IV 57, 156 pound launch.

In other words, Space X can deliver cargo to space for $772 a pound, compared to the $7,515 a pound ULA charges the US government. That's a hell of a price advantage.

You would wonder when the free enterprise system is going to kick in and why Space X doesn't already own this market.

But selling rockets are not the same as shifting iPhones, laptops, watches, or cars. There is a large overlap with the national defense of every country involved.

Many of the satellites launches are military in nature and top secret. As the cargoes are so valuable, costing tens of millions of dollars each, reliability and long track records are big issues.

Enter the wonderful world of Washington DC politics. ULA constructs its Delta IV rocket in Decatur, Alabama, the home state of Senator Richard Shelby, the powerful head of the Banking, Finance, and Urban Affairs Committee.

The first Delta rocket was launched in 1960, and much of its original ancient designs persist in the modern variants. It is a major job creator in the state.

Shelby has criticized President Obama's attempt to privatize and modernize the rocket business as a "faith based initiative." ULA is a major contributor to Shelby's campaigns.

ULA has no rocket engine of its own. So it buys engines from Russia, complete with blue prints, hardly a reliable supplier. Magically, the engines have so far been exempted from the economic and trade sanctions enforced by the US against Russia for its invasion of Ukraine.

ULA has since signed a contract with Amazon's Jeff Bezos owned Blue Origin, which is also attempting to develop a private rocket business, but is miles behind Space X.

Musk testified in front of congress in 2014 about the viability of Space X rockets as a financially attractive, cost saving option. His goal is to break the ULA monopoly and get the US government to buy American. You wouldn't think this is such a tough job, but it is.

Musk has since sued the US Air Force to open up the bidding.

Elon became a US citizen in 2002 primarily to qualify for bidding on government rocket contracts, addressing national security concerns.

NASA did hold open bidding to build a space capsule to ferry astronauts to the International Space Station. Boeing won a $4.2 billion contract, while Space X received only $2.6 billion, despite superior technology and a lower price.

It is all part of a 50 year plan than Musk confidently outlined to a venture capital friend of mine two decades ago. So far, everything has played out as predicted.

The Holy Grail for the space industry has long been the building of reusable rockets, thought by many industry veterans to be impossible.

Imagine what the economics of the airline business would be if you threw away the airplane after every flight? It would cost $1 million for one person to fly from San Francisco to Los Angeles.

This is how the launch business has been conducted since the inception of the industry in the 1950's.

Space X is on the verge of accomplishing exactly that. It will do so by using its Super Draco engines and thrusters to land rockets at a platform at sea. Then you just reload propellant and relaunch.

The concept has so far been successfully tested to an altitude of 1,000 meters (click here).

Attempts to do this from a live launch have so far failed (click here for the video where they almost made it and second video), but Musk predicts a 50% chance of success in the next test this coming December.

Pull this off, and launch costs will plummet to pennies on the dollar. If Space X can chop payload costs to under $100, compared to ULA's $7,515, that is a savings that even Richard Shelby can't cover up.

Talk about disruptive innovation with a turbocharger!

The company is building its own spaceport in Brownsville, Texas that will be able to launch multiple rockets a day.

The Hawthorne, CA factory (where I charge my own Tesla S-1 when in LA) now has the capacity to build 20 rockets a year. This will eventually be ramped up to hundreds.

Space X is the only organization that offers a launch price list on its website, similar to how Amazon sells its books (click here for that link). The Falcon 9 will carry 28,930 pounds of cargo into low earth orbit for only $60.2 million. Sounds like a bargain to me.

Space X currently has $5 billion in contracts to fly over 50 missions for a variety of private and governmental entities, making the company cash flow positive. This includes a $1.6 billion NASA contract to supply the (ISS).

This no doubt includes an assortment of tax breaks, which Musk has proven adept at harvesting. Elon has been a quick learner with the ways of Washington.

Customers have included the Thai telecommunications firm, Rupert Murdock's Sky News Japan, an Israeli telecommunications group, and the US Air Force.

So when do we mere mortals get to buy the stock? Musk estimates at 12 flights a year the company will earn a 10% return on capital, making it worth $4-5 billion.

The current exponential growth in broadband will lead to a similar growth in satellite orders, and therefore rocket launches. So the commercial future of the company looks especially bright.

However, Musk is in no rush to go public. A permanent, viable, and sustainable colony on Mars has always been a fundamental goal of Space X. It would be a huge distraction for a publicly managed company. That makes it a tough sell to investors in the public markets.

You can well imagine that the next recession would bring cries from shareholders for cost cutting that would put the Mars program at the top of any list of projects to go on the chopping block. So Musk prefers to wait until the Mars project is well established before entertaining an IPO.

Musk expects to launch a trip to Mars by 2025 and establish a colony that will eventually grow to 80,000. Tickets will be sold for $500,000.

There are other considerations. Many employee and early venture capital investors wish to realize their gains and move on. Public ownership would also give the company extra ammunition for cutting through Washington red tape. These factors point to an IPO that is earlier than later.

On the other hand, Musk may not care. The last net worth estimate I saw for him was $13 billion. If his three companies increase in value by ten times over the next decade, as I expect, that would increase his wealth to $130 billion, making him the richest person in the world.

If an IPO does come, investors should jump in with both boots. While the value of the firm may have already increased tenfold by then, there may be another tenfold gain to come. Get on the Elon Musk train before it leaves the station.

To describe Elon as a larger than life figure would be something of an understatement. Musk is the person on which the fictional playboy/industrialist/technology genius, Tony Stark, in the Iron Man movies has been based.

In the released Tomorrowland Disney movie, a Tesla supercharging station features prominently. Elon takes all this in in good humor, lending a Tesla roadster to the film producers.

Musk has said he wishes to die on Mars, but not on impact. Perhaps it would be the ideal retirement for him, say around 2045, when he will be 75.

To visit the Space X website, please click here. It offers very cool videos of rocket launches and a discussion with Elon Musk on the need for a Mars mission.

"The longer you wait to fire someone, the longer it has been since you should have fired them," said Elon Musk, founder and CEO of Space X and Tesla Motors.