Mad Hedge Technology Letter

August 10, 2020

Fiat Lux

Featured Trade:

(SCRAPING THE BOTTOM OF THE TECH BARREL WITH UBER)

(UBER), (LYFT), (FB), (AMZN), (GOOGL), (NFLX), (AAPL), (MSFT)

Mad Hedge Technology Letter

August 10, 2020

Fiat Lux

Featured Trade:

(SCRAPING THE BOTTOM OF THE TECH BARREL WITH UBER)

(UBER), (LYFT), (FB), (AMZN), (GOOGL), (NFLX), (AAPL), (MSFT)

The coronavirus and the resulting effects from it have had the single most sway on tech companies since the 2001 tech bust.

Marginal tech companies or even quasi-fraudulent ones have been exposed for what they are, while the secondary effects from the virus have supercharged the behemoths of the industry.

The stock market has no earnings growth in the past 5 years without the earnings from Microsoft (MSFT), Facebook (FB), Apple (AAPL), Google (GOOGL), Amazon (AMZN), and Netflix (NFLX). That means that without the Republican corporate tax cut, there has been negative earnings growth in the past five years.

One of those tech companies at the bottom of the barrel has been chauffeur service company Uber (UBER) and their latest earnings report is a glaring indictment of a shoddy business model that operates in a gray area.

The only reason this stock is at $33 is because of the piles of easy money printed by the central bank.

Uber needs all the help they can get, and shares are still trading 20% below the IPO price.

Competitor chauffeur service Lyft (LYFT) is doing even worse registering a 50% decline since the IPO.

Let’s do a little snooping around to see why these companies are doing so poorly and why you shouldn’t even think about investing in these companies long-term.

No matter how you dice it up, Uber’s core business, the one where they refuse to properly compensate their drivers, had a disaster of a quarter with gross ride volumes down 73% year-over-year.

Before we go any further with this one, I would like to point out yes, other areas of the business grew substantially, the problem is that the “other” part of the business is only 30% of total revenue.

Therefore, when 70% of your business that relies on pure volume to scale out crashes by 73%, it doesn’t really matter what else is in the report.

The only sensible idea now is capturing a snapshot of the silver linings, of which there were a few.

Delivery volumes through Uber Eats were up 49%, but the problem here is that first, it’s not profitable per delivery and second, it’s still a small part of the business.

Uber acquired Postmates who is another loss-making delivery service and the idea behind this is to achieve significant cost savings by scaling out these powerful assets.

The problem here is that it is essentially throwing good money on top of bad money because it’s proven that deliveries don’t make money per ride and that won’t change in the near future.

CEO of Uber Dara Khosrowshahi is on record saying Uber will become “profitable on an adjusted earnings basis before interest, taxes, depreciation, and amortization before the end of the year.”

This is almost like saying we won’t lose as much money as before and ironically, Dara Khosrowshahi has withdrawn this statement as the ride-sharing model has been repudiated by the consumer during the coronavirus.

Nowhere in the earnings report is the explanation of how Dara Khosrowshahi plans to attract people to share a car ride with a stranger during a global pandemic.

He didn’t share a solution because there isn’t one, hence the 73% decline in ride volumes.

If we assume this company is semi-fraudulent, then the silver lining would be that ride volumes didn’t decline by 100%.

That is where we are now with U.S. corporate companies such as the airlines that fired their employees but have subsidized them to stick around even though there is no work.

Instead of re-imagining itself through bankruptcies, the Fed has encouraged many marginal companies by breathing life into their finances through cheap loans.

This gives failing firms a last chance to enrich management with the capital and “cash out” before they hand the business off to someone who will essentially plan to do the same.

I will say that traders might have a trade or two in this one, because it’s hard to imagine Uber posting another 73% loss in ride volume and a dead cat bounce trade could be in the cards.

Long term investors should steer clear of this one and allow Uber to struggle on its own and just maybe in 5 or 10 years, it might just be “profitable on an adjusted earnings basis before interest, taxes, depreciation, and amortization before the end of the year.”

With so many high-quality tech companies and even one that is about to add super growth elements like TikTok into its portfolio, there are so many superior names to deploy capital in the tech ecosphere.

Either you must be galvanized by a gambler’s mentality to invest in Uber, or losing money is something that is habitual in your routine.

“Desperation sometimes drives innovation.” – Said CEO of Uber Dara Khosrowshahi

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

August 10, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GET READY FOR THE REVERSAL)

(INDU), (SPY), (TLT), (DIS), (BAC), (GLD)

Epidemics ebb and flow.

Every spike is followed by a retreat. The cycle continues until everyone has been exposed to the disease….or is dead.

Covid-19 has been on a tear for the last two months, doubling the number of US deaths to 162,000. An interim peak is just around the corner.

What happens when Covid takes a vacation? All existing trends in the financial markets will reverse. The big tech stocks will take a long-needed rest. Bonds will sell off. Gold will retest its recent breakout level at $1927. The US dollar will briefly get off the mat.

That means we are about to see a resurgence of “recovery” stocks, which have been ignored since June due to the declining probability of an economic resurgence as the “V” shaped recovery went out the window. Any break in the disease will bring a rally in this group. Those include hotels, casinos, movie theaters, restaurants, airlines, cruise lines….and banks.

Banks are far and away the quality play here. While other sectors may not see black ink for years, or may not survive at all, banks are making money right now.

Thanks to Dodd-Frank, the banks entered this crisis with less leverage and far stronger balance sheets than in 2008-2009. They will profit from falling bond prices, rising interest rates, waning defaults, and benefit mightily from generous government subsidies from multiple stimulus programs.

Institutions are underweight in banks, yet they are still at two-thirds of their January peak prices when the market leaders are 50% above old all-time highs.

If I am wrong and the next “recovery” rally takes weeks, or even months to start, they will continue to drift sideways. That makes them perfect candidates for short-dated option calls spreads. These make money whether the share goes up, sideways, or down small.

The campaign for a spectacular second-half performance has begun!

The U.S. Economy added jobs at a slower pace. US job growth weakened in July, with only 1.763 million people re-employed around the US as opposed to nearly 5 million in June, higher than estimates. The unemployment rate fell to 10.2% from 11.1% in June. At least 31.3 million people were receiving unemployment checks in mid-July.

Weekly Jobless Claims ticked down. The advance figure for seasonally adjusted initial claims was 1,186,000, a decrease of 249,000 from the previous week’s revised level. The report reflected the 20th straight week that new claims topped 1 million as the pandemic was the catalyst for a slew of firings. This number was the lowest since late March when the country saw an unprecedented explosion in requests for unemployment assistance.

The rehiring trend loses pace, indicating that virus infections slowed the economic recovery. Many states closed parts of their economies again and consumers remained cautious about spending. U.S. firms added just 167,000 jobs in July, payroll processor ADP said Wednesday, far below June’s gain of 4.3 million and May’s increase of 3.3 million. The economy still has 13 million fewer jobs than it did in February.

Congress is still unable to agree on a stimulus bill, with the $600 per week unemployment benefit ending. This is taking place while the virus rages through the mid-west and south. New Corona cases have exploded to 60,000 per day. Republicans want to cut the $600 per week excess benefit to $200, while the Democrats believe the $600 per week should be upheld.

A vaccine could hammer tech stocks, says Goldman Sachs, sparking a sell-off in bonds and rotation out of technology into cyclical stocks. The U.S. election and the evolution of the virus will be key drivers of the market. Approval of a vaccine could challenge market assumptions both about. This also could end with high-quality tech stocks having a massive correction.

Disney’s (DIS) digital subscriber base surged past 100 million. The company’s digital streaming segment was the sole bright spot for the company with Disney+ having 60.5 million paying customers as of Monday – up from 54.5 million on May 4. Disney also announced blockbuster feature Mulan in select markets as a $30 rental. I can’t wait to watch it.

The U.S. economy will recover to pre-pandemic levels by the end of 2021. Federal Reserve Vice Chairman Richard Clarida revealed that he expects the economy to grow in the third quarter. The health crisis hasn’t yet caused long-term damage to the U.S. economy, he said in an interview with CNBC, but the risks will grow the longer the pandemic lasts.

The 30-year fixed mortgage rate dropped to 3.14%. Mortgage rates have fallen faster than ever, and they've been remarkably willing to set record low after record low. Risk-adverse investors have been plowing their money into Treasury bonds (TLT) and government guaranteed mortgage backed securities, for safety.

Gold (GLD) to surpass $3,000 per ounce in 18 months, says Bank of America (BAC). Prices for gold futures for December delivery climbed to a record high above $2,000 per ounce. Retailers in malls and dealers in New York City’s Diamond District are swamped by orders due to the pandemic.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

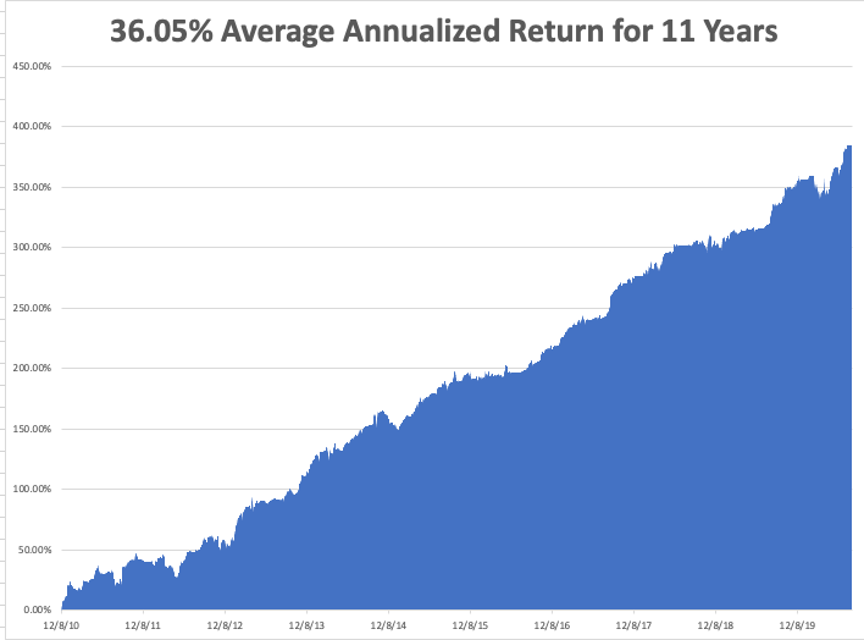

My Global Trading Dispatch has been flatlining for the past two weeks while I have been on vacation. July finished at a red hot 7.93%, delivering a 2020 year to date of 28.63%. That takes my eleven-year average annualizede performance to a new all-time high of 36.05%. My 11-year total return has stretched to 384.54%.

The only number that counts for the market is the number of US Coronavirus cases and deaths, which you can find here.

On Monday, August 10 at 11:00 AM EST, July US Inflation Expectations are published.

On Tuesday, August 11 at 6:00 AM EST, The NFIB Small Business Optimism Index for July is released.

On Wednesday, August 12, at 8:30 AM EST, the July US Inflation Rate is out. At 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out.

On Thursday, August 13 at 8:30 AM EST, the Weekly Jobless Claims are published.

On Friday, August 14, at 10:00 AM EST, the University of Michigan Consumer Sentiment is printed. At 2:00 PM, the Bakers Hughes Rig Count is released.

As for me, I shall be recovering from the multiple cuts and bruises I suffered from my 50-mile hike with the Boy Scouts. Nothing major, that beset multiple other hikers we encountered along the way, for which I provided first aid.

I managed to bring back 16 scouts who finished the entire 50 miles in seven days, accomplishing a vertical climb of 6,300 feet. Only a Marine graduating from boot camp could accomplish such an endurance contest.

It was all worth it. Every morning, I wound up to a view taken from a Christmas calendar. My exertions lost me 20 pounds, thus tripling my wardrobe. And the bears mercifully left us and our food supply alone.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Technology Letter

August 7, 2020

Fiat Lux

Featured Trade:

(FINTECH IN 2020 IS TOO HOT TO HANDLE)

(PYPL)

I’ve been kicking myself that I missed the boat this year on a stock that I spent last year hyping like no other after I predicted a tsunami of bullish action from fintech players.

I pigeonholed PayPal (PYPL) as one of the rising stars of the fintech industry and they certainly have delivered in spades.

But even I didn’t see this coming.

PayPal has more than doubled since the tech wreck in March and shares are trading north of $200.

A quick double of the stock has more than 20 analysts raising price targets for the stock since earnings came out, and most reiterated conviction buy ratings on the shares.

PayPal’s monetization engines take from both sides of its consumer and merchant platforms.

I expect growth on the top line to speed up and margins to increase if the rapid digitization of payments turns out to be here to stay, which I wholeheartedly believe it will.

PayPal’s business model has leaned on e-commerce payments, but now is the perfect time to invest in so-called frictionless payments, as well as consumer banking.

They hope to roll out QR code functionality in the US.

PayPal recently announced a partnership with CVS Health (CVS) to roll out QR-code payment options in more than 8,200 pharmacy stores in the fourth quarter.

The better-than-expected second-quarter results were solid across the board stemming from net new additions to the client (and merchant) count, TPV growth, Venmo growth, revenue growth, margins, and cash flow.

That is a whole lot of positives to work from!

Now, there is considerable evidence of sustainability of the underlying behavioral changes that are producing the growth.

Management’s decision to raise and increase estimates it had withdrawn demonstrates the company’s confidence.

There is bullish case for an opportunity for a new margin profile for the company longer term.

PayPal is about the shrug off the end of the eBay operating agreement and start harvesting volumes from several of its multi-year investments (Paymentus, MELI, Uber, Facebook, Honey acquisition).

PayPal is well-positioned in a market that could add up to $5 trillion even excluding online bill-payment services, in-store payments, and the Chinese market.

In mid-2020, it is clearly the most atrocious macroeconomic backdrop any of us have seen, with major parts of business travel and events on the back burner, and PayPal is still pulling off miracles by producing record numbers.

I attribute PayPal’s success to a multipronged, diverse platform scaled across the world that allows users to invest in this environment and shape the outcome, rather than sitting back and being a recipient.

The number that sticks out most is the more than 21 million net new active customers across its platform in the June quarter, a bigger number than in some entire years.

The bullish case for PayPal will outlast the health crisis as consumers are now tied to using PayPal during the crisis and will continue to do so long after because the product delivers the security and convenience that others don’t.

The outperformance certainly has something to do with a high level of trust and security that goes with it to boost the legitimacy of the brand and that is especially salient for new joiners.

No doubt that PayPal is hardly the only digital payment option, and competition is fierce, but they are good at what they do.

This is an inflection point in e-commerce and digital payments; the trends were pulled forward by two or three years, but the most fundamental difference right now is the new and expanded addressable market in the offline world.

The market has increased exponentially, in a world where digital payments are a major slice of all payments, PayPal is fully expected to continue to outperform.

There is the case that shares are too far out over its skis in the short-term, but for good reason.

I would put this stock on the high alert list ready to put new money to work in shares as soon as there is a medium-sized pullback.