Mad Hedge Technology Letter

April 13, 2018

Fiat Lux

Featured Trade:

(ANNOUNCING THE MAD HEDGE LAKE TAHOE, NEVADA, CONFERENCE, OCTOBER 26-27, 2018)

Mad Hedge Technology Letter

April 13, 2018

Fiat Lux

Featured Trade:

(ANNOUNCING THE MAD HEDGE LAKE TAHOE, NEVADA, CONFERENCE, OCTOBER 26-27, 2018)

We all had so much fun last year at the Mad Hedge Lake Tahoe Conference that we unanimously voted to meet a year later.

That time is now approaching, and the dates have been set for Friday and Saturday, October 26-27.

Come learn from the greatest trading minds in the markets for a day of discussion about making money in the current challenging conditions.

How soon will the next bear market start and the recession that inevitably follows?

How will you guarantee your retirement in these tumultuous times?

What will destroy the economy first: rising interest rates or a trade war?

Who will tell you what to buy at the next market bottom?

John Thomas is a 50-year market veteran and is the CEO and publisher of the Diary of a Mad Hedge Fund Trader. John will give you a laser-like focus on the best-performing asset classes, sectors, and individual companies of the coming months, years, and decades. John covers stocks, options, and ETFs. He delivers your one-stop global view.

Arthur Henry is the author of the Mad Hedge Technology Letter. He is a seasoned technology analyst, and speaks four Asian languages fluently. He will provide insights into the most important investment sector of our generation.

The event will be held at a five-star resort and casino on the pristine shores of Lake Tahoe in Incline Village, NV, the precise location of which will be emailed to you with your ticket purchase confirmation.

It will include a full breakfast on arrival, a sit-down lunch, and coffee break. The wine served will be from the best Napa Valley vineyards.

Come rub shoulders with some of the savviest individual investors in the business, trade investment ideas, and learn the secrets of the trading masters.

Ticket Prices

Copper Ticket - $599: Saturday conference all day on October 27, with buffet breakfast, lunch, and coffee break, with no accommodations provided

Silver Ticket - $1,299: Two nights of double occupancy accommodation for October 26 & 27, Saturday conference all day with buffet breakfast, lunch and coffee break

Gold Ticket - $1,499: Two nights of double occupancy accommodation for October 26 & 27, Saturday conference all day with buffet breakfast, lunch, and coffee break, and an October 26, 7:00 PM Friday night VIP Dinner with John Thomas

Platinum Ticket - $1,499: Two nights of double occupancy accommodation for October 26 & 27, Saturday conference all day with buffet breakfast, lunch, and coffee break, and an October 27, 7:00 PM Saturday night VIP Dinner with John Thomas

Diamond Ticket - $1,799: Two nights of double occupancy accommodation for October 26 & 27, Saturday conference all day with buffet breakfast, lunch, and coffee break, an October 26, 7:00 PM Friday night VIP Dinner with John Thomas, AND an October 27, 7:00 PM Saturday night VIP Dinner with John Thomas

Schedule of Events

Friday, October 26, 7:00 PM

7:00 PM - Exclusive dinner with John Thomas and Arthur Henry for 12 in a private room at a five-star hotel for gold and diamond ticket holders only

Saturday, October 27, 8:00 AM

8:00 AM - Breakfast for all guests

9:00 AM - Speaker 1: Arthur Henry - Mad Hedge Technology Letter editor Arthur Henry gives the 30,000-foot view on investing in technology stocks

10:00 AM - Speaker 2: Brad Barnes of Entruity Wealth on "An Introduction to Dynamic Risk Management for Individuals"

11:00 AM - Speaker 3: John Thomas - An all-asset class global view for the year ahead

12:00 PM - Lunch

1:30 PM - Speaker 4: Arthur Henry - Mad Hedge Technology Letter editor on the five best technology stocks to buy today

2:30 PM - Speaker 5: John Triantafelow of Renaissance Wealth Management

3:30 PM - Speaker 6: John Thomas

4:30-6:00 PM - Closing: Cocktail reception and open group discussions

7:00 PM - Exclusive dinner with John Thomas for 12 in a private room at a five-star hotel for Platinum or Diamond ticket holders only

To purchase tickets click: CONFERENCE.

Mad Hedge Technology Letter

April 12, 2018

Fiat Lux

Featured Trade:

(THE BIG PLAY IN AUTONOMOUS DRIVING WITH APTIV),

(APTV), (Waymo), (TSLA)

The conventional wisdom on Electric Vehicles (EVs) is that they are here to stay.

The secular trends of harsher government environmental policy, a healthy global economic backdrop, rapid-fire technological development, and broad-based mainstream acceptance are the catalysts that will place EVs at the apex of the digital transportation movement for the rest of this century.

EVs are set to eventually capture more than 60% of market share, forcing legacy automotive and niche start-ups to reinvest into their operations in a fiercely competitive industry.

The EV industry still has a mountain to climb as it only represented less than 1% of total global auto unit sales in 2016. That percentage has gradually risen to 1.25% at the end of 2017.

The transition to 60% EV share of total units will organically occur in a slow and steady manner giving automakers ample time to shed legacy technology.

Cost is a major obstacle for widespread EV adoption. Many consumers cannot afford one, but price efficiencies are slowly dropping the cost of owning an EV, appealing to the masses with sleeker models possessing price tags similar to normal cookie-cutter sedans such as the Tesla Model 3.

EV makers have coped with the arduous task of constructing a car within truncated cost limitations. They make up the difference by offering a proliferation of premium add-ons such as souped-up engines and glitzy interiors that extract additional marginal revenue from well-off individuals.

EV technology advancement paired together with higher emission standards will narrow the gap between electric vehicles and the legacy internal combustion engine within the next decade.

Modern EVs new to market such as the Tesla Model 3 could serve as a springboard for able consumers to dive head in to EV revolution.

The disruption time horizon will take around 15 years and affect 80% of the market.

EV mania is destined to integrate with the traditional concept of a car to give transportation breakthrough A.I. functionality, user-friendly connectivity, and self-driving capabilities.

Let's face it, it's easier to install computer systems and software in an electrified platform, and the technologies complement each other.

About 60% of autonomous, light vehicle retrofits are constructed over an electric powertrain, and an additional 21% go with a hybrid powertrain.

Thus, owning the best autonomous vehicle (AV) technology stocks positions investors for the next leg of hyper-accelerating tech.

Waymo's leadership in the AV space is frightening for Tesla, which trails the Alphabet subsidiary that smoothly rolled out its for-profit service in Arizona in early 2018.

Aptiv PLC made a massive splash in the deep-end by acquiring the second best AV technology company NuTonomy. The Cambridge, MA-based tech firm spun off from MIT in 2013, for $450 million late last year and was spun out again in 2017.

Delphi Technologies spun out its legacy and tech business into two separate companies. The legacy part of the company is now the ticker symbol (DLPH), and the AV company became Aptiv PLC (APTV).

Spin-offs give organizations the opportunity to streamline operations and allow the market to value the company on an independent basis instead of the sum of the parts. This can lead to uncorking additional shareholder value.

Aptiv is the closest thing on the market you will find for an unfettered play on self-driving technology.

Management declined against merging its legacy and AV technology, which is a smart move considering legacy technology gets the wrong rub of the green by investors.

NuTonomy lags Alphabet's Waymo but has been operating robo-taxis in Singapore since 2016. Delphi has gifted additional engineers, reinforcing its fantastic technical talent.

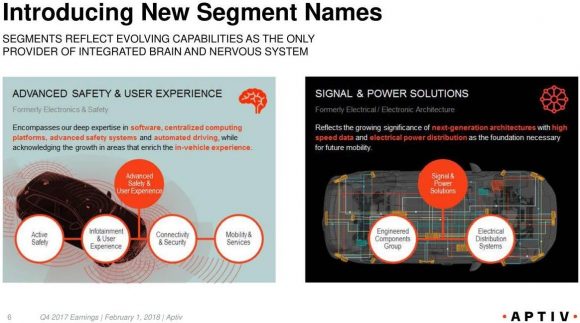

Aptiv has split its business into two new different segments in the new company.

The Advanced Safety and User experience segment will act as the brain in the vehicle, emphasizing software know-how to guarantee user security while a centralized system maintains connectivity.

The new Signal and Power Solutions segment will act as the nervous system in the vehicle by enabling high-speed data fluidity within the next-gen architecture. This segment includes the cable management and connector products that contribute a further $1 billion of revenue to the top line.

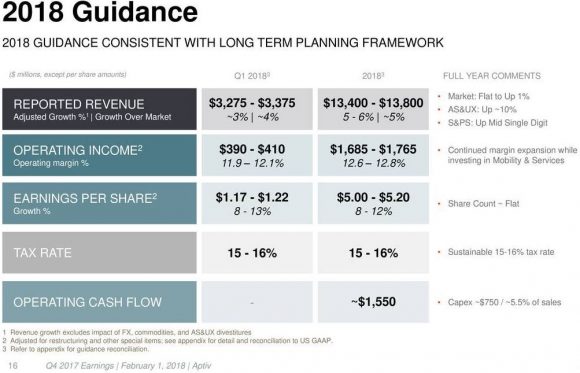

In total, Aptiv procured $12.9 billion in annual revenue in 2017, which was a boost of 4.9% from 2016. Earnings per share growth was up 10.5% YOY.

Investors cannot reasonably expect AV companies to annually grow top line by 20% to 30% as cloud companies, and the margins are unfortunately less savory. The dynamics of the business are different, and the revenue guidance of $13.4 to $13.8 billion should keep investors happy.

The pipeline is in fine fettle with $19.3 billion in bookings, which represent the lifetime gross revenue for consummated contracts.

Some of the outsized awards came in the form of an active safety contract with an OEM alliance, a high-voltage mobile charger contract from a leading North American EV producer, and an architectural contract for BYD's SUV platform in China.

It's no wonder both of the newly crafted segments expect a 10% boost in revenue for 2018.

NuTonomy is such a gem of a company that it is shocking that a large-cap tech firm declined to swoop in.

Half a billion is peanuts for such valuable and innovative technology.

Level 4 and Level 5 grade technologies are already starting to mature.

Other minor acquisitions of analytics firms Control-Tec and Movimento will initiate data monetization opportunities that effectively analyze their aggregated data then translate data into actionable profit-making opportunities.

Big data analytics are needed to decipher the path forward after compiling millions of miles of auto-robo data. And algorithms needing refinement are starving for the data, too.

A fully connected user experience will become standard in these robo-cars, and an integrated, optimized architecture is the secret sauce to commercialization of Level 4 and Level 5 automated vehicles.

Aptiv and Waymo are the only end-to-end system providers of the integrated brain and nervous system in a vehicle.

By late 2018, NuTonomy will have more than 150 Level 4 vehicles in live action.

Aptiv forecasts about $300 million in revenue from Level 4 or Level 5 AV systems by 2025.

Level 4 is practically autonomous - ready with a driver waiting to take control if need be.

Level 1, 2 and 3 revenues will mushroom to $1.8 billion per year, more than tripling from $500 million today.

Ottomatika, a Carnegie Mellon University spin-off founded in 2013, which provides software for self-driving cars, and NuTonomy are the in-house duo entirely focused on complex Level 4 and Level 5 solutions.

The shared access to the system has been set up to allow multiple teams access to the algorithms and technology that feeds through to other parts of the business.

Aptiv PLC is the perfect company to place in a buy and forget portfolio because AV monetization is still in its incubation phase.

Just as investors of pure cloud plays recently have been rewarded in spades, pure AV technology companies will be rewarded as mass rollouts of for-profit services become commonplace.

__________________________________________________________________________________________________

Quote of the Day

"The only constant in the technology industry is change." - said CEO of Salesforce Marc Benioff

Mad Hedge Technology Letter

April 11, 2018

Fiat Lux

Featured Trade:

(WHY YOU SHOULD BE BETTING THE RANCH ON TECHNOLOGY),

(AMZN), (NFLX), (FB), (Samsung), (Tencent)

Global IT spending is forecasted to surpass $3.7 trillion in 2018, a boost of 6.2% YOY, according to a report released by leading technology research firm Gartner, Inc. (IT).

This year is the best growth rate forecasted since 2007, and is a precursor to a period of flourishing IT growth.

IT budgetary resilience is oddly occurring in the face of a tech backlash engulfing Mark Zuckerberg as collateral damage during higher than normal volatility due to an unstable geo-political environment and nonstop chaos in the White House.

Zuckerberg's reputation has been torn to shreds by the media and politicians alike.

Tech has had better weeks and months, for instance as this past January when tech stocks went up every day. Facebook (FB) still had a great business model in January as well.

The biggest takeaway from the report was the outsized capital investments going into enterprise software, which spurs on exponential business formation.

Enterprise software will successfully record its highest spend rate increasing by 11.1% YOY to $391 billion. This is far and away an abnormally fast pace of increase, but is completely justified based on every brick and mortar migrating toward data harnessing.

The software industry will benefit immensely by the universal digitization of all facets of life as software acts as the tool that businessmen use to propel companies to stardom.

Application software spending will healthily rise into 2019, and infrastructure software also will continue to grow, boosted by the revamping of laggard architecture.

Data center systems are predicted to grow 3.7% in 2018, down from 6.3 percent growth in 2017. The longer-term outlook continues to have challenges, particularly for the storage segment.

The lower relative rate of spend is exacerbated by the chip shortage for memory components, and prices have shot up faster than previously expected.

The new Samsung Galaxy 9 cost an additional $45 in semiconductor chip costs because of the importunate costs that sabotage cost structures.

Exorbitant pricing was set to subside in the early part of 2018, but the dire shortage of chips is here to stay until the end of 2018.

Even though the supply side has ramped up 30%, demand is far outpacing supply, spoiling any chance for tech devices to be made on the cheap.

Global spend for digital devices will grow in 2018, reaching $706 billion, an increase of 6.6 percent from 2017. Not only will we see the standard characters such as phones and tablets, but new creative ways to produce devices in the micro-variety will soon populate our shores.

Amazon Alexa and Apple's HomePod are just the beginning and will spawn micro-devices that would fit nicely into a flashy James Bond film.

The demand for ultra-mobile premium smartphones will slow in 2018 as more consumers delay their upgrade and feel comfortable using older devices -- kind of like a smashed-up Volvo station wagon handed down from sibling to sibling.

In times of uncertainty, corporations hold back spending until the near-term variables can be flushed out, and unforeseen costs causing operational turbulence can be anticipated.

However, the industry has brushed aside the turmoil that has attempted to infiltrate the core growth story.

Investors cannot overlook that total tech spending growth for 2018 is the highest in the past 15 years.

Next quarter's earnings are now on tap, and investors will turn to fundamentals as a cheat sheet for what's in store.

It's undeniable that currently tech stocks aren't cheap anymore. They are also more expensive than they were at the beginning of the year barring Facebook and a few other stragglers.

The momentum has intensified with the five biggest tech firms accounting for more than 14% of the S&P 500 index's weighting.

Tech's relative performance has fended off the bears with PE multiples down a paltry 4.9% this year compared to the cratering of 11.4% in the general market.

And tech is still trading at a tiny fraction of the crisis of the dot-com era.

The outsized reinvestments back into business models don't tell the tale of an industry brought down to its knees begging for salvation.

Look no further than across the Pacific Ocean. Samsung Electronics Co. represents almost 25% in South Korea's Kospi index. At the same time, Asia's most valuable company, Tencent Holdings, makes up almost a 10% weighting in Hong Kong's Hang Seng Index.

Back stateside, about 90% of US tech firms beat revenue estimates in the last quarter of 2017, marking the best success rate for any industry.

The positive sentiment has continued into this year with wildly bullish expectations led by the FANG stocks.

The broader volatility is a gift to investors who hesitated and missed the monster rally that has graced tech the past few years.

Tech is vital to emerging markets. And this is the first year since 2004 that tech constitutes the biggest sector in the MSCI Emerging Markets Index blowing past financials.

Tech had a 28% weighting at the end of 2017, the weighting more than doubling from six years ago.

As it stands today, tech enjoys light regulation and by a long mile. Tech is actually the least regulated industry in America and has used this period of light regulation to stack up profits to the sky.

Banks are nine times more regulated than tech companies, and manufacturing companies are five times more regulated.

Legislation such as Dodd-Frank has done a lot to taper the excesses of the sub-prime frenzy that almost took down Wall Street.

The lean regulation has helped tech companies such as Facebook and Google build a gilt-edged competitive advantage that has been exploited to full effect.

After the Fed closed the curtains on its QE program, tech and its earnings are the sturdiest pillar of the nine-year bull market.

The Street is reliant on the big players to earn its crust of bread and show investors that tech isn't just a flash in the pan.

The two numbers acting as the de-facto indicators of the health of the overall economy are Netflix's subscriber growth numbers and Amazon's AWS Cloud revenue.

These two companies do not focus on profits and are the prototypical tech growth companies.

If they beat on these metrics, the rest of tech should follow suit.

The market is entirely dependent on big tech to drag investors through the time of transition. My bet is that tech will over-deliver booking stellar earnings.

__________________________________________________________________________________________________

Quote of the Day

"By giving the people the power to share, we're making the world more transparent." - said Facebook CEO Mark Zuckerberg

Mad Hedge Technology Letter

April 10, 2018

Fiat Lux

Featured Trade:

(WHY I'M PASSING ON ORACLE),

(ORCL), (MSFT), (AMZN), (CRM)

To say 2018 is the Year of the Cloud is an understatement.

Oracle (ORCL) felt the tremors of investors' fickle preference for quality cloud growth when the stock sold off hard after earnings that were relatively solid but unspectacular.

Oracle is a Silicon Valley legacy firm established in 1977 under the name of Software Development Laboratories. The company was co-founded by Larry Ellison, Bob Miner, and Ed Oates and the name later was changed to Oracle.

The company made its name through database software and still relies on it for the bulk of its $37 billion in annual revenue.

Legacy companies are put through the meat grinder by investors, and analysts are micro-sensitive to just a few narrow-defined metrics.

Not all cloud companies are treated equally.

It has become consensus that the only way to move forward is through advancing the cloud model, and neglecting this segment is a death knell for any quasi-cloud stock.

Oracle skirted any sort of calamitous earnings performance but left a lot to be desired.

Cloud SaaS (software-as-a-service) revenue for the quarter was $1.2 billion, up 21% YOY, and growth rates were in line with many that are part of the winners' bracket.

Oracle's overall cloud business is still a diminutive piece of its overall business constituting just 16%, which is incredibly worrisome.

This number accentuates the lack of brisk execution and its late entrance into this industry.

Gross cloud margin only increased 2% to 67%, up from 65% QOQ, providing minimum incremental growth.

Total cloud revenue guidance was substantially weak, which includes SaaS, PaaS (platform-as-a-service) and IaaS (infrastructure-as-a-service) expected to grow 19% to 23% in 2018, much less than the forecasted guidance of 27%.

Oracle should be growing its cloud segment faster, especially since its cloud business is many times smaller than competition, and growing pains habitually occur later in the growth cycle.

The outsized challenge is attempting to leverage its foundational database business to convince existing corporate clients to adopt Oracle's in-house cloud services instead of diverting capital toward cloud offerings from Microsoft (MSFT), Salesforce (CRM), or Amazon (AMZN).

It could be doing a better job.

Weak guidance of 1%-3% for annual total revenue topped off a generally underwhelming cloud forecast.

The lack of over-performance is highly disappointing for a company that has been touting its pivot to cloud.

The message from Oracle is the transformation is nowhere close to finished. That was investors' queue to stampede for the exits.

Investors only need to look a few miles up the coast at the competition.

Salesforce is putting up solid numbers, and many cloud companies are judged solely on a relative basis to the industry leaders.

The turnaround companies are getting crushed by these growth magnates. Salesforce is sequentially increasing total revenue over 20% each quarter and expects total revenue to rise more than 20% in 2019. It has set ambitious revenue targets for 2020, 2030, and 2040.

Microsoft Azure grew cloud revenue 98% QOQ, and Microsoft Windows, its legacy business, only makes up 42% of Microsoft's total revenue and is shrinking by the day.

Microsoft has earned its positon as the King of the Legacy Businesses offering proof by way of its position as the industry's second-best cloud company, engineering cloud quarterly revenue of $7.8 billion and gaining on Amazon Web Services (AWS).

Microsoft was in the same situation as Oracle a few years ago, stuck with a powerful business in a declining industry. It then turned to the cloud and never looked back.

Instead of leveraging databases, Microsoft leveraged its operating system and proprietary software to persuade new clients to adopt its cloud platform - and the numbers speak for themselves.

Oracle still has the chance to pivot toward the cloud because its database product is a brilliant entrance point for potential cloud converts.

In the meantime, Amazon has its sights set on Oracle's database product and plans to go after market share.

Oracle believes its database product is the best in the business - more affordable, quicker, and dependable. However, technology is evolving at such a rapid pace that these nimble companies can flip the script on their opponents in no time.

It's a dangerous proposition to compete with Amazon because of the nature of competing means dumping products, and unlimited cash burn battering opponents into submission by crushing profitability.

Oracle's margins would get hammered in this circumstance at a time when Oracle's gross margins have been a larger sore spot than first diagnosed.

Legacy companies are unwilling to enter price wars with Amazon because they still have dividends to defend and profit margins to nurture skyward.

Concurrently, Salesforce and Microsoft Dynamics CRM are attacking Oracle's CRM products (Customer Relationship Management), which could further impair margins.

The breadth of competition showed up to the detriment of margins with PaaS and IaaS gross margins eroding from 46% YOY, down to 35% YOY.

Microsoft's cloud revenue eked out a better than 60% gross margin even with its gargantuan size.

Investors punished Oracle for whispers of its cloud business plateauing with a size that is just a fraction of Microsoft Azure.

The leveling out is hard to take after Larry Ellison claimed cloud margins would soon breach 80% in upcoming quarters.

Conversely, Microsoft has claimed margins could start to erode as the company reallocates capital into expanding its cloud infrastructure, but it is understandable for maturing companies that must battle with the law of large numbers.

At the end of the day, Oracle's cloud business is failing to grow enough.

Oracle's competitors are speeding down the autobahn while Oracle has been dismissed to the frontage road.

Growth impediments with the small size of Oracle's cloud business is a red flag.

Avoid this legacy turnaround story that hasn't turned around yet.

Oracle looks like a value play at this point and could rise if it gets its cloud act together or the mere anticipation of a resurgence.

But with margins and competition pressuring its attempts at transformation, I would take a wait-and-see approach.

It's clear that Oracle is in the third inning of its turnaround, and teething problems are expected.

If you get the urge to suddenly buy cloud stocks, better look at any dip from Microsoft, Salesforce, and Amazon, which all directly compete with Oracle but are performing at a much higher level.

__________________________________________________________________________________________________

Quote of the Day

"A company is like a shark, it either has to move forward or it dies." - said Oracle co-founder Larry Ellison.

Mad Hedge Technology Letter

April 9, 2018

Fiat Lux

Featured Trade:

(HOW TO LOSE MONEY IN TECHNOLOGY STOCKS),

(AAPL), (MSFT), (OFO), (UBER), (MOBIKE), (OneCoin), (BABA)

Every new bull market in technology brings its excesses, and this time is more different.

Today, I'll outline some of the more egregious cases, which you and your money should avoid like the plague.

Spoiler alert: You are better off just parking your money in Apple (AAPL) or Microsoft (MSFT) and then forgetting about it.

The thirst to own a little sliver of technology in the greatest bull market of all time has reached a fever pitch with capital allocating to marginal assets.

Serious investors need to avoid the madness.

The excess was bred from the realization of how valuable data extraction and generation is to profitability.

The investment climate is reminiscent of the dot-com bubble during the 1990s that spawned companies with no intention of ever turning a profit.

This time, loss-making is blatant.

Ride-share vehicle services such as Uber and Lyft are great at losing money, and passengers would stand aside if prices became exorbitant.

Paying a derisory sum to ride in someone else's car while being chauffeured around is part of the allure of this business model.

The result is an artificially low price for the benefit of consumers amid a vicious price war with competitors.

The biggest problem with these ride-share services is they create nothing.

They are not building a proprietary operating system or creating technology that did not exist before.

Hence, these types of companies execute risky strategies that backfire.

Any technology company that expects to be in the game long term must create something unique and organic that other companies value and cannot copy.

These ride-hailing companies simply use an app on a smartphone, and this smartphone app can be created by any half decent high school app programmer.

Uber lost $4.5 billion in 2017, and that was great news for CEO Dara Khosrowshahi because Uber is losing less than before.

If you thought a tech company glorifying an annual loss of $4.5 billion was strange, then analyzing the state of the ride-share business model for the industry one degree further out on the risk curve will leave you scratching your head.

And by the way, Uber will try to soak your wallet when it launches its initial public offering next year.

Enter dockless ride-sharing bicycles.

Dockless bike-sharing has mushroomed around the world, spreading like wildfire fueled by grotesquely large injections of venture capital.

Ofo, a Chinese firm, initially raised more $1.2 billion and another $866 million from Alibaba (BABA) from a recent round of fundraising. CEO Dai Wei has stated that his company is worth north of $2 billion.

Mobike lured in more than $900 million in venture capital.

China is the epicenter of the bicycle ride-sharing experiment. More than 40 firms have sprouted up creating a bizarre scenario in major Chinese cities because of these companies dumping bicycles on every public street corner.

According to Xinhua News Agency, more than 2.5 million bikes are littered throughout the city by 15 companies in Beijing alone.

Local American firms have jumped on the bandwagon, too, with examples such as LimeBike, based in San Mateo, CA, that raised $12 million from Andreessen Horowitz in 2017, and topped up another $50 million from Coatue Management.

Meanwhile, Spin, the first stationless bikeshare company in the US, raised $8 million led by Grishin Robotics.

More than 40 bike-sharing companies have beat down the price of renting a bicycle to the paltry rate of 1 RMB (renminbi) ($0.15 USD) per 30-minute trip.

The intentional dumping at absurd price levels is not sustainable. The business model is predicated on collecting an initial deposit of $15 before a customer can hop on a bike.

The deposit has proved high risk as some companies have disappeared or gone bust.

Bluegogo, the third leading company in this space, emptied out its headquarters office, locked the doors, and failed to notify employees who claimed their wages had been garnished.

By last count, Bluegogo had distributed roughly 700,000 bicycles, and was estimated to have 20 million users, each paying $15 deposits to use the service.

Bluegogo was considered a legitimate competitor in the space along with Mobike and Ofo.

The $300 million dollars in Bluegogo deposits floated up to money heaven, and the deposits will never be repaid to customers.

Didi Chuxing, China's version of Uber and subsidiary of Tencent and Alibaba (BABA), purchased the bankrupt bike-sharing company, paid the work staff, and slipped them inside its portfolio of emerging tech firms in January 2018.

Mingbike, which failed in Shanghai and Beijing, migrated to emptier pastures in third and fourth tier Chinese cities and sacked 99% of its staff.

All told, $3 billion to $4 billion has been funneled into these bicycle-share monstrosities in the past 18 months.

It gets a lot worse in terms of high risk.

Another frontier of interest that has gone absolutely bananas is the ICO (Initial Coin Offering). ICOs are an unregulated new cryptocurrency venture raising funds by crowdfunding. A certain percentage of coins is sold to early investors in exchange for legal tender or Bitcoin.

This controversial means of raising money is a hotbed for scams galore. Of 1,000 that now exist, maybe 10 are legit.

These criminals are taking advantage of the headline effect of cryptocurrencies, promising every Joe and Jane early retirements and an easy way to provide college funds for children.

It's true that a founder of a cryptocurrency demonstrably benefits financially from leading this new form of payment.

Simply put, these ICOs function as Ponzi schemes with the last one to buy holding the bag when the sushi hits the fan after the founders run for the exits.

These fraudulent ICOs take on some of the characteristics of real Ponzi schemes such as guaranteed profits, promising their blockchain technology will solve all of the world's ills, no detailed roadmap except collecting funds, and lack of an online digital footprint.

Adding to the outsized risk is the confusion of which jurisdiction these companies are in and absence of any proper compliance.

OneCoin was a cryptocurrency promoted by offshore companies OneCoin Ltd (Dubai) and OneLife Network Ltd (Belize), founded by Ruja Ignatova. Many of the shady characters crucial to OneCoin were architects of similar Ponzi schemes, which was a dead giveaway to authorities.

Bulgarian enforcement officials raided and hauled away servers and other sensitive evidence at OneCoin's office in Sofia, Bulgaria, at the request of the prosecutor's office in Bielefeld, Germany.

German police and Europol also busted 14 other companies connected to OneCoin.

OneCoin CEO Ignatova was imprisoned in India for swindling investors after being investigated by Indian authorities in 2017.

The Ministry of Planning and Investment of Vietnam even issued a rebuttal that a forged document OneCoin used as proof to show it was the official licensed cryptocurrency in Vietnam was fake. It stated there was no possibility this document could ever exist.

SEC chairman Jay Clayton recently chimed in after being asked if all ICOs are fraudulent, boldly stating, "Absolutely not."

Uber and Ofo also are not frauds, but that does not mean investors should take a flier on it.

The strength of technology has attracted the marginal character to its doorstep; separating the wheat from the chaff is more important than ever.

These nascent industries can look good in the shop window, and slick advertising campaigns numb our rational decision making, but investors need to stay away at all costs.

The bicycle-sharing industry is a way for cash-rich venture capitalists to hoard data for applications irrespective of operating at a profit. The ICOs are charlatans attracted to the fluid cash flow tech companies command desiring a share in the spoils.

Keep your money in your pockets and wait for my next actionable trade alert.

__________________________________________________________________________________________________

Quote of the Day

"Stay away from it. It's a mirage, basically." - said legendary investor Warren Buffett when asked about cryptocurrency.