Come join me for lunch at the Mad Hedge Fund Trader’s World Tour strategy luncheons which I will be conducting in June and July this summer.

A three-course lunch will be followed by an extended question and answer period.

I’ll be giving you my up to date view on stocks, bonds, foreign currencies, commodities, precious metals, energy, and real estate.

And to keep you in suspense, I’ll be throwing a few surprises out there too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week.

I’ll be arriving early and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The lunches will be held at a dozen five-star hotels around the world. The exact location for each lunch will be emailed with your purchase confirmation.

I look forward to meeting you and thank you for supporting my research. I’ll be posting the lunches individually in the coming weeks. You won’t be able to buy tickets until then.

Here is my schedule:

Friday, June 21 12:30 PM Auckland, New Zealand

Monday, June 24 12:30 PM Melbourne, Australia

Tuesday, June 25 12:30 PM Sydney, Australia

Wednesday, June 26 12:30 PM Brisbane, Australia

Friday, June 28 12:30 PM Perth, Australia

Sunday, June 30 12:30 PM Manila, Philippines

Tuesday, July 2 12:30 PM New Delhi, India

Friday, July 5 12:30 PM Cairo, Egypt

Monday, July 8 12:30 PM Venice, Italy

Wednesday, July 10 12:30 PM Budapest, Hungary

https://www.madhedgefundtrader.com/wp-content/uploads/2015/07/John-Thomas1-e1436361891975.jpg389400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-25 01:07:362019-07-09 03:53:542019 Mad Hedge World Tour

The Five Most Important Things That Happened Today

(and what to do about them)

1) NASDAQ Hits a New All-Time High. Unfortunately, it’s all short covering and company share buybacks with no new money actually entering the market. How high is high? Tech would have to quadruple from here to hit the 2000 Dotcom Bubble top in valuation terms. Click here.

2) German Business Confidence is Falling Off a Cliff. Make war on your trade partners and you reap the bitter fruit. Click here.

3) Boeing Takes a $1 Billion Hit on the 737 MAX Fiasco, but the stock is up $3. Monthly production has plunged from 57 planes a month to 42. Maybe the end is near? Click here.

4) Bidding War Breaks Out for Anadarko, with Occidental Petroleum offering $57 Billion compared to Chevron’s $50 billion. What do California oil companies know that others don’t? Maybe it’s another unintended consequence of the legalization of marijuana? Click here.

5) Why There’s a Spy Shortage. With everyone in the world now on Facebook and the information staying there forever, there are no anonymous people anymore. Undercover becomes impossible. Click here.

Published today in the Mad HedgeGlobal Trading Dispatch and Mad Hedge Technology Letter:

(WHY ARE BOND YIELDS SO LOW?)

(TLT), (TBT), (LQD), (MUB), (LINE), (ELD),

(QQQ), (UUP), (EEM), (DBA)

(BRING BACK THE UPTICK RULE!)

(WHO BEAT WHOM IN THE APPLE/QUALCOMM BATTLE)

(QCOM), (INTC), (AAPL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-24 13:25:282019-04-24 13:25:28Mad Hedge Hot Tips for April 24, 2019

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-24 09:13:032019-04-24 09:13:03April 24, 2019 - MDT Pro Tips A.M.

Investors around the world have been confused, befuddled, and surprised by the persistent, ultra-low level of long-term interest rates in the United States.

At today’s close, the 30-year Treasury bond yielded a parsimonious 2.99%, the ten years 2.59%, and the five years only 2.40%. The ten-year was threatening its all-time low yield of 1.33% only three years ago, a return as rare as a dodo bird, last seen in the 19th century.

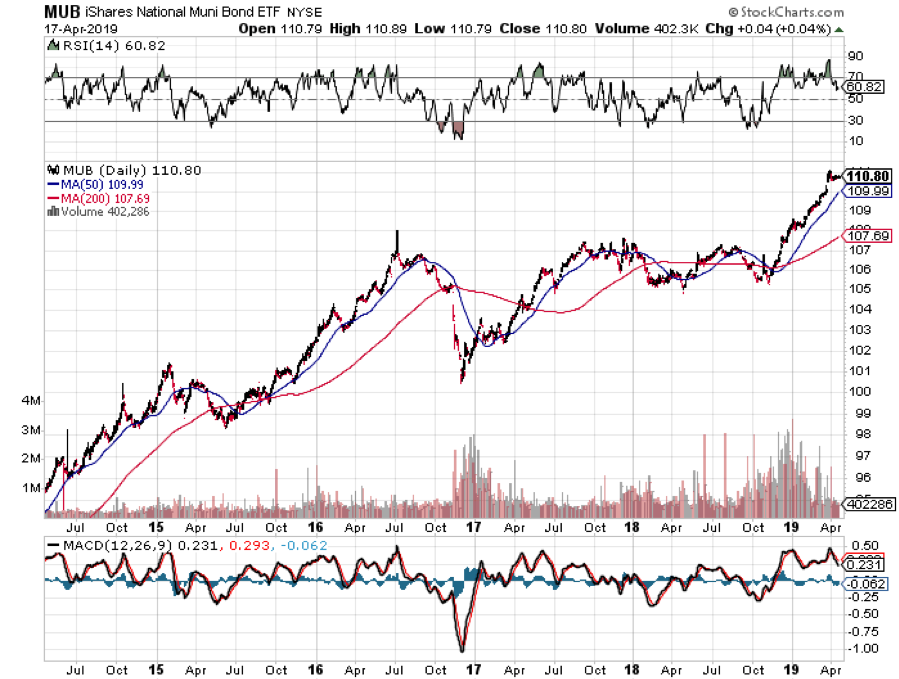

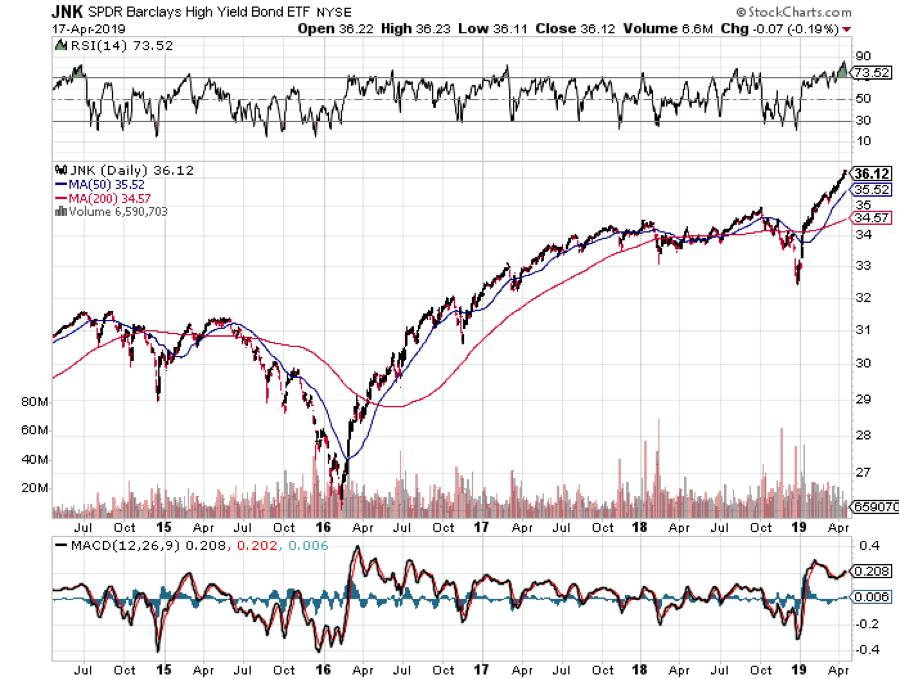

What’s more, yields across the entire fixed income spectrum have been plumbing new lows. Corporate bonds (LQD) have been fetching only 3.72%, tax-free municipal bonds (MUB) 2.19%, and junk (JNK) a pittance at 5.57%.

Spreads over Treasuries are approaching new all-time lows. The spread for junk over of ten-year Treasuries is now below an amazing 3.00%, a heady number not seen since the 2007 bubble top. “Covenant light” in borrower terms is making a big comeback.

Are investors being rewarded for taking on the debt of companies that are on the edge of bankruptcy, a tiny 3.3% premium? Or that the State of Illinois at 3.1%? I think not.

It is a global trend.

German bunds are now paying holders 0.05%, and JGBs are at an eye-popping -0.05%. The worst quality southern European paper has delivered the biggest rallies this year.

Yikes!

These numbers indicate that there is a massive global capital glut. There is too much money chasing too few low-risk investments everywhere. Has the world suddenly become risk averse? Is inflation gone forever? Will deflation become a permanent aspect of our investing lives? Does the reach for yield know no bounds?

It wasn’t supposed to be like this.

Almost to a man, hedge fund managers everywhere were unloading debt instruments last year when ten-year yields peaked at 3.25%. They were looking for a year of rising interest rates (TLT), accelerating stock prices (QQQ), falling commodities (DBA), and dying emerging markets (EEM). Surging capital inflows were supposed to prompt the dollar (UUP) to take off like a rocket.

It all ended up being almost a perfect mirror image portfolio of what actually transpired since then. As a result, almost all mutual funds were down in 2018. Many hedge fund managers are tearing their hair out, suffering their worst year in recent memory.

What is wrong with this picture?

Interest rates like these are hinting that the global economy is about to endure a serious nosedive, possibly even re-entering recession territory….or it isn’t.

To understand why not, we have to delve into deep structural issues which are changing the nature of the debt markets beyond all recognition. This is not your father’s bond market.

I’ll start with what I call the “1% effect.”

Rich people are different than you and I. Once they finally make their billions, they quickly evolve from being risk takers into wealth preservers. They don’t invest in start-ups, take fliers on stock tips, invest in the flavor of the day, or create jobs. In fact, many abandon shares completely, retreating to the safety of coupon clipping.

The problem for the rest of us is that this capital stagnates. It goes into the bond market where it stays forever. These people never sell, thus avoiding capital gains taxes and capturing a future step up in the cost basis whenever a spouse dies. Only the interest payments are taxable, and that at a lowly 2.59% rate.

This is the lesson I learned from servicing generations of Rothschilds, Du Ponts, Rockefellers, and Gettys. Extremely wealthy families stay that way by becoming extremely conservative investors. Those that don’t, you’ve never heard of because they all eventually went broke.

This didn’t use to mean much before 1980, back when the wealthy only owned less than 10% of the bond market, except to financial historians and private wealth specialists, of which I am one. Now they own a whopping 25%, and their behavior affects everyone.

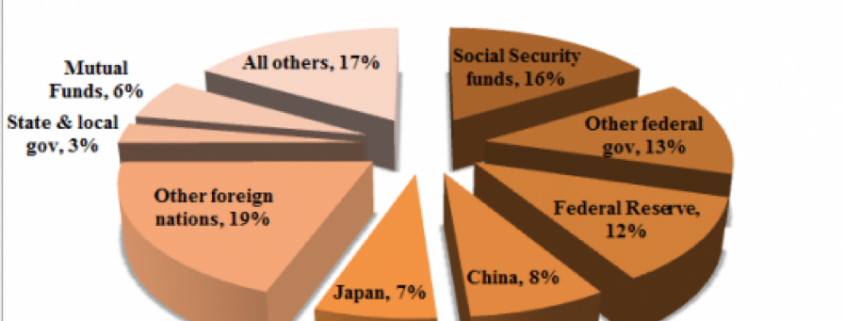

Who has been the largest buyer of Treasury bonds for the last 30 years? Foreign central banks and other governmental entities which count them among their country’s foreign exchange reserves. They own 36% of our national debt with China in the lead at 8% (the Bush tax cut that was borrowed), and Japan close behind with 7% (the Reagan tax cut that was borrowed). These days they purchase about 50% of every Treasury auction.

They never sell either, unless there is some kind of foreign exchange or balance of payments crisis which is rare. If anything, these holdings are still growing.

Who else has been soaking up bonds, deaf to repeated cries that prices are about to plunge? The Federal Reserve which, thanks to QE1, 2, 3, and 4, now owns 13.63% of our $22 trillion debt.

An assortment of other government entities possesses a further 29% of US government bonds, first and foremost the Social Security Administration with a 16% holding. And they ain’t selling either, baby.

So what you have here is the overwhelming majority of Treasury bond owners with no intention to sell. Ever. Only hedge funds have been selling this year, and they have already done so, in spades.

Which sets up a frightening possibility for them, now that we have broken through the bottom of the past year’s trading range in yields. What happens if bond yields fall further? It will set off the mother of all short-covering squeezes and could take ten-year yield down to match 2012, 1.33% low, or lower.

Fasten your seat belts, batten the hatches, and down the Dramamine!

There are a few other reasons why rates will stay at subterranean levels for some time. If hyper accelerating technology keeps cutting costs for the rest of the century, deflation basically never goes away (click here for “Peeking Into the Future With Ray Kurzweil” ).

Hyper accelerating corporate profits will also create a global cash glut, further levitating bond prices. Companies are becoming so profitable they are throwing off more cash than they can reasonably use or pay out.

This is why these gigantic corporate cash hoards are piling up in Europe in tax-free jurisdictions, now over $2 trillion. Is the US heading for Japanese style yields, of zero for 10-year Treasuries?

If so, bonds are a steal here at 2.59%. If we really do enter a period of long term -2% a year deflation, that means the purchasing power of a dollar increases by 35% every decade in real terms.

The threat of a second Cold War is keeping the flight to safety bid alive, and keeping the bull market for bonds percolating. You can count on that if the current president wins a second term.

Why Are They So Low?

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/US-debt-owners.png600897Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-24 02:07:262019-04-24 01:29:21Why Are Bond Yields So Low?

The 5G bonanza is slithering towards us in a slow yet predictable motion – that was the takeaway from Apple finally conceding that its bargaining positioning was weaker than initially thought.

Apple made amends with chipmaker Qualcomm (QCOM) in the nick of time, let me explain.

Qualcomm is the leader of 5G chip technology, and the two firms decided on a six-year pact that will allow Qualcomm to sell patent licensing to Apple while becoming a crucial supplier of 5G modems to the new iPhone that will roll-out to consumers in the back half of 2020.

Envisioning this 2 for 1 special a few weeks ago was impossible as the brouhaha spilled over into the national media with top executives exchanging barbs.

Qualcomm, to its credit, stayed steadfast on its position and was the bigger winner of the spat.

The rapid reaction in the stock price has vindicated Qualcomm’s initial reluctance to make a cut-price deal with Apple.

The new contract locks in Apple at around $9 per phone in licensing fees, almost double what many analysts were predicting.

Apple also paid a one-time fee of the backlog of patent usage from the past two years that many specialists estimate to be in the $6 billion range.

Qualcomm has previously stated that Apple owes them $7 billion from the kerfuffle and Apple’s refusal to pay stemmed from their belief that Qualcomm was “double dipping” – a claim based on Qualcomm charging a fee for each iPhone using its patents as well as a fee for the technology itself which Apple felt extortionate.

Ultimately, the jousting wasn’t worth the trouble as the best-case scenario of Apple saving $1 billion in patent fees was overshadowed by the opportunity cost which was significantly higher.

The updated terms see a substantial improvement for Qualcomm over the $7.50 per phone that Apple was paying before.

The end of the saga smells of desperation on CEO of Apple Tim Cook’s behalf, realizing that time was ticking down and competitors such as Huawei have already launched 5G-supported phones.

Apple is, in fact, late to the party and one of the main root causes was the logjam with Qualcomm.

If Apple didn’t come to terms with Qualcomm, suppliers and designers wouldn’t have enough time or supply to prepare to meet the fall 2020 deadline causing Apple to delay the new iPhone.

The worst-case scenario that became a realistic threat was that the new iPhone wouldn’t have been ready until 2021 – Apple shares would have dropped 20% in a heartbeat if this played out.

Avoiding this doomsday scenario is a massive bullish signal for Apple shares and brings forward revenue demand into 2020.

The new iPhone with ironically Qualcomm’s 5G modem technology is also the selling point for iPhone lovers to upgrade to a newer and faster iPhone iteration.

It’s a headscratcher that Tim Cook played his cards in the way that he did, another misstep in a long record of fumbles in the red zone.

Inevitably, scrunching up the production schedule heaps loads of pressure on the existing engineering teams to produce a flawless iPhone.

Apple simply couldn’t wait any longer and CEO of Qualcomm Steven Mollenkopf understood that, leading me to solely blame Tim Cook for this calculated error.

Where do the chips lie after this recent shakeout?

First, this piece of news is demonstrably bullish for Qualcomm and its business model while backloading around $6 billion or so in revenue onto its balance sheet.

In short, Qualcomm hit it out of the park and set itself up for the upcoming insatiable demand for 5G chips while publicly demonstrating they are best in show for 5G infrastructure equipment.

It might turn out to be Qualcomm’s best day in the history of the company and one that employees will never forget inside its headquarters.

This will embolden Qualcomm in the future to fight for the revenue that is rightfully theirs and they won’t be frightened by bigger sharks attempting to persuade them that they should receive a lesser share of the pie.

For Mollenkopf, this is his crowning moment and a pathway to another big-time job, the one day grabbing of the spoils has elevated his reputation.

Apple is a minor winner because of the adequate supply of chips that Qualcomm will provide that guarantees Apple’s engineers clarity instead of dragging itself deeper into a courtroom battle with a company that supplies an integral component to their iPhone.

Hours after the news hit the press, Intel (INTC) waived the white flag issuing a short response admitting they are exiting the 5G smartphone business, a bitter pill to swallow for a legacy company finding it difficult to stay with the big boys.

And if you remember, Intel was initially thought to be the one to provide memory to the 5G smartphone but now that notion is dead as a doornail.

Intel will hope they can capture a fair share of the 5G PC business to make up for the lost opportunity, but as consumers migrate away from PCs, shareholders could sense Intel could be left holding the bag.

Qualcomm has strengthened its stranglehold on the 5G smartphone modem market in an industry that will morph into a worldwide addressable market of $20 billion by 2025.

Even though Huawei just announced they would be willing to sell their 5G chips to Apple, Huawei and South Korea’s Samsung mainly produce chips for their in-house branded smartphones and shun feeding competitors like Apple who require the same chips.

Apple hoped to create some leveraging power to get a better 5G chip deal and loosen the jaws that gave Qualcomm a powerful position over Apple, but Intel quitting this segment left Apple with a series of bad choices and they chose the lesser of the evils.

What does this boil down to?

Qualcomm outmuscled Intel producing faster and better performing chips that supported longer battery life.

Qualcomm simply has better engineering talent.

Intel had an uphill battle in the first place, but it is clear they cut their losses because the writing was on the wall leaving Qualcomm to reap all the benefits.

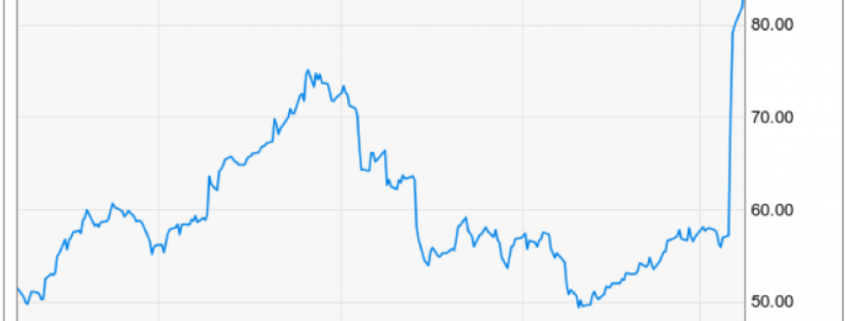

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/qualcomm.png562974Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-24 02:06:432019-07-10 21:48:50Who Beat Whom in the Apple/Qualcomm Battle

“A lot of the future of search is going to be about pictures instead of keywords. Computer vision technology is going to be a big deal.” – Said CEO of Pinterest Ben Silbermann

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/silbermann.png408256Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-24 02:05:362019-07-10 21:48:56April 24, 2019 - Quote of the Day

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to the six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-23 14:16:152019-04-23 14:16:15April 23, 2019 - MDT Alert (CNC)

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to the six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-23 13:27:192019-04-23 13:27:19April 23, 2019 - MDT Alert (CLW)

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.