Mad Hedge Technology Letter

February 21, 2018

Fiat Lux

Featured Trade:

(HOW CISCO SYSTEMS GOT ITS MOJO BACK)

(CSCO), (JNPR), (NOK), (MSFT)

??

Mad Hedge Technology Letter

February 21, 2018

Fiat Lux

Featured Trade:

(HOW CISCO SYSTEMS GOT ITS MOJO BACK)

(CSCO), (JNPR), (NOK), (MSFT)

Global Market Comments

February 21, 2018

Fiat Lux

SPECIAL FANG ISSUE

Featured Trade:

(FINDING A NEW FANG),

(FB), (AAPL), (NFLX), (GOOGL),

(TSLA), (BABA)

Studying the history of the 1849 California Gold Rush, there is not a single miner who is known today.

But the merchants who sold them shovels, food, and blue jeans have banks, hotels, and universities everywhere with names like Huntington, Stanford, Crocker, and Hopkins.

The modern-day Levi and shovel slingers come in the form of the internet infrastructure equipment manufacturer Cisco Systems (CSCO).

Not only does 85% of Internet traffic navigate across Cisco's Systems' powerful routers, Cisco is also run online, from product orders to intra staff circulation of information.

A myriad of tech companies will largely use Cisco's network infrastructure to keep their operations at the cutting edge.

Cisco (CSCO) is an American technology conglomerate headquartered in the heart of Silicon Valley, that builds, manufactures, and peddles networking hardware and telecommunications equipment.

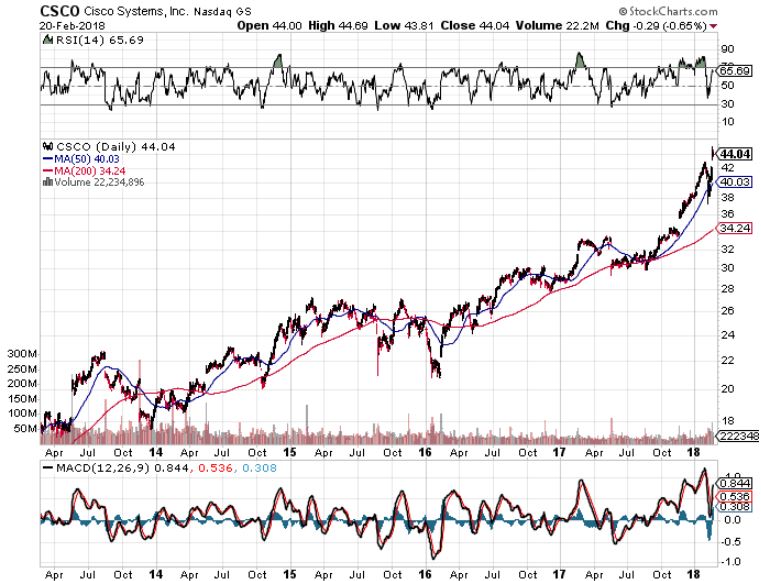

Cisco (CSCO) has finally come in from the cold after a long, hard 2-year slog that finally saw them return to revenue growth.

Quarter after quarter, Cisco (CSCO) was prisoned in the penalty box for sticking with their fading legacy business of network hardware solutions.

Even accumulating a massive $67 billion in profits from abroad, the company failed to impress investor sentiment as revenue sequentially dipped.

How did Cisco (CSCO) get their mojo back?

Cisco finally adopted the SaaS (Service as a subscription) model that has been put to great use by all the high flyers. The one-time fee has been replaced by annual recurring charge generating a perpetual income stream.

The shift means 33% of income is now recurring subscription revenue, comprising 52% of the company's software sales. Cisco (CSCO) made US$5.5 billion from recurring software and subscription in the recent quarter.

Re-calibrating the business model has caused the deferred revenue segment to explode from a pedestrian 6%, just 10 quarters ago, to an impressive 33% now.

The progress has evoked broad based, positive investor sentiment and Cisco is just in the first phase of this secular trend.

Cisco hopes to transition as much business as it can to cloud-based subscriptions to enhance the customer experience.

One of the solutions offered is Cisco UCS Services for data centers. The data center aids business and has a spectacular future ahead of it. Services are aligned with business needs by unique network-based optimization. Cisco Data Center Services cuts operating costs while offering customers a high standard of service.

The plan for their subscription model is to offer pricing that is less than the one-time fee model, but offer premium add-ons to the base model. This incremental quality improvement will justify the recurring model also increase revenue per customer.

The advanced subscriptions will offer the newest cloud-based solutions that Cisco develops and gives impetus towards the SaaS model which has been a boon for the entire tech sector.

Data center was up double digits in the recent quarter, driven by server products as well as the HyperFlex offerings that drew in 2,400 new customers. Security tools have seen a rise in momentum, up 6% QOQ.

Total revenue was up 3% to $11.9 billion, and guidance growth for the next quarter was set at 3% to 5% on the back of the SaaS model, while maintaining vibrant operating margins of 31.7%, and a guided gross margin rate expected in the range of 63% to 64%. These are fantastic numbers.

The second part of the revitalization plan is the $66 billion of repatriated cash. $31 billion will go directly into share buybacks "over the next 18 to 24 months."

Cisco continues to prop up the dividend and remains committed to returning cash, thus exciting institutional investors. Cisco announced a $0.04 boost to the quarterly dividend to $0.33 per share, up 14% YOY.

Acquisitions are also a critical part of the overall strategy, as it always has been. Cloud-based Broadsoft was one of the latest companies scooped up by Cisco.

The company provides the building blocks for service providers to build cloud-based communications services such as voice, video, and web. BroadSoft was founded in 1998 and is headquartered in Maryland.

These little purchases may seem insignificant, but synergistic acquisitions added 80 basis points to the bottom line, and overall inorganic impact bumps up another 0.5 point to about 130 basis points.

Cisco (CSCO) will still be net cash positive of $10 billion to $12 billion and will scour the field for more acquisitions that will levitate growth and improve the product.

When you consider that Cisco's growth is occurring amid a backdrop of a robust domestic and global economy, and amid a trend for all companies to adopt a comprehensive digital blueprint then Cisco is perfectly placed to sell its services to cloud converts.

The digital bias is in the nascent phase, and once brick and mortar grapple with digitization and scalability or extinction, the trend will swiftly compound.

The modernization of the business model explains the surge in Cisco's share price from 2016. The shares have rocketed by an amazing 158% since then. Before that, they were stigmatized as a dying, archaic business that languished for years.

If investors cannot identify new growth drivers on the short-term horizon, they bail out. The two-pronged approach of their subscription model and reallocation capital plan will solidify the accelerating growth rhetoric. In other words, they now have a new "story" to sell.

Their peer group consists of Hewlett Packard (HPE), China's Huawei, Juniper Networks (JNPR), and Finland's Nokia (NOK). Microsoft (MSFT) and Cisco have demonstrated that tech dinosaurs can reinvent, reload, and revitalize a business model on the brink.

Such is the beauty of the digital economy where tinkering with a business model is just a few clicks away.

To learn more about Cisco Systems please click here.

While the Global Trading Dispatch focuses on investment over a one week to six-month time frame, Mad Options Trader, provided by Matt Buckley, will focus primarily on the weekly US equity options expirations, with the goal of making profits at all times. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

February 20, 2018

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GOING WHERE THE MONEY IS),

(SPY), (AAPL), (MU), (FB), (CRM), (AMZN), (T),

(THE REBIRTH OF THE MASTER LIMITED PARTNERSHIP),

(USO), (AMLP), (FPL), (MLPS), (MLPX)

Things have changed.

That is about the only conclusion one can reach after the three most violent weeks in stock market history.

The historic average length of time for a 10% correction is 64 days, or more than two months. This time we did it in nine.

However, we all learned important things from the experience.

For a start, if your financial advisor told you to sell all your stocks at the bottom fire them immediately. A lot did, because we could see it in the February 9 capitulation market volume. Selling lows and buying highs is certainly NOT the way to financial freedom and independence.

Also, we learned the value of the 200-day moving average. A whole bunch of Fibonacci support numbers kicked in right about the same place.

I have never been big on technical analysis, viewing it as the refuge of newbies and wanabees who can't figure out what else to do. They are the red meat for the algos.

However, I could see the S&P 500 (SPY) gunning for this number at $252, and sent you trade alerts to BUY as fast as I could write them as we approached it. But the 2,000 Dow rally that followed? That was the stuff of B-movies.

I was also willing to bet the ranch that technology would lead any recovery. This is the sector that every investor, from the day trading college student to the $100 billion hedge fund manager has been trying to get into at a decent price for years.

And tech delivered big time. It has been the most instant creation of market wealth in history, with my names of Apple (AAPL), Micron Technology (MU), Facebook (FB), Salesforce (CRM), and Amazon (AMZN) leading the charge.

And then to short the Volatility Index (VIX) at $39 and watch it halve in days? It boggles the mind.

Probably the smartest thing I have done in my 50-year trading career was to start the Mad Hedge Technology Letter on February 1.

The insights I am gaining with the additional research has not only substantially upped my game in technology, but all other asset classes as well. They're all connected.

Why technology, when more attractive opportunities beckoned with gold or Bitcoin newsletters?

To quote the famed bank robber, Willie Sutton, as to why he robbed banks, "It's where the money is."

By the way, you can still buy the Mad Hedge Technology Letter

at the inaugural price of only $2,000. The full $2,500 price kicks in on March 1. To learned more please click here. To get the discount price please email Nancy at customer support at support@madhedgefundtrader.com

One amazing concept that I have just stumbled across is that big tech has become the new defensive "safe play", replacing the high yield telecom stocks of old, like AT&T (T).

Apple is already the largest dividend payer in the United States in absolute dollar terms. It is returning a stunning 90% of its gargantuan free cash flow to shareholders, with some 72% going to share buybacks alone.

After a 17-year hiatus, Apple resumed its dividend five years ago (Steve Jobs hated the idea), and now stands at a 1.46% yield. The company has since boosted its dividend by 10% every April like clockwork.

We here at Mad Hedge Fund Trader made a heroic effort to help followers of our Trade Alert service cope with the most tumultuous market in history.

At the worst of the worst we were down only -8%, and fought tooth and nail to get back up to +5.5% by Friday. It was a performance for the ages. It is also a vindication of the trading strategy I have been pursuing for the last decade.

If you can survive this week, you can survive anything. You are totally bombproof.

We only got nicked at the end with a short position in Apple which we picked up two days too soon. But then how often does the world's largest company rise in value by 12% in four days, adding $125 billion in market capitalization?

How about once a lifetime.

We are now done with Q4 earnings season, so the dominant factor will be the Fed governors who will be speaking at public appearances every day of this shortened week. No doubt inflation will be a hot topic, a definite market negative.

On Monday, February 19, the markets were closed for Presidents Day.

On Tuesday, February 20 no data releases of note take place.

On Wednesday, February 21, at 10:00 AM EST, we get January Existing Home Sales. The FOMC minutes of the last Fed meeting on interest rates will be released at 2:00 PM.

Thursday, February 22 leads with the 10:00 EST release of the Index of Leading Economic Indicators, a read on ten data points giving a read on economic performance six months into the future.

On Friday, February 23 at 1:00 PM we receive the Baker-Hughes Rig Count, which saw no change last week.

As for me, I am trying to get rid of the tag ends of pneumonia I have been dealing with for the past month, the result of my January battle with the flu.

I think I'll head over to Squaw Valley and dive down a couple of double black diamond slopes. I hear that exercise helps clear the lungs.

Good luck and good trading!

Mad Hedge Technology Letter

February 20, 2018

Fiat Lux

Featured Trade:

(MASAYOSHI SON'S VISION TO TAKE OVER THE WORLD),

(SFTBY), (BABA), (NVDA)

The wild west of the data wars is spawning into an all-out, gun slinging shoot out with a winner takes all mentality.

This slug fest is reminiscent of the unregulated 19th century American oil barons whose clout and complete control of the supply of oil fueled the industrial revolution that drove America's economy to the top of the global food chain.

Yes, data has become the oil of the 21st century. It is the oxygen of the next leg of the Internet revolution.

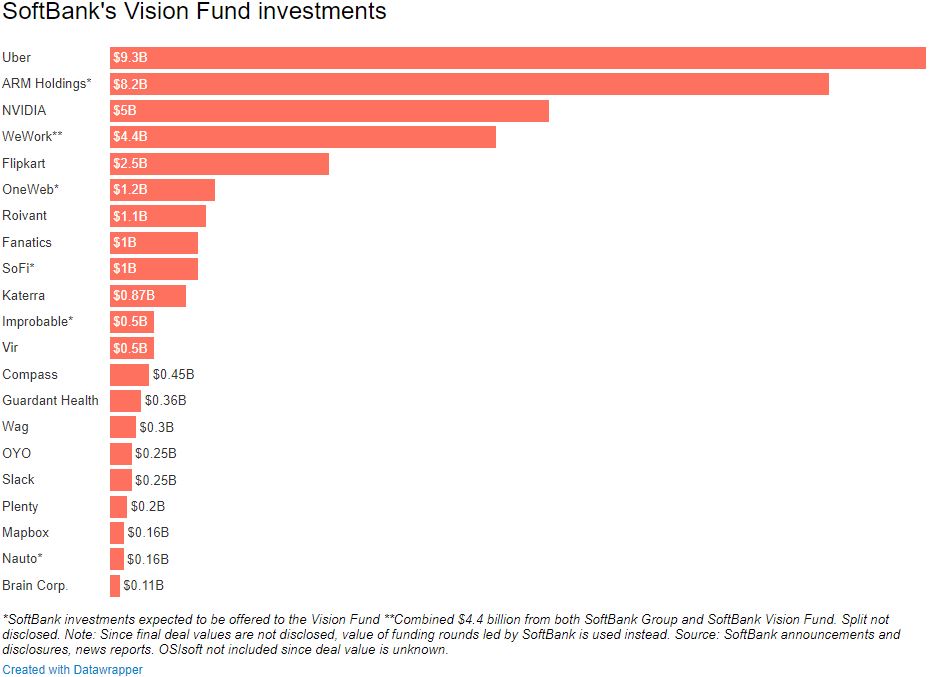

And there is one man moving early to stake out the premium real estate of our futures: Softbank's Masayoshi Son. His $100 million Softbank Vision Fund is not only creating waves in Silicon Valley, but tidal waves.

Many countries, like Iran, Saudi Arabia, and Russia, still rely on petroleum for the lion's share of government revenues. Even though oil is still integral to the growth of the global economy, there is a new sheriff in town: big data.

Cut it up anyway you want, data is simply information, the "zeros" and "ones" that make up the digital world. The information that commands mouthwatering premiums these days can be unraveled by computers.

Computer deciphered data can show behavioral and consumer trends in stark daylight, helping companies ferret out business strategies are proving immensely powerful.

There is an exponential hockey stick effect going on here. As the quantity of data accumulates, the more valuable it becomes.

The types of data being collected are personal data, transactional data, web data, and sensor data used for IoT (Internet of Things) products.

Who is the major player vacuuming up this data?

Masayoshi Son, the CEO of Softbank (SFTBY), an ethnic Korean who grew up in a small village in Japan. He transferred to the San Francisco Peninsula Serramonte High School as an ambitious youth and graduated in 3 weeks.

Son ventured on to UC Berkeley majoring in economics and computer science. He is one of the most dynamic people in the World and has amassed personal wealth of around $25 billion.

A few of his brilliant pre-emptive strikes were seed investing in Yahoo, creating Yahoo Japan, and $20 million for a stake in Alibaba (BABA) in 1999. These investments increased more than 100-fold in value.

Son is on a mission to own or control assets that are the linchpin to global growth nourished by Artificial Intelligence in selective industries such as transportation, food, work, medicine, and finance.

The anchor that ties all these firms together is the massive hordes of data they harvest, which are central to directing how future automated robots and machines perform.

His goal envisions the construction of responsive robots that will emerge as the cash cow in 2045. The construction, utilization, and high performance of these machines will be the key to his vision.

Instead of splurging for premium human data, investors will be competing for the best performing robots and the data derived from them. Accurate human data will provide the springboard to the machine data these robots will generate.

After the first generation of robots endow us with their first batch of data, all human data will be irrelevant. Human information is the test case that robots are founded on.

Once the first cohort of robot data comes to market, the 2nd generations of robots will be derived off the 1st generation of robots. Humans will become irrelevant.

Once you marry the treasure trove of data with A.I., the results will enter the realm of today's science fiction. Imagine being the first CEO to bring functional robots to mass market and how valuable that first batch of robot data would represent.

In short, Son is positioning himself to organically engineer the highest-grade robots catalyzing the next gap up in global competition.

This year, Son is on a global treasure hunt to meld together the most precise "big data" he requires to build his robot squadron that will take over the world.

The fight these days is acquiring the oxygen to power these non-human contraptions. Without pure oxygen, i.e. massive amounts of data, engineers will create faulty robots that under-perform.

Looking at the amalgam of companies in which Son has invested, it is difficult to find any rhyme or reason. That is until you find the commonalty of big data.

Son invested $200 million in "Plenty" in July 2017, a company developing indoor farms. If indoor farm data is not diverse enough, then how about the $300 million he showered on San Francisco dog-walking app called "Wag".

The biggest holding in the Softbank Vision Fund is Uber. Uber is ubiquitously known as a ride sharing company that shuttles passengers from spot A to spot B.

Sweetening the deal was a substantial discount the Vison Fund received on a private placement of Uber shares. Uber is now worth about $70 billion and may someday become a FANG in its own right.

Supplementing this transaction is the custom online map app Mapbox, founded as a competitor to Google Maps. Some of Mapbox's partners include Snapchat, Lonely Planet, and The Weather Channel.

Vision Fund's second largest position is ARM Holdings, which is an English semiconductor chip company that has carved out a large segment of the Android and laptop market.

They produce simple CPU's (central processing units) and much more advanced GPU's (graphics processing units) that are placed in smartphones, TV's, tablets, and computers.

Son has shelled out $8.2 billion through the Softbank Vision Fund and the remaining 75% stake is owned by parent company Softbank Group. ARM is one of the shining beacons of European tech and Softbank has pegged its future to its success.

Unsurprisingly, Nvidia (NVDA) is the 3rd largest weighting and the $5 billion Softbank investment into Nvidia (NVDA) represents a 4.9% stake in the company. The Nvidia commitment is logical considering ARM licenses their chip designs to Nvidia.

As autonomous vehicles will be one of the first benefactors from the cross pollination between big data and automation, these investments completely justify Son's long-term vision.

Son has also snapped up other ride sharing entities such as Didi Chuxing in China, Ola in India, Grab in Southeast Asia, and "99" in Brazil.

Some 31% of the global population is without Internet connectivity. Thus, Son bought OneWeb, which pioneers low cost, high quality satellites striving to grant Internet access for the people still without access. This maneuver will surely see his net data load increase.

In many of the Mad Hedge Technology Letters, we often offer readers the creme de la creme of public stock symbols, but this time it is different.

First, the major holdings in the Softbank vision fund, aside from Nvidia, are privately held companies that do not trade on any stock market.

However, it is very important to watch what he buys, as it gives insights into the best performing and fastest growing sub-sectors of technology.

Or you could just buy Softbank itself, whose shares have doubled over the past two years.

Son won't just flip these companies for a 30% or 50% profit. Tenfold, or hundred-fold gains are the order of the day.

In reality, Son's ultimate goal is to leach out the future aggregate data spewing out from his underlying portfolio and cross-pollinate it with A.I. and automation to revolutionize the world.

This year is a period of jockeying with other venture capitalists to positions themselves accordingly for the next 30, 40 and 50 years.

Welcome to the future.