Global Market Comments

April 17, 2018

Fiat Lux

Featured Trade:

(HAS THE RECESSION ALREADY STARTED?)

(WHERE THE ECONOMIST "BIG MAC" INDEX FINDS CURRENCY VALUE),

(FXF), (FXE), (CYB)

Global Market Comments

April 17, 2018

Fiat Lux

Featured Trade:

(HAS THE RECESSION ALREADY STARTED?)

(WHERE THE ECONOMIST "BIG MAC" INDEX FINDS CURRENCY VALUE),

(FXF), (FXE), (CYB)

It started with a slow drip.

Then it became a trickle.

Now it is an undeniable torrent.

Negative economic data reports, once as rare as hen's teeth, have suddenly become as common as NRA bumper stickers at a Trump rally. The economic data flow has definitely turned sour.

Is this a growth scare? Or is it the beginning of a full-blown recession, the return of which investors have been dreading for the past nine years.

The data flow was hotter than hot going into January, taking the stock market to a new all-time high.

We only got final confirmation of this a few weeks ago, when the last report on Q4 GDP rose by 0.2% to 2.9%, one of the best readings in years.

Then the rot began.

At first it was just one or two minor, inconsequential reports here and there. Then they ALL turned bad. Not by large amounts, but by small incremental ones, frequent enough to notice.

The February Dallas Fed General Business Activity Index dropped from 28 to 21, the March Institute of Supply Management Manufacturing Activity declined from 61 to 59, while Services Activity shaved a point, from 59 to 58.

The big one has been the March Nonfarm Payroll Report - that printed a soft 103,000 - which was far below the recent average of 200,000.

As recently as this morning, the National Association of Home Builders Sentiment Index dropped a point from 70 to 69.

When you see one cockroach, it is easy to ignore. When it becomes a massive infestation, it is a different story completely.

The potential explanations for the slowdown abound.

There is no doubt that the Trade War with China is eroding business confidence, as is the secret renegotiation of the North American Free Trade Agreement (NAFTA).

Decisions on major capital investments by companies were a slam dunk three months ago. Now, many are definitely on hold.

There is abundant evidence that the Chinese are scaling back investment in the US and pausing new trade deals with American counterparties. They have been boycotting purchases of new US Treasury bonds for eight months.

The new import duty for Canadian timber is raising the cost of low-end housing, worsening affordability and causing builders to cut back.

Instead they are refocusing efforts on high-end housing where profit margins are much wider.

Shooting wars with Syria, North Korea, and Iran are permanently just over the horizon, further giving nervous investors pause.

And the general level of chaos coming out of Washington, including the unprecedented level of administrations firings and resignations, are scaring a lot of people.

Since I am a person who puts my money where my mouth is every day of the year, I'll give you my 10 cents worth on what all this really means.

Two weeks ago I started piling into to an ultra-aggressive 100% "RISK ON" trading book, loading the boat with a range of asset classes, including longs in financial and technology stocks, and gold and big shorts in the bond market.

My bet is that while however serious all of the above concerns may be, they pale in comparison with Q1 2018 earnings growth of historic proportions that is now unfolding, prompted by the December tax bill.

The second 10$ correction of 2018 had nothing to do with fundamentals. It was all about hot money retreating to the sideline until the bad news waned and the good news returned.

And so it has. Forecast Q1 earnings are now looking to come in above 20% YOY. These will be reports for the ages.

My bet has paid off in spades, with followers of my Mad Hedge Trade Alert Service up 10.70% so far in April, up +17.46% in 2018, and up a breathtaking 54.04% on a trailing 12-month basis. It is a performance that causes my competitors to absolutely weep.

If fact, the rest of 2018 could play out exactly as it has done so far, with frantic sell-offs following the end of each quarterly reporting period, followed by slow grind-up rallies leading into the next. Technology will lead the rallies every time.

Which means we may go absolutely nowhere in the indexes 2018, but have a whole lot of fun getting there. If you see this coming you can make a ton of money trading around it.

With our current positions, Mad Hedge followers could be up 25% on the year as soon as mid-May.

Which raises the question of, "When will the recession really start?"

My bet is sometime in 2019, when earnings growth downshifts from 20% to 10% or even 5%.

If this happens in the face of an inverting yield curve where short-term interest rates are higher than long-term ones, and a continuing trade war AND shooting wars, and broadening Washington scandals, then a recession becomes a sure thing.

A bear market should precede that by about six months.

So date those high-risk positions, don't marry them.

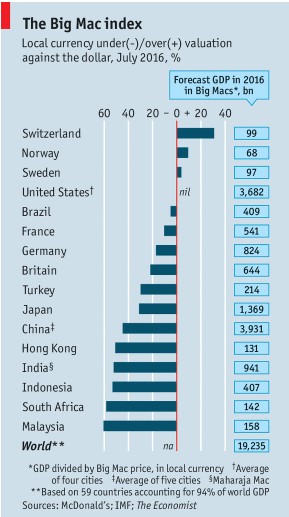

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its "Big Mac" index of international currency valuations.

Although initially launched as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

The index counts the cost of McDonald's (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai baht are cheap.

I couldn't agree more with many of these conclusions. It's as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool than a speedy lunch.

The World's Most Expensive Big Mac

Mad Hedge Technology Letter

April 17, 2018

Fiat Lux

Featured Trade:

(WHY THE CLOUD IS WHERE TRADING DREAMS COME TRUE),

(ZS), (ZUO), (SPOT), (DBX), (AMZN), (CSCO), (CRM)

Dreams don't often come true - but they do frequently these days.

Highly disruptive transformative companies on the verge of redefining the status quo give investors a golden chance to get in before the stock goes parabolic.

Traditional business models are all ripe for reinvention.

The first phase of reformulation in big data was inventing the cloud as a business.

Amazon (AMZN) and its Amazon Web Services (AWS) division pioneered this foundational model, and its share price is the obvious ballistic winner.

The second phase of cloud ingenuity is trickling in as we speak in the form of companies that focus on functionality, performance, and maintenance on the cloud platform.

This is a big break away from the pure accumulation side of stashing raw data in servers.

However, derivations of this type of application are limitless.

Swiftly identifying these applied cloud companies is crucial for investors to stay ahead of the game and participate in the next gap up of tech growth.

The markets' reaction to Spotify's (SPOT) and Dropbox's (DBX) hugely successful IPOs was head-turning.

Both companies finished the first day of trading firmly well above their respective, original opening prices -- or for Spotify, the opening reference price.

The pent-up momentum for anything "Cloud" has its merits, and these two shining stars will give other ambitious cloud firms the impetus to go public.

If Spotify and Dropbox laid an egg, momentum would have screeched to a juddering halt, and companies such as Pivotal Software would reanalyze the idea of soon going public.

Now it's a no-brainer proposition.

There are more than 40 more public cloud companies that are valued at more than a $1 billion, and more are in the pipeline.

To understand the full magnitude of the situation, evaluating recent IPO performance is a useful barometer of health in the tech industry.

The first company Zscaler (ZS) is an enterprise company focused on cloud security that closed 106% above its opening price when it went public this past March 16.

It opened up at $16 a share and finished the day at $33.

Zscaler CEO, Jay Chaudhry, audaciously rebuffed two offers leading up to the March 16 IPO. Both offers were more than $2 billion, and both were looking to acquire Zscaler at a discount.

The decision to forego these offers was a prudent move considering (ZS)s current market cap is around $3.3 billion and rising.

One of the companies vying for (ZS) was Cisco Systems (CSCO), which is also in the cloud security business. Cisco is looking to add another appendage to its offerings with the cash hoard it just repatriated from abroad.

Cisco has been willing to dip into its cash hoard by buying San Francisco-based AppDynamics for $3.7 billion in 2017, which specializes in managing the performance of apps across the cloud platform and inside the data center.

Cloud security is critical for outside companies to feel comfortable implementing universal cloud technology.

Storing sensitive data online in a storage server is also a risk and difficult to migrate back once on the cloud.

Without solid security to protect data, data-heavy companies will hesitate to vault up their data in a public place and could remain old-school with external data locations storing all of a firm's secrets.

However, this traditional approach is not sustainable. There is just too much generated data in 2018.

Cybersecurity has expeditiously evolved because hackers have become greatly sophisticated. Plus, they are getting a lot of free PR.

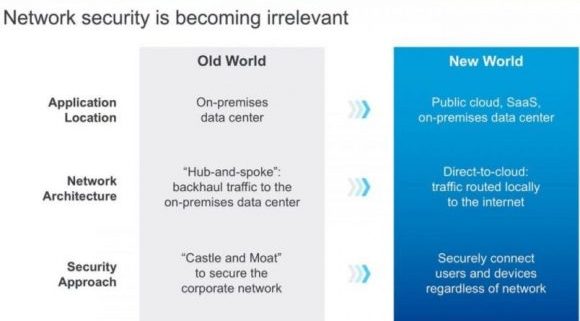

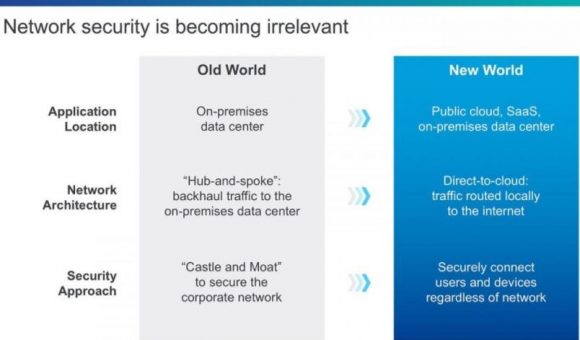

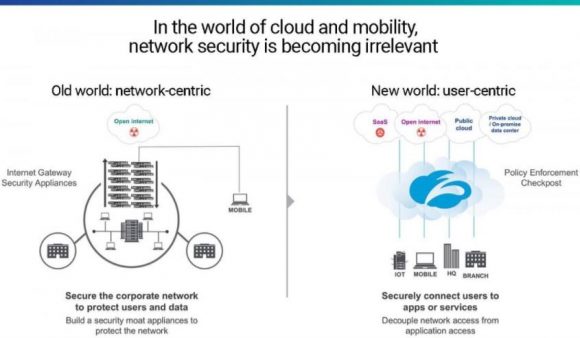

Data center and in-house applications secured operations by managing access and using an industrial strength firewall.

This was the old security model.

Security became ineffective as companies started using cloud platforms, meaning many users accessed applications outside of corporate networks and on various devices.

The archaic "moat" method to security has died a quick death, as organizations have toiled to ziplock end points that offer hackers premium entry points into the system.

Zscaler combats the danger with a new breed of security. The platform works to control network traffic without crashing or stalling applications.

As cloud migration accelerates, the demand for cloud security will be robust.

Another point of cloud monetization falls within payments.

Tech billing has evolved past the linear models that credit and debit in simplistic fashion.

SaaS (Software as a Service), the hot payment model, has gone ballistic in every segment of the cloud and even has been adopted by legacy companies for legacy products.

Instead of billing once for full ownership, companies offer an annual subscription fee to annually lease the product.

However, reoccurring payments blew up the analog accounting models that couldn't adjust and cannot record this type of revenue stream 10 to 20 years out.

Zuora (ZUO) CEO Tien Tzuo understood the obstacles years ago when he worked for Marc Benioff, CEO of Salesforce (CRM), during the early stages in the 90s.

Cherry-picked after graduating from Stanford's MBA program, he made a great impression at Salesforce and parlayed it into CMO (Chief Marketing Officer) where he built the product management and marketing organization from scratch.

More importantly, Tzuo built Salesforce's original billing system and pioneered the underlying system for SaaS.

It was in his nine years at Salesforce that Tzuo diagnosed what Salesforce and the general industry were lacking in the billing system.

His response was creating a company to seal up these technical deficits.

Other second derivative cloud plays are popping up, focusing on just one smidgeon of the business such as analytics or Red Hat's container management cloud service.

SaaS payment model has become the standard, and legacy accounting programs are too far behind to capture the benefits.

Zuora allows tech companies to seamlessly integrate and automate SaaS billing into their businesses.

Tzuo's last official job at Salesforce was Chief Strategy Officer before handing in his two-week notice. Benioff, his former boss, was impressed by Tzuo's vision, and is one of the seed investors for Zuora.

These smaller niche cloud plays are mouthwateringly attractive to the bigger firms that desire additional optionality and functionality such as MuleSoft, integration software connecting applications, data and devices.

MuleSoft was bought by Salesforce for $6.5 billion to fill a gap in the business. Cloud security is another area in which it is looking to acquire more talent and products.

If you believe SaaS is a payment model here to stay, which it is, then Zuora is a must-buy stock, even after the 42% melt up on the first day of trading.

The stock opened at $14 and finished at $20.

One of the next cloud IPOs of 2018 is DocuSign, a company that provides electronic signature technology on the cloud and is used by 90% of Fortune 500 companies.

The company was worth more than $3 billion in a round of 2015 funding and is worth substantially more today.

These smaller cloud plays valued around $2 billion to $3 billion are a great entry point into the cloud story because of the growth trajectory. They will be worth double or triple their valuation in years to come.

It's a safe bet that Microsoft and Amazon will continue to push the envelope as the No. 1 and No. 2 leaders of the industry. However, these big cloud platforms always are improving by diverting large sums of money for reinvestment.

The easiest way to improve is by buying companies such as Zuora and Zscaler.

In short, cloud companies are in demand although there is a shortage of quality cloud companies.

__________________________________________________________________________________________________

Quote of the Day

"The great thing about fact-based decisions is that they overrule the hierarchy." - said Amazon founder and CEO, Jeff Bezos

While the Global Trading Dispatch focuses on investment over a one week to six-month time frame, Mad Options Trader, provided by Matt Buckley, will focus primarily on the weekly US equity options expirations, with the goal of making profits at all times. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

April 16, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WEEK THAT NOTHING HAPPENED),

(TLT), (GLD), (SPY), (QQQ), (USO), (UUP),

(VXX), (GOOGL), (JPM), (AAPL),

(HOW TO HANDLE THE FRIDAY, APRIL 20 OPTIONS EXPIRATION), (TLT), (VXX), (GOOGL), (JPM)