While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to the six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

April 26, 2019

Fiat Lux

Featured Trade:

(HOW TO RELIABLY PICK A WINNING OPTIONS TRADE)

Mad Hedge Hot Tips

April 25, 2019

Fiat Lux

The Five Most Important Things That Happened Today

(and what to do about them)

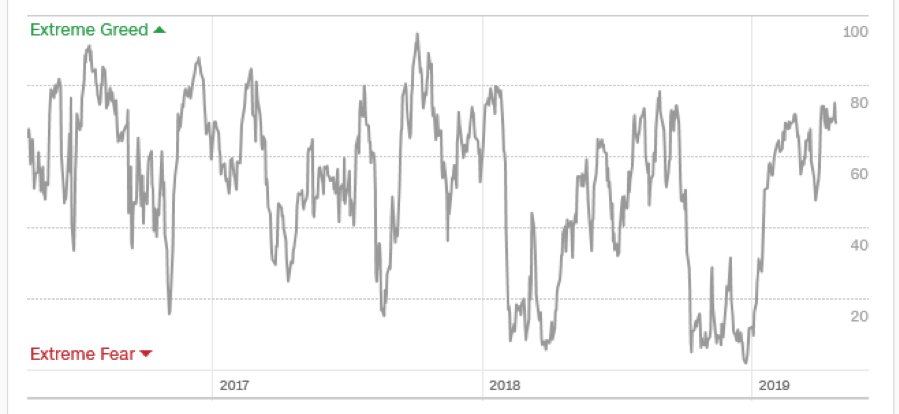

1) Risk in the Market is Rising. Look at the big overreaction to weak 3M earnings this morning. With the Mad Hedge Market Timing Index at 69, there is only a 31% chance that your next “BUY” will make money. Click here.

2) Tesla Loses $700 million in Q1, but the stock rallies anyway. It’s tough to press the world’s most heavily shorted stock down here. It’s all because the EV subsidy dropped by half since January. Look for a profit rebound in quarters two and three. Capital raise anyone? Tesla junk bonds now yielding 8.51% if you’re looking for an income play. Click here.

3) Microsoft Knocks it Out of the Park, with great earnings and a massive 47% increase in cloud growth. Stock looks hell-bent to hit $140, and Mad Hedge followers who bought the stock are making a killing. (MSFT) is now the third company to join the $1 trillion club. Click here.

4) All Eyes on Amazon which reports after the close. Will they pop 5% like the other FANGs? Or will the focus be on the divorce? Click here.

5) Chipotle Gets Hammered. Earnings were good, but they disclosed the existence of a criminal investigation stemming from a few unfortunate burritos last year. This business never gets old. Click here.

Published today in the Mad Hedge Global Trading Dispatch and Mad Hedge Technology Letter:

(2019 MAD HEDGE WORLD TOUR)

(THE REAL ESTATE MARKET IN 2030)

(XHB)

(THE RESILIENCE OF TWITTER)

(TWTR), (FB)

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Mad Hedge Technology Letter

April 25, 2019

Fiat Lux

Featured Trade:

(THE RESILIENCE OF TWITTER)

(TWTR), (FB)