“If something's important enough, you should try. Even if - the probable outcome is failure.” – Said Elon Musk

“If something's important enough, you should try. Even if - the probable outcome is failure.” – Said Elon Musk

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

(THE RETAIL INVESTOR IS BUYING THE DIP)

March 28, 2025

Hello everyone

The buy-the-dip mentality is still strong among the retail investing crowd, even though markets have been spooked by the Trump administration trade war and the growing risk of a recession.

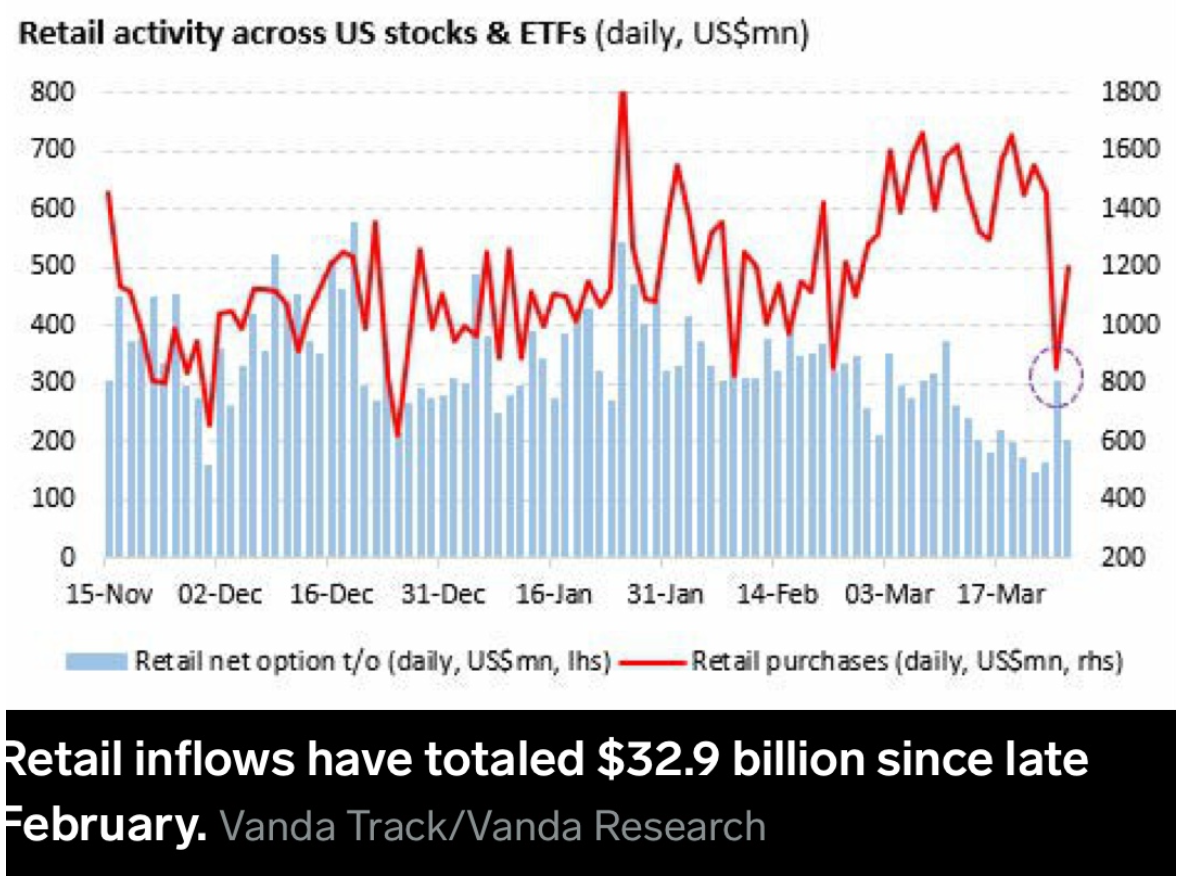

Individual investors have invested $32.9 billion into stocks since late February, according to Vanda Research.

Retail Investors have been buying the dip mostly in mega-cap tech names and among chip stocks.

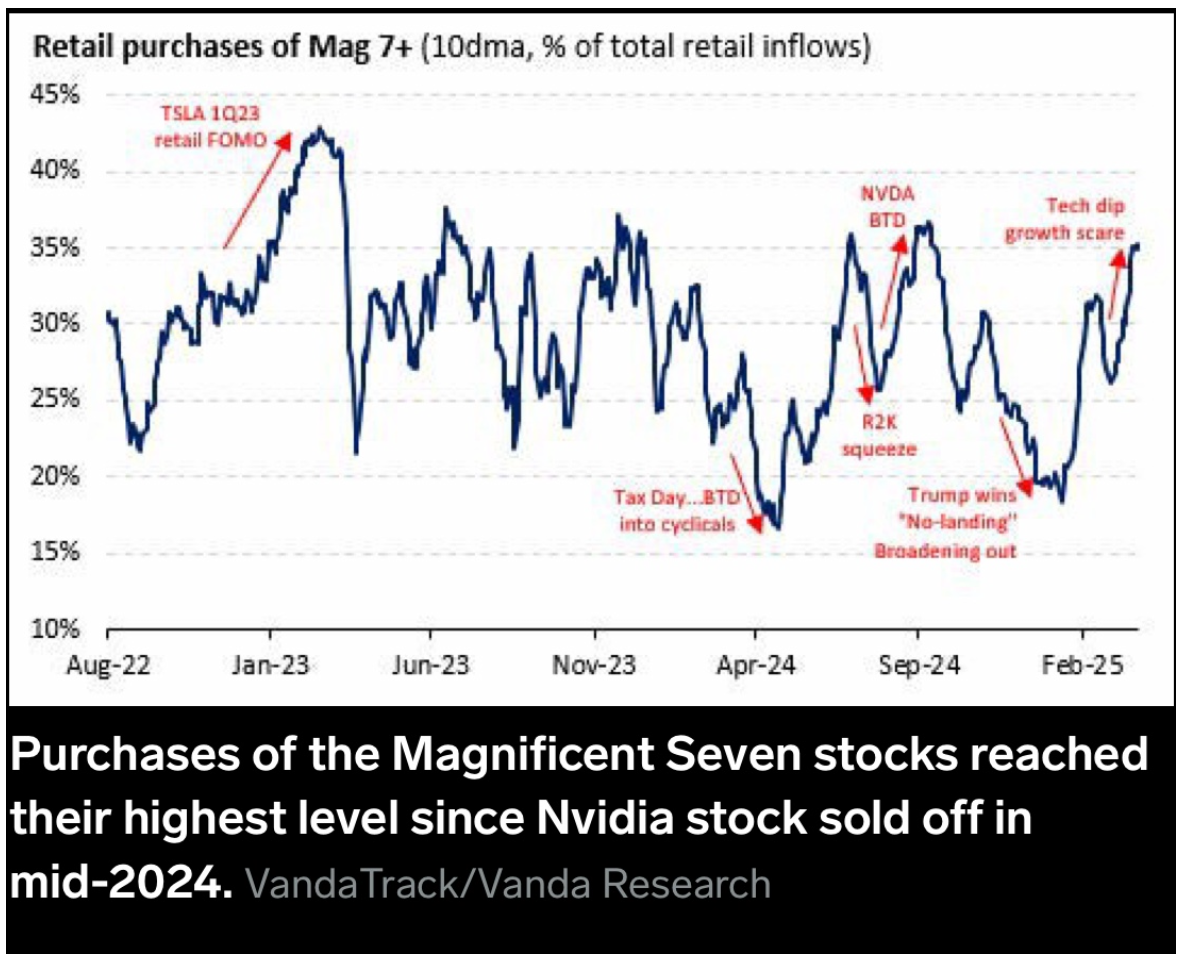

The 10-day moving average of retail flows into the Magnificent Seven stocks climbed to its highest level since mid-2024 when investors bought the dip as Nvidia shares declined 30% from a peak of $135 a share last June.

Nvidia remained the most popular retail stock, with net flows reaching 1.39 billion in the last five trading days. Nvidia shares are down 18% year-to-date.

Tesla was the second-most popular stock among retail investors, who bought a net $811 million worth of shares in the last five trading days. The stock is down 28% year-to-date.

Palantir (PLTR), Amazon (AMZN), and Advanced Micro Devices (AMD) were also among the top five most popular retail stocks in the last week, with investors pouring in a net $417 million in the three companies.

The jitters on Wall Street are not discouraging retail investors from buying the dip. That’s even despite growing concern over the impact Trump’s trade war may have on the economy and the potential for the U.S. to enter a recession later this year. (The U.S. is probably already in recession – but hard data will only confirm that later this year).

Citi and HSBC downgraded their ratings for the US stock market this month, citing growth concerns in the US. Meanwhile, Goldman Sachs, RBC, and Barclays have also trimmed their price targets for the S&P500.

It seems that the retail investor has grown numb to hard data, or should I say they have grown a rhino hide in response to the hard data being thrown at them.

To be still buying this market when consumer confidence declined for a fourth straight month in March, and expectations for income, business activity, and the job market declined to a 12-year low, reveals a truly blaze attitude.

Retail investors have probably been taught to lean into the fear and buy anyway.

And this is why this bear market will probably end up looking like an expanding triangle. Example provided here.

Retail investors return to the market after the first drop and buy heartily, not concerned at all about any future drops in the market. Then a second fall happens, and the retail investor once again picks up the pieces and buys again, and the market rallies. However, it might be the third big drop that really sets the heart pounding and makes them think twice about buying again. Have they been taken in by a buying the dip mentality, without question?

I think so.

QI CORNER

Take care.

Be well.

Cheers

Jacquie

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Biotech and Healthcare Letter

March 27, 2025

Fiat Lux

Featured Trade:

(NO SHERPA REQUIRED)

(MRK), (BMY)

Perched high above the timberline on Colorado's Mt. Elbert last weekend, I found myself short on oxygen and long on questions—namely, which pharmaceutical heavyweight deserves a spot in my portfolio: Merck (MRK) or Bristol-Myers Squibb (BMY)?

At 14,438 feet, the air thins out fast, but the thinking gets clearer. Clarity tends to arrive when your brain’s running at 60% capacity.

I’d stuffed my pack with company reports, earnings transcripts, and a few too many granola bars—one of which was being stalked by a very persistent marmot as I paused to catch my breath. I must’ve looked like an underprepared Everest hopeful, hunched over charts and trying to find altitude-adjusted alpha.

On paper, both firms dominate the oncology space and have made a career out of telling cancer where to shove it. But markets don’t care about reputations—they care about margins, pipelines, and who's going to make it through the next patent cliff without blowing out their kneecaps.

Let’s start with the money.

Merck posted Q4 2024 revenue of $17.76 billion, up 6.77% year-on-year. Its price-to-sales ratio sits at 3.74x—above the sector median, but still 14.7% cheaper than its own five-year average. It’s also beaten revenue expectations for 12 straight quarters. That’s not a hot streak. That’s clinical precision.

Bristol-Myers pulled in $12.34 billion last quarter with 7.5% YoY growth, but it trades at a much lower 2.51x P/S. That’s a discount—16.5% under the sector median. Ten out of twelve quarters beating the Street is nothing to sneeze at either. You get the sense both firms have their accounting departments on creatine.

Debt? Merck sits on $24.6 billion in net debt, but with a net debt/EBITDA ratio of 0.84x, it's practically sipping debt through a paper straw. Bristol-Myers, on the other hand, carries $40.1 billion with a 2.07x ratio. Still manageable, but not the kind of leverage that makes you sleep like a baby—unless you're the baby in question.

Dividends? Bristol-Myers pays more—4.14% vs. Merck’s 3.42%. That might earn it a second glance from income hawks, but when you zoom out, Merck still wears the financial crown.

Now here’s where things get messier.

Merck has a bit of a single-product addiction problem. Keytruda brought in $7.83 billion last quarter, making up a jaw-dropping 50.2% of total revenue. It's a blockbuster, yes, but when one drug makes up half your business, you start looking like a biotech version of Jenga. Merck’s top five products represent 75.7% of sales.

Bristol-Myers shows better balance. Eliquis is its biggest hitter, pulling in 25.9%, while its top five products account for 71.6% overall. Not exactly ironclad diversification, but a more even spread than Merck’s lineup.

Still, Keytruda is a monster. It outsold Bristol’s Opdivo by a whopping $5.4 billion in Q4 alone. That’s not a competition—that’s a beatdown. But both companies are running out the clock on their oncology flagships. Keytruda loses U.S. patent protection in 2028. Merck’s answer is a subcutaneous version—MK-3475A—patent-protected until 2039. Bristol’s already fired back with Opdivo Qvantig, a smart preemptive strike that could buy them time and market share.

Pipelines? Merck leads here too. BMY has 74 active R&D projects, 11 in Phase 3. Merck? Over 90 clinical-stage assets, 31 of them in Phase 3, and five are already under regulatory review. They’re not just defending Keytruda—they’re building the next dynasty.

Meanwhile, Bristol-Myers’ stock is flashing overbought signals like a Christmas tree. Merck, by contrast, trades below its VWAP, and Wall Street sees an 18.3% upside from here. Bristol-Myers? A yawn-worthy 1.36%. That's a rounding error, not an investment thesis.

Fast forward to 2029. I expect Merck to print a non-GAAP EPS of $11, led by Keytruda, Welireg, and a few wild cards currently in late-stage trials. Bristol-Myers might reach $6.80 EPS on $44 billion in revenue. Not bad, just... not Merck.

After sorting through this on the summit—between water breaks, altitude headaches, and one increasingly assertive marmot—the picture came into focus. Merck is the better long-term pick. They’ve got the product, the pipeline, the margin, and the momentum.

As I packed up and started the long descent, I dropped my guard for half a second and the marmot made his move—snatched my energy bar right off my pack. Bold little bastard. But honestly, he earned it.

Sometimes, the one who climbs higher sees further and waits patiently gets the prize. Merck just did all three.

After all, in investing—as in mountain climbing—peaks and profits favour those who don’t lose their breath or their nerve.

Global Market Comments

March 27, 2025

Fiat Lux

Featured Trade:

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL)

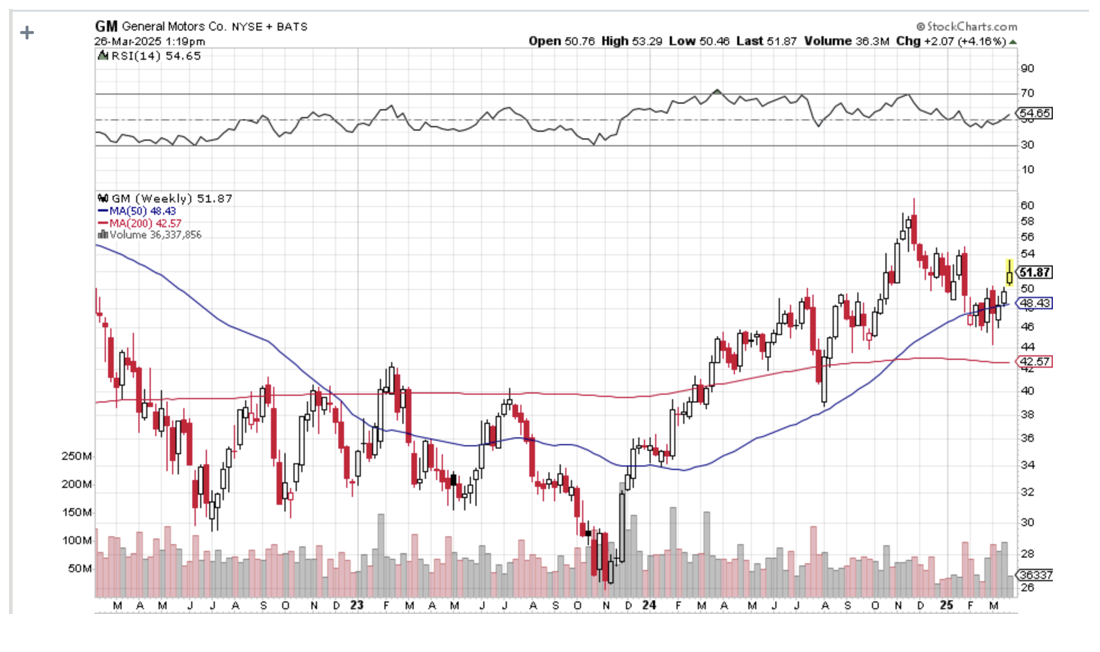

One of the most fascinating things I learned when I first joined the equity trading desk at Morgan Stanley during the early 1980s was how to parallel trade.

A customer order would come in to buy a million shares of General Motors (GM), and what did the in-house proprietary trading book do immediately?

It loaded the boat with the shares of Ford Motors (F).

When I asked about this tactic, I was taken away to a quiet corner of the office and read the riot act.

“This is how you legally front-run a customer,” I was told.

Buy (GM) in front of a customer order, and you will find yourself in Sing Sing shortly.

Ford (F), Toyota (TM), Nissan (NSANY), Daimler Benz (DDAIF), BMW (BMWYY), and Volkswagen (VWAPY), were all fair game.

The logic here was very simple.

Perhaps the client completed an exhaustive piece of research concluding that (GM) earnings were about to rise.

Or maybe a client's old boy network picked up some valuable insider information.

(GM) doesn’t do business in isolation. It has thousands of parts suppliers for a start. While whatever is good for (GM) is good for America, it is GREAT for the auto industry.

So through buying (F) on the back of a (GM) might not only match the (GM) share performance, it might even exceed it.

This is known as a Primary Parallel Trade.

This understanding led me on a lifelong quest to understand Cross Asset Class Correlations, which continues to this day.

Whenever you buy one thing, you buy another related thing as well, which might do considerably better.

I eventually made friends with a senior trader at Salomon Brothers while they were attempting to recruit me to run their Japanese desk.

I asked if this kind of legal front-running happened on their desk.

“Absolutely,” he responded. But he then took Cross Asset Class Correlations to a whole new level for me.

Not only did Salomon’s buy (F) in that situation, they also bought palladium (PALL).

I was puzzled. Why palladium?

Because palladium is the principal metal used in catalytic converters, it removes toxic emissions from car exhaust and has been required for every U.S.-manufactured car since 1975.

Lots of car sales, which the (GM) buying implied, ALSO meant lots of palladium buying.

And here’s the sweetener.

Palladium trading is relatively illiquid.

So, if you catch a surge in the price of this white metal, you would earn a multiple of what you would make on your boring old parallel (F) trade.

This is known in the trade as a Secondary Parallel Trade.

A few months later, Morgan Stanley sent me to an investment conference to represent the firm.

I was having lunch with a trader at Goldman Sachs (GS) who would later become a famous hedge fund manager, and asked him about the (GM)-(F)-(PALL) trade.

He said I would be an IDIOT not to take advantage of such correlations. Then he one-upped me.

You can do a Tertiary Parallel Trade here by buying mining equipment companies such as Caterpillar (CAT), Cummins (CMI), and Komatsu (KMTUY).

Since this guy was one of the smartest traders I ever ran into, I asked him if there was such a thing as a Quaternary Parallel Trade.

He answered “Abso******lutely,” as was his way.

But the first thing he always did when searching for Quaternary Parallel Trades would be to buy the country ETF for the world’s largest supplier of the commodity in question.

In the case of palladium, that would be South Africa (EZA).

Since then, I have discovered hundreds of what I call Parallel Trading Chains and have been actively making money off of them. So have you, you just haven’t realized it yet.

I could go on and on.

If you ever become puzzled or confused about a trade alert I am sending out (Why on earth is he doing THAT?), there is often a parallel trade in play.

Do this for decades as I have and you learn that some parallel trades break down and die. The cross relationships no longer function.

The best example I can think of is the photography/silver connection. When the photography business was booming, silver prices rose smartly.

Digital photography wiped out this trade, and silver-based film development is still only used by a handful of professionals and hobbyists.

Oh, and Eastman Kodak (KODK) went bankrupt in 2012.

However, it seems that whenever one Parallel Trading Chain disappears, many more replace it.

You could build chains a mile long simply based on how well Apple (AAPL) or NVIDIA (NVDA) is doing.

And guess what? There is a new parallel trade in silver developing. Whenever someone builds a solar panel anywhere in the world, they use a small amount of silver for the wiring. Build several tens of millions of solar panels and that can add up to quite a lot of silver.

What goes around comes around.

Suffice it to say that parallel trading is an incredibly useful trading strategy.

Ignore it at your peril.

“Cheap is a dangerous word,” said technical analyst Carter Braxton Worth.

Washington D.C. - A seismic shift is underway in the landscape of financial regulation, as burgeoning calls for the deregulation of artificial intelligence (AI) within the sector gain momentum. While proponents tout the potential for innovation and efficiency, a growing chorus of experts warns that unchecked AI deployment could unleash unprecedented volatility and systemic risk upon global financial markets.

The debate, which has intensified following recent policy shifts, centers on the balance between fostering technological advancement and safeguarding the stability of the financial system. Critics argue that the rapid evolution of AI, coupled with insufficient regulatory oversight, creates a fertile ground for market manipulation, algorithmic flash crashes, and a potential erosion of market integrity.

The Deregulation Drive:

The push for AI deregulation is fueled by several factors. Firstly, the financial industry's embrace of AI has accelerated dramatically, with algorithms now playing a crucial role in everything from high-frequency trading to risk assessment and portfolio management. Advocates claim that stringent regulations stifle innovation and hinder the United States' ability to compete in the global AI race.

Secondly, a prevailing sentiment within certain political circles emphasizes minimizing government intervention in the market, viewing regulation as an impediment to economic growth. This ideology, combined with powerful lobbying efforts from tech and financial firms, has created a political climate conducive to deregulation.

"We must unleash the transformative power of AI to drive economic prosperity," argues a prominent industry lobbyist, speaking on condition of anonymity. "Excessive regulation will only serve to hamstring our financial institutions and cede our competitive advantage to nations with more permissive regulatory environments."

However, this perspective is met with fierce opposition from regulators, academics, and consumer advocacy groups, who express deep concerns about the potential consequences of unfettered AI deployment.

The Shadow of Algorithmic Risk:

One of the most pressing concerns revolves around the inherent complexity and opacity of AI algorithms. "These systems are often black boxes," explains Dr. Eleanor Vance, a leading expert in financial risk management. "We don't always fully understand how they arrive at their decisions, which makes it incredibly difficult to anticipate or mitigate potential risks."

This lack of transparency poses a significant challenge for regulators, who are tasked with ensuring market fairness and stability. The potential for algorithmic bias, where AI systems perpetuate or amplify existing inequalities, further complicates the regulatory landscape.

Furthermore, the interconnectedness of AI systems within the financial ecosystem creates the potential for cascading failures. A single algorithmic error or malicious attack could trigger a chain reaction, leading to widespread market disruption and systemic risk.

"We've already seen instances of algorithmic flash crashes, where automated trading systems triggered rapid and dramatic price swings," warns a senior regulatory official. "Without proper safeguards, these events could become far more frequent and severe."

Concerns of Market Manipulation:

The potential for AI-powered market manipulation is another major source of concern. Sophisticated algorithms could be used to exploit market vulnerabilities, engage in predatory trading practices, or spread misinformation to manipulate asset prices.

"Imagine an AI system designed to detect and exploit subtle patterns in market data, allowing it to front-run trades or manipulate prices with unprecedented precision," says a cybersecurity expert specializing in financial systems. "The potential for abuse is immense."

The proliferation of deepfakes and AI-generated misinformation further exacerbates these concerns. Malicious actors could use these technologies to spread false rumors or manipulate market sentiment, creating artificial volatility and profiting from the resulting chaos.

The Regulatory Void:

The current regulatory framework is ill-equipped to address the unique challenges posed by AI. Existing regulations, designed for traditional financial instruments and trading practices, are often inadequate for overseeing complex algorithmic systems.

"We're facing a regulatory gap," admits a financial regulator. "The pace of technological innovation has outstripped our ability to develop effective oversight mechanisms."

The development of new regulatory frameworks is further complicated by the lack of consensus on best practices and ethical guidelines for AI deployment in finance. International cooperation is also crucial, as financial markets are increasingly interconnected, and regulatory arbitrage could lead to a race to the bottom.

The Social and Economic Implications:

The potential consequences of AI-driven market instability extend far beyond the financial sector. A major market crash could trigger a global economic recession, leading to widespread job losses, social unrest, and a loss of public trust in the financial system.

Furthermore, the increasing reliance on AI in financial decision-making raises concerns about algorithmic bias and discrimination. AI systems could perpetuate existing inequalities, denying access to credit or investment opportunities to marginalized communities.

"We need to consider the social and ethical implications of AI deployment in finance," emphasizes a social justice advocate. "These systems should be designed to promote fairness and equity, not to exacerbate existing disparities."

The Call for Responsible Innovation:

Despite the risks, many experts believe that AI has the potential to revolutionize the financial industry, improving efficiency, reducing costs, and expanding access to financial services. However, they stress the need for responsible innovation, guided by robust regulatory oversight and ethical principles.

"We need to strike a balance between fostering innovation and mitigating risk," argues a financial technology expert. "This requires a collaborative effort between regulators, industry leaders, and academic researchers."

Key recommendations include:

The Future of Finance:

The future of finance hinges on our ability to navigate the complex challenges posed by AI. A failure to establish robust regulatory safeguards could lead to a period of unprecedented market volatility and systemic risk, with potentially devastating consequences for the global economy.

However, if we can embrace responsible innovation, guided by ethical principles and robust oversight, AI has the potential to transform the financial industry for the better, creating a more efficient, inclusive, and resilient financial system.

The coming years will be critical in determining whether we can harness the power of AI for the benefit of society, or whether we succumb to the algorithmic abyss.