The Five Most Important Things That Happened Today

(and what to do about them)

1) Boeing Hits Bottom, as the US becomes the last country to ban the 737 Max 8. Imagine being 35,000 feet in the air and you find out your plane is grounded for safety reasons, as 6,000 people did yesterday. Buy more (BA) on the dip. The next move is from $360 to $450. Click here.

2) New Homes Sales Down 6.9%, in January, far worse than expected. The report is an unmitigated disaster for the industry. If you’re trying to sell a house now, you’re screwed. Click here.

3) Weekly Jobless Claims Jump, by 6,000 to a seasonally adjusted 229,000. Notice claims aren’t calling anymore. Another sign the tax cut stimulus is shrinking? Click here.

4) The Number of US Millionaires Grew for the 10th Year, to 11.8 million. And some 1.4 million are worth $5 million to $25 million. You’re obviously not working hard enough. Click here.

5) General Electric to Burn $2 billion This Year, but the stock rallies anyway. We may be trying to put in a long term bottom this year. Buy (GE) on the dips. Click here.

Published today in the Mad Hedge Global Trading Dispatch and Mad Hedge Technology Letter:

(LEARN MORE ABOUT ME THAN YOU PROBABLY WANT TO KNOW),

(GOOG), (AMZN), (AMGN)

(AIRBNB’S SECOND THOUGHTS),

(AIRBNB)

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/John-Thomas.png337325Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-14 13:11:132019-03-14 13:11:13Mad Hedge Hot Tips for March 14, 2019

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-14 08:49:242019-03-14 12:53:57March 14, 2019 - MDT Pro Tips A.M.

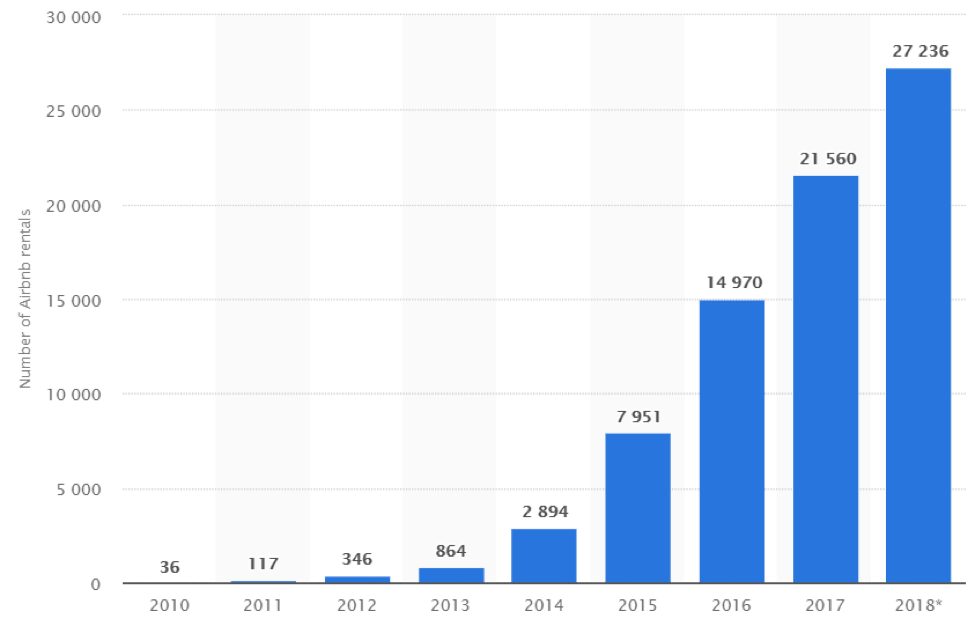

In an unusual U-turn, Airbnb co-founder Nathan Blecharczyk revealed sudden skepticism on his companies’ odds of going public in 2019.

The base case was that Airbnb was on schedule to be listed in mid-2019.

Blecharczyk fueled confusion by going on record saying that Airbnb “are taking the steps to be ready to go public in 2019. That doesn’t mean we will go public in 2019.”

The company is currently valued at $31 billion.

The co-founder resisted in offering a specific explanation in why the company is hesitant in pulling back from the public market, but part of the factors could boil down to the Brexit mess currently ongoing at 10 Downing Street and the trade war between America and China creating uncertainty around crucial Airbnb housing markets.

Executing the IPO is another quandary where the Securities and Exchange Commission (SEC) shuttered its IPO division during the government shutdown and its staff has not regained full capabilities.

The global economic slowdown has made IPO investors nervous and the slew of IPOs planned for 2019 could take rolling rain checks to ensure the stability of newly minted shares.

This is not the only problem roiling Airbnb.

Taxes.

Municipalities are sick of being shafted from the outsized revenues pocketed by Airbnb.

Hotels have been incessantly complaining that they are on the leash for taxes that Airbnb does not have to face even though they are directly competing.

Things are about to change.

Let’s take the state of Maryland as an example.

Hosts are now pre-warning potential guests that they are on the hook for 15.5% in taxes upon arrival.

The sticker shock could have the effect of killing demand or reducing it severely.

Another bill before the Senate Budget and Taxation Committee would force short-term rental brokers to collect the 6% Maryland sales and use tax at the time of booking and pass on the fees to the state.

And this is just the beginning when you consider the onslaught of regulation other states are grappling with.

Take for instance, Maryland’s neighbor Washington D.C.

The capital has come down heavy-handed on the short-term rental platform forbidding property owners renting out 2nd homes.

They have also limited the days owners can rent out their house if they are not currently present in the city forcing owners to stick around to maximize revenue.

As of now, D.C. taxes Airbnb and other short-term rental companies 14.5% and the company has aired its grievances claiming favoritism towards the local hotel industry.

City councilors have cited figures as much as $96 million over four years of potential lost taxes.

Airbnb has been painted as the scapegoat by many jurisdictions around America when you consider that traditional hotels are taxed at 13% if averaged out in the largest 150 cities.

In many cases, Airbnb is treated not as a hotel and is responsible to self-report its occupancy and revenue data giving them a chance to find loopholes to push large amounts of revenue streams through unscathed.

Governments are also dealing with additional headaches of a wave of displacement for regular payroll jobs because of the domination of Airbnb units.

This whole situation will go from bad to worse because local government is frothing at the mouth when they understand the potential tax windfall they could seize from these online platforms.

Whether legitimate or not, states could cite taxes on hotels as a starting point and start purging Airbnb of revenue through cumbersome charges, fees, licenses, penalties, and regulation.

Airbnb could end up with a bunch of Miami Beach markets on their books with the situation on the ground turning into a slugfest.

The state is at war with property owners who rent out their unit short-term with owners trying to skirt the law.

Any rentals of less than 6 months have been illegal in Miami for years.

Fines were small amounts just three years ago but the tsunami of demand to rent units at tourist hot-spots has ignited the debate of short-term rentals and the pros and cons to business and the community.

The fines have exploded to $20,000 for each citation and the local government has bombarded owners with over $8 million in fines since 2016.

Complicating the matter, owners are often not even the culprits renting out the units.

Tenants who sign up for legitimate leases are running the show themselves muddying the situation in who is liable for the fine – the owner or the tenant?

Short-term rentals have generated over $10 million in taxes to Miami-Dade County in 2018, but the state is continuing to take the stance that this tax would have flooded their coffers plus more from hotels.

This sets up a dire situation in which Airbnb will need to report quarterly earnings 4 times per year and explain to analysts and investors alike the state of regulations and engagement with authorities.

I believe the situation will deteriorate with both sides entrenching more looking to get what they want potentially turning into a legal circus.

Tech firms are known to play hardball and brinkmanship encourages rapid growth, however, this will be harder as a public company.

Airbnb is on the way to ex-growth as mounting financial and regulatory burdens are engulfing the firm.

Better to get their ducks all in a row and supercharge growth one last time before the founders finally get their big payday.

Delaying the IPO is a risky move, but if they can squeeze out a few local victories from a New York, London, or another high market revenue driver and the fact they have been cash flow positive for the last few years, look for them to rush into the IPO and cash out.

And when that time comes, Airbnb’s ultimate competitive advantage of paying minimal taxes in many locales could be dead and buried and the company might become a shell of its former self.

I’ve seen crazier things happen.

YOU ARE FINED $20,000

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/airbnb-mar14.png593858Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-14 07:06:582019-07-10 21:40:51Airbnb's Second Thoughts

“When you offer consumers choice, let them vote with their wallets.” - Said Co-Founder of Airbnb Nathan Blecharczyk

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/airbnb-cofounder.png297293Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-14 07:05:532019-07-10 21:40:58March 14, 2019 - Quote of the Day

"I manage one million people, and managing people is like managing animals, and I don't like managing one million animals," said Terry Gou, CEO of Chinese manufacturer, Foxconn, where employee suicides have been rife.

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Terry-Gou.jpg340468The Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngThe Mad Hedge Fund Trader2019-03-14 01:05:202019-03-13 19:27:49Quote of the Day - March 14, 2019

The Five Most Important Things That Happened Today

(and what to do about them)

1) Pick Your Airline Carefully. Southwest, American, Norwegian, and Icelandic Air have the most 737 Max 8 planes and their shares are getting hammered, while United (UAL) has none. As for me, I either fly my own plane or take the train. Keep buying the dip in (BA). Click here.

2) China Trade Talks to End Within Weeks, deal or no deal, says head US negotiator Robert Lighthizer. What is this, the 45th time the administration has used this headline to goose the market? Traders are getting fed up. Click here.

3) Tesla Unveils its Model Y on Thursday, a small SUV to compete with the Toyota RAV 4. The grab for market share and volume production continues. Firing their sales staff cuts overall costs by 6%. Buy (TSLA) at $260 with a tight stop. Click here.

4) Reverse Mortgages are Making a Big Comeback. Just ask actor Tom Selleck who is making millions advertising them on TV. Be careful, or your mother will end up on the street when the equity goes below zero. Click here.

5) January Construction Spending Up 1.3%, in a rare positive data point. Nothing to say here. Click here.

Published today in the Mad Hedge Global Trading Dispatch and Mad Hedge Technology Letter:

https://www.madhedgefundtrader.com/wp-content/uploads/2016/07/John-with-Tiger-Moth-e1469406885370.jpg398400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-13 11:35:262019-03-13 12:44:56Mad Hedge Hot Tips for March 13, 2019

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-13 08:45:262019-03-13 08:45:26March 13, 2019 - MDT Pro Tips A.M.

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.