Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(WHY YOU CANNOT NEGLECT THE CLOUD)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(WHY YOU CANNOT NEGLECT THE CLOUD)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Global Market Comments

December 27, 2019

Fiat Lux

SPECIAL ISSUE ABOUT THE FAR FUTURE

Featured Trade:

(PEAKING INTO THE FUTURE WITH RAY KURZWEIL),

(GOOG), (INTC), (AAPL), (TXN),

Cloud stocks should be at the vanguard of your tech portfolio, no ifs, ands, or buts.

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

Microsoft's (MSFT) pivot to its Azure enterprise business has sent its stock skyward, and it is poised to rake in more than $100 billion in cloud revenue over the next 10 years.

Microsoft's share of the cloud market rose from 10% to 15% and is rapidly zeroing in on Amazon Web Services (AWS).

Amazon leads the cloud industry it created which is partly why the first-mover advantage is so effective.

It still maintains more than 30% of the cloud market and Microsoft still needs to gain a lot of ground to even come close.

Amazon (AMZN) relies on AWS to underpin the rest of its businesses and that is why AWS contributes the lion’s share of Amazon's total operating income.

Cloud revenue is even starting to account for a noticeable share of Apple's (AAPL) earnings, which has previously bet the ranch on hardware products, most notably the iPhone and iPad.

The future is about the cloud.

These days, the average venture capitalist probably hears about the cloud 100 times a day.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations. Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest-growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to dramatic investment opportunities.

And that's where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside imposing data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even collaborate in real-time, making it the perfect force multiplier in our globalized world.

Once you start using the cloud to store a company's data, the benefits are countless.

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can divert resources on the core aspects of their business where they can increase value without worrying about managing IT staff of prima donnas.

Today's employees want to have a better work/life balance and this goal can be best achieved through telecommuting. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I shoot off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees while boosting performance.

According to a recent survey, 79% of respondents already work outside of their office some of the time, while another 60% would switch jobs if offered this flexibility.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way, a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document, so they can stay on top of real-time changes which can help businesses to better manage workflow regardless of geographical location.

Another important reason to move to the cloud is superior data security, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down operations for days.

The cloud simply routes traffic around disaster zones as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud to avoid such disruptions.

Even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

The cloud can slash expenses fast.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, resources that in turn can be used to expand the business. Setting up an in-house data center requires millions, and that's not to mention perpetual maintenance costs.

Creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

“Life is not fair; get used to it.” Said founder of Microsoft Bill Gates.

Mad Hedge Biotech & Healthcare Letter

December 26, 2019

Fiat Lux

Featured Trade:

(THE BOOM IN CANCER DRUGS),

(MRK), (CELG), (RHHBY), (BMY), (LLY), (NOVN)

Forecasting drug revenue can be a tricky business -- just ask the biotech leaders who overpromised but underdelivered.

These days, more and more variables are coming into play, with the US elections looming over us and the threat of generic meds overtaking market leaders becoming more tangible by the minute.

Another threat is the entry of biosimilars in the US, knocking down big-name drugs even in the most lucrative markets. Payers are also constantly seeking discounts, forcing tougher competition among crowded markets like diabetes and hepatitis.

However, the oncology sector remains a booming sector for the biotech industry.

Practically all major companies are either developing oncology treatments or already marketing these as blockbuster treatments, with 63 cancer drugs launched in just the past five years.

Unfortunately, not all cancer drugs are created equal. Looking at the spending on the treatments in recent years, it can clearly be seen that almost 80% of the money has been hogged by the industry leaders with the rest of the group lagging far behind.

To put things in perspective, bear in mind that the annual sales of the top 20 cancer drugs have reached over $50 billion, with $31 billion distributed among industry leaders Merck and Co (MRK), Celgene (CELG), and Roche Holdings (RHHBY).

These numbers hardly come as a surprise especially in light of over $133 billion recorded in spending for cancer treatments.

The top-selling oncology drug to date is multiple myeloma treatment Revlimid. Technically a Celgene product, the company’s $74 billion acquisition by Bristol-Myers Squibb (BMY) means the drug will be joining the other powerhouse offerings in the newly formed company’s lineup in the years to come.

With over a decade of dominance in the market and an impressive $9.7 billion in global sales annually, Revlimid has yet to hit its peak.

In fact, this mega-blockbuster is projected to exceed $15 billion in sales next year.

As if that wasn’t impressive enough, this oncology leader is estimated to bring more than double that amount come 2022.

Another dominant player in the oncology market is lung cancer drug Keytruda. Since its launch, this Merck immunotherapy leader has been able to usher in a boatload of cancer treatments using its core indications -- and it’s not yet done.

With an FDA approval eyed on June 29, 2020 for yet another indication for Keytruda, specifically for treating cutaneous squamous cell carcinoma (cSCC), its goal to dethrone Revlimid as the leader in this space now looks achievable.

Right now, Keytruda is used for various cancer types.

Aside from dominating the large addressable lung cancer market, it’s also used to treat head and neck cancer as well as melanoma. This makes Keytruda’s contributions indispensable to Merck’s overall top-line and continuous growth in sales in the past years.

Hence, it comes as no surprise that Merck’s recent third-quarter earnings had Keytruda is the starring role once again. Sales for this oncology drug jumped 62% year over year, reaching almost $3.1 billion.

One more dominant force in the oncology sector is Roche, with breast cancer drug Herceptin serving as the primary moneymaker of the company in the past 15 years.

With Herceptin raking in roughly $7 billion in annual sales in recent years, Roche has been proactive in securing its position in the oncology space by adding blockbusters ovarian cancer drug Avastin and leukemia medication Rituxan in the list.

For years, these three cancer drugs have formed the foundation of Roche’s continuous growth in the oncology sector. However, these treatments are now in danger of facing competition.

A particularly aggressive competitor is Pfizer (PFE), with its breast cancer drug Ibrance gaining traction as shown by its growing sales from $0.7 billion in 2015 to a promising $4.1 billion in 2018. Other competitors include Eli Lilly’s (LLY) Verzinio and Novartis’ (NOVN) Piqray.

To maintain its stronghold, Roche has been aggressive as well in developing new drugs.

Word has it that the company is expecting an addition $5 billion in sales for its new cancer treatments like breast cancer drugs Perjeta and Kadycla along with lung cancer medications Tecentriq and Alecensa.

Global Market Comments

December 26, 2019

Fiat Lux

Featured Trade:

(TRADING THE NEW APPLE IN 2020),

(AAPL),

(THE EIGHT WORST TRADES IN HISTORY),

(TESTIMONIAL)

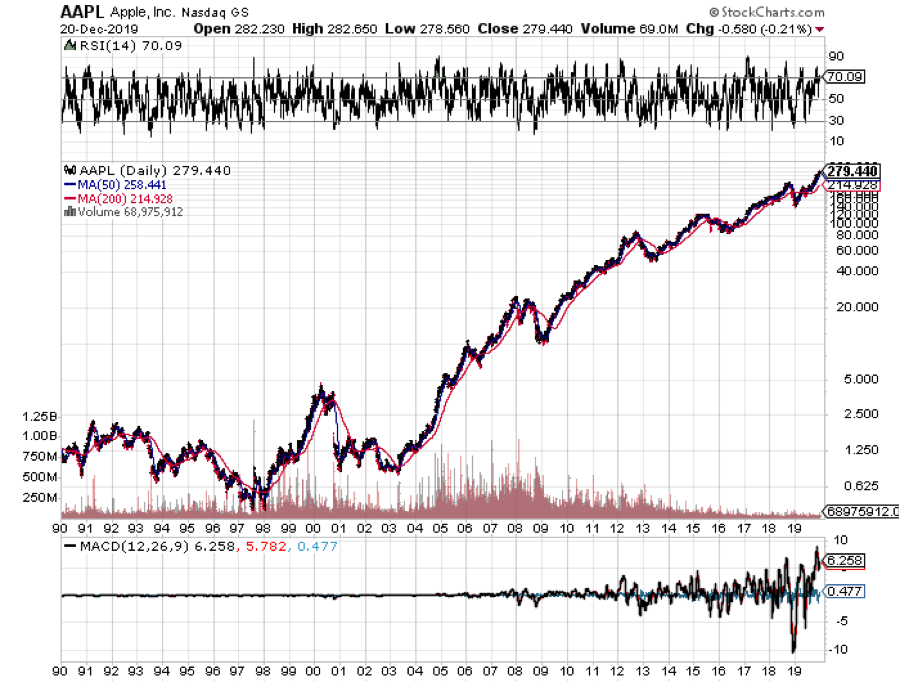

Not a day goes by when someone doesn’t ask me about what to do about Apple (AAPL).

After all, it is the world largest publicly-traded company at a $1.2 trillion market capitalization. It is the planet’s most widely owned stock. Almost everyone uses their products in some form or another. It buys back more of its own stock than any other company on the planet. Oh yes, it is also one of Warren Buffet’s favorite picks.

So, the widespread adulation is totally understandable.

Apple is a company with which I have a very long relationship. During the early 1980s, I was ordered by Morgan Stanley to take Steve Jobs around to the big New York Institutional Investors to pitch a secondary share offering for the sole reason that I was one of three people who worked for the firm who was then from California.

They thought one West Coast hippy would easily get along with another. Boy, were they wrong, me in my three-piece navy blue pinstripe suit and Steve in his work Levi’s. It was the worst day of my life. Steve was not a guy who palled around with anyone. He especially hated investment bankers.

I got into Apple with my personal account when the company only had four weeks of cash flow remaining and was on the verge of bankruptcy. I got in at $7 which, on a split-adjusted basis today, is 50 cents. I still have them. In fact, my cost basis in Apple is less than the 77-cent quarterly dividend now.

Today, some 200 Apple employees subscribe to the Diary of a Mad Hedge Fund Trader looking to diversify their substantial holdings. Many own Apple stock with an adjusted cost basis of under $5. Suffice it to say, they all drive really nice Priuses.

So I get a lot of information about the firm far above and beyond the normal effluent of the media and stock analysts. That’s why Apple has become a favorite target of my Trade Alerts over the years.

And here is the great irony: Nobody would touch the stock with a ten-foot pole at the end of 2018. Since then, Apple has rallied 71%, creating more market cap in a year than any company in history.

Here’s why. Apple was all about the iPhone which then accounted for 75% of its total earnings. The TV, the watch, the car, the iPod, the iMac, and Apple Pay were all a waste of time and consumed far more coverage than they are collectively worth.

The good news is that iPhone sales are subject to a fairly predictable cycle. Apple launches a major new iPhone every other fall. The share price peaks shortly after that. The odd years see minor upgrades, not generational changes.

Just like you see a big pullback in the tide before a tsunami hits, iPhone sales are flattening out between major upgrades. This is because consumers start delaying purchases in expectation of the introduction of the new iPhones 7 more power, gadgets, and gizmos.

So during those in-between years, the stock performance was disappointing. 2018 certainly followed this script with Apple down a horrific 30.13% at the lows. Maybe it’s a coincidence, but the previous generation in Apple shares in 2015 brought a decline of, you guessed it, exactly 29.33%.

The coming quarter could bring quite the opposite.

After March, things will start to get interesting, especially post the Q1 earnings report in April. That’s when investors will start to discount the rollout of the new 5G iPhone seven months later. Everyone and his brother is waiting for 5G until they purchase their next iPhone, unless it gets lost or stolen first.

The last time this happened, in 2018, Apple stock rocketed by $86, or 55.33%. This time, I expect a minimum rally to $400 high, or much higher. After all, I am such a conservative guy with my predictions (Dow 120,000 by 2030?).

Even at that price, it will still be one of the cheaper stocks in the market on a valuation basis which currently trades at a 20X earnings multiple. The is up from a subterranean multiple of 14X a year ago. The value players will have no choice to join in, if they’re not already there.

But Apple is a much bigger company this time around, and well-established cycles tend to bring in diminishing returns. It’s like watching the declining peaks of a bouncing rubber ball.

This is not your father’s Apple anymore. Services like iTunes and the new Apple+ streaming service are accounting for an even larger share of the company’s profits. And guess what? Services companies command much higher multiples than boring old hardware ones. It’s the old questions of linear versus exponential growth.

A China trade deal will bring a new spring to Apple’s step, where sales have recently been in free fall. Their new membership lease program promises to deliver a faster upgrade cycle that will allow higher premium prices for their products. That will bring larger profits.

It all adds up to keeping Apple as a core to any long term portfolio.

Just thought you’d like to know.

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

December 24, 2019

Fiat Lux

Featured Trades:

(A CHRISTMAS STORY),

(THE U-HAUL INDICATOR)