When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-11-06 15:42:542020-11-06 15:42:54Trade Alert - (TWTR) November 6, 2020 - BUY

Tech has been trending downwards for the past 2 months apart from this relief rally celebrating potential gridlock in the senate.

There is a high probability that tech will be dormant in the short-term offering me a great opening to focus on alternative industries adjacent to tech that is also forward-looking.

Despite the global pandemic destroying large segments of the U.S. economy, the solar sector has been a revelation.

This is not much of a surprise for long-time solar industry nerds since a similar decoupling occurred in 2009 when many economics were hard hit by the Financial Crisis of 2008.

Under normal seasonality, the solar industry typically strengthens each quarter with the first quarter being the weakest boding well for the last 2 months of 2020

Enphase Energy, Inc. (ENPH) is the company I would like to fill you in on today and they design, develop, manufacture, and sell home energy solutions for the solar photovoltaic industry in the United States.

Looking forward, Enphase expects third quarter revenues to range between $160 to $175 million.

One of Enphase's critical competitive advantages is that the company operates more as a technology company than a commodity manufacturer.

While other companies do produce its main power inverter product, Enphase has market dominance in the micro-inverter segment.

For residential solar applications, micro-inverters do offer an advantageous alternative. Enphase's shipment growth over the past couple of years is the empirical evidence.

Even more salient, the company avoids ruinous capital expenditures by deploying contract manufacturing similar to peers with proprietary technology.

By leveraging these variables, Enphase has accelerated its high gross margins above 30%.

The company's lower margins last year were in part due to higher expedited shipping costs to satisfy demand but has solved that bottleneck and boosted gross margins to over 40% this year.

Enphase's stable high gross margin is the x-factor.

Most solar module producers have high fixed costs which deteriorate margins and drag down utilization rates.

As a result, not only do shipment gyrate between industry cycles but also gross margin. While Enphase is also exposed to industry fiscal cliffs, high gross margins should be highly constructive even in down years.

During up cycles, Enphase's high gross margins and lower operating structure give it abnormally advantageous earnings leverage.

Enphase's earnings leverage will be even more dramatic once revenue growth reaccelerates after the pandemic filters through the U.S. economy.

Up until now, Enphase has been pigeonholed as an inverter company within the solar industry.

The company did offer a battery storage option, but it was not an overwhelming segment of total revenues.

This may change moving forward after the company's next generation Encharge storage option released lately has shown glimpses of stardom among its competition.

As the election grinds down to a bitter finish, Presidential candidate Biden has already announced a $2 trillion climate plan which obviously would include expanding solar installations and be on the table if Biden eventually claims victory.

While a Democratic blue wave could have opened up an opportunity for sweeping change for US solar companies such as Enphase, flipping the US Senate to Democratic control is not a prerequisite for the solar industry to be successful.

It’s already trending in that direction as a mega growth industry like technology.

Also, the Democrats will try to crowbar in any climate-related infrastructure spending with any potential stimulus bill which could add more dollars behind the solar industry.

If annual residential solar installations double with a slightly higher per home average, about one million homes would be converted to solar annually.

With over 139 million homes in the US, only a small fraction would be converted to produce solar electricity over the next decade or two, even if the US residential solar market doubled.

The main takeaway is that the solar market in the US still has a huge upside under the right policies.

Enphase has a current micro-inverter capacity of 10 million units annually and based on its per-unit assumption of 325 watts, can supply 3.25 GW annually.

Based on comments in the company's second quarter earnings conference call, capacity could potentially be raised to 16 million annually with the expansion of its Mexico-based facility and a new India-based contract manufacturer.

Given the lead time required to ramp, actual shipment capacity next year may only be equivalent to 4 GW. If the company's geographic mix remains steady with last year's 83.9% US exposure, about 3.36 GW would be allocated to the US market. This would represent about 68.6% of the total US residential and commercial market during 2019.

Should the US solar market double due to beneficial policies, Enphase's potential market share will rise above 34%.

This would represent about a 10% increase in US market share from Q4 2019.

Ultimately, Enphase's high margins and fixed cost structure should not be underestimated especially under a systemic industry shift such as a Biden-led US economy laser-focused on green infrastructure.

Enphase is one of a few cost-effective US solar companies with attractive products that could get a boost from favorable governmental policies.

Expanded US market share due to favorable policies could push annual earnings well above any expected scenario.

The secret recipe of high gross margin and low-cost structure make Enphase incredibly leveraged to top-line growth.

Lately, a new storage revenue stream and continued shipment growth in a rapidly expanding solar market should result in overperforming earnings growth.

New storage products will meaningfully add to earnings next year without diluting gross margin and Enphase's high US exposure could benefit under a Democratic administration more biased to renewable energy.

Enphase is an unequivocal buy and hold stock and it’s no surprise that shares are up 400% in 2020 at the time of the writing.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-11-06 11:02:472020-11-10 21:55:19In the Know About Enphase Energy

“Technology is a useful servant but a dangerous master.” - Said Norwegian Historian Christian Lous Lange

https://www.madhedgefundtrader.com/wp-content/uploads/2020/11/lange.png268196Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-11-06 11:00:432020-11-06 11:18:00November 6, 2020 - Quote of the Day

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-11-06 10:36:112020-11-06 10:36:11Trade Alert - (GOLD) November 6, 2020 - SELL-TAKE PROFITS

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-11-06 09:59:502020-11-06 09:59:50November 5, 2020 - MDT Pro Tips

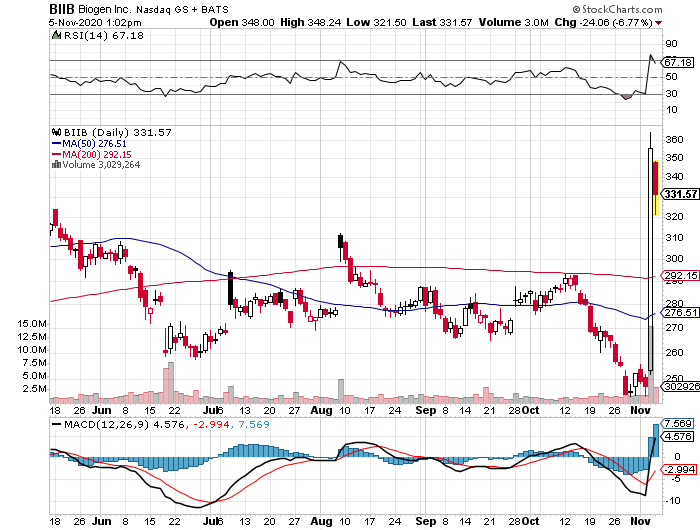

Investing in beaten-up stocks in this period of uncertainty demands nerves of steel.

In fact, some biotechnology and healthcare stocks have been left for dead in recent months. Meanwhile, there are others that continue to deliver amidst the ongoing pandemic.

Biogen has been consistently tagged as a high-risk-high-reward stock even before the COVID-19 pandemic started.

However, people seem to miss the fact that the company has relatively low debt and a surprisingly positive free cash flow in the past years.

Since 2019, the banner headline for Biogen has been its experimental Alzheimer’s disease treatment Aducanumab.

Recently, Biogen released promising progress following its decision to submit the Alzheimer’s candidate for a priority review to the FDA. It has also been accepted for review by European health regulators.

Although this move appears risky, the goal is to accelerate FDA’s timeline for Aducanumab.

That is, Biogen’s decision to submit the drug for approval earlier than expected also pushes the decision to an earlier date, which is March 7, 2021.

If approved, then Aducanumab will be the first-ever approved drug for Alzheimer’s disease.

The road to this point was not easy though. Biogen went through a series of failed trials and even a brief period of giving up on the project before the company gave the effort another chance.

Looking at the market opportunity for this sector, Biogen’s about-face no longer comes as a surprise.

For decades now, companies have been looking into ways to at least slow the progress of the condition, treat the symptoms, and offer faster ways to diagnose it.

There is currently no cure for this disease, which is ranked as the sixth leading cause of death in the country and accounts for approximately 2 million deaths globally.

Given that this disease takes years to progress, it means tens of millions of patients live with the condition on a daily basis -- and this sector comprise the target niche for Aducanumab.

In the United States alone, over 5 million people are diagnosed with Alzheimer’s disease annually and this number is projected to increase to nearly triple by 2050.

With all the treatments geared towards Alzheimer’s disease, sales for these products were estimated at $3.5 billion in 2018. This cost is expected to hit a 7.2% compound growth rate yearly until 2030.

If successful, Aducanumab can reach peak sales somewhere between $10 billion and $20 billion.

For context, the annual sales of Biogen today is only under $15 billion.

This underscores the significance of Aducanumab for the company as the drug can more than double its total earnings and even its market capitalization. It can also offer a 3x to 4x jump in Biogen’s share price.

Apart from Biogen, other big names working on an Alzheimer’s treatment are Eli Lilly (LLY) and Axsome Therapeutics (AXSM).

Outside Biogen’s work on Aducanumab, the company also has an impressive asset portfolio.

Its second quarter earnings results for 2020 showed that revenues from its multiple sclerosis drug segment contributed significantly to the company’s profits, with Ocrevus raking in $2.3 billion for the period.

The newly acquired rare spinal muscular atrophy disease drug Spinraza also performed well, reporting approximately $2 billion in annual sales.

Even its embattled multiple sclerosis treatment Tecfidera, which has been facing patent exclusivity issues with generic companies like Mylan (MYL), reported an increase from its notable $1 billion in revenue for the first quarter of the year to $1.2 billion in the second quarter.

Finally, Biogen has been working on expanding its biosimilar segment to increase its competitive advantage particularly for its drugs that are nearing the end of their patent exclusivity.

Amid the pandemic, Biogen’s revenue was up by 1% to hit $3.5 billion in the first quarter of 2020 and increased by 2% to reach $3.7 billion in the second quarter.

The company’s financial results also rose by approximately $100 million in the first three months of this challenging year.

However, a widely known caveat not only for Biogen but also for a number of biotechnology companies is the volatility of the stocks.

There is no one-size-fits-all formula for investing in beaten-up stocks. It comes with zero guarantees that their past performances would make a repeat either.

The strategy for these things though is quite basic. Make sure to look at businesses that offer sufficient bandwidth to bounce back once things normalize and the effects of the pandemic start to ease.

Looking at its overall performance, Biogen has achieved an impressively strong financial position despite the setbacks along the way. The company even offers room for growth regardless of the performance of its much-awaited Aducanumab.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-11-05 13:00:132020-11-06 00:06:31It’s Go Time for Biogen's Alzheimer's Drug

PRA has been trading in a range since the position was put on.

And as I write this, it is trading around $15.27.

We can collect $.20 per share by selling the November monthly calls against the position and that is what I suggest you do.

Here is the trade:

Sell to November 20th - $17.50 call for $.20.

These calls expire in two weeks.

This will bring to $1.00 per share the premium collected on the position.

And if the calls are assigned on the 20th, the return will be 12.5%.

Only sell these calls if you are long the stock. And sell 1 call for every 100 shares you own.

This alert applies to you only if you own shares in PRA.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-11-05 12:55:232020-11-05 12:55:23November 5, 2020 - MDT Alert (PRA)

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.