My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its "Big Mac" index of international currency valuations.

Although initially launched as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

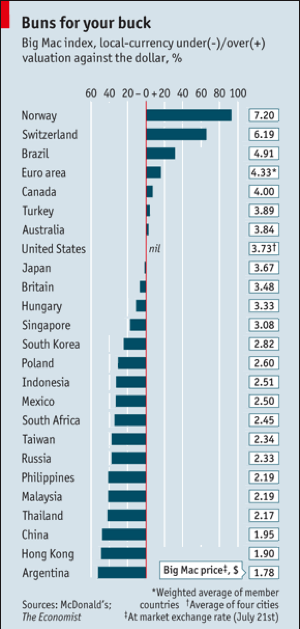

The index counts the cost of McDonald's (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai baht are cheap.

I couldn't agree more with many of these conclusions. It's as if the august weekly publication was tapping The Diary of a Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool than a speedy lunch.

The Big Mac in Yen is Definitely Not a Buy

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-07-05 02:04:412019-08-05 17:45:40Where The Economist "Big Mac" Index Finds Currency Value

For many, one of the most surprising impacts of the administration’s tariffs on Chinese imports announced today has been a rocketing bond market.

Since the December $116 low, the iShares 20+ Year Treasury Bond ETF (TLT) has jumped by a staggering $16 points, the largest move up so far in years.

The tariffs are a highly regressive tax that will hit consumers hard in the pocketbook, thus reducing their purchasing power.

It will dramatically slow US economic growth. If the trade war escalates, and it almost certainly will, it could shrink US GDP by as much as 1% a year. A weaker economy means less demand for money, lower interest rates, and higher bond prices.

There is no political view here. This is just basic economics.

And while there has been a lot of hand-wringing over the prospect of China dumping its $1.1 trillion in American bond holdings, it is unlikely to take action here.

The Beijing government isn’t going to do anything to damage the value of its own investments. The only time it actually does sell US bonds is to support its own currency, the renminbi, in the foreign exchange markets.

What it CAN do is to boycott new Treasury bond purchases, which it already has been doing for the past year.

The tariffs also raise a lot of uncertainty about the future of business in the United States. Companies are definitely not going to increase capital spending if they believe a depression is coming, which the last serious trade war during the 1930s greatly exacerbated.

While stocks despise uncertainty, bonds absolutely love it.

Those of you who are short the bond market through the ProShares Ultra Short 20+ Year Treasury ETF (TBT) have a particular problem that is often ignored.

The cost of carry of this fund is now more than 5% (two times the 2.10% coupon plus management fees and expenses). Thus, long-term holders have to see interest rates rise by more than 5% a year just to break even. The (TBT) can be a great trade, but a money-losing investment.

The Chinese, which have been studying the American economic and political systems very carefully for decades, will be particularly clever in its retaliation. And you thought all those Chinese tourists were over here just to buy our Levi’s?

It will target Republican districts with a laser focus, and those in particular who supported Donald Trump. It wants to make its measures especially hurt for those who started this trade war in the first place.

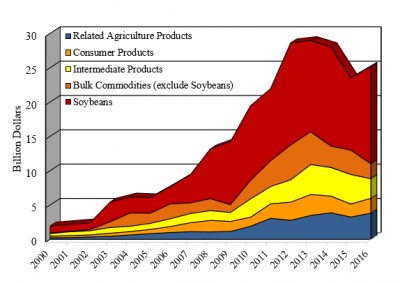

First on the chopping block: soybeans, which are almost entirely produced in red states. In 2016, the last full year for which data is available, the US sold $15 billion worth of soybeans to China. Which are the largest soybean producing states? Iowa followed by Minnesota.

A major American export is aircraft, some $131 billion in 2017, and China is overwhelmingly the largest buyer. The Middle Kingdom needs to purchase 1,000 aircraft over the next 10 years to accommodate its burgeoning middle class. It will be easy to shift some of these orders to Europe’s Airbus Industries.

This is why the shares of Boeing (BA) have been slaughtered recently, down some 13.5% from the top. While Boeing planes are assembled in Washington state, they draw on parts suppliers in all 50 states.

Guess what the biggest selling foreign car in China is? The General Motors (GM) Buick which saw more than 400,000 in sales last year. I have to tell you that it is hilarious to see my mom’s car driven up to the Great Wall of China. Where are these cars assembled? Michigan and China.

The global trading system is an intricate, finally balanced system that has taken hundreds of years to evolve. Take out one small piece, and the entire structure falls down upon your head.

This is something the administration is about to find out.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/03/China-chart-photo-2.jpg282400MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-07-05 02:02:302019-08-05 17:45:34Why US Bonds Love Chinese Tariffs

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-03 09:18:452019-07-03 09:18:45July 3, 2019 - MDT Pro Tips A.M.

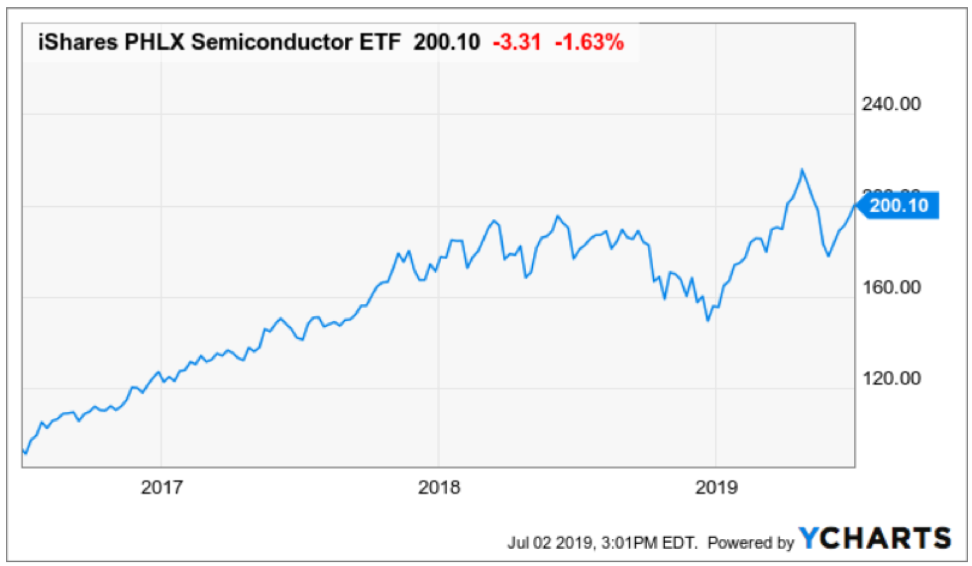

The overwhelming victors of the G20 were the semiconductor companies who have been lumped into the middle of the U.S. and China trade war.

Nothing substantial was agreed at the Osaka event except a small wrinkle allowing American companies to sell certain chips to Huawei on a limited basis for the time being.

As expected, these few words set off an avalanche of risk on sentiment in the broader market along with allowing chip companies to get rid of built-up inventory as the red sea parted.

Tech companies that apply chip stocks to products involved with value added China sales were also rewarded handsomely.

Apple (AAPL) rose almost 4% on this news and many investors believe the market cannot sustain this rally unless Apple isn’t taken along for the ride.

Stepping back and looking at the bigger picture is needed to digest this one-off event.

On one hand, Huawei sales comprise a massive portion of sales, even up to 50% in Nvidia’s case, but on the other hand, it is the heart and soul of China Inc. hellbent on developing One Belt One Road (OBOR) which is its political and economic vehicle to dominate foreign technology using Huawei, infrastructure markets, and foreign sales of its manufactured products.

Ironically enough, Huawei was created because of exactly that – national security.

China anointed it part of the national security apparatus critical to the health and economy of the Chinese communist party and showered it with generous loans starting from the 1980s.

China still needs about 10 years to figure out how to make better chips than the Americans and if this happens, American chip sales will dry up like a puddle in the Saharan desert.

Considering the background of this complicated issue, American chip companies risk being nationalized because they are following the Chinese communist route of applying the national security tag on this vital sector.

Huawei is effectively dumping products on other markets because private companies cannot compete on any price points against entire states.

This was how Huawei scored their first major tech infrastructure contract in Sweden in 2009 even though Sweden has Ericsson in their backyard.

We were all naïve then, to say the least.

Huawei can afford to take the long view with an Amazon-like market share grab strategy because of possessing the largest population in the world, the biggest market, and backed by the state.

Even more tactically critical is this new development crushes the effectiveness of passive investing.

Before the trade war commenced, the low-hanging fruit were the FANGs.

Buying Google, Amazon, Apple, Netflix, and Facebook were great trades until they weren’t.

Things are different now.

Riding on the coattails of an economic recovery from the 2008 housing crisis, this group of companies could do no wrong with our own economy flooded with cheap money from the Fed.

Well, not anymore.

We are entering into a phase where active investors have tremendous opportunities to exploit market inefficiencies.

Get this correct and the world is your oyster.

Get this wrong, like celebrity investors such as John Paulson, who called the 2008 housing crisis, then your hedge fund will convert to a family office and squeeze out the extra profit through safe fixed income bets.

This is another way to say being put out to pasture in the financial world.

My point being, big cap tech isn’t going up in a straight line anymore.

Investors will need to be more tactically cautious shifting between names that are bullish in the period of time they can be bullish while escaping dreadful selloffs that are pertinent in this stage of the late cycle.

In short, as the trade winds blow each way, strategies must pivot on a dime.

Geopolitical events prompted market participants to buy semis on the dips until something materially changes.

This is the trade today but might be gone with one Tweet.

If you want to reduce your beta, then buy the semiconductor chip iShares PHLX Semiconductor ETF (SOXX).

I will double down in saying that no American chip company will ever commit one more incremental cent of capital in mainland China.

That ship has sailed, and the transition will whipsaw markets because of the uncertainty in earnings.

The rerouting of capital expenditure to lesser-known Asian countries will deliver control of business models back to the corporation’s management and that is how free market capitalism likes it.

Furthermore, the lifting of the ban does not include all components, and this could be a maneuver to deliver more face-saving window-dressing for Chairman Xi.

In reality, there is still an effective ban because technically all chip components could be regarded as connected to the national security interests of the U.S.

Bullish traders are chomping at the bit to see how these narrow exemptions on non-sensitive technologies will lead to a greater rapprochement that could include the removal of all new tariffs imposed since last summer.

The risk that more tariffs are levied is also high as well.

I put the odds of removing tariffs at 30% and I wouldn’t be surprised if the administration doubles down on China to claim a foreign policy victory leading up to the 2020 election which could be the catalyst to more tariffs.

It’s difficult to decode if U.S. President Trump’s statements carry any real weight in real time.

The bottom line is the American government now controls the mechanism to when, how, and the volume of chip sales to Huawei and that is a dangerous game for investors to play if you plan on owning chip stocks that sell to Huawei.

Artificial intelligence or 5G applications chips are the most waterlogged and aren’t and will never be on the table for export.

This means that a variety of companies pulled into the dragnet zone are Intel (INTC), Nvidia (NVDA), and Analog Devices (ADI) as companies that will be deemed vital to national security.

These companies all performed admirably in the market following the news, but that could be short lived.

Other major logjams include Broadcom’s future revenue which is in jeopardy because of a heavy reliance on Huawei as a dominant customer for its networking and storage products.

Rounding out the chip sector, other names with short-term bullish price action are Qualcomm (QCOM) up 2.3%, Texas Instruments (TXN) up 2.6%, and Advanced Micro Devices (AMD) up 3.9%.

(AMD) is a stock I told attendees at the Mad Hedge Lake Tahoe conference to buy at $18 and is now above $31.

Xilinix (XLNX) is another integral 5G company in the mix that has their fortunes tied to this Huawei mess.

Investors must take advantage of this short-term détente with a risk on, buy the dip trade in the semi space and be ready to rip the cord on the first scent of blood.

That is the market we have right now.

If you can’t handle this environment when there is blood in the streets, then stay on the sidelines until there is another market sweet spot.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/chip-stocks.png564972Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-03 03:02:302019-08-05 17:49:59Chips are Back from the Dead

“Google is all about information. So the notion of using and presenting information in the right point at the right time to users is what, in essence, describes Google.” – Said Current CEO of Google Sundar Pichai

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/sundar.png325249Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-03 03:00:312019-08-05 17:49:51July 3, 2019 - Quote of the Day

Come join me for lunch at the Mad Hedge Fund Trader’s Global Strategy Luncheon which I will be conducting in Budapest, Hungary on Wednesday, July 10, 2019 at 12:30 PM.

An excellent meal will be followed by a wide-ranging discussion and a question-and-answer period. I’ll be giving you my up to date view on stocks, bonds, currencies, commodities, precious metals, energy, and real estate.

I also hope to provide some insight into America’s opaque and confusing political system. And to keep you in suspense, I’ll be throwing a few surprises out there too.

Tickets are available for $240.

The lunch will be held at an exclusive hotel on the Buda side of the Danube near the St Matthias church, the location of which will be emailed with your purchase confirmation.

I look forward to meeting you and thank you for supporting my research. To purchase tickets for this luncheon, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/05/budapest.png308462Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-03 01:04:362019-07-08 09:44:01SOLD OUT - Wednesday, July 10 Budapest, Hungary Global Strategy Luncheon

Hang around any professional options trading desk and it will only be seconds before you hear the terms Delta, Theta, Gamma, or Vega. No, they are not reminiscing about their good old fraternity or sorority days (Go Delta Sigma Phi!).

These are all symbols for mathematical explanations of how options prices behave when something changes. They provide additional tools for understanding the price action of options and can greatly enhance your own trading performance.

Bottom line: they are all additional ways to make money trading options.

The best part about the Greeks is that they are all displayed on your online options trading platform FOR FREE! So, if you can read a number off a screen, you gain several new advantages in the options trading world. That’s not a lot to ask.

Delta

The simplest and most basic Greek symbol to comprehend is the Delta. An option delta is a prediction of how much the option price will change relative to a change in the underlying security.

Here, it is easiest to teach by example. Let’s go back to our (AAPL) June 17, 2016 $110 strike call option. Let’s assume that (AAPL) shares are trading at $110, and our call option is worth $2.00.

If (APPL) share rise $1 from $110 to $111, the call options will rise by 50 cents to $2.50. This is because an at-the-money call option has a delta of +0.50, or +50%. In other words, the (AAPL) call options will rise by 50%, or half of the amount of the (AAPL) shares.

Let’s say you bought (AAPL) shares because you expect them to rise 10% going into the next big earnings announcement. How much will the above-mentioned call options rise?

That’s easy. A call option with a delta of 50% will rise by half the amount of the shares. So, if (AAPL) shares rise by 10% from $110 to $121, the call options will appreciate by half this dollar about or by $5.50. This means that the call options should jump from in price from $2.00 to $7.50, a gain of 375%.

By the way, did I mention that I love trading options?

Now let’s look at the Put option side of the equation. Let's assume that Apple is about to disappoint terribly in their next earnings report, and that the stock is about to FALL 10%.

We want to buy the (AAPL) June 17, 2016 $110 strike put option which will profit when to stock falls. Remember, put options are always more expensive than call options because investors are always willing to pay a premium for downside protection. So, our put options here should cost about $4.00.

If we’re right and Apple shares tank 10%, from $110 to $99, how much will the put options increase in value?

We use the same arithmetic as with the call options. An at-the-money put options also has a delta of 0.50, or 50%. So, the put options will capture half the downside move of the stock, or $5.50. Add this to our $4.00 cost, and our put option should now be worth $9.50, a gain of 237.5%.

Did I happen to tell you that I love trading options?

Let’s consider one more example, the short position. Let’s assume that Apple shares are going to fall, but we don’t know by how much, or how soon.

It that case, you are better off selling short a call option than buying a put option. That way, if the stock only falls by a small amount, or goes nowhere, you can still make a profit.

When you sell short an option, your broker PAYS you the premium which sits in your account until you close the position.

Short positions in options always have negative deltas. So, a short position in the (AAPL) June 17, 2016 $110 strike call option will have a delta of -50%.

Let’s say you sold short the (AAPL) calls for $2.00 and Apple shares fell by 10%. What does the short position in the call option do? Since it has a delta of -50%, it will drop by half, from $2.00 to $1.00 and you will make a profit of $1.00.

Here is the beauty of short positions options. Let’s assume that (AAPL) stock doesn’t move at all. It just sits there at $110 right through the options expiration date of June 17, 2016.

Then the value of the call option you sold at $2.00 goes to zero. Your broker closes out the expired position from your account and frees up you margin requirement.

(AAPL) June 17, 2016 $110 strike call option

-50% delta X $11 stock decline means the options drops by half, or from $2.00 to $1.00

Sounds pretty good, doesn’t it? In fact, the numbers are so attractive that a large proportion of professional traders only engage in selling short options to earn a living.

To accomplish this, they usually have mainframe computers, highly skilled programmers, and teams of mathematicians backing them up which cost tens of millions of dollars a year.

However there is a catch.

When you sell short a call option, you are taking on UNLIMITED RISK. The position is said to be naked, or unhedged. Let’s say you sell short the (AAPL) June 17, 2016 $110 strike call option, and (AAPL) shares, instead of falling, RISE from $110 to $200, a gain of $90.

Then the value of your short position soars from $2.00 to $45.00. You will get wiped out. It gets worse. The delta on this option is only 50% for the immediate move above $110. The higher the stock rise, the faster your delta increases until it eventually reaches 100%. You now have a loss that increases exponentially!

This is why many hedge fund managers refer to naked option shorting as the “picking up the pennies in front of the steamroller” strategy.

For this reason, brokers either demand extremely high margin requirement for these “naked” or unhedged short positions, or they won’t let you do them at all.

If you dig down behind many of the extravagant performance claims of other options trading services, they are almost always reliant on the naked shorting of options. They all blow up. It is just a matter of when.

For that reason, we here at the Mad Hedge Fund Trader NEVER recommend the naked shorting of put or call options, no matter what the circumstances.

We want to keep you as a happy, money-making customer for the long term. If you succumb to temptation and engage in naked shorting of options, you will be separated from your money in fairly short order.

(AAPL) June 17, 2016 $110 strike call option

(AAPL) shares rise from $110 to $200

$2.00 short sale proceeds + $90 - $88.00

a loss of 4,400%!!

Theta

All options have time value. This is why an option with a one-year expiration date cost far more than one with a one-week expiration date. The theta is the measurement of how much premium you lose in a day. This is what options traders like me refer to as time decay.

The theta on an option changes every day. For example, an option with a year until expiration has a theta that is miniscule. An option that has a single day until expiration is close to 100% since it will lose its entire value within 24 hours if it is out of the money. The closer we get to expiration; the faster theta accelerates. As mathematicians say, it is not a straight-line move.

This is why you never want to hold a long option position going into expiration. The value of this option will vaporize by the day. Unless the stock goes your way very quickly, you will have a really tough time making money.

If you are short an option, this is when you can earn your greatest profits. But you only want to consider a short option position when you have an offsetting hedge against it. That will minimize and define your risk, limit your margin requirement, and keep you from blowing up and going to the poor house. We’ll talk more about that later.

I could go into how you calculate your own thetas, but that would be boring. Suffice it to say that you can read it right off the screen for you online trading platform.

Implied Volatility

While we’re here meeting the Greeks, there is one more concept that I want to get across to make your life as an option trader easier.

You have probably heard the term implied volatility. But to understand what this is, let me give you a little background.

Back in the 1970s, a couple of mathematicians developed a model for pricing options. Their names were Fisher Black and Myron Scholes and they received the Nobel prize for their work. Their equation became known as the Black Scholes Equation.

The Black Scholes equations predicts how much an option should be worth based on the historic volatility of the underlying securities, the current level of interest rates, and a few other factors.

When options trade over their Black Scholes value, they are said to have a high implied volatility. When they trade at a discount, they have a low implied volatility.

Let’s say that a piece of news comes out that a company is going to be taken over. The shares will rocket, and so will the implied volatility of the options.

If you pay a very high implied volatility for a call option, the chances of you making money decline and you are taking on more risk. If you pay too much, you could even see a situation where the stock rises, but the call option doesn’t rise, or even falls.

On the other hand, let’s say you buy a call option that is trading at a big discount to its theoretical implied volatility. You usually find this when a stock has shown little movement over a long period of time.

Chances are that you will get a good return on this low risk position, especially if you pick it up just before a major news event that you have correctly predicted.

At the end of the day, you should attempt to do with implied volatilities what you do with stocks and their options, buy low and sell high.

The Minors

There are a few other Greek letters you may hear about in the options market or find on your screen. For the most part, these are unnecessary most basic options strategies, gamma is well above your pay grade.

Gamma is the name of the most powerful type of radiation emitted when an atomic bomb goes off. It is always fatal. But we won’t talk about that here.

In the options world, gamma is the amount that the delta changes generated by a $1 move in the underlying stock price.

You may hear news reports of funds gamma hedging their portfolio during times of extreme market volatility. This occurs when managers want to reduce the volatility of their portfolios relative to the market.

Vega is another Greek term you’ll find on your screen. All options have a measurement called implied volatility or “vol” which indicated how much the option should move relative to a move in the underlying stock.

Vega is the measurement of the change in that option volatility. When a stock has volatility that is changing rapidly, vega will be high. When a stock is boring, vega will be low.

Finally, for the sake of completeness, I’ll mention rho. Rho is the amount that the price of an option will change compared to a change in the risk-free interest rate, i.e. the interest rate of US Treasury bills.

Back in the 1980s, rho was a big deal because interest rates were very high, with Fed funds rates as high as 13%. Since interest rates have been close to zero for the past eight years, rho has been pretty much useless. The only reason you would want to mention rho today is if you were writing a book about options trading.

With that, you should be fairly fluent in the Greeks, at least in regards to trading options. Just don’t expect this to get you anywhere if you ever plan to take a vacation to Greece.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/black-scholes.png522750Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-03 01:02:222019-08-05 17:45:28Meet the Greeks

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.