Mad Hedge Technology Letter

June 16, 2021

Fiat Lux

Featured Trade:

(SMARTPHONES AREN’T GOING AWAY)

(AMZN), (TSLA), (FB), (GOOGL), (AAPL), (NFLX)

Mad Hedge Technology Letter

June 16, 2021

Fiat Lux

Featured Trade:

(SMARTPHONES AREN’T GOING AWAY)

(AMZN), (TSLA), (FB), (GOOGL), (AAPL), (NFLX)

The United States has long been the world leader in science and technology, but lately, they are falling asleep at the wheel.

At a psychological level, the feeling of threat has led to all sorts of unintended consequences, and it has been no accident we are seeing at a trade war.

The one key ingredient that has been missing is sustained investment in our research enterprise.

Without relentless investment into scientific and technological leadership, don’t expect any new breakthroughs, and the stagnation of US technology is evident in the evolution of a product that goes on sale to the consumer.

What happened to 5G? It’s been hyped for the past 3 years, but people have felt no need to upgrade for the spotty 5G that is available.

What happened to automated cars?

I thought by now, we would be able to get around with our flying cars.

What we do have are bigger iPads, faster iMacs, and the Microsoft Surface which is a tablet with an attachable keyboard.

I wouldn’t call that success.

But what the pandemic did was allow these big tech firms to get away without innovating, and I am not talking about the incremental innovation that makes a Model 3 Tesla 4% better than the prior iteration.

The hype of 10 years of digital transformation into one year has been profusely disseminated but misunderstood.

I can tell you that we didn’t experience 10 years of digital development pulled forward into 1 year.

That definitely was not the case over the past 15 months.

More accurately said, we had 10 years of expandable margin opportunities squeezed into one and the biggest beneficiary of this is the balance sheet of big tech.

What we did was give a reason for tech to not ditch this over-reliance on the smartphone which is going strong into its 13th year.

It was 2007 when Steve Jobs delivered us the iPhone and by 2008, many consumers were using it.

In 2021, the iPhone and variants still have a stranglehold on human life and the way business models are put together.

That won’t go away because of the pandemic and now these big tech behemoths have no reason to dip too far into capital expenditures.

Not only that, but they are also cutting back spend on office space and business travel too while sneakily reducing salaries of remote employees who move to cheaper cities.

In fact, the pandemic will elongate the smartphone dynasty, and any other meaningful tech has been put back on the backburner for the time being.

Then there are companies like Uber that are busy sorting out its decimated ride-sharing business before they can even dream about flying uber cars.

So, I am not surprised that the House Science Committee is taking up two bipartisan bills to try to push the agenda forward.

The need to act is best captured by two data points. First, as much as 85% of America’s long-term economic growth is due to advances in science and technology. There’s a direct connection between investment in research and development and job growth in the U.S.

Second, China increased public R&D by 56% between 2011 and 2016, but U.S. investment in the same period fell by 12% in absolute terms. China has likely surpassed the U.S. in total R&D spending and — through both investment and cyber theft — is working to overtake the U.S. as the global leader in science and technology.

America’s continued scientific leadership requires a comprehensive and strategic approach to research and development that provides long-term increased investment and stability across the research ecosystem. And it must focus on evolving technologies that are crucial to our national and economic security, like semiconductors and quantum sciences.

Now that the U.S. government has identified this issue as a national security issue, money will be thrown at the problem, but don’t expect anything to change tomorrow.

We are still a way off from forcing big tech to change their profit models and that will happen when they need to keep up with the next big thing.

There is no big next thing yet.

Until then, expect more incremental progress from your smartphone and Tesla.

It’s certainly not a bad situation to wield a smartphone that is 4% better each year or drive a Tesla that performs just a bit better as well.

Effectively, these enormous and profitable revenue models will stay in place and investors have no reason to worry about big tech moving forward.

This benefits the likes of Amazon, Tesla, Facebook, Google, Apple, and Netflix.

The only risk to U.S. tech is a threat that the U.S. government is absorbing themselves. What a great industry to be in.

Net-net, this is a great win for big tech and I don’t expect anything to drastically change, but get ready for a lot more digital ads in your daily consumption of digital content and more of the same products.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

June 16, 2021

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT VIDEOS ARE UP!)

(THE MAD HEDGE DICTIONARY OF TRADING SLANG)

Mad Hedge Biotech & Healthcare Letter

June 15, 2021

Fiat Lux

FEATURED TRADE:

(A STOCK TO ADD TO YOUR RETIREMENT PORTFOLIO)

(MRK), (REGN), (GSK), (LLY), (GILD)

Building a retirement portfolio is different from when you’re aggressively playing the market. With this, you’d want something with less risk and more stability. A healthy helping of income definitely wouldn’t hurt either.

Taking these into consideration, a particular stock that offers a well-balanced mix of income and capital appreciation comes to mind: Merck (MRK).

The biggest news for Merck recently is its $1.2 billion deal with the US government involving its experimental COVID-19 antiviral.

The treatment, called Molnupiravir, is expected to cost about $700 per course, putting the total of the order from the US to 1.7 million courses.

This is just the beginning though. According to Merck and its partner, Ridgeback Biotherapeutics, they can produce at least 10 million courses of Molnupiravir by the end of 2021.

If we use the same pricing as the US, then we can expect approximately $7.1 billion in sales for Molnupiravir alone this year.

Still, the $1.2 billion deal with the US is already a massive win for Merck as experts initially estimated that Molnupiravir sales would only reach $25 million this year.

What makes Molnupiravir unique and more advantageous than its competitors is that the drug is taken orally.

The convenience alone easily edges out the other monoclonal antibody therapies from the likes of Regeneron (REGN), GlaxoSmithKline (GSK), and Eli Lilly (LLY)—all of which need to be administered intravenously.

If Molnupiravir does gain emergency use authorization from the FDA, its sole competitor in the market today is Veklury from Gilead Sciences (GILD).

To offer an idea on the size of the market for this treatment, Gilead recorded $2.8 billion in sales of Veklury in 2020. This figure is even projected to go up to $2.9 billion for this year.

Apart from its COVID-19 program, Merck has always been a favorite among value investors.

It’s a great dividend stock and has gained a reputable name in the industry as being one of the biggest and oldest companies in this field.

It’s also the force behind blockbuster treatments like the top-selling cancer drug Keytruda, HPV vaccine Gardasil, and of course, the diabetes medication Januvia.

In fact, Keytruda is estimated to become the No. 1 selling drug in the world by 2023—an achievement that Merck has lots of time to capitalize on considering that the treatment’s patent exclusivity lasts until 2028.

Keytruda is a key revenue generator for Merck, with the cancer drug showing off a 19% jump to reach $3.9 billion in sales in the first quarter of 2021.

This puts it on track to rake in roughly $16 billion in sales for this year, showcasing an 11% increase from 2020.

By 2026, Keytruda is estimated to generate $24.32 billion in sales annually.

Apart from Keytruda, Merck has been boosting its pipeline as well. For example, Bridion, one of its newer drugs, raked in $1.2 billion in sales in the first quarter, which is up 6% year-over-year.

Looking at its history, Merck has repeatedly shown that it can compete aggressively in the biopharmaceutical industry.

In 2020, the company still managed to generate $48 billion in sales despite the pandemic, with an earnings per share of $5.94—a value that’s 65% stronger than it was just five years ago.

Its strong profit growth and promising pipeline programs have allowed the company to boost its dividend payout at an impressive 7.1% pace over the past years.

This is a performance that most blue-chip companies, regardless of their size and market cap, struggle to keep up with.

Merck isn’t as exciting as the other stocks in the biotechnology and healthcare market, but that’s a comforting thought for investors who are on the lookout for a stable business.

Although Merck stock is not dirt cheap, I think it’s attractive for those who have extra cash or are hesitant to roll the dice on more volatile companies today.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

June 15, 2021

Fiat Lux

Featured Trade:

(THE BIG TECH LEAPS OPPORTUNITIES THAT JUST OPENED UP),

(AMZN), (MSFT), (AAPL)

The blockbuster Consumer Price Index report on Thursday delivering a 5% inflation rate, the highest since 2008, has befuddled, gobsmacked, and stunned fund and hedge fund managers alike. With the hottest economic growth in history now underway, this was not supposed to be in the script.

The plunging interest rates this triggered has also created once-in-a-lifetime trades in big technology stocks, which have been written off for dead for almost a year. The shift from value to tech happened in a heartbeat.

During that time, a remarkable thing has happened. Tech valuations have dropped by a third or more. Apple (AAPL) has fallen from 32X earnings to 23X against a current market multiple of 21X. Amazon (AMZN) shares are unchanged in a year, despite a meteoric 44% growth in sales, hiring 500,000 during the pandemic, and explosive growth in profits.

What was once growth is now value AND growth.

The technical damage in the bond market has been severe. Best case, rates chop sideways to lower for months. A 1.25% yield for the ten-year US Treasury bond is now screaming for attention. However, by the fall, I expect talk of Fed tapering to send the bond market back into its long-term bear trend.

So, when your trade of the century runs out, what do you do?

You find another trade of the century!

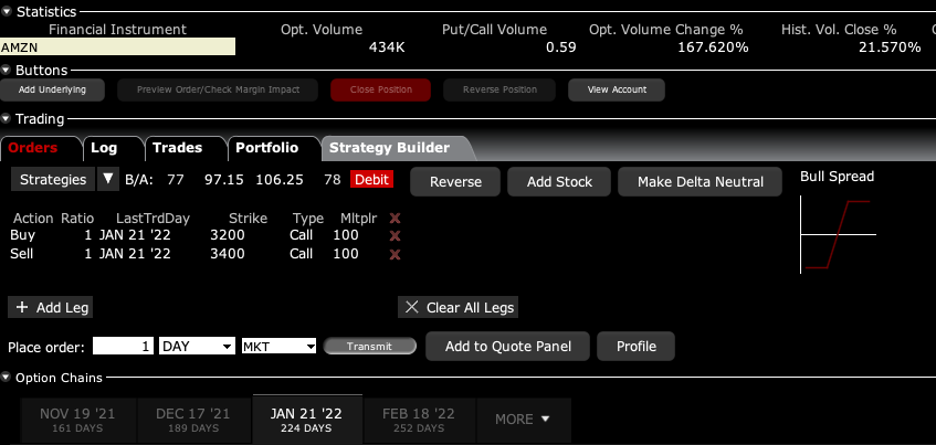

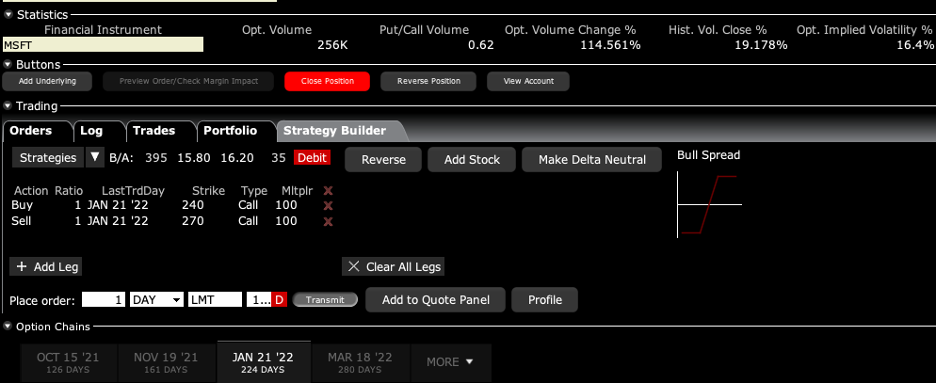

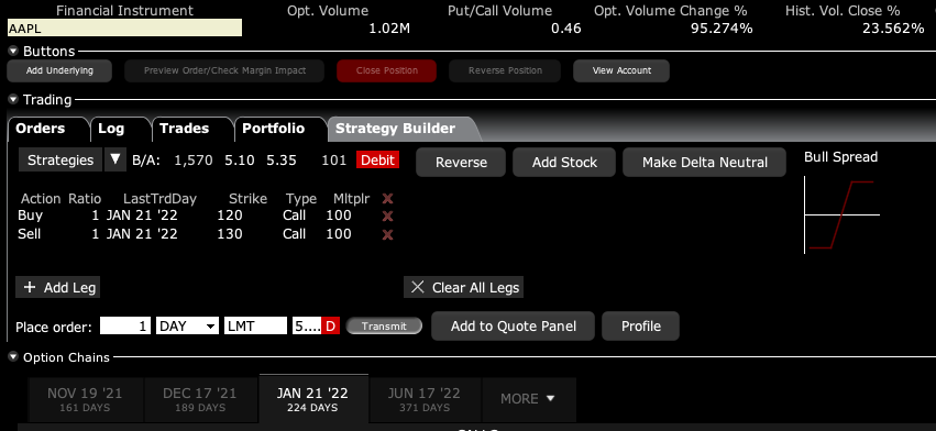

It just so happens I have such animals. I’ll give yxou three LEAPS, or Long-Term Equity Anticipation Securities to execute RIGHT NOW that should enable you to double your money by January 2022 with very low risk. They include the:

Amazon (AMZN) January 2022 $3,200-$3,400 vertical bull call spread

Microsoft (MSFT) January 2022 $240-$270 vertical bull call spread

Apple (AAPL) January 2022 $120-$130 vertical bull call spread

The liquidity for long-dated options is not that great. That is why entering limit orders in LEAPS only, as opposed to market orders, is crucial.

These are really for your buy-and-forget investment portfolio, defined benefit plan, 401k, or IRA.

Like all options contracts, LEAPS give its owner the right to exercise the option to buy or sell 100 shares of stock at a set price for a given time.

LEAPS have been around since 1990, and trade on the Chicago Board Options Exchange (CBOE).

To participate, you need an options account with a brokerage house, an easy process that mainly involves acknowledging the risk disclosures that no one ever reads.

If LEAPS expires "out-of-the-money" on expiration day, you can lose all the money you spent on the premium to buy it. There's no toughing it out waiting for a recovery, as with actual shares of stock. Poof, and your money is gone.

Note that a LEAPS owner does not vote proxies or receive dividends because the underlying stock is owned by the seller, or "writer," of the LEAPS contract until the LEAPS owner exercises.

Despite the Wild West image of options, LEAPS are actually ideal for the right type of conservative investor.

They offer vastly more margin and more efficient use of capital than traditional broker margin accounts. And you don’t have to pay the usurious interest rates that margin accounts usually charge.

And for a moderate increase in risk, they present hugely outsized profit opportunities.

For the right investor, they are the ideal instrument.

So, let’s get on with my specific math for the (AMZN) LEAPS to discover its inner beauty.

By now, you should all know what vertical bull call spreads are. If you don’t, then please click this link for my quickie video tutorial.

(you must be logged in to your account).

Warning: I have aged since I made this video.

Today, Amazon closed at $3,346.83.

The cautious investor should buy the (AMZN) January 2022 $3,200-$3,400 vertical bull call debit spread for $102. One contract gets you a $10,000 exposure. This is a bet that (AMZN) shares will close at $3,400 or higher by the January 22, 2022, option expiration, some 1.6% higher than here.

Sounds like a total no-brainer, doesn’t it?

Here are the specific trades you need to execute this position:

expiration date: January 21, 2022

Portfolio weighting: 10%

Number of Contracts = 1 contract

Buy 1 January 2022 (AMZN) $3,200 calls at…..…….………$374.00

Sell short 1 January 2022 (AMZN) $3,400 calls at…………$272.00

Net Cost:………………………….………..…….............…….….....$102.00

Potential Profit: $200.00 - $102.00 = $98.00

(1 X 100 X $98.00) = $9,800 or 150.00% in six months.

In other words, your $10,200 investment turned into $19,800 with an almost sure thing bet giving you a profit of 94.11%.

Why do a vertical bull call debit spread instead of just buying the January 2022 (AMZN) $3,400 calls outright?

You need a much bigger upside move to make money on this trade. (AMZN) would have to rise all the way to $3,674 to break even on the calls, and all the way up to $3,772 to match the profit of the call spread.

While I think it is possible that (AMZN) could rise that much by January, it is vastly more probable that (AMZN) will be over $3,400 by then. That is what hedge funds do all day long. Find the most probable trade out there and then leverage up like crazy.

Remember, one call option gives you the right to buy 100 shares. That means over $3,400 your call spread that cost $10,200 will enable you to control 100 shares of Amazon worth $340,000. The potential upside leverage over $3,400 is 33.33X!

By paying only $102 for the spread instead of $274.00 for an outright call only position, you can increase your size by 2.68 times, from 1 to 3 contracts for the same $10,200 commitment. That triples your upside leverage on the most probable move in (AMZN), the one above $3,400. That increase the upside leverage over $3,400 to an impressive 100X compared to the outright call buy.

How could this trade go wrong?

There is only one thing. We get a new variant on Covid-19 that overcomes the existing vaccines and brings a fourth wave in the pandemic.

In this case, (AMZN) doesn’t rise above $3,400 but crashes down to the $1,700 low we saw during the 2020 pandemic. We go back into recession. Both of the above positions go to zero. But if we get a fourth wave, you are going to have much bigger problems that your options positions.

So there it is. You pay you money and take your chances. That why the potential returns on these simple trades are so incredibly high.

Enjoy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more