Mad Hedge Technology Letter

August 19, 2024

Fiat Lux

Featured Trade:

(WHAT WILL PALANTIR STOCK DO FOR THE REST OF 2024?)

(PLTR)

Mad Hedge Technology Letter

August 19, 2024

Fiat Lux

Featured Trade:

(WHAT WILL PALANTIR STOCK DO FOR THE REST OF 2024?)

(PLTR)

Not all tech stocks are created equal.

Some have the power of connections from the beginning and that goes a long way to understand if a company can do what it takes to survive.

Very rarely do tech companies come out of nowhere and it is true that recognized venture capitalists help like rocket fuel.

Palantir (PLTR) was supported initially by tech insider billionaire Peter Thiel.

It’s not surprising that this is a company sitting deep at the intersection of strategic national intelligence and artificial intelligence.

The stock hit a low of $5 per share and now trades north of $32 per share.

Investors might easily understand this company as the war tech stock and co-founder and CEO Alex Karp is in no mood to apologize or be politically correct for its military, police, and U.S. Immigration and Customs Enforcement services despite facing massive backlash.

Karp acknowledged the company’s consistent pro-Western view despite polarizing views regarding the appeasement of Iran, Russia, and China.

Karp refused to apologize for defending the U.S. government on any issue and he has never wavered behind their principle of powering the U.S. government.

Karp stood out for his fierce criticism of Former US President Donald Trump, but he has said that he will work with both administrations.

Karp also maintained his pro-artificial intelligence stance, indispensable to preventing AI abuse.

In August, Palantir reported second-quarter revenue of $678.13 million, up 27% year-over-year, topping the analyst consensus of $652.1 million.

Palantir has been selling AI software for much longer than most of its competitors, which gives it a leg up on its competition. It started off as a software program intended for government use, with the simple concept of data in and insights out. This helped guide real-time decision-making by ensuring the people making the choices had the best possible information in front of them.

Still, government revenue makes up more than half of Palantir's total and rose at a 23% pace. It was powered by U.S. government revenue, which saw the highest demand since 2022.

No matter how you dice it up, Palantir's Q2 results were phenomenal. However, management thinks its growth may slow in Q3. Third-quarter revenue is expected to be about $699 million, indicating growth of 25%. While that's less than Q2's growth rate, management has consistently beaten its guidance.

My opinion about where the PLTR’s stock is going might surprise some people.

On one hand, the United States has the biggest military in the world and will covet and utilize PLTR’s software to continue to make real-time decisions in a national security sense.

On the other hand, the issue I have with PLTR is not with the quality of the business, but the price of their stock.

The stock has risen too fast too furiously in a short-amount of time.

The move from $5 per share to $32 took place over a 2.5-year time frame obviously boosted by global events in Eastern Europe and the Middle East.

For the rest of the year, I do think PLTR has a chance to blow past $40 per share and at that point, we will most likely reach the short-term high water mark of the stock.

The stock is due for a big sell-off once the AI frenzy cools down a little and that could be later this year.

Remember that the AI narrative has reignited in the short-term so it is smooth saying until the next road bump.

This is a complex company and with many of those, the trajectory of the stock can be many times more complicated.

“The superior man understands what is right; the inferior man understands what will sell.” – Said Chinese Philosopher Confucius

(THE JACKSON HOLE SYMPOSIUM WILL STEAL THE SPOTLIGHT THIS WEEK)

August 19, 2024

Hello everyone,

Week ahead calendar

2024 Democratic National Convention Aug. 19 - 22

2024 Jackson Hole Economic Policy Symposium Aug. 22 – 24

Monday Aug. 19

10 a.m. Leading Indicators (July)

9:30 p.m. Australia RBA Minutes

Earnings: Palo Alto Networks, Estee Lauder.

Tuesday Aug 20

8:30 a.m. Canada Inflation Rate

Previous: 2.7%

Forecast: 2.7%

Earnings: Lowe’s

Wednesday Aug 21

2 p.m. FOMC Minutes

Earnings: TJX Companies, Analog Devices, Target, Raymond James Financial.

Thursday Aug 22

8:30 a.m. Chicago Fed National Activity Index (July)

8:30 a.m. Continuing Jobless Claims (08/10)

8:30 a.m. Initial Claims (08/17)

9:45 a.m. PMI Composite preliminary (August)

9:45 a.m. Markit PMI Manufacturing preliminary (August)

9:45 a.m. Markit PMI Services preliminary (August)

10 a.m. Existing Home Sales (July)

11 a.m. Kansas City Fed Manufacturing Index (August)

7:30 p.m. Japan Inflation Rate

Previous: 2.8%

Forecast: 2.9%

Earnings: Intuit, Ross Stores

Friday Aug 23

8:00 a.m. Building Permits (July)

10 a.m. New Home Sales (July)

Later this week, we will be tuned into Jerome Powell’s speech at the Jackson Hole symposium. This speech comes just a few weeks after the July Fed meeting where he gave investors some confidence that a September rate cut was on the table. This confidence was built on “coded statements” from Powell, that appeared to say a lot, without saying anything decisive.

To further confuse investors about the Fed’s actions going forward, we were whipsawed by the Aug 2 non-farm payrolls data, and then the retail sales report and softer inflation data last week.

This week investors will also be able to examine the behaviour of the consumer as we have earnings results from retail chains, including Lowe’s and Target.

We can also pore over weekly continuing and initial unemployment claims data to gauge the temperature of the labour market.

Outside the U.S., attention will focus on inflation metrics, with significant data releases from Canada and Japan.

Goldman Sachs urges investors to “keep the faith” that the U.S. will avoid a recession…

My advice: be ready to take advantage of any volatility going forward. Scale into sold-off stocks and gradually build your positions.

MARKET UPDATE

S&P 500

The market rejected the recent low a couple of weeks ago very quickly. Is that the low? We can never be certain. If it is, then we have made an Elliott Wave 4 pattern low, which should now be followed by the market running up to new highs in the mid-5,700’s or toward 6000. (But don’t expect a straight lineup). Only once this Wave 5 is over, will the bullish sequence from the October 2022 low of 3,492 be complete. And this then leaves the market vulnerable to its biggest corrective sell-off since this bottom. The market will tell us where the top is in its Wave structure over the coming weeks/months.

GOLD

Gold has pierced the $2,500 level, and now seems set to rally to the mid $2,500’s and then $2,670. Support lies around $2,480-$2,450.

BITCOIN

Bitcoin is still undergoing a complex corrective structure. Support is still found in that band between $40k and $50k. We are looking for a sustained break above $60,000 to encourage advance toward the $70,000 level, enroute to the key $73,794 resistance.

QI CORNER

Elon Musk, Albert Einstein, Charlie Munger and many others are big believers in INVERSION THINKING.

What is it exactly?

Let’s throw some light on it by looking at some extracts from Alex Penunuri on X.

SOMETHING TO THINK ABOUT

Cheers,

Jacquie

Global Market Comments

August 19, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD or LESSONS LEARNED) plus (GLIDING INTO LITHUANIA),

(SPY), (GLD), (DHI), (TSLA), (JPM), (AAPL), (DHI), (LRCX)

After the worst week of the year, we get the best. If you are confused by all of this, so am I.

On the one hand, the downside was firmly rejected by the $8 trillion sitting under the market that has been trying unsuccessfully to get into the market all year. The upside was rejected as well and who knows why? Did it run too far, too fast? Did valuations get overblown? Or was it simply time to take a summer vacation?

Who knows? All three were true.

I don’t really care. I am up 2.67% in August and am 100% in cash. I’m waiting for the market to tell me what to do next. If we get another crash, I’ll buy. I’m selling the next melt-up as well. The only thing I’m really confident in is my 6,000 target for the S&P 500 by year-end which appears right on schedule.

London certainly has become the most internationally diverse city in the world. Last week my tablemates in pubs included two women from Japan who nearly fell out of their chairs when they heard me speak Japanese. A business consultant from Milan was visiting London for the first time. The head of international marketing for Industrial Light & Magic from Mill Valley, CA, filled me in on the latest developments in the digital arts.

Two Arabic-speaking ladies from Oxford University were working for a charity getting food into Gaza. One bartender was headed for Sandhurst, England’s West Point. The other was from China, and I had to explain to him what Bushmills was (it’s an Irish whiskey). Oh, and my barber was from Syria and my cleaning lady was from Barbados.

All seven of my languages were given a thorough workout. There are 56 countries in the British Commonwealth, and it seems like all of them are here at once.

This summer’s crash down, then up offered many lessons and I want to make sure you catch them all. Let every loss be a learning experience, lest you be doomed to repeat it. Of the 20 great single-day losses in the S&P 500 (SPX) since 1923, I have traded through nine. The other 11 took place in the aftermath of the 1929 crash where the market eventually dropped by 90%. But I had many friends who traded all of those. Click here for details.

For a start, it helps a lot if you see a crash coming. This market had been begging for a crash during May and June and I positioned accordingly. I went into the meltdown with nine short positions in July-August, which covered most of my losses. And I only ran positions into very short August 16 option expiration, thus greatly limiting damage incurred by the losers.

I limited losses by stopping out of out-of-the-money losers quickly in (CAT), (BRK/B), and (AMZN), right at the August 5 opening in most cases. I then became super aggressive when the Volatility Index ($VIX) hit $65, a 2-year high. I also went hyper-conservative by adding four technology positions very deep 20% in-the-money in (NVDA), (META), (TSLA), and (MSFT), which instantly became money makers.

I used the first 1,000-point rally to add a short position for a very long, thus neutralizing the portfolio at the middle of the recent range and taking in a lot of extra income.

I did ALL of this while traveling in England, Switzerland, Lithuania, Poland, Austria, and Slovakia, from assorted airport business lounges, hotels, and Airbnb’s. The travel actually helped because the New York market doesn’t open until 3:30 PM each day, giving me plenty of time to plan the day’s strategy.

Now all we have to do is figure out what the Volatility Crash ($VIX) from $65 to $14 in 9 days means, the fastest in history by a huge margin. It usually takes 170 days to make this kind of move. Could it mean that our lives are about to become boring beyond tears once again?

I doubt it.

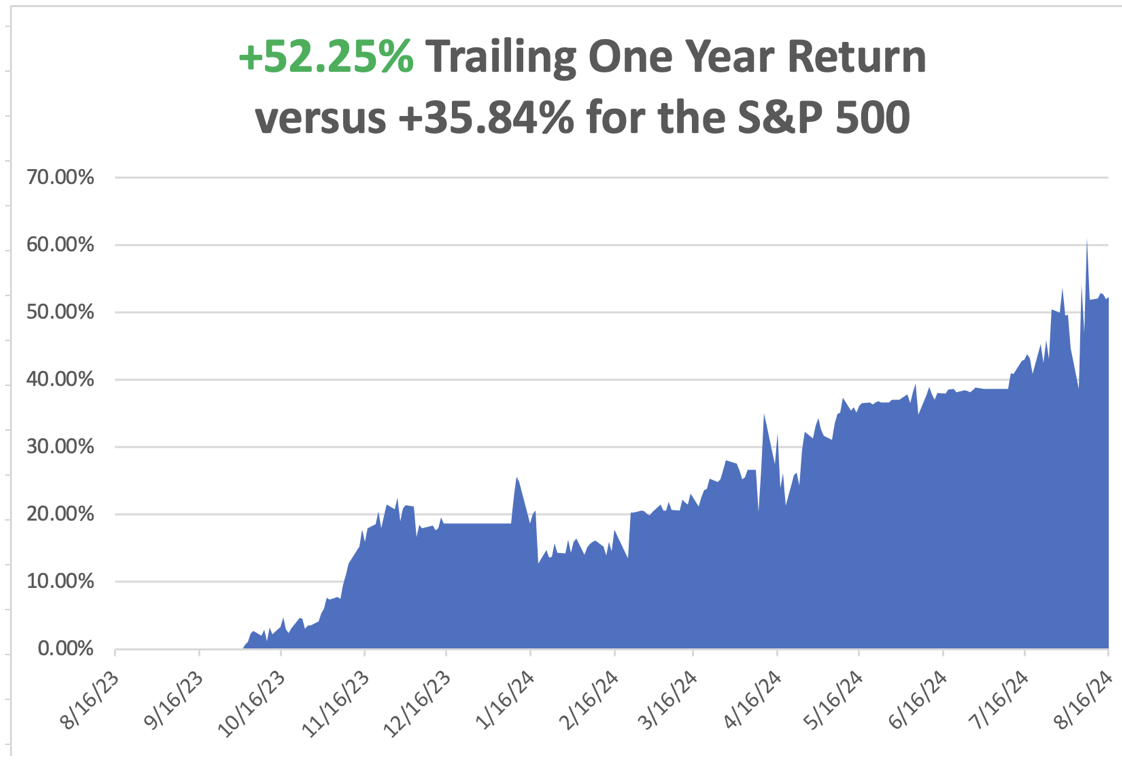

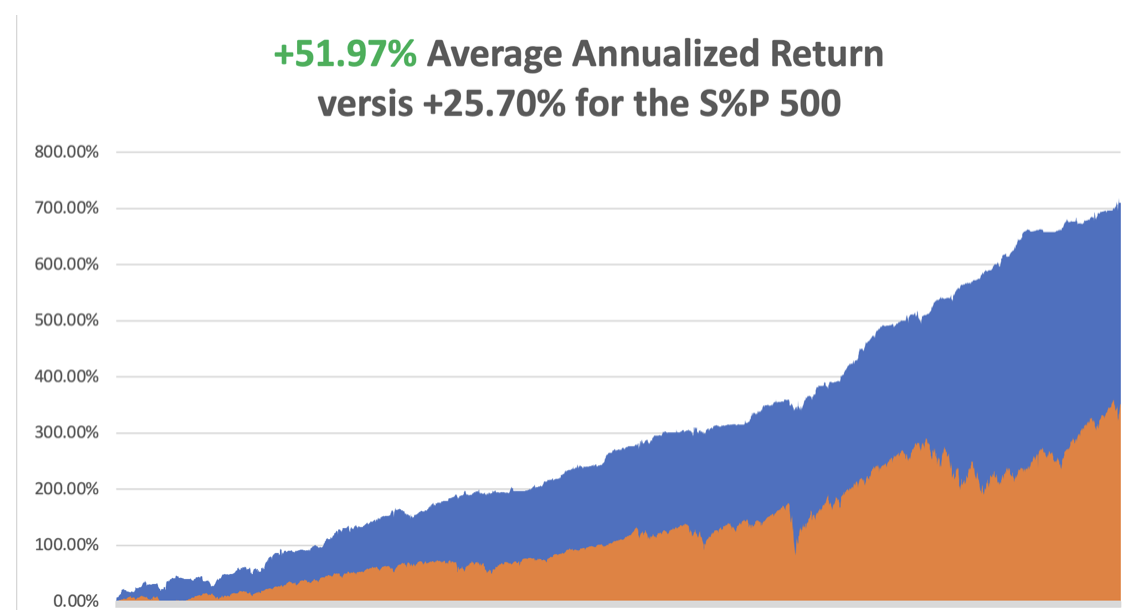

In July we ended up a stratospheric +10.92%. So far in August, we are up by +2.67%. My 2024 year-to-date performance is at +33.61%. The S&P 500 (SPY) is up +16.14% so far in 2024. My trailing one-year return reached +52.25.

That brings my 16-year total return to +710.24. My average annualized return has recovered to +51.97%.

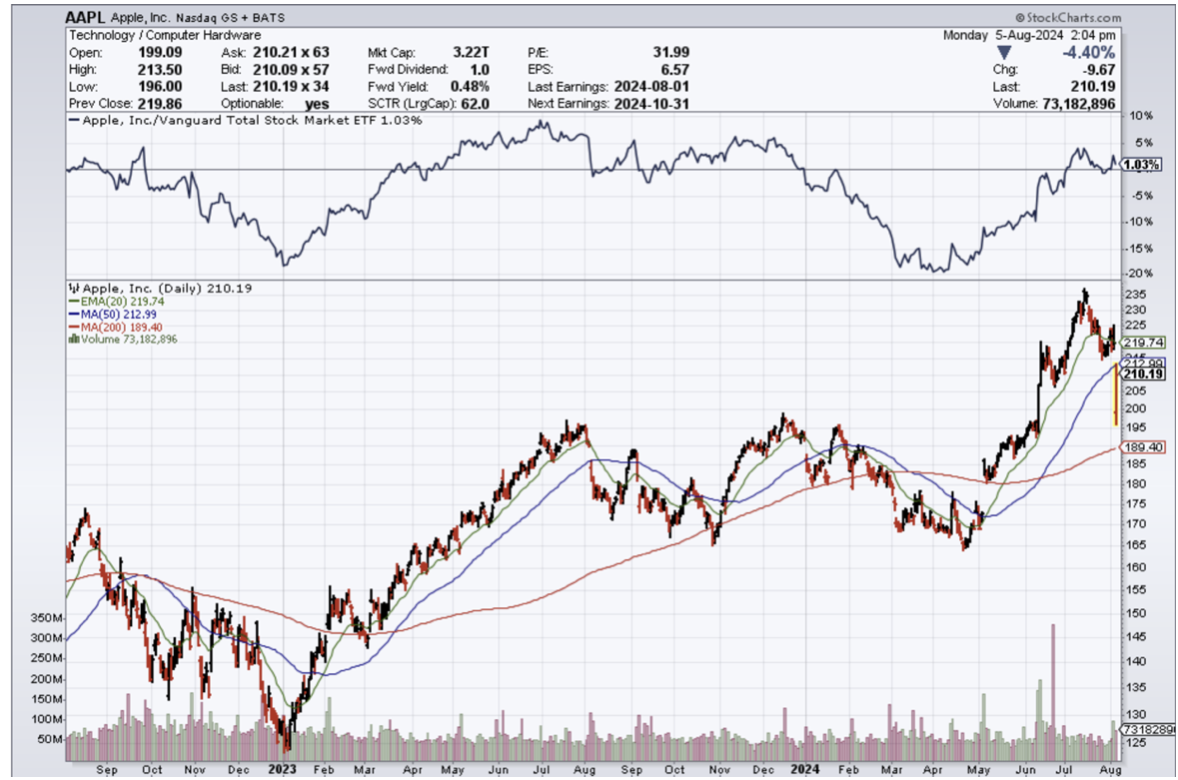

I spent the entire week taking profits. I cashed in on my longs in (GLD) and (DHI) and covered shorts in (TSLA), (JPM), (AAPL), and (DHI). I am now 100% in cash and boy does it feel good.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 49 of 66 trades have been profitable so far in 2024, and several of those losses were really break-even. That is a success rate of 74.24%.

Try beating that anywhere.

The “Soft Landing” is Back, or so says Goldman Sachs after the meteoric rise in share prices of the last ten days. The extreme concerns about the U.S. economy that have re-emerged over the past month appear overblown and investors shouldn’t get too defensive. The recent spike of market volatility had more to do with positioning than a real scare about economic growth and that investors should “keep the faith” that the U.S. avoids a recession, while also avoiding a revival in inflation.

Now it’s Volatility That’s Crashing, down a record 49 points from $65 to $16 in 9 trading days, suggesting that investors may be returning to strategies that bank on low stock volatility despite a near-meltdown in equities early this month. The ($VIX) long-term median level is $17.6. Similar reversions in the so-called fear gauge have, on average, taken 170 sessions to play out.

Consumer Price Index is a Snore, at 0.2% MOM and 2.9% YOY, below the long-term average. Ebbing inflation aligns with anecdotes from businesses that consumers are pushing back against high prices, through bargain hunting, cutting back on purchases, and trading down to lower-priced substitutes. Stock was a snore as well.

Consumer Sentiment Drops, to an eight-month low according to the University of Michigan. It was revised higher to 66.4 in July 2024 from a preliminary reading of 66.

The Yen Carry Trade is Back, with hedge funds piling back into positions they baled on only two weeks ago. It’s just a matter of math, now that the Bank of Japan has given up on raising interest rates anytime soon. What this means is more leverage, risk, and volatility for global financial markets. I love it!

New Home Construction Dives, in July to the lowest level since the aftermath of the pandemic as builders respond to weak demand that’s keeping inventory levels high. Total housing starts decreased 6.8% to a 1.2 million annualized rate last month, dragged down the biggest decline in single-family units since April 2020

Global EV Sales Jump 21% YOY, in July thanks to a large rise in China. In the European Union MG Motor, owned by China's SAIC Motor Corp, expects to be hit hardest by provisional imposed on EVs imported from China. Europe is not going to give away its core industry, especially Germany’s. EVs - whether fully electric (BEV) or plug-in hybrids (PHEV) - sold worldwide were at 1.35 million in July, of which 0.88 million were in China, where they were up 31% year-on-year.

Refi’s Rocket 35% in a Week, the result of falling inflation and a monster rally in the bond market. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) fell slightly to 6.54% from 6.55%. The refinance share of mortgage activity increased to 48.6% of total applications from 41.7% in the previous week

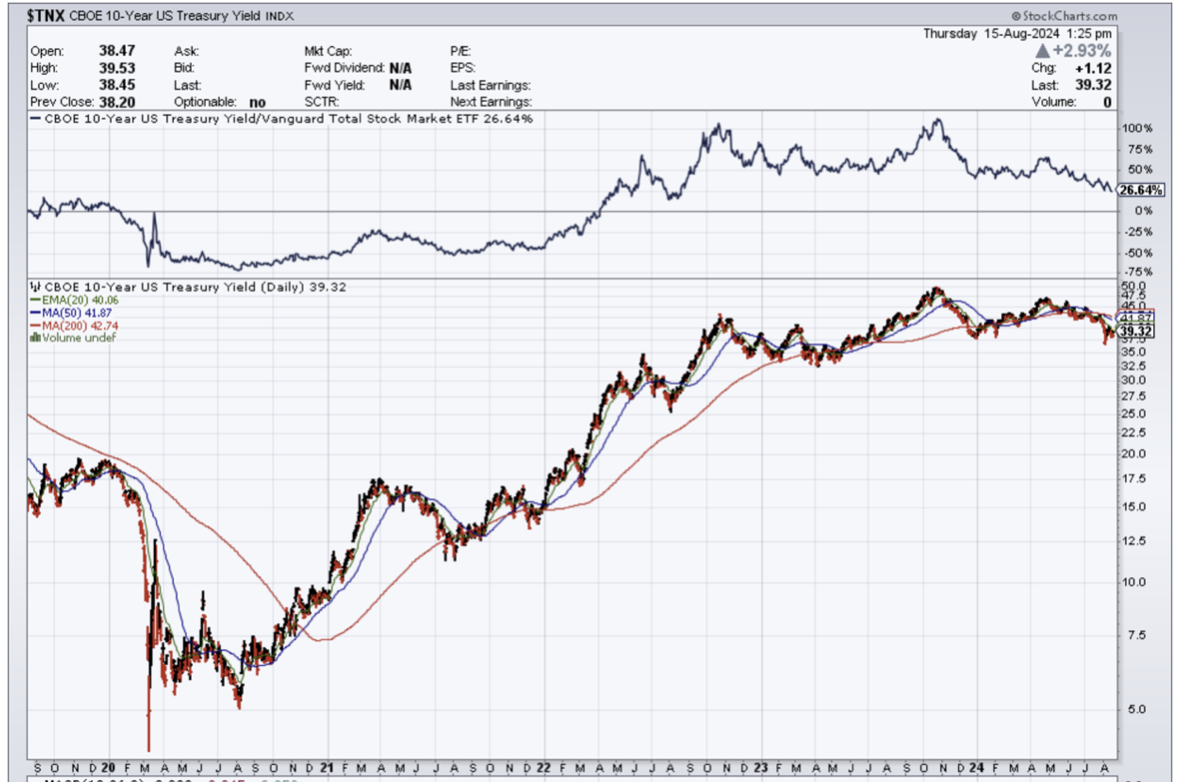

US Producer Price Index Fades, coming in at a weak 0.1%, and giving the interest rate cut crown a high five. Stocks took off like a scalded chimp. Treasury yields fell on Tuesday as wholesale inflation measures came in softer than expected. The yield on the ten-year US Treasury was lower by about 4 basis points at 3.867%.

Foreign Investors Pull Record Amount from China, $15 billion in Q2. Chinese firms invest a record $71 billion overseas at the same time. It’s why the Chinese yuan has been so weak. The glory days are never coming back. Avoid (FXI).

Weekly Jobless Claims totaled 227,000, a decrease of 7,000 from the previous week and lower than the estimate for 235,000.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, August 19 the Meeting of Central Bankers at Jackson Hole begins. Traders will peruse the tea leaves looking for clues about future interest rates policy. All the major countries of the world have already started cutting rates except the US.

On Tuesday, August 20 nothing of note is released.

On Wednesday, August 21 at 8:30 PM EST, the Minutes from the last FOMC meeting are released.

On Thursday, August 22 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, August 16 at 8:30 AM, Federal Reserve Chairman Jay Powell speaks. Also, New Home Sales are disclosed. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when a Concierge member invited me to spend a week in Lithuania, I jumped at the chance. I had never been to this miniscule country of 3 million, formerly a part of the Soviet Union. The last time I spent any appreciable amount of time in Eastern Europe was in 1968, at the height of the Cold War.

My friend grew up in the old USSR. He remembers as a child having to go to school in the snow wearing worn-out shoes repaired with duct tape because there weren’t any in the stores.

I remember the old Soviet Union and it was grim beyond belief. Standards of living were sacrificed for military spending in the extreme. I remember I swapped my Levi’s for a worn-out pair plus $50 because they were unobtainable.

My friend cashed in on the collapse of the Soviet Union and the mass privatizations that followed. As a trader in Gazprom shares, he made millions. Now he lives a life of leisure, taking occasional potshots at the market with my assistance. He has been with me since 2011.

Knowing I was an avid pilot he treated me to a day at the local glider club. Introduced as a Top Gun instructor who had flown everything from RAF Spitfires to F-18s, and whose grandfather had worked for Orville Wright, the club pilots were somewhat in awe. I was asked to sign logbooks, which is a great honor among pilots.

I donned my parachute with ease, and everyone relaxed. A tow plane took us up to 2,500 feet, we pulled the release from the cable and suddenly were floating over the endless green forests of Eastern Europe.

I took the stick and performed some light aerobatics, careful not to scare the daylights out of my co-pilot. The thing that really impresses you about gliders is the complete silence. No earplugs inside your headphones here, just the whooshing of the wind. We headed for the nearest clouds in search of uplifting thermals.

I was informed that birds knew more about thermals than any of us, and sure enough, we found a flock and followed them right in. We immediately picked up a few hundred feet, our electronic altimeter whining all the way.

Flying with the birds on a perfect day, how cool is that?

We could have stayed up for hours but I had a lunch appointment. So we yanked on the speed brakes and plummeted down towards the field. At 50 feet, wind shear hit us from the side and we fell like a ton of bricks, bouncing hard. My left elbow smashed against the side of the cockpit inflicting a big gash.

The glider club rushed the aircraft expecting the worst, but I gave them a thumbs up. Any landing you walk away from is a good landing. I later learned that the previous day another pilot broke both legs executing the same maneuver.

When the Soviet Union broke up in 1991, we thought it would take 100 years to integrate the former republics with the West. Although Lithuania is still one of the cheapest countries in Europe, the improvement in the standard of living has been enormous. Old Towns in Europe are usually prime real estate with the most expensive accommodation. Here it’s so cheap that you see a lot of young families with kids in strollers on the sidewalks and in the parks.

They have adopted our vices too, with elaborate tattoos commonplace and teenagers vaping on every street corner.

In the capital city of Vilnius, I developed a work schedule that was tolerable. I spent my mornings walking the Old Town, visiting palaces, castles, baroque churches, museums, and art galleries. Then when the New York Stock Exchange opened up at 4:30 PM I was at my computer banging out my trade alerts as fast as I could write them. The market closed at 11:00 PM. Thank goodness the bars were still open.

Of course, the language is a challenge. Usually, I can understand half of what is going on in Europe. But Lithuanian is a direct descendant of Sanskrit so I couldn’t understand a single word. Everyone under 40 speaks English so I was thankfully able to do my grocery shopping with some assistance.

Every year, I like to return to all my favorite countries, plus add one or two new ones. Where will next year’s new countries be? I’m already scheduled to visit Nicaragua, Columbia, Panama, Costa Rica, and Curacao before yearend. Estonia, Argentina, Latvia, Brazil, Tahiti, who knows?

Ask me in 2025.

To watch a short video of my Lithuanian glider flight, please click here.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

"The level of fact available from news services is way less than it once was," said Roger McNamee, co-founder of venture capital fund Elevation Partners.

The initial euphoria surrounding the artificial intelligence (AI) boom seems to be waning as of late, evidenced by the recent market performance of tech giants Alphabet, Amazon, and Microsoft. These companies, once the darlings of the AI trade, have seen their shares tumble over the past month, raising questions about the sustainability of the AI-driven market rally. This article delves into the factors behind this recent downturn, exploring the interplay of market sentiment, economic indicators, and industry-specific challenges.

Market Sentiment and the AI Hype Cycle

The AI market has been on a roller coaster ride, with investor sentiment oscillating between extreme optimism and cautious skepticism. The initial surge in AI-related stocks was fueled by a wave of hype surrounding the transformative potential of AI technologies. However, as the market matures, investors are becoming more discerning, demanding concrete evidence of profitability and sustainable growth. The recent market downturn suggests that the initial AI hype cycle may be peaking, with investors reassessing their expectations and adopting a more cautious approach.

The hype cycle is a common phenomenon in emerging technologies, characterized by a period of inflated expectations followed by a trough of disillusionment. The AI market appears to be entering this trough, as investors grapple with the realities of commercializing AI technologies and navigating the complexities of the regulatory landscape. The recent market downturn may be a necessary correction, forcing investors to adopt a more realistic perspective on the AI market's growth trajectory.

Economic Indicators and Investor Confidence

The broader economic landscape also plays a crucial role in shaping investor confidence and market sentiment. Rising interest rates, inflationary pressures, and geopolitical tensions can create a climate of uncertainty, prompting investors to seek safer havens for their capital. The recent market downturn coincides with a period of economic volatility, with concerns about a potential recession looming large. These macroeconomic factors may be contributing to the decline in AI-related stocks, as investors reassess their risk appetite and prioritize stability over growth potential.

Investor confidence is a fragile commodity, easily swayed by economic indicators and market trends. The recent downturn in AI-related stocks suggests that investor confidence may be waning, as concerns about the broader economic outlook overshadow the excitement surrounding AI technologies. This shift in sentiment may be a temporary phenomenon, or it may signal a more profound reassessment of the AI market's prospects.

Industry-Specific Challenges and Market Dynamics

The AI industry faces a unique set of challenges that can impact market dynamics and investor sentiment. These challenges include:

Regulatory scrutiny: The rapid advancement of AI technologies has raised concerns about ethical implications, data privacy, and potential misuse. Governments around the world are grappling with the complexities of regulating AI, with the potential for stricter regulations looming on the horizon. This regulatory uncertainty can create a climate of risk aversion, deterring investors from committing capital to AI-related ventures.

Talent shortage: The AI industry is experiencing a severe talent shortage, with demand for skilled AI professionals far outstripping supply. This talent gap can hinder innovation, slow down product development, and increase operational costs. The scarcity of AI talent may be a limiting factor in the growth of AI-related companies, impacting their market performance and investor appeal.

Competition and market saturation: The AI market is becoming increasingly crowded, with numerous players vying for market share. This intensified competition can lead to price wars, margin compression, and consolidation. The risk of market saturation may be a concern for investors, as it can limit the growth potential of individual companies and create a more challenging operating environment.

Technological hurdles: The development and deployment of AI technologies are fraught with technical challenges, including data quality issues, algorithmic bias, and scalability limitations. These hurdles can delay product launches, increase development costs, and impact the overall user experience. The complexities of AI technology may be a source of frustration for investors, who may be seeking more tangible evidence of progress and commercial viability.

The Future of the AI Trade: Opportunities and Challenges

Despite the recent market downturn, the AI trade is far from over. The long-term potential of AI technologies remains undeniable, with numerous applications across various industries. However, the path to realizing this potential is likely to be bumpy, with challenges and setbacks along the way.

Investors who remain committed to the AI trade must adopt a long-term perspective, focusing on companies with strong fundamentals, innovative technologies, and a clear path to profitability. It is also crucial to stay informed about regulatory developments, industry trends, and macroeconomic factors that can impact the AI market.

The AI trade may be losing its luster in the short term, but the long-term outlook remains bright. The companies that can navigate the challenges and capitalize on the opportunities presented by AI technologies are likely to emerge as the winners in this evolving market landscape.

Additional Insights and Considerations

Conclusion

The AI trade has undoubtedly lost some of its luster in recent weeks, as the market grapples with a confluence of factors, including shifting investor sentiment, economic uncertainty, and industry-specific challenges. However, the long-term potential of AI technologies remains undeniable, and the companies that can navigate the complexities of this evolving market are likely to emerge as the leaders of tomorrow. Investors who remain committed to the AI trade must adopt a long-term perspective, focus on fundamentals, and stay informed about the latest developments in this dynamic and rapidly changing field.

The AI revolution is far from over, and the opportunities for growth and innovation remain abundant for those who are willing to embrace the challenges and seize the moment.

Mad Hedge Technology Letter

August 16, 2024

Fiat Lux

Featured Trade:

(BIG RISKS TO TECH DISSIPATE)

($COMPQ), ($TNX), (FXY)

I don’t believe the tech sector is toast and it isn’t true to say that the burnt crust is the only part left over.

There is still vitality in it at the core of the tech sector ($COMPQ).

Granted, the trajectory left isn’t enough to propel tech stocks to a meteoric rise, but tech stocks should perform quite robustly in the run-up to the next earnings report.

So for all that are waiting for the bubble to burst – wait a little longer my friends.

In the meantime, let’s take a quick barometer of some of the outsized risks to big tech and ponder about the idea that outside or indirect events could possibly takedown tech shares.

China bailed the world out of the last three recessions and now they are a risk to drag down the rest of the world.

In each case, China's high growth and massive issuance of stimulus kick-started global expansion, and now that is gone with the wind.

China's model of economic development which worked so brilliantly in the boost phase, is now out of potency.

If American tech shares are sideswiped by global contagion, don’t bet on China to come bail out the radical overlords of Silicon Valley. China has its own problems and is entirely focused on that.

The era of zero-interest rates and unlimited government borrowing has ended. As Japan has shown, even at insane low rates ($TNX) of 1%, interest payments on skyrocketing government debt eventually consume virtually all tax revenues.

Japan was the black swan that could have cratered the tech market. Instead, it was a mild selloff yet manageable selloff creating a beautiful entry point for most of tech stocks.

Money is coming off the sideline to join in on a sharp rally into the U.S. presidential election so in the end the Japanese currency (FXY) risk was basically much-a-do-about-nothing.

At the start of the cycle, global debt levels (government and private sector) were low. Now they are high. The boost phase of debt expansion and debt-funded spending is over, and we're in the stagnation-decline phase where adding debt generates diminishing returns.

The era of low inflation has also ended for multiple reasons, but the tech shares have proven they can unequivocally march higher in an era of high inflation.

This is ironically due to tech being better positioned than other industries on a relative basis, because of their strong moats and iron-clad balance sheets.

The resilience in tech also echoes the idea that every company has become a tech company by integrating its products and revenue streams into daily business operations.

Tech productivity boom is hardly a one-off so as readers fret, please don’t think shares will magically drop to zero.

Dips are being bought and prices will go higher in the short term.

Economists were in awe in the early 1990s by the productivity stemming from the tremendous investments made in personal and corporate computers, a boom launched in the mid-1980s with Apple's (AAPL) Macintosh and desktop publishing, and Microsoft's Mac-clone Windows operating system.

By the mid-1990s, productivity continued to rise and the emergence of the Internet triggered the adoption of most of the population to get online and do business.

All the doomsday prophets who said high debt and high interest rates were the cocktails to finally stop tech stocks in their tracks got it completely wrong.

I am not saying debt and high interest rates are positive for equities, but tech has been able to skillfully navigate the headwinds with their excellent management skills and pivot towards leanness.

The buzz around AI holds still has a lot to prove, but the market is still celebrating its deflection of the Japanese yen carry trade.

I am not saying that tech shares will never have to confront anything that can drag them down meaningfully, but many of the high risks have either been postponed or dealt with.

We are in a position where tech should steamroll into the end of the year barring some type of crazy event.