While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-13 09:23:292020-05-13 09:23:29May 13, 2020 - MDT Pro Tips A.M.

There certainly will be crippling longer-term implications for the airline industry, hotel chains, and of course hospitality – but I can’t say the same for online learning platform Chegg (CHGG), which is now a great option if you're looking for tech stocks to invest in.

Chegg, is a U.S. education technology company based in Santa Clara, California who has hit pay dirt with this coronavirus epidemic.

Chegg provides digital textbook rentals, online tutoring, and other digital student services.

Schools around the U.S. and the world closed in an effort to slow the spread of the coronavirus as well as protecting our future leaders.

Despite the domestic economy on the verge of reopening, it is unclear when schools will.

Naturally, parents are also afraid to allow their children in a school environment where bacteria and germs act as a giant petri dish.

To read more about how schools are having a heck of a time reopening, click here.

Digital learning was already becoming part of the playbook, as college costs continued to soar unabated.

A rule of thumb in every industry is that a crisis often accelerates the inevitable and that is what I see happening in higher education.

Chegg is a portmanteau of the words chicken and egg and references the founders’ unenviable experience of being unable to obtain a job without experience while being unable to acquire experience without a job like many young graduates complain about.

With that in mind, the founders of Chegg, Aayush Phumbhra, Osman Rashid, and Josh Carlson, aspired to disrupt the textbook industry.

Business grew fast in the early stages – the company adjusted its business model to reflect that of Netflix's then rental-based model, concentrating on renting textbooks to students in 2007.

Eventually, the growth led into a textbook rental partnership with education mainstay Pearson Education.

Fast forward to today and Chegg’s stock chart looks like a hockey stick with shares going from $30 to $64 in 2 months.

Chegg’s first quarter revenue jumped 35%, with its services sales up 33% to account for 76% of its total revenue.

The firm also saw the number of Chegg Services subscribers surge 35% to over 3 million for the first time.

And the company forecasted that the momentum it experienced at the end of the first quarter will carry over into Q2, with it calling for its “Q2 subscriber growth to be greater than 45%.”

The substantial increase in engagement from existing subscribers is following through into a meaningful increase in the take rate of the new Chegg Study Pack, much earlier than expected.

Chegg Study Pack is a three-in-one package that bundles together Chegg Study, Chegg Math Solver, and EasyBib Plus. To understand more about the Chegg Study Pack and Chegg’s other online learning products, click here.

Chegg did not provide guidance for the second half of 2020 due to many unknowns such as school start dates, enrollment trends, and whether schools will be taught on-campus, online, or both.

The pain doesn’t stop with the toddler, what about the young adults?

The Graduating Class of 2020 is confronted with the worst hiring climate in history that has seen rescinded internships and evaporating job offers.

These students might back out of the job market completely before they get a sniff and elect to attend graduate school, meaning more online learning in the short-term.

To read about the hardships for fresh graduates, click here.

I am encouraged by Chegg's strong trends 1Q into 2Q and the broader shift of higher education in Chegg's wheelhouse, whether done on or off-campus.

Investors are focused on firms that can grow during semi-apocalyptic conditions, especially ones that seem poised for longer-term expansion within a future-looking industry like Chegg.

Meanwhile, Chegg’s adjusted second quarter earnings are expected to explode to 48% and EPS at $0.34 a share. Overall, the company’s adjusted fiscal year EPS figures are projected to surge to 33% and 22%, respectively.

Shares are overheated for the time being and readers should wait for a significant dip in shares as we approach the summer.

Buy that dip because remote learning is here to stay and first movers like Chegg will have staying power with their sticky products.

With the gains concentrated in biggest names in the Nasdaq, there is a sprinkling of uber growth names of the likes of Chegg, Docusign, Datadog, and Teladoc that are outperforming by an order of magnitude.

The issue I have with smaller cap tech stocks right now is that large cap tech stocks have durability because of balance sheet strength.

If there is a sell-off, investors will migrate further up the food chain, meaning FANGs.

As the FANGs make new highs, they continue to reward long-term investors paying a high premium of a future increase in cash flow.

Lastly, FANGs are the biggest beneficiary of the rerating of the tech market after the unprecedented surge of Fed helicopter money.

Sadly, the smaller caps do not get the lions’ share of the Fed funding funneled into its shares.

The bottom line is that the dreaded coronavirus is mutating from its original version, and this iteration has been reported to affect children.

To read about the virus mutation, please click here.

The reopening of schools is going to be staggered, expensive, unfair, and controversial in the best-case scenario.

It’s impossible to envision that students won’t be given a huge dose of Chegg’s digital learning products and even though not a FANG, the secular tailwinds in Chegg are too powerful to ignore, making it again, one of the good tech stocks to invest in.

I am bullish Chegg (CHGG).

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-13 09:02:502020-06-15 12:14:24Chegg is Another Winning "Stay at Home" Stock

“If you can't make it good, at least make it look good.” – Said Co-Founder of Microsoft Bill Gates

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/bill-gates.png178242Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-13 09:00:502020-05-13 10:01:41May 13, 2020 - Quote of the Day

We are now in the throes of a market correction that could last anywhere from a couple of weeks more to a couple of months. So, generational opportunities are starting to open up in some of the best long term market sectors.

Suppose there was an exchange-traded fund that focused on the single most important technology trend in the world today.

You might think that I was smoking California’s largest export (it’s not grapes). But such a fund DOES

The Global X Robotics & Artificial Intelligence ETF (BOTZ) drops a golden opportunity into investors’ laps as a way to capture part of the growing movement behind automation.

The fund currently has an impressive $2.2 billion in assets under management.

The universal trend of preferring automation over human labor is spreading with each passing day. Suffice to say, there is the unfortunate emotional element of sacking a human and the negative knock-on effect to the local community like in Detroit, Michigan.

But simply put, robots do a better job, don’t complain, don’t fall ill, don’t join unions, or don’t ask for pay raises. It’s all very much a capitalist’s dream come true.

Instead of dallying around in single stock symbols, now is the time to seize the moment and take advantage of the single seminal trend of our lifetime.

No, it’s not online dating, gambling, or bitcoin, it’s Artificial Intelligence.

Selecting individual stocks that are purely exposed to A.I. is a challenging endeavor. Companies need a way to generate returns to shareholders first and foremost, hence, most pure A.I. plays do not exist right now.

However, the Mad Hedge Fund Trader has found the most unadulterated A.I. play out there. A real diamond in the rough.

The best way to expose yourself to this A.I. trend is through Global X Robotics & Artificial Intelligence ETF (BOTZ).

This ETF tracks the price and yield performance of ten crucial companies that sit on the forefront of the A.I. and robotic development curve. It invests at least 80% of its total assets in the securities of the underlying index. The expense ratio is only 0.68%.

Another caveat is that the underlying companies are only derived from developed countries. Out of the 10 disclosed largest holdings, seven are from Japan, two are from Silicon Valley, and one, ABB Group, is a Swedish-Swiss multinational headquartered in Zurich, Switzerland.

Robotics and A.I. walk hand in hand, and robotics are entirely dependent on the germination prospects of A.I. Without A.I., robots are just a clunk of heavy metal.

Robots require a high level of A.I. to meld seamlessly into our workforce. The stronger the A.I. functions, the stronger the robot’s ability, filtering down to the bottom line.

A.I.-embedded robots are especially prevalent in the military, car manufacturing, and heavy machinery. The industrial robot industry projects to reach $80 billion per year in sales by 2024 as more of the workforce gradually becomes automated.

The robotics industry has become so prominent in the automotive industry that they constitute greater than 50% of robot investments in America.

Let’s get the ball rolling and familiarize readers of the Mad Hedge Technology Letter with the top 5 weightings in the underlying ETF (BOTZ).

Nvidia (NVDA)

Nvidia Corporation is a company I often write about as their main business is producing GPU chips for the video game industry.

This Santa Clara, California-based company is spearheading the next wave of A.I. advancement by focusing on autonomous vehicle technology and A.I.-integrated cloud data centers as their next cash cow.

All these new groundbreaking technologies require ample amounts of GPU chips. Consumers will eventually cohabitate with state of the art IOT products (internet of things), fueled by GPU chips, coming to mass market like the Apple Homepod.

The company is led by genius Jensen Huang, a Taiwanese American, who cut his teeth as a microprocessor designer at competitor Advanced Micro Devices (AMD).

Yaskawa Electric is the world's largest manufacturer of AC Inverter Drives, Servo and Motion Control, and Robotics Automation Systems, headquartered in Kitakyushu, Japan.

It is a company I know well, having covered this former zaibatsu company as a budding young analyst in Japan 45 years ago.

Yaskawa has fully committed to improving global productivity through automation. It comprises the 2nd largest portion of BOTZ at 8.35%.

The 3rd largest portion in the (BOTZ) ETF at 7.78% is Fanuc Corp. This company provides automation products and computer numerical control systems, headquartered in Oshino, Yamanashi.

Fanuc was one of the hot robotics companies I used to trade in during the 1970s and I have visited their main factory many times.

They were once a subsidiary of Fujitsu, which focused on the field of numerical control. The bulk of their business is done with American and Japanese automakers and electronics manufacturers.

They have snapped up 65% of the worldwide market in the computerized numerical device market (CNC). Fanuc has branch offices in 46 different countries.

To visit their company website, please click here.

Intuitive Surgical (ISRG)

Intuitive Surgical Inc (ISRG) trades on Nasdaq and is located in sun-drenched Sunnyvale, California.

This local firm designs, manufactures, and markets surgical systems and is completely industriously focused on the medical industry.

The company's da Vinci Surgical System converts surgeon's hand movements into corresponding micro-movements of instruments positioned inside the patient.

The products include surgeon's consoles, patient-side carts, 3D vision systems, da Vinci skills simulators, da Vinci Xi integrated table motions.

This company comprises 7.60% of BOTZ. To visit their website, please click here.

Keyence Corp (Japan)

Keyence Corp is the leading supplier of automation sensors, vision systems, barcode readers, laser markers, measuring instruments, and digital microscope.

They offer a full array of service support and closely work with customers to guarantee full functionality and operation of the equipment. Their technical staff and sales teams add value to the company by cooperating with its buyers.

They have been consistently ranked as the top 10 best companies in Japan and boast an eye-opening 50% operating margin.

They are headquartered in Osaka, Japan and make up 7.54% of the BOTZ ETF.

(BOTZ) does have some pros and cons. The best AI plays are either still private at the venture capital level or have already been taken over by giant firms like NVIDIA.

You also need to have a pretty broad definition of AI to bring together enough companies to make up a decent ETF.

However, it does get you a cheap entry into many for the illiquid foreign names in this fund.

Automation is one of the reasons why this is turning into the deflationary century and I recommend all readers who don’t own their own robotic-led business pick up some Global X Robotics & Artificial Intelligence ETF (BOTZ).

And by the way, the entry point right here on the charts is almost perfect.

To learn more about (BOTZ), please visit their website by clicking here.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/john-thomas-micron.png463379Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-13 08:02:552020-06-15 12:09:48Here's an Easy Way to Play Artificial Intelligence

It’s all-hands-on-deck for the biotech sector as the world battles the deadly coronavirus disease COVID-19.

As the US coronavirus-related deaths mount to over 80,000 and reported cases hitting over 1.3 million, the need to find a cure and vaccines increases in urgency every passing minute.

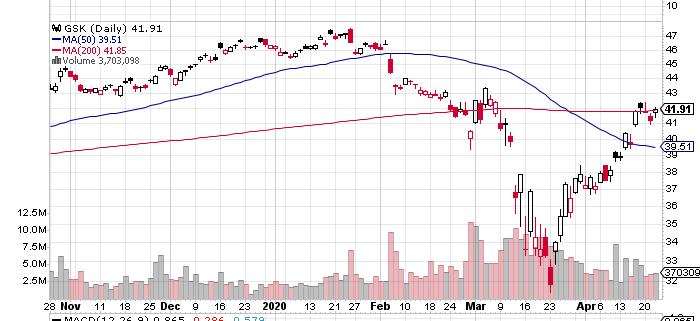

Joining the biotech companies throwing their hats into the ring is GlaxoSmithKline (GSK), which recently announced its decision to work hand in hand with Vir Biotechnology (VIR) in the search for a coronavirus cure.

On top of the collaboration efforts, the partnership will also involve GSK investing $250 million in Vir. According to these terms, each Vir share will be worth $37.73.

The collaboration announcement also pushed Vir shares to rise by as much as 34% and trading more than doubled. Meanwhile, (GSK) went up by roughly 2%.

The partnership will explore several platforms to come up with a treatment for COVID-19.

So far, the most promising candidates involve two antibodies presently dubbed as VIR-7831 and VIR-7832. Both were developed by Vir as treatments for SARS, which is also caused by a coronavirus.

Actually, these antibodies were developed using samples from a patient who recovered from SARS. However, these could also be produced artificially.

(GSK) and Vir estimate that Phase 2 clinical trials will commence in three to five months.

Apart from these antibody treatments, the two companies are also looking into utilizing CRISPR screening technology to figure out which proteins are used by the coronavirus to infect the healthy cells.

Once they identify these, (GSK) and Vir could come up with drugs that block viral infection. That is, they can use the information to create a vaccine to be used not only for COVID-19 but also for other types of coronaviruses.

According to (GSK), the Vir proteins had been identified as “highly potent” when targeted at the coronavirus in the laboratory.

If all goes well, a coronavirus vaccine could be on its way in 12 to 18 months.

Aside from (GSK), Vir also has an ongoing collaboration with another bigwig biotech, Biogen (BIIB).

This isn’t the first venture of (GSK) in looking for a COVID-19 cure though.

The British biotech giant is also working with China’s Xiamen Innovex on another potential coronavirus vaccine.

In addition, (GSK) is looking into forming a joint laboratory with AstraZeneca (AZN) to assist the UK government in stretching and expanding its supplies for COVID-19 diagnostic tests.

Although diagnostics are not part of their primary efforts, the goal is for the two big biotechs to determine the best ways to help in detecting the spread of COVID-19.

While these efforts to help find a solution to the pandemic are at the forefront of the biotech world today, GSK has a lot more to offer.

(GSK) manufactures products that people need to take on a regular basis.

The need is so great that the company actually allocates 80% of its research efforts focused on drug development for various issues like oncology, immuno-inflammation, and HIV. These treatments are vital to the daily existence of so many patients across the globe.

Meanwhile, (GSK) also aims to streamline its business and focus on the research and development of products and services. Hence, it decided to split its businesses into two.

One will be geared towards pharmaceutical efforts. The second will be focused on consumer health.

This is an excellent move in ensuring that (GSK) maximizes its potential to dominate its chosen markets.

Throughout the years, (GSK) has demonstrated its capacity to grow while delivering a strong bottom line. From 2015 until 2019, the biotech giant’s sales increased by over 40% with its operating margin rising as well.

While it’s undeniable that this global biotech stock has gotten itself caught up in the COVID-19 whirlwind that managed to hurt virtually every sector, its downside alternative makes absolutely no sense.

No one has the ability to predict and control when they get sick or what type of illness they get afflicted with, which makes the biotech sector and specifically drug developers particularly safe bet whatever the financial climate is.

So, investors looking for a stable stock can now afford to buy (GSK) shares at approximately 10 times worth of next year’s per-share profit potential. As if that’s not enough, the company also offers a mouthwatering 7.5% dividend yield.

Keep in mind that a wise way to insulate your portfolio amid the fears of a market crash is through investing in stable businesses that offer products and services needed on a daily basis.

If the companies provide essential items in both good and bad times, it’s a good sign the stocks will be able to survive any market crash.

(GSK), which is currently at an 11-year low due to the pandemic and economic crisis, is worth considering.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/april282020biotech.png530700Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-12 18:00:132020-05-12 18:24:12GlaxoSmithKline’s Entry Into the COVID-19 Vaccine Race

Mad Hedge Biotech & Healthcare Letter April 28, 2020 Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE) (GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but take advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/jt101.jpg400400JPhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngJP2020-05-12 17:34:012021-04-05 14:00:23The Five Frontrunners in the Race for a COVID-19 VACCINE

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.