The Market Outlook for the Week Ahead

Ahhhh…the wonders of global excess liquidity.

Last week saw senior-level felony convictions, the real estate and auto industries rolling over and playing dead, rising inflation, escalating trade wars, sagging exports. It’s as if an entire flock of black swans landed on the markets.

And what did stocks do? Rocket to new all-time highs, Of course! What, are you, some kind of dummy? Didn’t you get the memo? With $50 trillion of global excess liquidity spawned by a decade of quantitative easing, of course stocks will go straight up, forever!

Until they don’t.

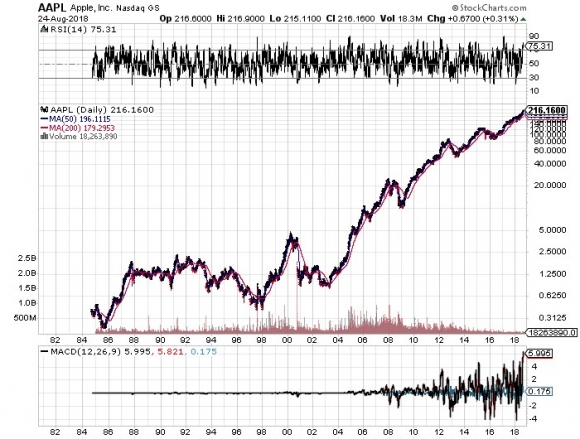

Even my favorite, Apple (AAPL) blasted through to new highs at $219 after an analyst raised his target to $245. You may recall me loading the boat with Apple calls during the February meltdown when the shares hit $150.

My target for Apple this year was $200, which I then raised to $220. Am I going to raise my target again? No. As my late mentor, Barton Biggs used to say, “Always leave the last 10% for the next guy.”

It kind of makes my own split adjusted cost of Apple shares of 50 cents, which I picked up in 1998, look pretty good. Yup. That double bottom on the charts at 40 cents said it all.

I used the strength to increase my cash position from 80% to 90%, unloading my long position in Walt Disney options at cost. That leaves me with a single short position in bonds (TLT), which have to see yield on the 10-year U.S. Treasury bond market to fall below 2.67% in three weeks before I lose money.

I am even focusing a sharp eye on the Volatility Index (VIX) for a trade alert this week. If you buy the January 2019 (VXX) $40 calls at $2.90 and the ETF rises 25 points to its April high of $54, these calls would rocket by 382% to $14.00. Sounds like a trade to me! Then I can say thank you very much to Mr. Market, thumb my nose at him, and then take off for the rest of the year. TA-TA!

In the meantime, much of industrial America is getting ready to shut down. Tariffs on 50% of all Chinese imports come into force in September. It turns out that you can’t make anything in the U.S. without the millions of little Chinese parts you’ve never heard of, which also have no U.S. equivalent.

Factories will have to either pass their costs on to consumers in a deflationary economy or shut down. What the administration has done is offset a tax cut with a tax increase in the form of higher import taxes. It was not supposed to work out like that.

The bond rally has pared back my August performance to a dead even at 0.02%. My 2018 year-to-date performance has pulled back to 24.84% and my nine-year return appreciated to 301.31%. The Averaged Annualized Return stands at 34.76%. The more narrowly focused Mad Hedge Technology Fund Trade Alert performance is annualizing now at an impressive 32.24%.

This coming week will be real estate dominated on the data front.

On Monday, August 27, at 10:30 AM EST, we obtain the Dallas Fed Manufacturing Survey.

On Tuesday, August 28, at 9:00 AM EST, we get the June S&P CoreLogic Case-Shiller National Home Price Index. Will we start to see the price falls that more current data are already showing?

On Wednesday, August 29, at 10:00 AM EST, we learn July Pending Home Sales, which lately have been weak.

Thursday, August 30, leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a fall of 2,000 last week to 210,000.

On Friday, August 31, at 10:00 AM EST, we get Chicago Purchasing Managers Index for July. Then the Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me, I think I’ll pop over to the Pebble Beach Concours d'Elegance vintage car show this weekend and place a bid on Ferris Bueller’s red 1962 Ferrari GT California. It’s actually a Hollywood custom chassis built around a Ford engine. I can’t afford a real vintage Ferrari GTO, one of which is expected to sell for an eye-popping $60 million this weekend.

Good luck and good trading.