Mad Hedge Technology Letter

May 2, 2018

Fiat Lux

Featured Trade:

(FACEBOOK GOES FROM STRENGTH TO STRENGTH),

(FB), (AMZN), (GOOGL), (NFLX)

Mad Hedge Technology Letter

May 2, 2018

Fiat Lux

Featured Trade:

(FACEBOOK GOES FROM STRENGTH TO STRENGTH),

(FB), (AMZN), (GOOGL), (NFLX)

"We have not been investing this year, we have been on a battleground," said noted UK hedge fund manager Crispin Odey.

Everyone and their mother was waiting for Facebook (FB) to fluff their lines, but they defied the odds by posting solid performance.

The data police can go back to eating doughnuts because it is obvious that regulation won't fizzle out the precious growth drivers that Mark Zuckerberg relies on to please investors.

I even begged readers to buy the regulatory dip, and I was proved correct with Facebook shares rebounding from $155 to $173.

The dip buying was proof that investors have faith in Facebook's business model.

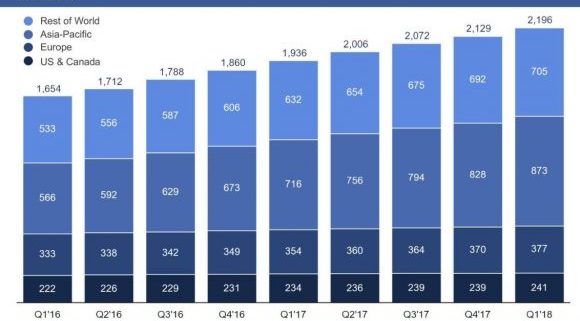

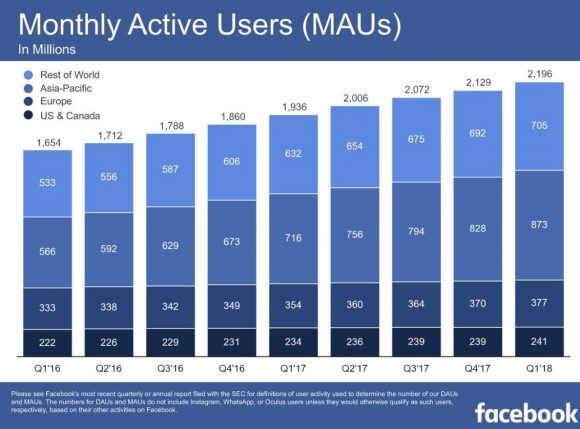

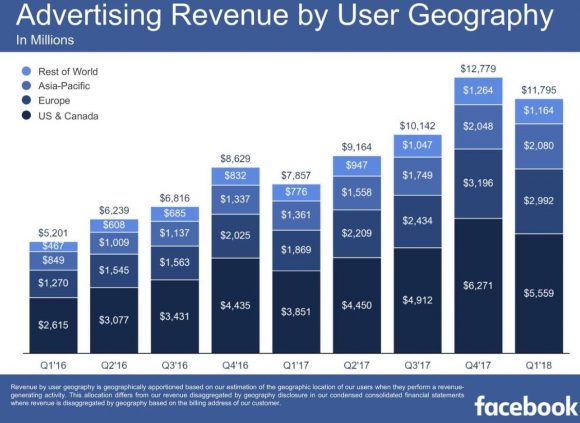

The Cambridge Analytica scandal threatened to tear apart the quarterly numbers and place Facebook in the tech doghouse, but stabilization in Monthly Active Users (MAU) and bumper digital ad revenue growth was the perfect elixir to an eagerly anticipated earnings report.

Facebook showed resilience by growing (MAU) to 2.2 billion, up 13% at a time when attrition could have reared its ugly head.

The market breathed a huge sigh of relief as the Facebook beat came to light.

The battering that Facebook received in the press effectively lowered the bar and Facebook delivered in spades.

The unfaltering migration to mobile continues throughout the industry with mobile digital ad revenue making up 91% of ad revenue, which is a nice bump from the 85% last quarter.

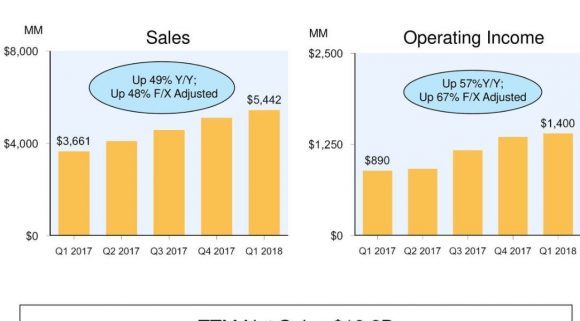

Overall, Facebook grew revenues 49% YOY to $11.97 billion.

There is no getting around that Facebook is a highly profitable business due to the lack of costs. I should be so lucky.

Remember at Facebook, the user is the product.

Instead of paying for rising TAC (Traffic Acquisition Costs) as does Google (GOOGL) or the $8 billion outlay for Netflix's (NFLX) annual content budget, Facebook pours its money into improving its digital platform and advancing its ad tech capabilities.

However, moving forward, Facebook will have to cope with extra regulatory costs.

Facebook recently hired a legion of content supervisors at minimum wage to root out the toxic content roaming around on its platform.

Site operators have doubled to 14,000. This number gives you a taste why the large cap tech names are best positioned to combat the new era of regulation.

Doubling the staff of any business would be a tough cost pill to swallow.

Many companies would go under, but Facebook has the cash to mitigate the additional cost of doing business.

This defensive initiative casts Facebook in a better light than before like a superhero rooting out the evil villain.

Facebook and its co-founder Mark Zuckerberg need to hire a better public relations team to ensure that Mark Zuckerberg isn't pigeonholed in mainstream media as the monster of tech.

The Amazon-effect is infiltrating every possible industry, and even the bigger tech names are coping with the Amazon (AMZN) spillage onto competitors' turf.

A risk down the line is Amazon's booming digital ad business nibbling away at Facebook's own digital ad model.

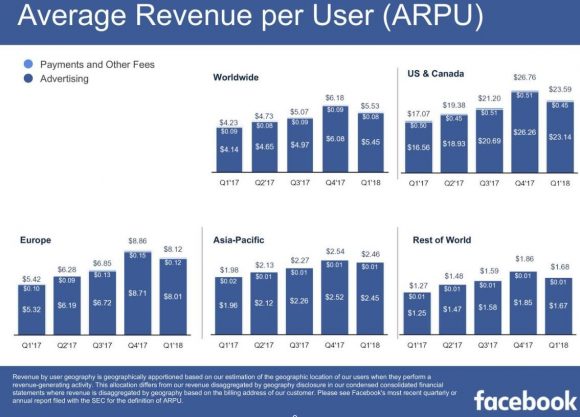

ARPU (Average Revenue Per User) remains robust with Facebook earning $23.59 per North American user, which is the most lucrative geographic location.

Artificial Intelligence (A.I.) is a tool that Facebook has implemented into its platform and monitoring apparatus.

Removing damaging content preemptively is the order of the day instead of being blamed for harboring nefarious content.

One example of this use case has been targeting ISIS- and Al Qaeda-related terror content with 99% of inappropriate content removed before being flagged by a human.

Heavy investments in A.I. will make Facebook a safer place to share content.

Big events exemplify the strength of Facebook.

During the Super Bowl in February, around 95% of national TV advertisers were simultaneously posting ads on Facebook because of the viral effect commercials and posts have during massive events.

Tourism Australia is another firm that bought ads on Instagram and Facebook platforms during the Super Bowl.

The campaign was hugely successful with half the leads for Tourism Australia coming directly from Facebook.

Facebook acts as the go-to provider for quality digital marketing and this will not change for the foreseeable future.

Investors can feel comfortable that there was no advertiser revolt after the big data chaos.

Facebook is improving its ad tech, and new ad products will be introduced to the 2.2 billion MAUs.

For instance, Facebook developed a carousel of rotating ads on Instagram Stories, and advertisers will be able to share up to three video or photos now instead of one. If the user swipes up, the swipe will take them directly to the advertisers' websites.

The shopping experience is more personalized now with an updated news feed that will show a full-screen catalog to help the user find whatever is in their search.

Facebook will only get better at placing suitable ads that mesh with the users' interests or hobbies.

Investors must be cautious to not let macro-headwinds sabotage existing positions.

Facebook's underlying growth drivers remain intact, but the stock is vulnerable to regulation headline risk that caps its short-term upside.

There is also the possibility that another Cambridge Analytica is just around the corner, which would result in a swift 10% correction.

Next earnings report should be interesting because it will reflect the first quarter that Facebook has operated with higher security expenses and will go a long way to validating its business model in a new era of rigid regulation.

If Facebook does not fill in the moat around the business, then Facebook is braced to grow top and bottom line with minimal resistance.

The cherry on top was the additional $9 billion of buybacks giving the stock price further support.

Facebook is a long-term hold but a risky short-term trade.

_________________________________________________________________________________________________

Quote of the Day

"Never trust a computer you can't throw out a window." - said Apple cofounder Steve Wozniak.

While the Global Trading Dispatch focuses on investment over a one week to six-month time frame, Mad Options Trader, provided by Matt Buckley, will focus primarily on the weekly US equity options expirations, with the goal of making profits at all times. Read more

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

May 1, 2018

Fiat Lux

Featured Trade:

(FRIDAY, JUNE 15, 2018, DENVER, CO, GLOBAL STRATEGY LUNCHEON)

(ANATOMY OF A GREAT TRADE)

(TLT), (TBT), (SPY), (GLD), (USO),

(CYBERSECURITY IS ONLY JUST GETTING STARTED),

(PANW), (HACK), (FEYE), (CSCO), (FTNT), (JNPR), (CIBR)

So, I'm sitting here agonizing over whether I should sell short the US Treasury bond market (TLT) once again.

Thanks to the bombshell Israel announced today alleging the existence of a secret Iranian nuclear missile program, oil has rallied by 2%, the US dollar has soared, and stocks have been crushed.

The (TLT) has popped smartly, some $2.5 points off of last week's low, taking yields down from a four-year high at 3.03% down to 2.93%.

The report is probably based on false intelligence, which is becoming a regular thing in the Middle East. Suffice it to say that the presenter, Prime Minister Benjamin "Bibi" Netanyahu, may soon be indicted on corruption charges. Clearly, they are going "American" in the Holy Land.

But for today, the market believes it.

You can understand me chomping at the bit, as selling short US government bonds has been my new rich uncle since the market last peaked in July 2017.

I just ran my Trade Alert history over the past nine months and here is what I found.

I sent you 38 Trade Alerts to sell short bonds generating 18 round trips, AND EVERY SINGLE ONE WAS PROFITABLE! In total these Alerts generated a trading profit of 216%, or 21.62% of my total portfolio return.

That means 35% of my profits over the past year came from selling short Treasuries.

You should do the same.

Falling Treasury prices have been one of the few sustainable trends in financial markets during the past year.

Stock rallied, then gave up a chunk. Gold (GLD) has gone nowhere. Only oil has surpassed as a sustainable trade, thanks to successful OPEC production quotas, which have been extended multiple times.

Texas tea is up an admirable 67% since the June $42 low. And who was loading up on crude way down there?

Absolutely no one.

Of course, I have an unfair advantage as a bond trader, as I have been doing this for nearly 50 years.

I caught the big inflation driven fixed income collapse during the 1970s, which had a major assist then from a rapidly devaluing US dollar.

That's when they brought out zero-coupon bonds, effectively increasing our leverage by 500% for virtually no cost. Principal only strips followed, another license to bring money on the short side.

The big lesson from trading this market for a half century is that trends last for a really long time. The bull market in bonds that started in 1982, when 10-year yields hit 14%, lasted for 33 years.

As we are less than three years into the current bear market the opportunities are rife. We are very early into the new game. This one could last for the rest of my life.

The reasons are quite simple. The fundamentals demand it.

1) The Global Synchronized Recovery is accelerating.

2) The Fed will start dropping on the bond market in the very near future $6 billion a month, or $200 million a day, worth of paper in its QE unwind.

3) Tax cuts will provide further stimulus for the US economy.

4) With the foreign exchange markets now laser-focused on America's exploding deficits, a weak US dollar has triggered a capital flight out of the US.

5) We also now have evidence that China has started to dump its massive $1 trillion in US Treasury bond holdings.

All are HUGELY bond negative.

All of this should take bonds down to new 2018 lows. What we could be seeing here is the setting up for the perfect head and shoulders top of the (TLT) for 2018.

As for that next Trade Alert, I think I'll hold out for a better price to sell again. What's the point in spoiling a perforce record?

Time to Stick to Your Guns

Mad Hedge Technology Letter

May 1, 2018

Fiat Lux

Featured Trade:

(AMAZON KILLS IT AGAIN),

(AMZN), (WMT), (FB), (TGT), (GOOGL)

Jeff Bezos is a god.

Well, not quite but he is turning into one after Amazon delivered a mythical earnings report that left Amazon haters in awe.

The Amazon bears patiently waiting for the day of reckoning will have to wait longer as Amazon smashed earnings expectations by a magnitude of two or three.

Amazon had a lot riding on the most recent earnings report after racing to new highs in mid-March.

The brief macro-correction then gave investors yet another entry point into one of the best companies of our generation that is still up more than 30% this year.

Amazon Web Services (AWS) revenue reaccelerated from its 42% growth last year to a high octane 49% YOY and made up a disproportionate 73% of Amazon's operating income.

Amazon is heavily reliant on the AWS segment to carry it through feast or famine.

According to Jeff Bezos, its critically acclaimed cloud segments' outstanding results originate from the "seven-year head start before like-minded competition."

This reaffirms the benefit of first-mover advantage with which large cap tech is obsessed.

There is room for other companies in the cloud space, with the cloud industry expanding 20% in 2018 to $186 billion.

Therefore, expanding by 20% is the bare bones minimum to be considered relevant.

Amazon has positioned itself to funnel in the most dollars that migrate toward the cloud as the industries pioneer and best of breed.

After the latest earnings report, Amazon is in pole position to become the first publicly traded $1 trillion company.

This latest quarter wrapped up its 62nd consecutive quarter of 20% plus growth.

And the commentary coming out of the earnings reports makes it almost certain that Amazon will capture more market share.

There were a few bombshells dropped that were unequivocal positives for investors.

First, Amazon has become the third player in digital ad industry with the duopoly of Google search and Facebook.

Amazon revved up its digital ad revenue by 139% QOQ to a substantial $2.03 billion per quarter business.

This business is particularly appetizing because of its high margins and will help alleviate tight margins on the e-commerce side.

Amazon's digital ad business is by far the fastest growth lever in its portfolio. It will ramp up this side of the business whose main function is to match consumers with suitable products that consumers otherwise would miss out on in a standard Amazon search.

The extraordinary numbers support the notion that the hoopla of Washington regulation is all bark and no bite.

Facebook also delivered a prodigious quarter for the ages amid testimony and public backlash that resulted in immaterial damage to top- and bottom-line numbers.

The second bombshell announced was the change in pricing to prime members. Amazon upped its annual prime membership to $119 from $99.

This additional $20 price hike, or 20% on 100 million prime members, will swell revenue by an extra $2 billion of incremental revenue.

In total, Amazon will accrue a bonus of 4% of revenue by this price change.

Amazon has a high fixed-cost business, and slightly tweaking prices will create a huge windfall with the revenue almost entirely flowing down to the bottom line in the form of pure profit.

Many industry analysts claim that Amazon has the best management team in the industry and explicate this company as an "Internet staple."

More than 100 million products are delivered with free shipping for Amazon prime customers. This is starkly higher than the 20 million products shipped for free in 2014.

Amazon does everything in its power to offer a unique and efficient experience for customers.

The customer satisfaction reveals itself by the rock-bottom churn rate.

Amazon prime at an annual cost of $119 is such a value that no analysts even dared to ask Amazon CFO Brian Olsavsky if consumers would take issue with the rise in price.

Investors and strangers alike assume that broad-based reoccurring revenue from annual prime membership is a given.

In an era of mass-scrutinization, Amazon's earnings call seemed like a celebration of the mythical achievements that are changing consumer behavior by the day.

The lack of inquiry was justifiable this time because the one major shortcoming suddenly remedied itself.

Amazon's doubters frequently attack the lack of margin growth because its business model is first and foremost a land grab for market share ignoring any remnants of margin stability.

Now that Amazon's digital ad business has sprouted up, the margin story, starting from a miniscule base, will go from weakness to an unrelenting success.

Amazon started with its ultra-thin margin e-commerce business that made an operating loss of $160 billion in 2017.

Cranking up a shiny, high margin business will be hard for the other FANGs to compete with as they gyrate toward other businesses that have lower margins than Amazon's digital ad segment.

This is a horrible time to start fighting Amazon in price wars as the paradigm shift to quantitative tightening has made the cost of capital demonstrably pricier.

Operating margins almost doubled from 2% to 3.8% on $51 billion of quarterly sales.

This is a huge deal.

Amazon has been continuously harangued for "not making money." Well, that era is over.

Profits, and not only revenue, will start accelerating and Amazon will become the closest thing to a perfect company.

The years and years of plowing cheap capital back into fulfillment center and e-commerce activity gave Amazon a stained reputation for years.

However, as Amazon turns the screws and uses its foundational leverage to capture additional profits, the other FANGs will be forced down the same path ruining operating margins for the other big players.

Amazon telegraphed its quest for market share strategy to investors years ago, and investors understand they are paying for growth and growth only.

That will change now that profits have become a real part of its arsenal.

There is no doubt that Amazon will deploy its profits back into expanding its company because Jeff Bezos knows that if he can grow Amazon's top-line number, investors will follow suit.

Also, spending means improving the products, and Amazon has never hesitated to spend big.

The move into digital ad growth is a warning shot to Facebook and Google. Amazon will mobilize its workforce to take on other business, and anything that is high margin is fair game.

The future looks bleak for retail competitors Walmart and Target, as the contents of the earnings report reaffirms Amazon's unrelenting assault on the retail sector, which is systematically being dissected by Amazon for fun.

Google search and Facebook are in Amazon's crosshairs. Staving off this monster will be hard to do in the long run.

Amazon has a clear path to further market gains, and operating margins are almost at a tipping point.

Revenue is poised to re-accelerate because of the reignition of AWS to a higher growth trajectory.

Shoring up operating margins through a burgeoning digital ad division will only be a boon to earnings in the future.

Amazon is one of the best companies in the world, and any weakness in the stock should be bought and held forever.

_________________________________________________________________________________________________

Quote of the Day

"I do not fear computers. I fear a lack of them," - said writer Isaac Asimov.