Mad Hedge Biotech and Healthcare Letter

March 11, 2025

Fiat Lux

Featured Trade:

(WHEN INSIDERS GO SHOPPING, PAY ATTENTION)

(MRNA), (MRK)

Mad Hedge Biotech and Healthcare Letter

March 11, 2025

Fiat Lux

Featured Trade:

(WHEN INSIDERS GO SHOPPING, PAY ATTENTION)

(MRNA), (MRK)

In 1815, Nathan Rothschild made his legendary fortune buying British securities when they were deeply discounted after Waterloo. “Buy when there's blood in the streets,” he allegedly said. That kind of contrarian wisdom has made fortunes across centuries.

Two centuries later, I find myself applying this timeless principle to Moderna (MRNA). The biotech darling has shed over 90% of its value since the pandemic peak, plummeting from $400+ to under $30. And now, insiders are quietly loading up.

The shift in insider activity at Moderna has been striking. Over the past year, insiders unloaded more than 602,000 shares, with the heaviest selling in 2024 when the stock was trading above $120.

One director alone offloaded 202,832 shares in a single transaction, pocketing $30 million. But as Moderna’s share price took a nosedive, insider selling slowed to a trickle. By the time the stock fell below $100, most trades involved fewer than 1,000 shares.

Then, on March 3, the narrative took a dramatic turn: two insiders — including CEO Stéphane Bancel — scooped up nearly 200,000 shares, investing about $6 million. Bancel accounted for $5 million of that sum.

This move is telling. Bancel already controls over 21 million shares. You don’t drop another $5 million into a stock unless you believe you're buying Manhattan for beads and trinkets. The contrast is stark: when prices were high, executives couldn’t sell fast enough. Now, they’re buying.

The timing of these insider purchases is even more intriguing. Moderna had just slashed its 2025 revenue target by $1 billion, bringing guidance down to $2.5 to $3.5 billion. Yet, insiders chose that precise moment to buy, signaling confidence that sales will bottom out this year.

The company's drug pipeline isn't barren, either. Ten drugs are expected to receive FDA approvals by 2027, including a skin cancer vaccine developed with Merck (MRK) slated for a 2027 launch, pending Phase 3 data.

These ten anticipated drugs collectively target a market exceeding $30 billion, with analysts projecting Moderna's revenue to climb to $3.3 billion in 2027 and $4.77 billion by 2028.

On their Q4 '24 earnings call, President Stephen Hoge underscored the cancer vaccine’s potential: "As for INT, obviously, we're all looking forward to the melanoma -- adjuvant melanoma Phase 3 readout. As you know, and as I mentioned, there are additional Phase 3s as well as two randomized Phase 2s, including bladder cancer, renal cell carcinoma, which, depending on the rate of approval of events, could have readouts that we would be updating on as well in the coming years."

Still, the road ahead isn’t without challenges. Moderna expects to burn up to $3.5 billion in cash during 2025, reducing its cash position to $6 billion. Estimated cash costs for 2025 stand at $5.5 billion, projected to decline to $5 billion in 2026.

To reach breakeven by 2028, the company needs to generate $6+ billion in sales at 80% gross margins or implement further cost-cutting measures.

Despite these financial hurdles, Moderna's market cap is a mere $14 billion — practically pocket change for a company with multiple promising vaccine candidates.

There's undeniable risk in buying Moderna at these levels, but historically, the most profitable investments come before the financials improve. The company has effectively announced that its numbers will likely deteriorate further before rebounding — and yet, insiders are still buying.

Speaking of gathering valuable insights from industry leaders, I’ve been preparing for our Mad Hedge Traders & Investors Summit on March 11-13.

After decades in the markets, I’ve learned there’s something uniquely valuable about getting multiple perspectives in one place. It reminds me of my time in Tokyo during the '70s, where real opportunities often emerged from late-night conversations between veteran traders.

Even in today’s volatile environment, the wisdom of those who’ve navigated every market cycle remains invaluable.

In the end, Moderna presents a textbook contrarian opportunity. The stock is deeply out of favor, yet insider buying suggests a potential shift in sentiment as shares hover around $30.

The real question isn’t whether Moderna will recover but whether investors have the stomach to buy when others are still heading for the exits.

As for me, I’m keeping Moderna firmly on my watchlist, right next to my dog-eared copy of "Extraordinary Popular Delusions and the Madness of Crowds."

Some things never change.

Mad Hedge Biotech and Healthcare Letter

March 6, 2025

Fiat Lux

Featured Trade:

(THE DANISH DILEMMA)

(LLY), (NVO)

I was having dinner with a group of Mad Hedge Fund Trader readers in Salt Lake City the other week.

One, a successful financial advisor who's been following my market calls for years, posed a question that got the whole table talking: "Between Eli Lilly (LLY) and Novo Nordisk (NVO), which horse should I bet on in this weight loss drug race?"

It's the kind of direct question I appreciate. No beating around the bush, just cut straight to the investment thesis.

And the question couldn't have come at a better time—I'd spent the previous months analyzing the shifting dynamics between these two pharmaceutical powerhouses.

For those who haven't been following the battle between Eli Lilly and Novo Nordisk closely, you've been missing one of the most fascinating corporate duels in recent memory.

The American challenger has been steadily gaining ground against the Danish heavyweight in the GLP-1 market—drugs that were originally developed for diabetes but have become blockbusters for weight loss.

What's particularly interesting is the momentum shift that began in May 2024, with Lilly's upward trajectory continuing through February while Novo Nordisk's stock halted its precipitous decline at a critical juncture.

While bargain hunters are picking through NVO's wreckage, I'm skeptical we'll see a mass migration back to the Danish giant. Here's why.

First, there's the Trump factor. Our newly reinstalled president hasn't been subtle about demanding pharma companies shift production capacity back to American soil or face potential tariffs.

This presents a much bigger problem for Novo Nordisk than for Lilly.

The Indiana-based Lilly has a well-diversified manufacturing footprint, including substantial domestic capacity, while NVO relies heavily on non-U.S. production.

Years spent covering the White House taught me one thing: when a president threatens tariffs, smart investors listen—even if those threats haven't materialized yet.

Trump's policy shifts can come suddenly and dramatically. I've seen enough administration policy pivots over decades to know that being caught flat-footed when the music stops is a recipe for portfolio pain.

Beyond geopolitical considerations, Lilly's Zepbound (their branded weight loss medication) has been steadily gaining share in new prescriptions, showing more robust efficacy than Novo's offerings, and—in a savvy competitive move—is priced at a relative discount. It's a triple threat that's steadily eroding Novo's first-mover advantage.

But what's really impressive about Lilly's position is that they aren't putting all their eggs in the weight loss basket.

They've made solid advances in immunology and oncology, with a diverse pipeline that doesn't rely solely on incretin-based growth drivers.

This brings to mind a conversation I had with a pharmaceutical executive while flying my Ercoupe to an industry conference last weekend.

"The companies that survive long-term in this industry," he told me, "never let themselves become dependent on a single breakthrough, no matter how big."

Meanwhile, Wall Street has been revising upward its estimates for the total addressable market for weight loss drugs, anticipating expanded indications, sustained consumer adoption, and penetration into markets outside the U.S.

This strengthens the bull case for Lilly while simultaneously raising concerns about Novo Nordisk's ability to maintain its market leadership.

Speaking of market leadership, Lilly's oral GLP-1 receptor agonist Orforglipron could be submitted for regulatory approval in late 2025, potentially beating Novo's next-generation product to market.

If commercialized in 2026 as anticipated, it could further disrupt Wegovy's (Novo's weight loss drug) market position.

Some might argue that Lilly's outperformance against Novo since mid-2024 has already priced in these advantages.

But a closer look at Lilly's valuation suggests the market still isn't fully convinced of the company's growth potential.

Is this caution warranted? Perhaps. Wall Street doesn't expect Lilly's current surge in revenue growth to continue through 2027.

Lilly's management has indicated pricing will likely remain stable, but the broader expectation is that medium-term pricing may remain muted or even decline, especially as Novo's products face pricing negotiations by 2027.

This could pressure Lilly's market position, particularly given the relatively high prices in U.S. markets.

We should anticipate a more competitive landscape after 2027 as other competitors enter the weight loss drug market, though market share dynamics should remain relatively stable through 2030.

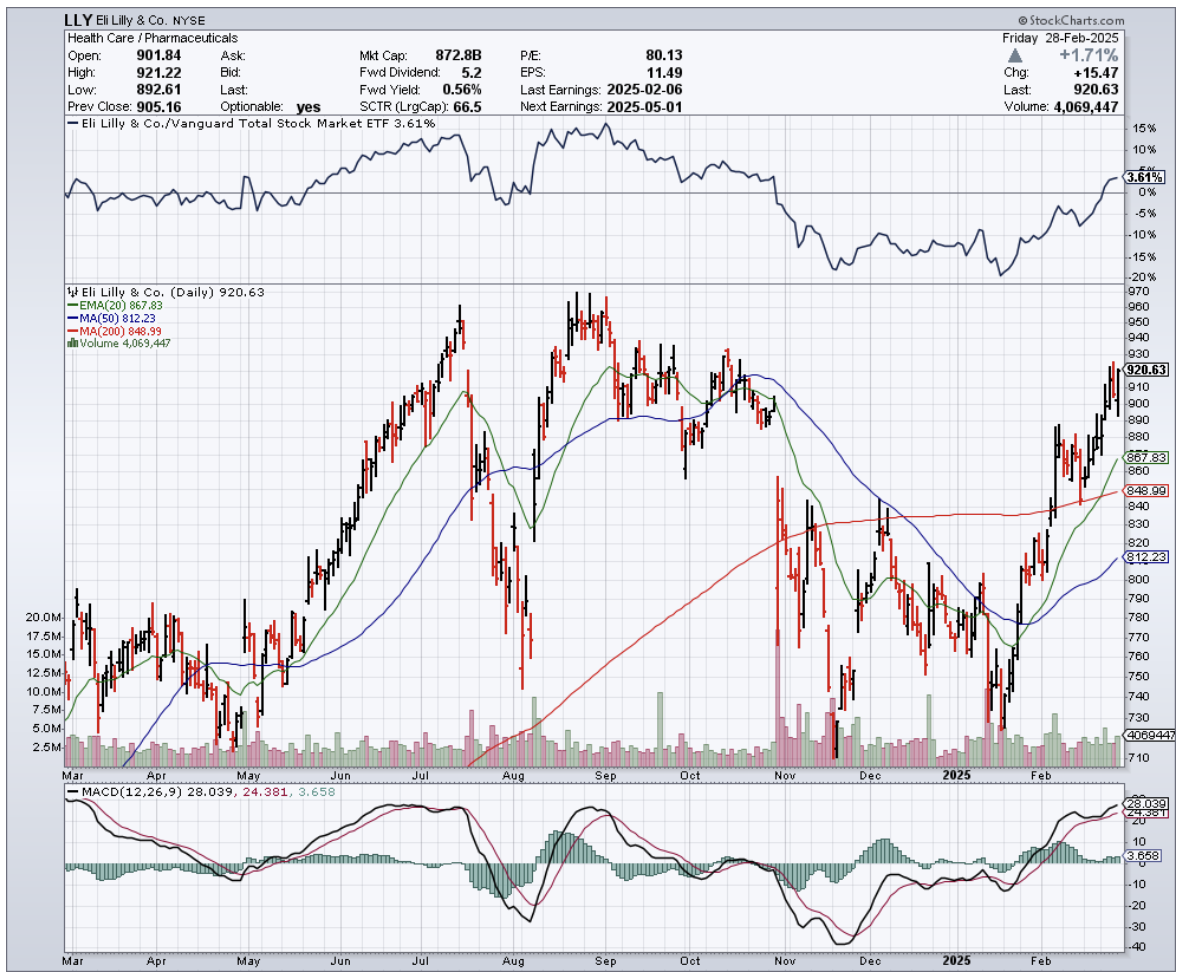

Let's talk valuation. Lilly is trading at a forward non-GAAP P/E of 37.8x, almost double its sector peers. That sounds expensive until you realize it's more than 10% below its five-year average.

More tellingly, when accounting for earnings growth prospects, Lilly's PEG ratio of 1.13 is almost 40% below the sector median.

Translation? The market hasn't gone full FOMO on Lilly yet, despite its recent outperformance of the S&P 500. In fact, price action suggests growing conviction that the stock is poised to retest its all-time highs.

Lilly weathered two setbacks in 2024 as the market questioned whether it could credibly challenge Novo's dominance.

Yet the stock found firm support above the $700 level in August, November, and again in January, confirming my belief that this support zone is rock-solid, attracting value-conscious buyers who recognize Lilly's growth potential relative to its valuation.

The breakout above the $840 zone (December highs) marks a decisive move that validates the bull case.

And while the outlook beyond 2027 remains murky, the market's restraint in valuing Lilly gives investors who've been watching from the sidelines another opportunity to board this train before it leaves the station.

"So what's your call?" pressed the advisor, who like many in his field has been forced to dump expensive research analysts while still needing solid investment ideas for his growing client base.

The rest of the table, a mix of successful entrepreneurs and self-taught traders, leaned in to hear my response.

"If you're picking between the two for a long position, Lilly is the clear choice," I replied. "They've got the edge on domestic production, they're better insulated from potential tariffs, they have a more diverse pipeline, and the market momentum is clearly in their favor."

As the waiter cleared our plates, one of the younger traders at the table asked about price targets. I tapped my wineglass thoughtfully with my pen—a habit that drives my wife crazy.

"The breakout above $840 was significant," I said. "If the fundamentals hold, which I believe they will, we could see a return to all-time highs before the bears even realize what hit them."

This led to a spirited debate about pharmaceutical valuations that lasted well past dessert.

It's these impromptu investment summits that remind me why I still travel the country meeting readers, despite having technically "retired" years ago.

The collective wisdom and diverse perspectives always sharpen my own thinking.

When the check arrived, someone joked that talking about weight loss drugs had made them lose their appetite.

“Not Lilly,” I quipped. “They're happily eating Novo's lunch”

Mad Hedge Biotech and Healthcare Letter

March 4, 2025

Fiat Lux

Featured Trade:

(A PHARMA GIANT BUILT FOR THE LONG HAUL)

(ABBV)

I was sitting in my 1946 Ercoupe at the Nevada airfield last weekend, waiting for clearance to take off for a quick joy flight, when my phone buzzed with a text from a longtime Concierge client.

"What's the deal with AbbVie (ABBV)?" he wanted to know. "Is it worth adding to my portfolio now?"

The timing was perfect. I'd just spent the previous evening poring over AbbVie's financials while sipping a particularly good Napa Cabernet I'd picked up at an estate sale for $15 (retail: $95).

There's something about the methodical drone of analyzing pharmaceutical company balance sheets that pairs beautifully with a rich red wine.

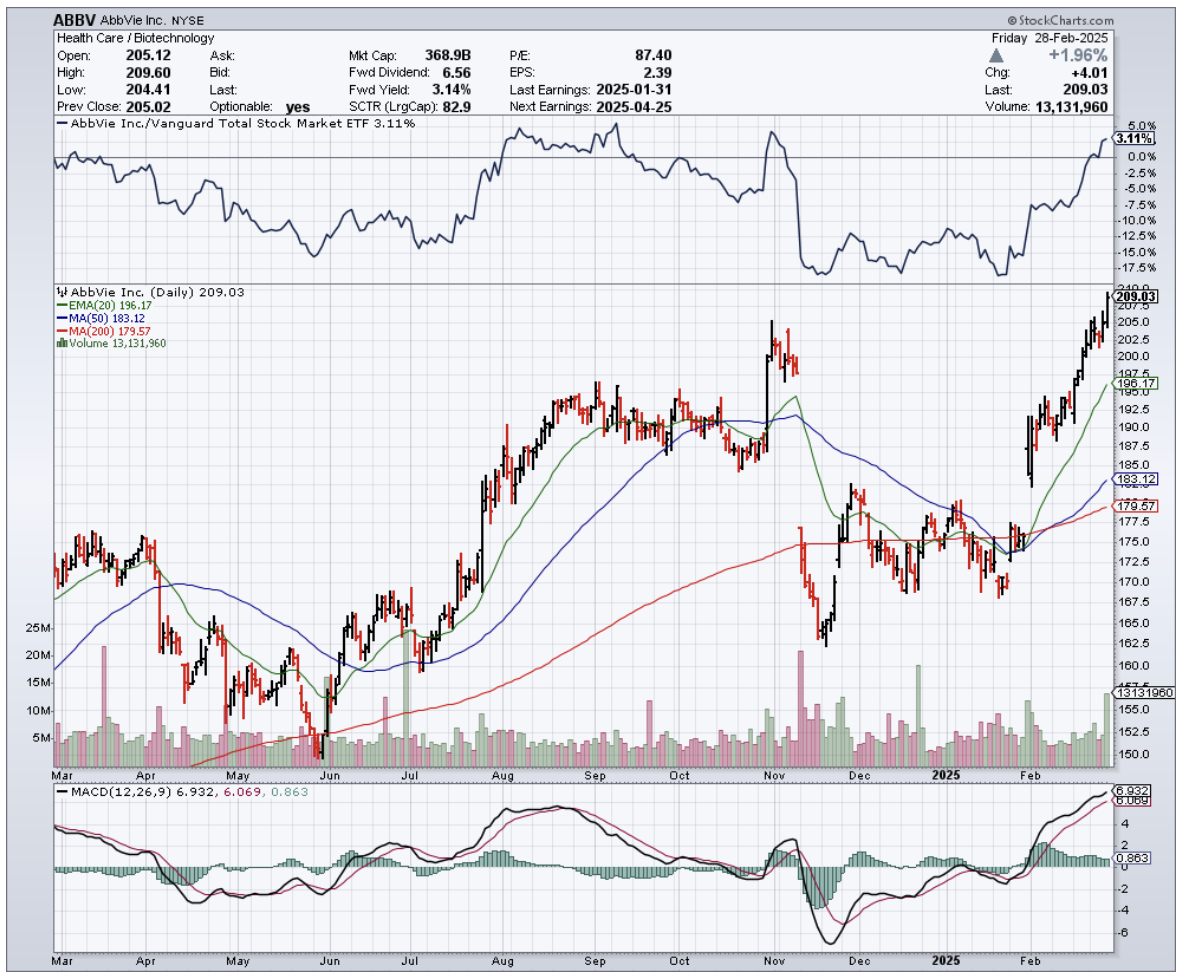

With a market cap north of $340 billion, AbbVie isn't exactly flying under anyone's radar.

But what fascinates me about this pharmaceutical behemoth is how it's managed to construct a business that's both defensively positioned and aggressively growing. It's like finding a Sherman tank that can also win drag races.

Let's dissect this beast, shall we?

Half of AbbVie's revenue comes from its immunology portfolio. The rest flows from neuroscience, oncology, and—here's where it gets interesting—aesthetics. This diversity isn't just window dressing; it's strategic positioning in markets growing far faster than inflation or GDP.

Take the immunology market, which analysts project will deliver a 10.2% CAGR over the next decade. That's the kind of growth that makes central bankers nervous and investors giddy.

AbbVie dominates this space with Rinvoq, Skyrizi, and the now-patent-expired but still lucrative Humira.

Speaking of Humira, it's worth noting what happened when this superstar drug lost patent protection in 2023.

After nearly two decades of market dominance, Humira finally faced the onslaught of biosimilars (think generic drugs, but for biologic medications).

Most pharmaceutical companies would have curled into the fetal position watching their golden goose get plucked. But AbbVie had been preparing, transitioning patients to newer offerings like Rinvoq and Skyrizi.

How well did that strategy work? These two upstarts now command a jaw-dropping 50% market share in inflammatory bowel disease indications.

If you've ever had to overcome entrenched competition in a market, you'll appreciate just how remarkable that achievement is.

Then there's neuroscience, where AbbVie's footprint includes Botox (not just for smoothing frown lines, folks), Qulipta, and Ubrelvy.

This Central Nervous System therapeutics market is projected to grow at 10.5% annually through 2030. Again, that's the kind of growth that makes you sit up straight in your ergonomic office chair.

The oncology space is a bit more challenging for AbbVie, with other pharmaceutical giants claiming larger market shares.

Still, AbbVie managed 10.8% revenue growth in oncology for 2024. Not too shabby for a supposedly "smaller player."

But the real head-turner is aesthetics medicine, projected to grow at a blistering 12.8% CAGR through 2030.

AbbVie isn't just participating here – it's dominating with Botox and Juvéderm holding 60% and 40% market shares in the U.S. toxins segment, respectively.

I remember speaking with a plastic surgeon at a conference in New York last year who told me, "When someone walks in asking for 'Botox,' it's like when people ask for a 'Kleenex' instead of a tissue. The brand has become the generic term."

That's market penetration you simply can't buy with advertising.

AbbVie's growth strategy is two-pronged: aggressive R&D investment (which increased from 13.44% to 15.22% of revenue year-over-year) and strategic acquisitions.

The company maintains a robust pipeline of new products, with several in late-stage FDA approval processes. They're also not too proud to partner with other pharmaceutical companies to develop new offerings—a pragmatic approach I've always admired in business leaders.

For income-focused investors, AbbVie offers a particularly compelling story.

The company just declared a $1.64 quarterly dividend per share, translating to a 3.4% forward yield.

More impressively, AbbVie is a member of the S&P Dividend Aristocrats Index, meaning it has increased its dividend annually for at least 25 consecutive years.

Is AbbVie financially strong enough to maintain this dividend streak while funding growth? With over $7 billion in cash and moderate leverage, all signs point to yes.

The company's stellar profitability provides additional confidence, despite slightly higher R&D expenses eating into operating margins.

The latest quarterly earnings release should put any remaining doubts to rest, with Q4 year-over-year revenue growth accelerating to 5.6%—significantly better than previous quarters—and a slight improvement in gross margin.

Of course, no investment comes without risks.

Competition in pharmaceuticals is brutal, with both innovative giants and generic producers constantly nipping at AbbVie's heels.

The rapid decline in Humira revenue following patent expiration serves as a stark reminder of how quickly fortunes can change. While the company has successfully navigated this transition, there's no guarantee it will repeat this feat with future patent expirations.

Manufacturing complexity and supply chain vulnerabilities also present risks, though these aren't unique to AbbVie.

Perhaps more concerning is the political and regulatory uncertainty following Donald Trump's return to the White House, including potential trade wars and controversial appointments like vaccine critic Robert F. Kennedy Jr.

Despite these risks, AbbVie presents an exceptionally attractive combination of growth potential and income generation.

The company's diversified business mix, strong positions in growing markets, aggressive growth strategy, and shareholder-friendly capital allocation make it a compelling addition to almost any portfolio.

As I finally got clearance and my little Ercoupe lifted off the Nevada runway, I texted my Concierge client back: "ABBV is a buy on the dip. Rock-solid business with growth. Don't overthink this one."

One of the benefits of our Mad Hedge Concierge service is exactly this kind of real-time market guidance—though most questions don't catch me mid-takeoff.

Sometimes the best investment ideas aren't the most exotic or revolutionary. Sometimes they're just exceptionally well-run businesses selling products people need, returning value to shareholders, and positioned in growing markets.

AbbVie checks all of these boxes with room to spare.

Mad Hedge Biotech and Healthcare Letter

February 27, 2025

Fiat Lux

Featured Trade:

(THE KENNEDY-ERA STOCK THAT'S STILL PAYING MY DINNER BILLS)

(JNJ), (ITCI)

The other day, while sorting through my oldest trading records (yes, I keep everything), I found my first Johnson & Johnson (JNJ) dividend check from decades ago. It wasn't much—just enough for a nice dinner back then.

But here's the kicker: that dividend has grown every single year since, weathering oil shocks, dot-com bubbles, financial crises, and even pandemics. It got me thinking about what truly makes a fortress stock in today's market.

While everyone's chasing the latest biotech and healthcare moonshot, JNJ has been quietly building an empire.

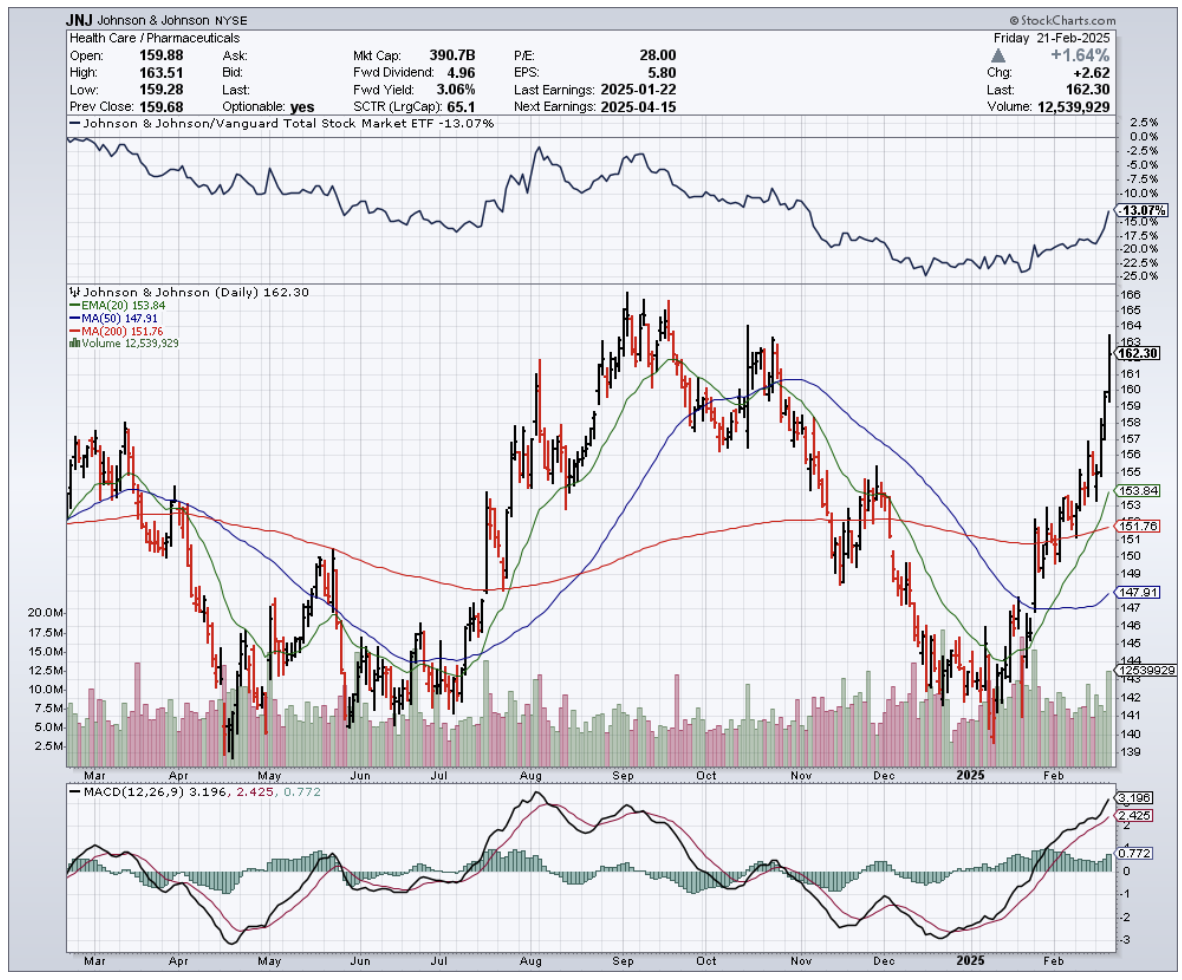

With a market cap of $375 billion and revenue growing at an impressive 7.55% annual clip since the 1980s, this company has accomplished something few others have—long-term, consistent growth while raising dividends for over six decades. And then there's the balance sheet.

JNJ is sitting on $25 billion in cash against $38 billion in total debt, resulting in a covered ratio of 29.4. That means they could pay their debt service with spare change found in their corporate couch cushions.

Some investors dismiss JNJ as just another mature healthcare stock, but that perspective overlooks the quiet revolution happening within the company.

In the first two months of 2025 alone, JNJ secured multiple FDA approvals. The most notable? SPRAVATO, the first and only monotherapy for treatment-resistant depression. And they're not stopping there.

JNJ recently announced a $14.6 billion acquisition of Intra-Cellular (ITCI), securing CAPLYTA, a blockbuster drug for bipolar disorder and schizophrenia.

With the global Central Nervous System therapeutics market projected to grow at a 10.5% CAGR through 2034, JNJ is strategically positioning itself for future expansion.

What's particularly impressive is how JNJ has transformed its research and development approach. They're not just throwing money at problems—they're getting smarter about their investments.

Their R&D success rate has been climbing, with a higher percentage of late-stage trials making it to market compared to industry averages. This isn't by accident.

JNJ has been leveraging artificial intelligence and machine learning to better predict which compounds are most likely to succeed, potentially saving billions in development costs. It's like having a crystal ball in the lab, and it's giving them a significant edge over competitors who are still using traditional development methods.

Despite its fortress balance sheet and track record of reliability, JNJ is currently trading at a discount to historical averages.

Its forward P/E ratio sits at 15.8, compared to a five-year average of 17.9. The dividend yield is at 3.18%, higher than its 10-year average of 2.7%. Its price-to-sales (P/S) ratio stands at 4.4, below its five-year average of 4.8.

These numbers suggest the market is underpricing JNJ's resilience and growth potential.

Of course, no investment is risk-free. JNJ is facing looming patent expirations on key drugs, including Stelara, which generated $10.3 billion in 2024 sales, and Xarelto, which brought in $2.3 billion.

However, history suggests that patent cliffs aren't a new challenge for JNJ—they've successfully navigated them for decades. Their strong drug pipeline, along with strategic acquisitions, should help offset any revenue declines.

Beyond pharmaceuticals, JNJ's business diversification is a major advantage.

With roughly two-thirds of revenue coming from Innovative Medicine and the remainder from MedTech, and with 43% of total revenue sourced outside the U.S., this diversified revenue mix helps mitigate risks tied to any single product or market.

What many investors miss is how JNJ's MedTech division is quietly becoming a powerhouse in its own right.

The division has been making strategic moves in robotics and AI-enabled surgical tools, positioning itself at the intersection of healthcare and technology.

This isn't just about selling more medical devices—it's about creating entirely new categories of treatment options. In an aging global population, this kind of innovation could be worth billions in future revenue streams.

With a 16.7% return on invested capital (ROIC) over the last decade and a modest 49% payout ratio, JNJ's dividend isn't just stable—it's poised for growth. The market's current pessimism has created a 24% discount on a company that has delivered for generations.

That's the kind of opportunity that made me start buying JNJ decades ago—and why I'm still adding to my position today.

In a world where even tech giants stumble, owning a company that's been raising its dividend since the Kennedy administration isn't just smart—it's common sense.

The question isn't whether JNJ is a buy. The real question is whether you'll regret not buying the dip.

Mad Hedge Biotech and Healthcare Letter

February 25, 2025

Fiat Lux

Featured Trade:

(WALL STREET'S MYOPIA IS YOUR OPPORTUNITY)

(REGN), (RHHBY), (AMGN), (AZN), (ABBV), (LLY)

While preparing my presentation for this week's Online Traders Conference, I came across a pattern that made me stop cold. You see, I've been gathering examples of how institutional investors quietly accumulate positions while retail traders are looking the other way.

And there it was, right in front of me - Regeneron Pharmaceuticals (REGN), displaying exactly the kind of setup I'll be warning traders about starting February 24.

You see, while everyone's been obsessing over the latest AI darlings, Regeneron has been quietly crushing it. Their Q4 revenue hit $3.79 billion, up 10.5% year-on-year.

But here's where it gets interesting - they beat consensus estimates by $43 million, and that's with their flagship eye drug Eylea taking a hit.

Speaking of Eylea, let's address the elephant in the room. Its sales dropped 11% to $1.19 billion, thanks to Roche's (RHHBY) Vabysmo muscling into their territory and Amgen's (AMGN) biosimilar crashing the party.

Four more biosimilars are waiting in the wings, held back only by patent disputes. Normally, this would send investors running for the hills.

But here's what the panic-sellers are missing.

Despite Eylea's challenges, Regeneron's non-GAAP EPS still climbed to $12.07, beating analyst expectations by 88 cents.

In fact, they've been playing jump rope with analyst estimates, leaping over them in 10 of the last 12 quarters. Yet their stock price has been doing its best impression of a sleeping cat - just lying there, barely moving.

As someone who's spent decades watching market cycles, I recognize this pattern.

We're in what technical analysts call an “accumulation phase.” While retail investors yawn and look elsewhere, institutional money is quietly building positions.

It's like watching a spring being compressed - boring until it isn't.

But here's what really got my attention: Regeneron just joined the dividend club. Starting March 20, they're paying $0.88 per quarter. Sure, the yield won't make income investors swoon, but that's not the point.

It reminds me of how AstraZeneca (AZN) played it - first, dominate growing markets, then gradually turn on the dividend spigot to attract the steady-money crowd.

They're also backing up the dividend with a $3 billion share buyback program.

With $9 billion in cash and short-term investments, they've got more dry powder than a Revolutionary War armory.

In Q4 alone, Regeneron spent $1.23 billion buying back shares - up 64.1% from last year.

And here's where it gets even more interesting. Their oncology franchise, led by Libtayo, is looking like a dark horse winner. Libtayo sales jumped 50.4% year-over-year to $367 million.

While that might not sound earth-shattering compared to cancer drug heavyweights like Merck's (MRK) Keytruda, Libtayo just pulled off something remarkable.

In their Phase 3 C-POST trial for high-risk skin cancer patients, Libtayo reduced death and disease recurrence risk by 68% compared to placebo.

Even better? Merck's competing trial for Keytruda in the same indication fell flat on its face. In this business, that's like watching your main competitor trip at the Olympic finals.

Looking ahead to 2029, I'm seeing revenue hitting $20.4 billion - think high single-digit growth each year. That would bring their price-to-sales ratio down from 5.12x to 3.53x.

Their non-GAAP EPS should hit $76.5, implying double-digit growth most years. With the stock currently trading at just 14.76x earnings - below most peers like AbbVie (19.06x) and Eli Lilly (64.96x).

On top of these, 2025 is packed with potential catalysts - clinical trial results and FDA decisions that could light a fire under the stock.

Analysts' average target is $929.37, suggesting about 38% upside. But in my experience, when you combine strong fundamentals, multiple growth drivers, and a market that's sleeping on the story, those targets often end up looking conservative.

Remember, the market loves nothing more than a comeback story.

With Regeneron, we might just be watching one unfold in slow motion. The question is: will you be holding shares when the spring finally releases?

For those who want to learn more about spotting these kinds of opportunities, I'll be diving deeper into institutional accumulation patterns at the Online Traders Conference running February 24 through March 1.

But don't wait for my presentation to take a serious look at Regeneron - the smart money isn't.