“In a social democracy with a fiat currency, all roads lead to inflation,” said legendary hedge fund manager Bill Fleckenstein.

“In a social democracy with a fiat currency, all roads lead to inflation,” said legendary hedge fund manager Bill Fleckenstein.

(DELL), (SFTBY), (AMZN), (MSFT), (META), (GOOGL), (NVDA)

Back in 2004, a hedge fund buddy of mine flew out to Round Rock, Texas, for what he called a “PC dinosaur autopsy.” He came back unimpressed, writing Dell (DELL) off as a relic of the beige-box era.

Fast forward two decades, and that same “dinosaur” is quietly morphing into the backbone of the AI age.

While the rest of the tech world was busy branding, rebranding, and tweeting about the metaverse or whatever the hype cycle dictated that week, Dell was rolling up its sleeves and building what actually matters: the infrastructure.

It’s been deep in the trenches with pipes, racks, and cooling systems, solving the nuts-and-bolts challenges of AI at scale. This isn’t about flash. It’s about function.

The kind that keeps trillion-parameter models from overheating and blowing fuses. That kind of real-world utility doesn’t make headlines, but it sure does drive cash flow.

Here’s the thing: Dell has stealthily re-engineered itself into the scaffolding of AI’s digital coliseum.

The company’s AI-optimized servers now power the very clusters that keep large language models caffeinated. We’re not talking about slapping a GPU in a box and calling it a day.

Dell’s hardware is the backbone of multi-billion-dollar data centers – machines engineered to keep heat, latency, and electricity bills from turning billion-dollar AI projects into smoking wreckage.

It’s high-margin, high-stakes, and very much underappreciated.

Just take a look at Project Stargate: a $500 billion venture with OpenAI, Oracle (ORCL), and SoftBank (SFTBY) to build 20 AI data centers the size of small cities across Texas. Each one will need tens of thousands of GPU-packed servers.

By some estimates, Dell could capture a double-digit share of this hardware spend, not to mention fat-margin integration and support services.

Yet the company still trades like it’s peddling fax machines – at just 0.9 times sales, a discount so wide it could host its own data center.

And it’s not just Stargate. Hyperscalers, including Amazon (AMZN), Microsoft (MSFT), Meta (META), and Alphabet (GOOGL), are collectively shelling out $315 billion this year on AI infrastructure.

About 70% of that goes into the kinds of servers, networking systems, and power optimization tools Dell happens to excel at.

While the market hyperventilates over Nvidia (NVDA)’s quarterly chip allocation, Dell is raking in $12 billion in AI server orders and delivering only a fraction so far.

That’s a sevenfold order-to-shipment ratio. Imagine booking a cruise that sells out seven times before it even docks.

Now let’s talk about that sweet, sweet operational leverage.

Dell’s Infrastructure Solutions Group, the division building these AI servers, grew revenue 12% year-over-year, but operating income leapt 36%.

Margins expanded to nearly 10%, with plenty of room to climb as the product mix tilts toward high-end AI systems.

Operating cash flow surged by 168%, while adjusted free cash flow rocketed 258% higher – a rare feat even in tech’s fast lane.

Yet the market snores on. Dell’s forward P/E? Just 13.3. The sector median? A bloated 24. EV-to-sales? 1.1x versus 3.3x. The disconnect here is so stark it feels like Dell showed up to the AI party in a tuxedo, and the bouncers still think it’s delivering the catering.

And here’s the kicker: this isn’t just a one-off quarter. Dell’s AI server revenue, which was effectively zero last year, is on pace to top $15 billion next year. That’s before accounting for a $14.4 billion backlog that’s growing faster than a ChatGPT prompt.

Conservatively, the pipeline stretches to $43 billion over the next 15 months.

Meanwhile, their traditional server and storage business is a stable $33 billion cash cow, and the PC division (despite headwinds) is holding steady at $50 billion in annual revenue, with a new AI PC cycle on the horizon.

Add it up, apply even modest multiples, and Dell’s sum-of-the-parts valuation clocks in around $190 billion. Today? It trades at a hair over $105 billion.

That’s a 70% upside for those seasoned enough to remember when “buy low, sell high” was more than just a Pinterest quote.

Dell doesn’t need to be sexy. It just needs to keep shipping AI infrastructure like clockwork, letting its numbers do the flirting.

For me, the path is clear: buy the dip, ignore the noise, and enjoy the ride as the rest of the market finally wakes up to what’s hiding in plain sight.

Mad Hedge Technology Letter

July 21, 2025

Fiat Lux

Featured Trade:

(WEBULL TO THE MOON)

(BULL)

The digital brokers will outperform in the short-term and long-term as retail dives into stocks and crypto.

It is not a surprise that markets are surging with the volume of options exploding.

As inflation persists, traders are going all in and big.

This is minting new millionaires in droves and creating massive demand for my trading services.

Webull, a digital investment platform founded in 2016 and headquartered in Saint Petersburg, Florida, has quickly established itself as a competitive player in the online brokerage space, rivaling platforms like Robinhood, Charles Schwab, and E-Trade.

Webull will be an outsized winner the next few years as trading volume goes from hot to out of control.

Webull has demonstrated impressive user acquisition, boasting over 24.1 million registered users and 4.72 million funded accounts as of Q1 2025, reflecting a 17% and 10% year-over-year increase, respectively.

Customer assets have surged 45% year-over-year to $12.6 billion, driven by strong net deposits of $1.054 billion in Q1 2025 alone.

This growth underscores Webull’s ability to attract and retain users, particularly younger, tech-savvy investors who are increasingly participating in the stock market.

Webull’s Q1 2025 earnings reported a 32% year-over-year revenue increase to $117.4 million, with a significant improvement in profitability.

Webull is expanding its platform with new products, such as its Webull Premium subscription, cryptocurrency trading in international markets, and corporate bond trading planned for 2025. Its partnership with BlackRock to provide portfolio solutions will enhance its appeal to a broad range of investors.

The reintroduction of crypto trading in Brazil and plans for U.S. crypto relaunch in Q3 2025 align with growing retail interest in digital assets. These initiatives position Webull as a versatile platform catering to evolving investor preferences, potentially driving user engagement and revenue.

The commission-free brokerage model, coupled with Webull’s focus on fractional share trading and advanced tools like charting and paper trading, appeals to both novice and experienced investors.

Webull faces risks, including intense competition from Robinhood and regulatory scrutiny over its model and past ties to Chinese investors.

including technical bullishness and upcoming earnings, support near-term price appreciation, while long-term expansion into new markets and asset classes positions Webull for sustained growth.

Stepping back and taking a look at Webull, I do believe they are smack dab in a growth phase that should excite investors.

We are in the beginning stages of crypto going mainstream, and as this trend accelerates, the volume trading at Webull is positioned perfectly.

It appears as if the power brokers of the business world are hellbent on grinding stock prices higher even at these nosebleed levels.

Just take at the Mag 7, who are all poised to announce positive earnings.

The trend is your friend, and retail trading isn’t going away anytime soon.

This is why activities such as sports gambling have become popular, because people are looking for that moonshot.

No longer can many Western countries deliver a slow and stable rise up in life standards.

Individuals need to catch the rocket out of financial misery to achieve their dreams, at Webull delivers that to the masses in spades.

The stock is poised to move to the upside for the rest of 2025, especially if Bitcoin continues its rampage to $200,000 per coin.

“The first step is to establish that something is possible; then probability will occur.” – Said Elon Musk

(THE STOCK MARKET IN SECOND-HALF 2025)

July 21, 2025

Hello everyone

WEEK AHEAD CALENDAR

MONDAY, JULY 21

10:00 a.m. Leading Indicators (June)

9:30 p.m. Australia RBA Minutes

Earnings: Steel Dynamics, Verizon Communications, Domino’s Pizza

TUESDAY, JULY 22

8:30 a.m. US Fed Powell Speech

10:00 a.m. Richmond Fed Index (July)

Earnings: Baker Hughes, Intuitive Surgical, Enphase Energy, Capital One Financial, Texas Instruments, EQT, Lockheed Martin, Sherwin-Williams, Philip Morris International, IQVIA Holdings, Coca-Cola, Haliburton, Quest Diagnostics, Pulte Group, KeyCorp, General Motors, D.R. Horton, Equifax, Danaher, RTX, Northrop Grumman

WEDNESDAY, JULY 23

10:00 a.m. Existing Home Sales (June)

Earnings: O’Reilly Automotive, ServiceNow, Chipotle Mexican Grill, T-Mobile US, United Rentals, Tesla, International Business Machines, Alphabet, Lamb Weston, Freeport McMoRan, General Dynamics, Lennox International, Hasbro, Boston Scientific, Thermo Fisher Scientific, Hilton Worldwide Holdings, AT&T, Otis Worldwide, NextEra Energy, GE Vernova, Raymond James Financial

THURSDAY, JULY 24

8:15 a.m. Euro Area Rate Decision

Previous: 2.0%

Forecast: 2.0%

8:30 a.m. Continuing Jobless Claims (07/12)

8:30 a.m. Initial Claims (07/19)

8:30 a.m. PMI Composite preliminary (July)

8:30 a.m. S&P PMI Manufacturing preliminary (July)

8:30 a.m. S&P PMI Services preliminary (July)

10:00 a.m. New Home Sales (June)

11:00 a.m. Kansas City Fed Manufacturing Index (July)

Earnings: Edwards Lifesciences, Deckers Outdoor, Intel Newmont, Ameriprise Financial, Union Pacific, Pool, Nasdaq, A.O. Smith, Valero Energy, West Pharmaceutical Services, Honeywell International, Dow, Westinghouse Air Brake Technologies, Textron, Tractor Supply, L3 Harris Technologies, Keurig Dr Pepper, CenterPoint Energy, Blackstone, Southwest Airlines

FRIDAY, JULY 25

8:30 a.m. Durable Orders preliminary (June)

Previous: 16.4%

Forecast: -11%

Earnings: HCA Healthcare, Phillips66, Charter Communication, Centene.

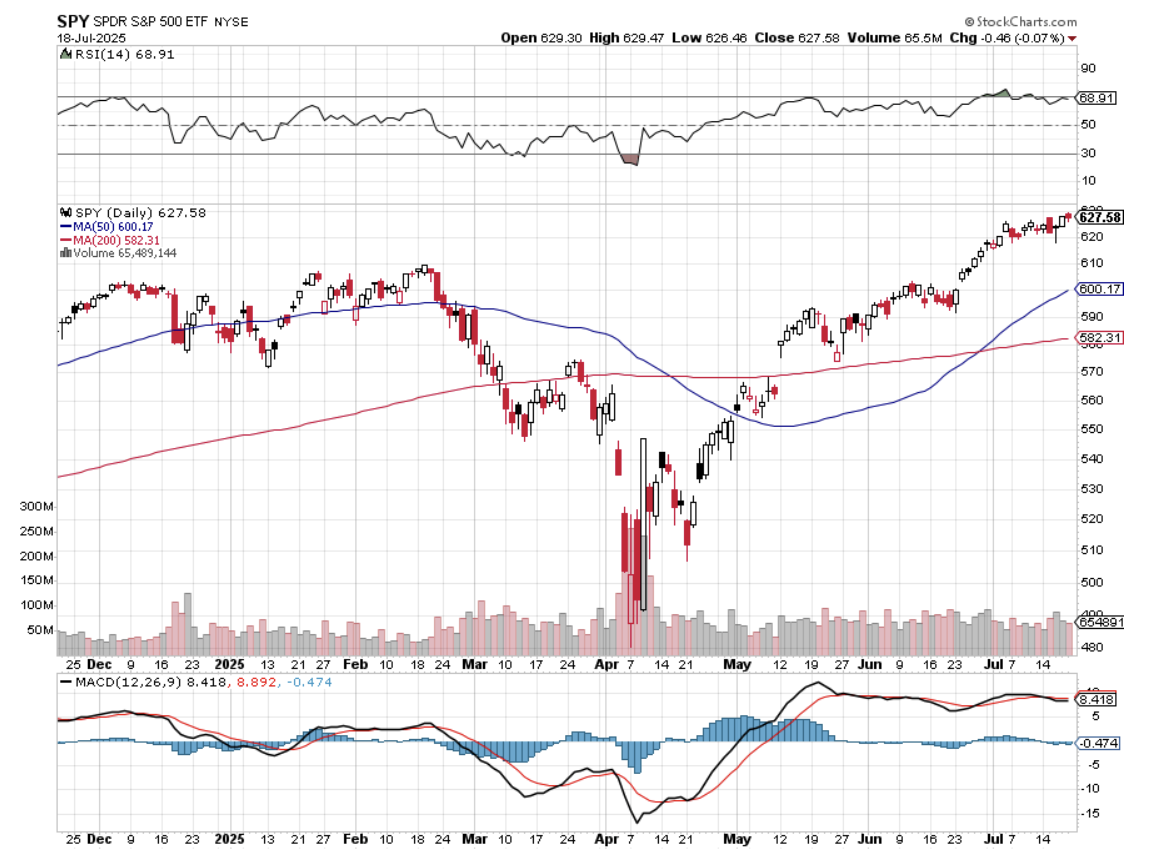

Will the record-setting run continue in the stock market?

Those in the bearish camp point toward weaker GDP, cracks in the job market, and inflation risks. Bullish investors think most of those risks were priced in during the spring sell-off, and the bar has been set low enough that anything less than disaster would be good enough to push forward revenue, earnings, and economic outlooks higher, rather than lower.

We must remember that stocks are forward-looking and are considered a leading, rather than lagging, indicator. The ability of stock prices to predict what may happen to the economy can look disorderly. A bit of stop and start here and there – a bit chaotic looking sometimes.

However, we know that the market can represent collective psychology, and this can be a valuable tool for economists and investors.

The predictive nature of markets is one reason behind the old Wall Street adage, “stocks climb a wall of worry.” Often, stocks bottom when everyone thinks the worst has yet to happen, and they top when everyone sees roses and daisies.

Over the past three months, the stock market has climbed a big wall of concern.

U.S. employers have announced over 696,000 layoffs through May, up 80% year over year, according to Challenger, Gray & Christmas. The unemployment rate has inched up to 4.1% in June from 3.4% in 2023. And inflation, while much lower than in 2022, when the Fed declared war on it by significantly raising interest rates, is still above the 2% level targeted by many, including the Fed.

The overarching landscape still suggests that stagflation, or even a recession, is a possibility. But so far, stocks indicate that the economy will side-step most damage.

Even though most are modelling lower rates over the coming year, which would help fuel economic activity, some analysts are not so confident about that outlook and are urging investors not to depend on the Fed stepping in to cut rates.

And let’s not forget the One Big Beautiful Bill Act, and its effects on the economy. It contains significant tax cuts, including new Social Security income tax breaks and a higher State and Local Tax deduction, which provide additional money to support spending and GDP.

Analysts who cut revenue and growth outlooks earlier in the year, may be increasing forecasts and potentially fuelling additional upside.

Arguably, those upward revisions could go a long way toward appeasing those concerned about the S&P 500’s valuation, given that the recent rally has inflated its price-to-earnings (P/E) ratio.

The S&P500 topped out in February when its forward price-to-earnings ratio eclipsed 22. It bottomed out when the P/E ratio reached about 19. The recent rally has again pushed the S&P 500’s P/E over 22, which historically doesn’t correspond with favourable one-year returns.

Carson Group’s Chief Strategist, Ryan Detrick, has updated their outlook. He has been bullish for a while.

Detrick’s optimism is partially rooted in history.

The strategist points out that since the early 1970’s, there have been five instances when the S&P 500 rose by 19% in 27 trading days like this year. Each time, the market was higher one year later, returning a median of 32.6%. Since 1950, the S&P500 has been up one year later 74% of the time, returning a median of 10.4%.

Detrick’s team writes, “This is still a young bull market.” The average bull market lasts 67 months, and this one has only lasted a little over 30 months so far.

The team goes on to say, “Like a cruise ship that is very hard to turn once it gets moving, bull markets tend to carry their momentum forward, another reason this once could last much longer than many think.”

Regarding valuation, the team believes there’s a bull case that a “low tariffs, big tax bill” environment will provide a catalyst for earnings, helping keep the P/E ratio in check.

If we are left with 15% tariffs, Detrick argues that “companies should be able to navigate the additional tariffs and maintain profit margins, especially larger companies with less fragile supply chains.”

Detrick acknowledges that 2025 has been a wild ride and that we should prepare for more ups and downs. Ultimately, he sees reasons to expect this bull market to continue.

Also in Detrick’s corner is hedge fund manager Bill Ackman, who manages Pershing Square, a hedge fund with $18 billion under management.

Ackman is bullish because he believes that the increase in money stashed in money market funds over the past year could make its way back into risk assets, propping up the stock market.

Let me give you an idea just how much is sitting in money market funds. As of July 10, the Investment Company Institute says $7.07 trillion is sitting in funds and that is up from $7.02 trillion on June 25.

Dan Ives is another bull, who is particularly bullish on technology. His current role is Wedbush Securities’ managing director and global head of technology research.

He argues, “The AI revolution is just hitting its next stage of growth from software to consumer to really the rest of the supply chain.” Ives believes potential numbers are being underestimated for the second half of the year.

Ives thinks that spending on AI will continue as more companies look to harness its power to shave costs from their system, using AI agents to increase efficiency and reduce labour costs.

Consequently, Ives thinks numbers can go a lot higher because of the spending, and because “we’re going to see 2 trillion of incremental spend over the next three years.

Ives argues that we could be looking at S&P potentially at 7,000.

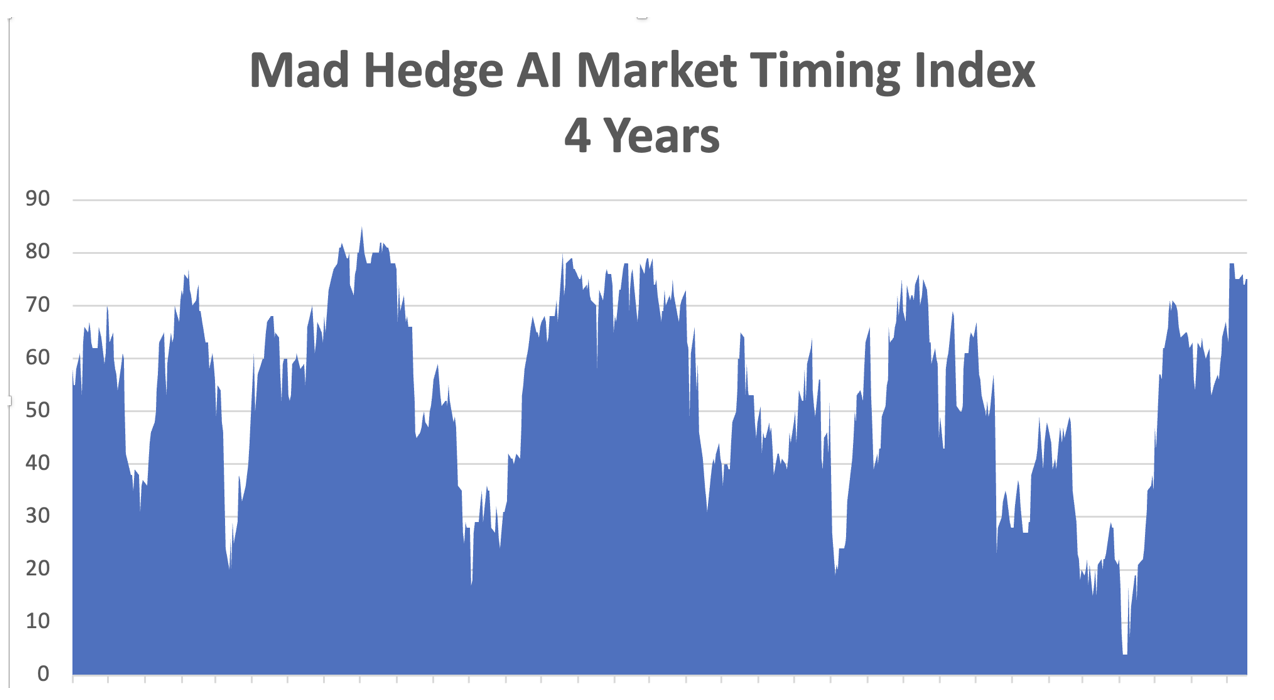

MARKET UPDATE

S&P500

The index reached another new high – 6314 – on July 18. There is still no sign of a peak yet “pattern wise” – although many talking heads, analysts & experts are pounding the table about “bubbles”, stretched P/E’s, & overbought markets. And of course, we are hearing about the “crash” in the markets that is going to happen in the very near future. (When are we not hearing about that?) Let’s pin them down and ask when exactly that is going to happen? Can they answer that?

Yes, we have had a long run from the April low, and momentum is starting to slow, and even some technicals have turned bearish – (check daily MACD).

But, as I have outlined above, many other hedge-fund managers and strategists are still bullish.

So, to approach the markets with great respect, you could start taking some profits on your trades – you can either take all profits, take half off the table, or roll forward. (All depends on your risk tolerance). Most of those option spreads I sent out in early June are in the money now; you may have some time premium left, but it might be better to take some profit and roll it into another trade. (I have found if you don’t take your profits, the market will often take them from you). I am not one to leave it to option expiration. Nobody knows what is going to happen on August 1.

Jacquie’s Post Option Spreads:

(IWM 215/225 Dec. 2025 & 215/220 Dec. 2025),

(AMZN 210/220 Oct 17, 2025 & 215/225 Oct. 17, 2025),

(QQQ 545/555 Sept. 30, 2025 & 550/560 Nov. 21, 2025),

(VST 180/185 Sept.19 2025)

Support = 6200/10 & 6140/50

Resistance = 6385/10

GOLD

Gold is still the dingo strolling across the island landscape. This extended period of choppiness could still be viewed as part of a longer-term topping pattern that is still unfolding. Gold is potentially forming a rising wedge/reversal pattern and could even test the ceiling at $3470/75k before rolling over.

Support = $3285/90

Resistance = $3375/80

Silver is the metal that is moving now, and we have two option spreads to take advantage of the rally happening now. (SLV) 33/35 & 33/36.

BITCOIN

After its spike higher to 123k, the coin is consolidating. The market has broken above key resistance of 112/115k area; the upside pattern is not yet complete from the June low at 98.2k, so further upside is favoured.

Support = 112/115k area (a break below here would put the bullish view on hold)

Resistance = 122/123k area

HISTORY CORNER

On July 21

QI CORNER

DEEP DIVE

Bitcoin

Daily chart

I have drawn on this chart to show you what could happen between now and the end of the year/early next year.

Bitcoin could rally further before it retraces for a period. It could then rally again into year end. Possible target = ~$150/$155k.

And then, I’m afraid, after everybody has jumped into bitcoin – including institutions – bitcoin could take a “deep dive” down to around the $40k/$30k handle over a two-year period.

My suggestion: start taking your money off the table as the coin keeps making new highs.

And that goes for your holdings in MicroStrategy and IBIT. MicroStrategy could be hit very hard when bitcoin does turn lower.

It’s about making the profit, taking it off the table and then rotating into the next trade/stock/sector.

Leave some crumbs for someone else.

This bitcoin chart goes back to 2020 showing rallies and retracements and a long consolidation pattern from 2022 to early 2024. This long sideways movement provided the platform from which bitcoin has launched.

SOMETHING TO THINK ABOUT

Cheers

Jacquie

Global Market Comments

July 21, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE CASE OF THE MISSING TARIFFS)

($VIX), (MSFT), (GOOGL), (META), (SPY), (QQQ), (CSCO), (TSLA), (AMGN), (MSTR), (AAPL)

NOTE: This is a Jeffrey Epstein-free letter.

The Volatility Index ($VIX) closed on Friday at a lowly $16.45. At that price, the index is predicting that the S&P 500 will move up or down less than 1.05% over the next 30 days. Somehow, I don’t think that is going to happen, especially going into September, the most volatile month of the year.

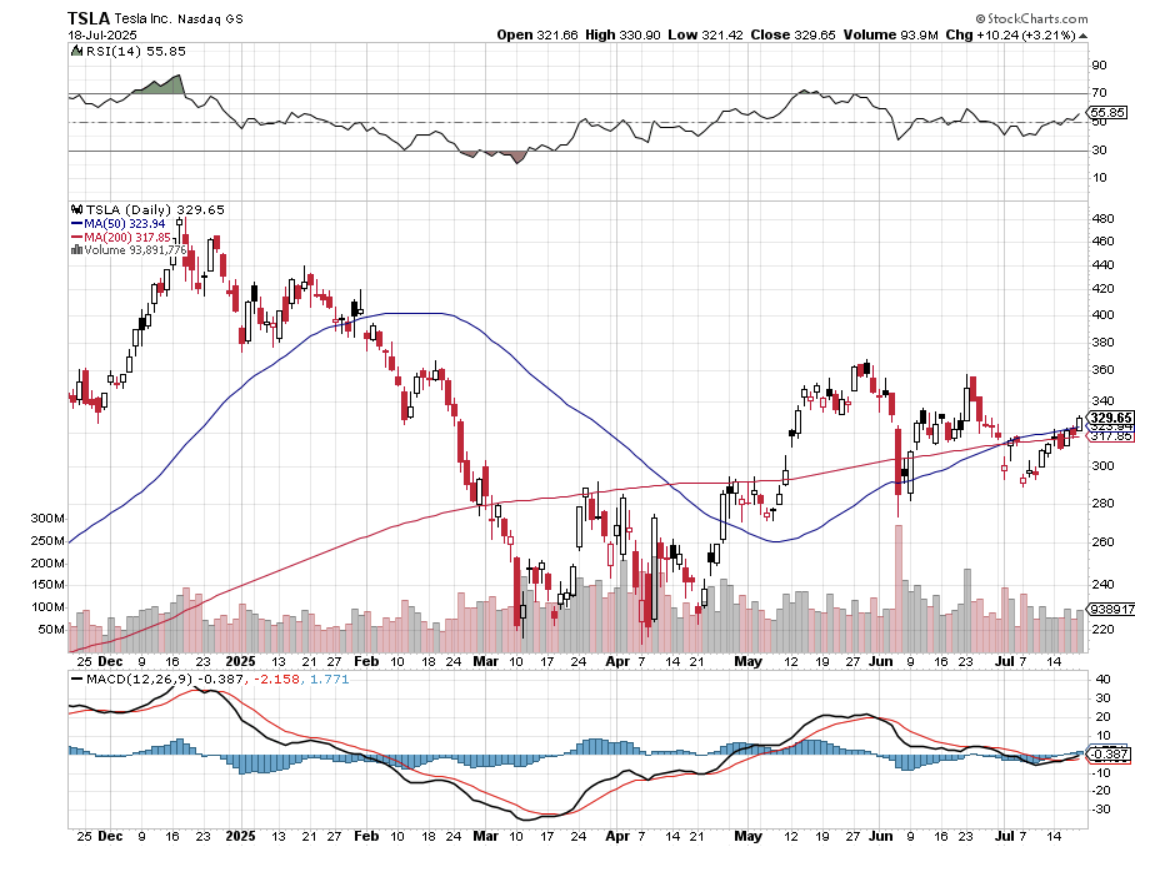

Many indicators are showing the stock market is now the most overbought in history. (QQQ) at 60 days above the 20-day moving average, endless days of positive MACD, and so on. But I have a much better indicator than those. The number of hedge funds calling me and begging for short ideas hit an 18-year high last week, even more than I saw during the dire days of the Great Recession. Many are worried about the impact global tariffs will have on the US economy when they kick in on August 1. I gave them my favorites: Tesla (TSLA), Apple (AAPL), and Strategy (MSTR).

The bulls are arguing that if we are in a stock bubble, it could go on for a long time.

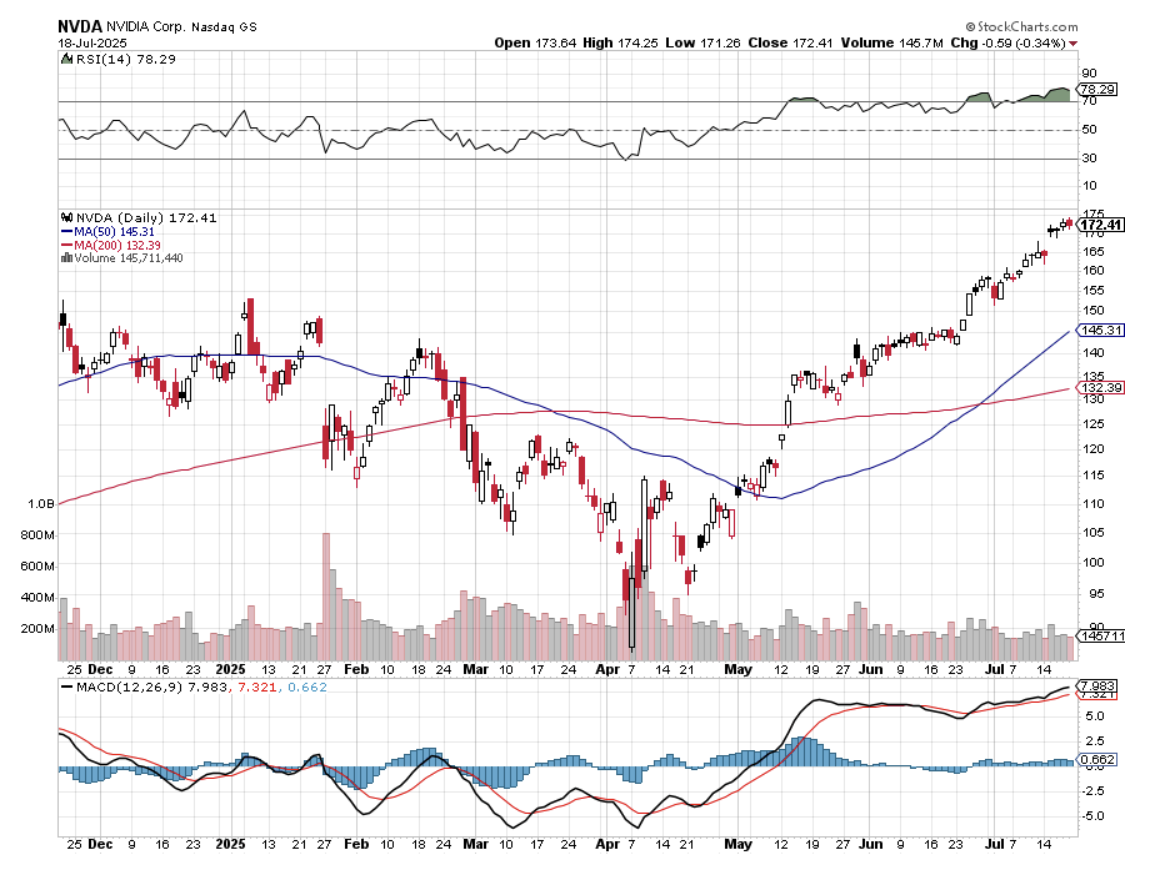

We are nowhere near a bubble top for AI. With China back in play, Nvidia (NVDA) is back on a ballistic revenue growth track. Microsoft (MSFT) and Alphabet (GOOGL) are still seeing explosive token growth. Spending on AI infrastructure is still taking place at the trillion-dollar level. Meta (META) is still seeing surging demand for its services.

The budget bill that passed last week gives tech companies a massive incentive to accelerate their capital spending. What it does is allow companies to expense capital investments in the year they are incurred instead of spreading them out over anywhere from 3-39 years, depending on the asset (my company amortized computers over seven years).

What this effectively does is take the oil depletion allowance unique to the energy industry adopted during the Great Depression and apply it to all industries. Readers in Texas will know what I am talking about, as if AI needed another incentive. Some 46% of all US capital spending right now is for AI.

If the government is trying to create a stock market bubble, this is a great way to do it. Worry about the inevitable crash later (1987, 2000, 2008, 2018, 2020, 2025).

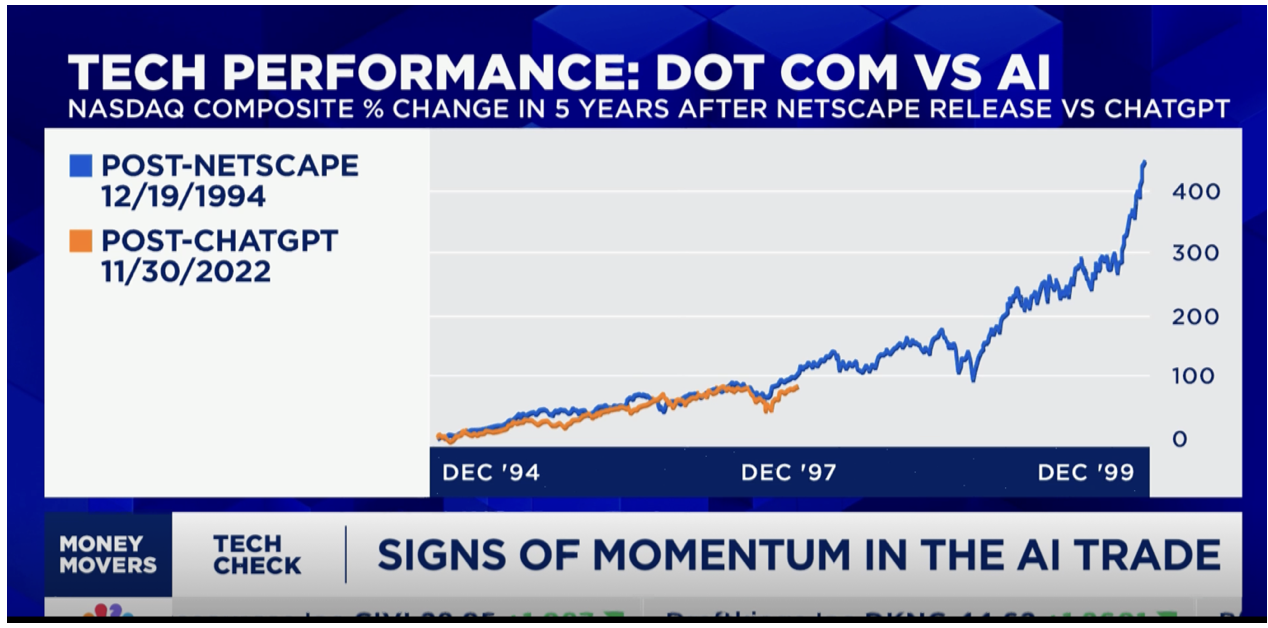

Look at the chart below, and you will see that current technology valuations have barely scratched the surface of the highs we saw during the Dotcom Bubble in the late 1990s. Back then, sky-high valuations were driven by eyeballs and the vast potential of the Internet. Now we have massive AI spending.

Today, the S&P 500 (SPY) trades as a 23X price-earnings multiple, while hypergrowth Nvidia sports a 56X multiple. In 1999, NASDAQ (QQQ) reached a 100X multiple, while the lead stock, Cisco Systems (CSCO), hit 200X. Those were heady times!

It is not a trade without risk. The trade war might never end. The bond market could crash at any time from the rocketing National Debt. Investors might grow impatient waiting for actual profits instead of promises. China might release another DeepSeek AI competitor.

Which brings us to the Case of the Missing Tariffs. Since the new administration came into office, tariff revenues for the US government have rocketed to all-time highs. During the first five months of this year, the US Treasury has collected over $100 billion in tariff revenues. The previous record for a full year is $100 billion. Projections for the full year run as high as $300 billion.

Front-running of the tariffs has been massive, generating the above record revenues, with the Port of Los Angeles seeing record congestion. What happens after August 1 when punitive tariffs on 140 countries that failed to cut a deal kick in? International trade will grind to a halt, possibly dragging the US into recession. With imports for the Christmas season almost done, importers have enough inventory to last for the rest of 2025. Then what?

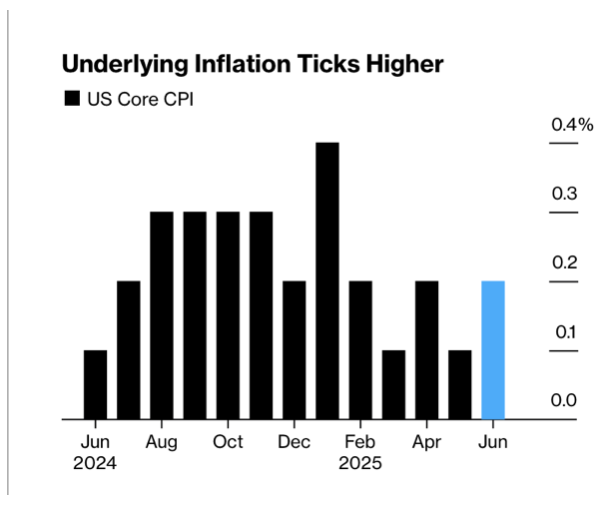

If the $100 billion is paid by American consumers, prices will rise, and inflation will take off. If tariffs are eaten by companies, profits will fall, and the stock market will plunge. Yet the inflation rate stood at only 2.7% YOY in June (click here). Will we see inflation in the July and August reports? Or is the stock market about to sell off? What if we get both?

Who paid the tariffs?

It is a mystery worthy of Sherlock Holmes.

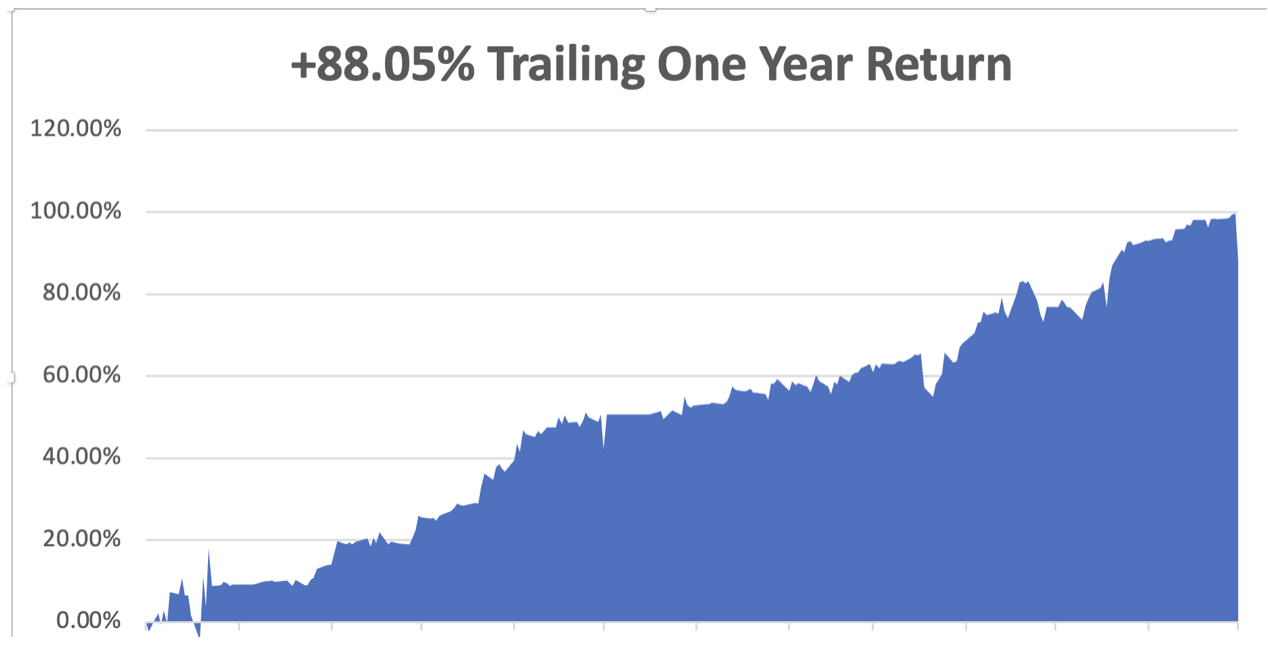

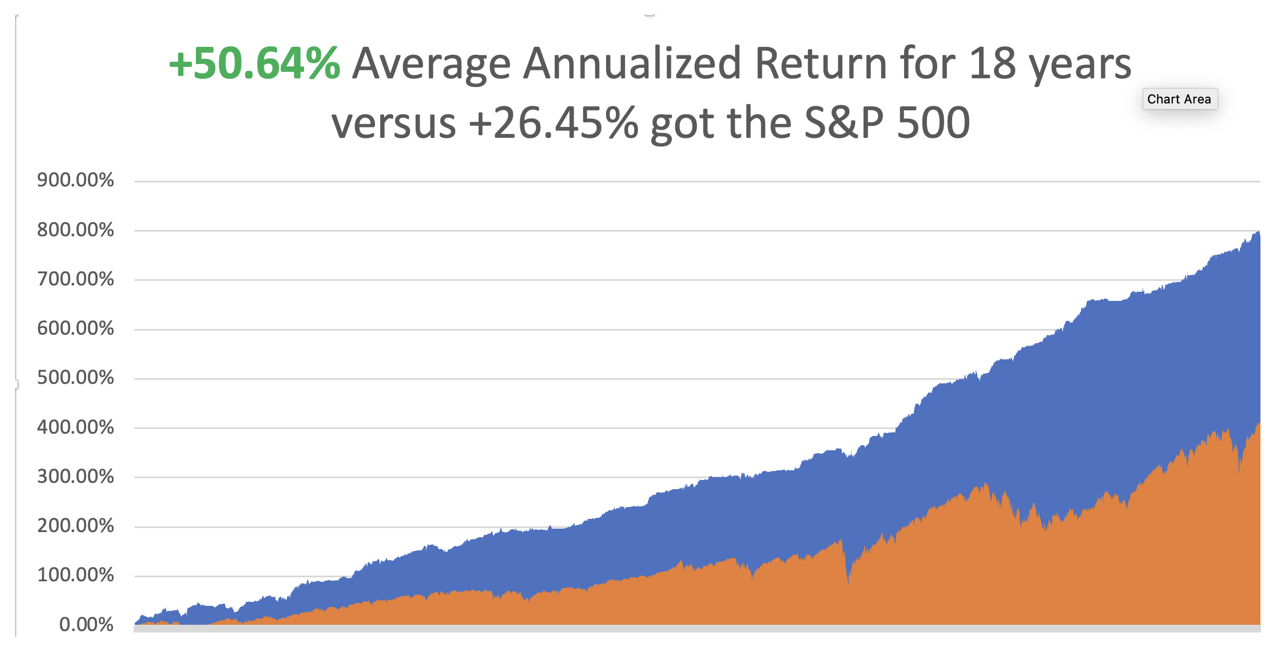

My July performance started off with a bang, with a +47.89% gain, taking us to new all-time highs on all metrics. That takes us to a year-to-date profit of +48.69%. My trailing one-year return rose to +88.05%. That takes my average annualized return to +50.64%, and my performance since inception finally topped +800.58%. These are all non-compounded numbers.

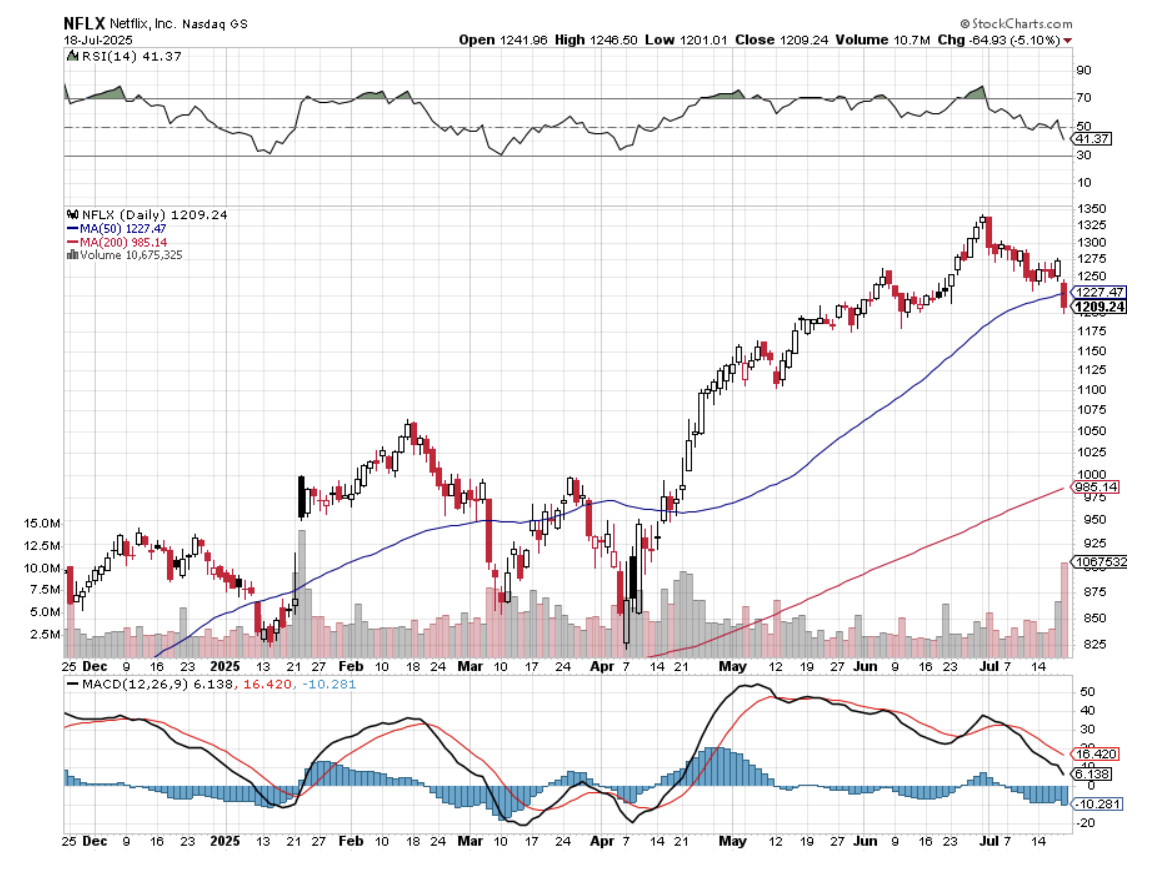

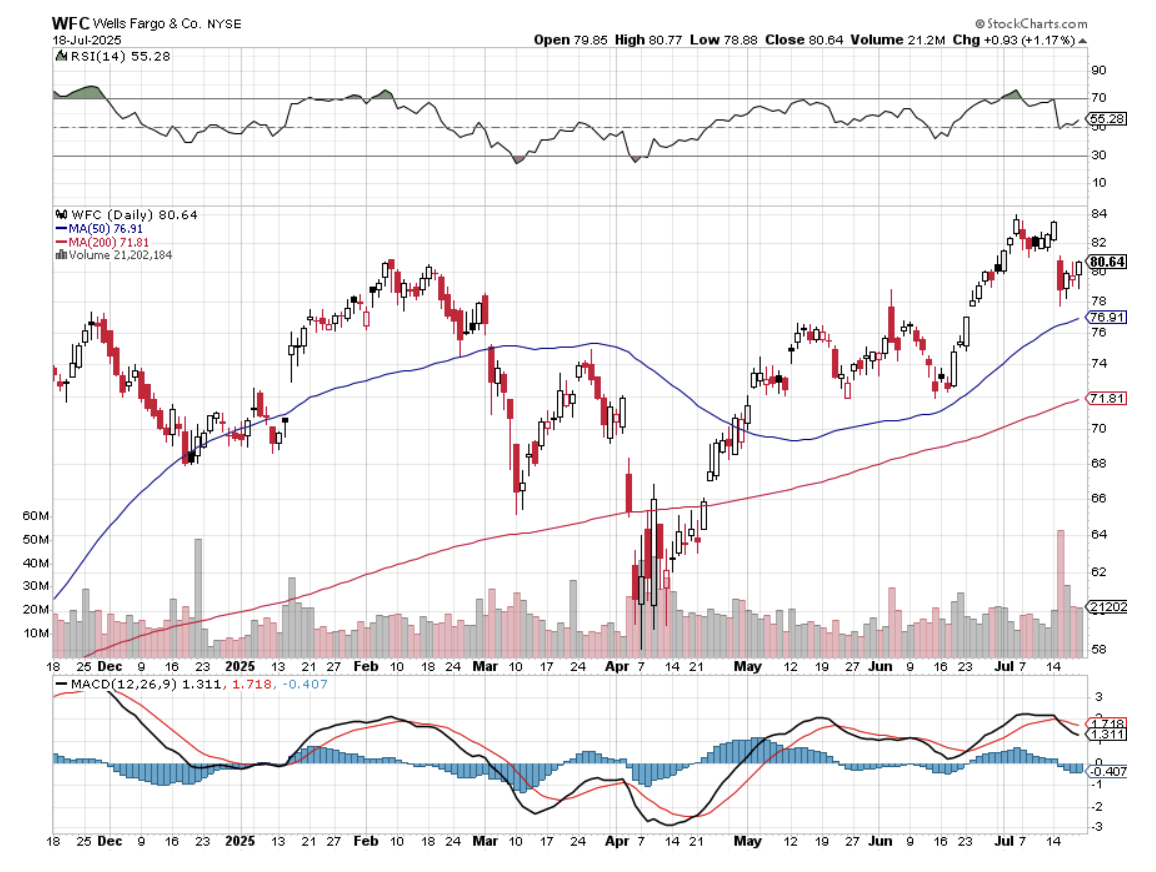

It was a totally dead week of desultory summer trading. I had three positions expire at max profit: a long in (AMGN) and two shorts in (TSLA). I then used selloffs to add two new longs in Wells Fargo (WFC) and Netflix (NFLX), the perfect stocks to own now because they are immune to the trade war.

That leaves me 80% cash, 0% short, and 20% long. With the Volatility Index hugging the $16 handle, we may be entering a trade drought.

Some 63 of my 70 round trips in 2023, or 90%, were profitable. Some 74 of 94 trades were profitable in 2024, and several of those losses were really break-even. That is a success rate of +78.72%.

Try beating that anywhere.

A Stock Rotation but Not a Selloff? That’s what Bank of America thinks is happening this summer. Investor sentiment surged in July to its most bullish since February, driven by the biggest jump in profit optimism in five years and a record surge in risk appetite. Cash levels dropped to 3.9% from 4.2%, triggering a sell signal on the bank’s proprietary trading model. The most crowded of trades is the consensus on shorting the dollar (DXY), which, at 34%, replaces long gold as the most pronounced investor bias. The flipside of this stance is the net overweight of 20% to the euro, the biggest for two decades. Is the trade to buy dollars, sell Euros?

China’s Economy Grows by 5.2% in Q2, as exports hold up remarkably well. That compares to US growth, which is flat at best. Is China winning the trade war at America’s expense?

Trade Desk (TTD) to Join S&P 500, at the expense of Ansys (ANSS), which is being bought by Synopsis (SNPS). (TTD) was up 9% on the news. Shares of Trade Desk, which provides a platform for advertising buyers, were sharply higher in premarket trading Tuesday, up 15% to $86.79, after being little changed in regular trading Monday

The Port of Los Angeles Sees Import Surge as importers rush to beat tariffs. It processed some 892,000 twenty-foot-equivalent units or TEUs, a record for June and up 32% from the previous month. It also highlights the tariff whipsaw effect. There’s a concern among American outbound shippers that we’ll start to see more reciprocal tariffs on US goods. The surge should continue in July, but higher costs will continue to hit importers, with trade forecasters expecting a severe drop for the rest of the summer and through the holiday period.

US Military Becomes the Largest Shareholder in MP Materials, the largest producer of rare earths in the US. The shares soared 50% on the news. This business can’t stand alone against Chinese cost advantages in labor and a lack of environmental controls. Rare earths are strategic minerals essential for national defense, the supply of which China has cut off many times. The previous iteration of this company, which had a sole mine at Mountain Pass, California, went bankrupt years ago. The Feds as a shareholder! What’s next?

Netflix Earnings Beat. It has a very high growth rate for a $542 billion company. It has an option implied volatility of 40%. It also just announced blockbuster earnings yesterday, removing a potential downside risk. With a price earnings multiple of 60X, it is one of the most expensive stocks in the market, but in this case, the high multiple is justified. Revenue for the quarter reached $11.08 billion, up 16% year over year. But nearly two-thirds of the online streamer’s sales come from abroad. Much of the strength came from a weak US dollar. Buy (NFLX) on dips. It is one of the few companies immune to the trade war.

US Retail Sales Pop, in a rush to beat price increases from the coming tariffs, suggesting a modest improvement in economic activity and giving the Federal Reserve cover to delay cutting interest rates while it gauges the inflation fallout from tariffs.

Tariffs on Most Countries Don’t Kick in Until August 1, meaning that we haven’t even seen a hint of inflation yet. Prices will take off like a rocket next month, but not get reported until September 10. No wonder Jay Powell is in no hurry to cut interest rates.

Housing Starts Rise by 4.6% from the previous month to a seasonally adjusted annualized rate of 1.321 million in June of 2025, trimming the revised 9.7% slide in the previous month. Starts fell in the Midwest (-5.3% to 179 thousand), the West (-1.4% to 286 thousand), and the South (-0.7% to 674 thousand)

Fed Beige Book Turns Pessimistic, with businesses reporting that tariffs caused upward pressure on prices. Fed report says employment slightly rose, hiring decisions postponed due to uncertainty. The US central bank is expected to maintain the current policy rate until at least September

Morgan Stanley Reports Record Profits, but my shares in my old firm dropped on the news. Investment banking revenue falls 5%, lagging Goldman and JPMorgan. Client assets at Morgan Stanley Asset Management moved closer to the long-term goal of $10 trillion.

Government Lifts Nvidia Ban on Chip Sales to China. Sales of the Mid-level H2O chips to the Chinese were banned by the previous administration. What’s changed since then? Have the Chinese suddenly become nice? I have no idea. It was Lenin who said,

“A capitalist will sell you the rope to hang him.” (NVDA) gets about 25% of its sales from China. Buy (NVDA) on dips.

Producer Price Index Comes in Flat, taking the annual rate down to 2.3%. It looks like the recession is offsetting the inflationary impact of the tariffs. Companies have no pricing power. The data will likely keep the Federal Reserve in a cautious stance about resuming its interest rate cuts. Trump has demanded that the U.S. central bank start lowering borrowing costs now.

Inflation Rises in June by 0.3%, to a 2.7% annual rate. You can forget about any interest rate cut in July with inflation rising. A big jump is expected in August and September.

My Ten-Year View – A Reassessment

We have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties, is now looking at multiple gale-force headwinds. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. My Dow 240,000 target has been pushed back to 2035.

On Monday, July 21, nothing of note takes place.

On Tuesday, July 22, at 7:30 AM EST, the Richmond Fed Manufacturing Index is announced.

On Wednesday, July 23, at 7:00 AM, we get the Existing Homes Sales.

On Thursday, July 24, we get Weekly Jobless Claims. We also get New Home Sales.

On Friday, July 25, at 8:30 AM, we get Durable Goods Orders.

As for me, since many of you are now planning long-overdue summer vacations, I thought I would pass on what I learned from the ultimate travel guru of all time.

After all, who knows how long it will be until the next pandemic? The next decade, next year, or next week?

When I backpacked around Europe in 1968, I relied heavily on Arthur Frommer’s legendary paperback guide, Europe on $5 a Day, which then boasted a cult like following among impoverished, but adventurous Americans. The charter airline business was then booming, plunging air fares, and suddenly Europe came within reach of ordinary Americans like me.

Over the following years, he directed me down cobblestoned alleyways, dubious foreign neighborhoods, and sometimes converted WWII air raid shelters, to find those incredible travel deals. When he passed through my town some 50 years later, I jumped at the chance to chat with the ever-cheerful, worshipped travel guru.

Frommer believes there are three sea change trends going on in the travel industry today. Business is moving away from the big three travel websites, Travelocity, Orbitz, and Priceline, which have more preferential, lucrative, but self-enriching side deals with airlines than can be counted, towards pure aggregator sites that almost always offer cheaper fares, like Kayak.com, Sidestep.com, and Fairchase.com.

There is a move away from traditional 48-person escorted bus tours towards small group adventures, like those offered by Gap Adventures, Intrepid Tours, and Adventure Center, that take parties of 12 or less on culturally eye-opening public transportation.

There has also been a huge surge in programs offered by universities that turn travelers into students for a week to study the liberal arts at Oxford, Cambridge, and UC Berkeley. His favorite was the Great Books programs offered by St. John’s University in Santa Fe, New Mexico.

Frommer says that the Internet has given a huge boost to international travel, but warns against user-generated content, 70% of which is bogus, posted by hotels and restaurants touting themselves.

The 93-year-old Frommer turned an army posting in Berlin in 1952 into a travel empire that publishes 340 books a year, or one out of every four travel books on the market. I met him on a swing through the San Francisco Bay Area (his ticket from New York was only $150), and he graciously signed my tattered, dog-eared original 1968 copy of his opus, which I still have.

Which country has changed the most in its 60 years of travel writing? France, where the citizenry has become noticeably more civil since losing WWII. Bali is the only place where you can still actually travel for $5/day, although you can see Honduras for $10/day. Always looking for a deal, Arthur’s next trip is to Chile, the only country in the world he has never visited.

Arthur’s Next Big Play is Bali

“Everybody talks about the Volatility Index (VIX), but the new fear gauge is the 10-year Treasury bond,” said Art Cashin of UBS Financial Services.

Mad Hedge Technology Letter

July 18, 2025

Fiat Lux

Featured Trade:

(THE EYEWEAR PIVOT NOBODY SAW COMING)

(META), (ESSILORLUXOTTICA)