“Artificial Intelligence will be beneficial for us if it doesn’t kill us first, said Senator John Kennedy of Louisiana.

“Artificial Intelligence will be beneficial for us if it doesn’t kill us first, said Senator John Kennedy of Louisiana.

Mad Hedge Biotech and Healthcare Letter

June 3, 2025

Fiat Lux

Featured Trade:

(WHEN BIG PHARMA DREAMS GO UP IN SMOKE)

(SNY), (REGN), (AAPL)

Last week, I got a call from an old friend who runs a biotech fund. “Did you see what happened to Sanofi?” he asked, his voice carrying that particular mix of schadenfreude and genuine concern that only comes from watching a $3 billion drug prospect implode in real time.

He was talking about itepekimab, Sanofi’s (SNY) partnership with Regeneron (REGN) that just face-planted harder than a tourist trying to navigate Lombard Street in a rental car.

The drug was supposed to be the heir apparent to Dupixent, their $14 billion blockbuster that’s keeping the lights on at both companies.

Instead, it delivered results so inconsistent that even the most optimistic Wall Street analysts are now treating it like yesterday’s sushi – something you definitely don’t want to touch.

Here’s what happened, and why it matters more than you might think for anyone with skin in the biotech game.

Itepekimab targets IL-33, a key inflammatory marker in COPD – that’s chronic obstructive pulmonary disease for those keeping score at home.

The companies ran two similarly designed Phase 3 trials, AERIFY-1 and AERIFY-2, each enrolling around 1,000 patients.

Both compared the drug to placebo over 52 weeks, measuring whether it could reduce COPD flare-ups. Simple enough concept, right?

Wrong.

The results revealed that AERIFY-1 showed a 27% reduction in exacerbations with the bi-weekly dose and 21% with the monthly dose – statistically significant and clinically meaningful, the kind of numbers that make CFOs start planning yacht upgrades.

And AERIFY-2? A pathetic 2% and 12% respectively, missing statistical significance by a country mile.

When your drug works brilliantly in one trial and barely moves the needle in another, that’s not a minor hiccup – that’s a fundamental problem that no amount of creative PowerPoint slides can fix.

Now, some apologists are pointing to lower-than-expected event rates during the pandemic, when social distancing theoretically reduced respiratory infections.

That’s a nice theory, but the FDA doesn’t accept excuses with Biological License Applications any more than my tax accountant accepts “the dog ate my receipts.”

More troubling, the data showed itepekimab’s efficacy seemed to wear off over time in both studies.

For a chronic disease requiring long-term treatment, that’s about as useful as a chocolate teapot or a Ferrari in Manhattan traffic.

Before this debacle, analysts were projecting $3 billion in peak annual revenue for itepekimab.

The market’s response tells you everything about those projections now – both Sanofi and Regeneron got hammered. When you promise the moon and deliver green cheese, investors tend to remember.

But here’s where it gets interesting from an investment perspective, and why I’m not writing off this French pharmaceutical giant just yet.

Despite this setback, my DCF analysis suggests Sanofi is trading at a 12% discount to fair value.

The market is pricing the stock for growth of just 1.2%, which seems overly pessimistic even accounting for the itepekimab failure.

That’s the kind of pessimism usually reserved for companies facing bankruptcy, not ones sitting on a $14 billion revenue stream.

The reality is that Sanofi remains heavily dependent on Dupixent, which generated over $14 billion in revenue last year – nearly a third of total company sales. That concentration is both a blessing and a curse, like having all your money in Apple (AAPL) stock in 2007.

Dupixent is still showing 23.8% year-over-year growth following its COPD approval, and it’s safe until patent expiration in the early 2030s.

But relying so heavily on one product makes every pipeline failure sting that much more, especially when you’re supposed to be a diversified pharmaceutical powerhouse.

Looking at the broader metrics, Sanofi can still be diplomatically called “challenged quality biopharma.”

Revenue growth has stalled at an anemic 0.1% CAGR, though gross margins have recovered to a respectable 70.2%.

The company’s spending 16.7% of revenue on R&D, which is adequate but not impressive for a company supposedly focused on innovation.

For context, that’s like a tech company spending pocket change on software development and wondering why their products feel dated.

The patent cliff looming for Dupixent creates an interesting dynamic that reminds me of watching a slow-motion train wreck.

Sanofi needs to replace that $14 billion revenue stream within the next decade, but their track record on major pipeline successes has been spotty.

Legacy products like Lantus insulin are already facing biosimilar competition and price erosion, making the company increasingly dependent on that single golden goose.

But the actual key question isn’t whether Sanofi will face challenges – it will, just like every other pharmaceutical company trying to replace blockbuster drugs. The question is whether those challenges are fully reflected in the current valuation.

Using conservative assumptions of 3% revenue growth and 15% FCF margin, the answer is yes. The market has already priced in the potential failure of the company’s pipeline candidates.

Still, it’s not prudent to write off Sanfi just yet. For biotech investors willing to bet on a pharmaceutical giant potentially exceeding rock-bottom expectations, this company offers an intriguing risk-reward profile that’s hard to ignore.

Just don’t expect any more miracle drugs to emerge from their labs anytime soon – those days appear to be behind them, filed away with their glory years like old photographs in a dusty album.

Besides, in the biotech world, sometimes the best cure for disappointment is a good discount.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

June 3, 2025

Fiat Lux

Featured Trade:

(LOOKING AT THE LARGE NUMBERS)

(TLT), (TBT) (BITCOIN), (MSTR), (BLOK), (HUT)

I friend of mine asked me what the Global Money supply was.

I just so happen to know that number. It is around $100 trillion. That includes the world’s total M2 money supply, all the physical cash in circulation, plus deposits, promissory notes, and other liquid money instruments.

Writing for The Economist magazine in London for ten years, I still constantly update these numbers in my mind. This, after all, is the air we breathe and the language we speak.

Then it occurred to me that most people don’t know these mega numbers, so I thought I would give you a basic primer and some conclusions.

Enjoy.

$1 quadrillion – the value of all assets in the world, both financial and physical

$100 trillion – Global money supply

$150 trillion – the value of all global bonds and fixed income securities

$100 trillion – value of global stock markets

$54 trillion – US stock market capitalization

$30 trillion – the value of global real estate

$36 trillion – US National debt

$27 trillion – US GDP and end Q1 2025

$22 trillion – US M2 money supply

$20 trillion – total value of US real Estate

$17.8 trillion – GDP of China

$18 trillion – value of global physical gold holdings

$4 trillion – 2021 US corporate profits

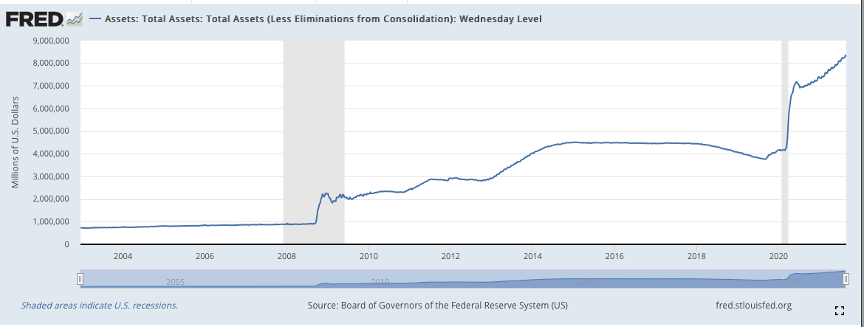

$6.7 trillion – US Federal Reserve balance sheet

$6.8 trillion – FY 2024 US Budget Spending (click here for details)

$4.9 trillion – 2024 US Budget revenues

$1.9 trillion – 2024 US Budget deficit

$4.2 trillion GDP of Japan

$4.5 trillion – GDP of Germany

$3.6 trillion – value of all issued cryptocurrencies

$4.0 trillion – GDP of California

$1.7 trillion – GDP of Australia

$2 trillion – GDP of Russia

Looking at this impressive list of numbers, there is one that leaps right out at you. That is the value of cryptocurrencies, which is only $2 trillion, two-thirds of which is Bitcoin.

That is less than 2% of the value of all assets in the world, 1% of the Global money supply, and .1% of US stock market capitalization. In other words, Bitcoin accounts for only a tiny share of global assets.

Which leads one to an obvious conclusion. The next big movement in money will be out of the largest asset classes into the smallest ones. The most obvious target here is the $150 trillion in the value of all bonds and fixed income securities, most of which have negative yields, or yields close to zero.

Move even a small portion out of bonds into Bitcoin, and its value has to double, triple, move up ten times, or even 100 times.

There are other screaming conclusions to be found in these numbers. The bond market (TLT) is toast and can only really go down from here. The same is true for the US dollar (UUP). Oh yes, and you want to buy the Australian dollar (FXA).

It gets better.

The US money supply is currently worth $20.5 trillion and is growing at a 30% rate. So, in a year it will be worth $26.65 trillion, and in two years it will be worth $34.65 trillion.

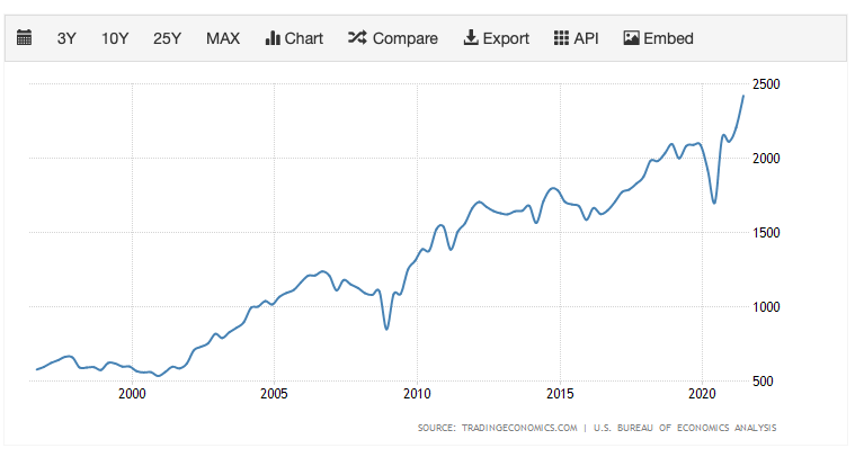

The biggest factor expanding the money supply today is NOT the government, but the explosive growth a US corporate profits, at $10 trillion in 2021, which is essentially a bet on the future of everything.

And US corporate earnings could continue growing at this ballistic for another decade or more.

That means that not only will global liquidity continue to increase, but it will also do so at an exponential rate.

US Corporate Profits

Federal Reserve Balance Sheet

“It’s not true that the government spends money like a drunken sailor. A drunken sailor spends his own money,” said JP Morgan CEO Jamie Diamond.

(AMD), (NVDA), (MSFT)

Only in tech investing can “not being NVIDIA” be considered a character flaw.

Last month, I was at yet another tech conference — you know the type, where VCs sip overpriced lattes and argue loudly about things they only half understand. One particularly confident investor declared, with a smirk, that “betting on AMD is like rooting for the Washington Generals against the Harlem Globetrotters.”

I nearly spit out my coffee. Not because he was wrong about NVIDIA’s (NVDA) dominance, but because he’d accidentally hit on exactly why AMD (AMD) might be one of the smartest contrarian plays in this entire AI-fueled market mania.

Let me tell you something about underdogs: the bar is so low, they get applause just for showing up. When they actually perform? The market loses its collective mind.

AMD is currently trading around $110, well off its $230 highs — complete with a markdown tag that screams “slightly bruised, still delicious.”

Wall Street’s neat little AI narrative goes like this: NVIDIA is the overlord, AMD is the afterthought, and any smart investor should cough up whatever premium NVIDIA demands. It’s a lovely story. Also incomplete.

Here’s the inconvenient truth: AMD just posted 75% revenue growth. Their data center business grew 57% year-over-year. Gross margins? Expanding. While the crowd worshipped at the altar of Jensen Huang’s leather jacket, AMD was out here quietly building a serious AI business.

And valuation-wise? We’re talking a forward P/E around 17x, compared to NVIDIA’s 21x — not a steal, but certainly not the nosebleed territory most of big tech is floating in. You’re getting real growth at a price that doesn’t require a confession booth after you hit the “buy” button.

No, AMD isn’t going to knock NVIDIA off its perch. That’s like saying your favorite local diner is going to take down McDonald’s. But in a trillion-dollar market, you don’t need to be the king to get rich — you just need to be a really good baron.

The beauty of AMD’s setup is this: they don’t have to win. They just need to keep not losing. And based on recent moves — Microsoft (MSFT) partnerships for Copilot+ PCs, expanding cloud relationships, a gaming division that’s actually growing — “not losing” looks very achievable.

Now let’s talk options, because this is where things get delightfully tactical. With AMD’s volatility spiking like it’s had one too many Red Bulls, the premium for selling puts is unusually attractive. Selling August $100 strike puts? That can net you about 4% in under three months — roughly 17% annualized, if you can keep rolling.

Here’s the kicker: either you pocket the premium, or you get assigned a stock you already like at a better price. That’s not risk; that’s a strategy. This is a classic maneuver: get paid to wait, or get paid to own.

AMD isn’t some dusty dividend play tossing retirees pocket change. It’s a growth story hiding inside a value wrapper. That rare combo where the stock’s not only undervalued but also growing like a weed in a biotech rally.

Yes, NVIDIA has better tech, deeper pockets, and Wall Street’s collective crush. They’re minting cash and priced like they’re going to solve climate change and write Shakespeare sonnets at the same time.

AMD is the barroom brawler in a tuxedo world. They’re rough around the edges, but increasingly hard to ignore. Their R&D spend is rising. Their balance sheet is solid. And they’re capturing meaningful slices of both data centers and gaming — not exactly rounding errors.

The real question isn’t “Can AMD beat NVIDIA?” It’s “Is AMD good enough to justify its current price?” Spoiler: yes. A 75% grower with diversified segments, real partnerships, and geopolitical tail coverage — that’s not a charity case, that’s a compelling investment.

Speaking of geopolitics, both AMD and NVIDIA are dancing on the same Taiwan Semiconductor supply chain tripwire. But AMD’s revenue base — spread across gaming, data centers, and embedded systems — offers better downside insulation if global tensions heat up.

And the options market agrees. This is a volatility story with upside. Sell puts for income. Buy shares for growth. Either way, you’re betting that the market eventually remembers profitable growth still matters.

My take? AMD is that rare beast: a company Wall Street’s overlooked just long enough for you to profit. It won’t scratch your NVIDIA FOMO itch, but it might just pay for your lake house.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Technology Letter

June 2, 2025

Fiat Lux

Featured Trade:

(A NEW AI INFRASTRUCTURE TO LOOK AT)

(VRT)