Mad Hedge Biotech and Healthcare Letter

February 20, 2025

Fiat Lux

Featured Trade:

(PORTFOLIO MANAGEMENT DURING PAIN MANAGEMENT)

(VRTX), (DSNKY), (AZN), (GILD), (SNY), (GSK), (JNJ), (BMY), (LLY)

Mad Hedge Biotech and Healthcare Letter

February 20, 2025

Fiat Lux

Featured Trade:

(PORTFOLIO MANAGEMENT DURING PAIN MANAGEMENT)

(VRTX), (DSNKY), (AZN), (GILD), (SNY), (GSK), (JNJ), (BMY), (LLY)

During physical therapy last week - still working on that Russian bullet in my hip from Ukraine - I was going through pharmaceutical pipeline data on my laptop. Between resistance exercises, I spotted something that made me forget about the pain entirely. After decades of tracking biotech launches, I rarely see numbers that make me sit up straight. But these did exactly that.

My analysis shows a potential $29 billion boom in annual sales by 2030 from the biggest drug launches expected in 2025. That's not a typo - we're looking at almost double last year's forecast of $15.2 billion. And while my therapist kept telling me to focus on my exercises, I couldn't take my eyes off these projections.

The numbers tell a compelling story. Leading the pack is Vertex Pharmaceuticals' (VRTX) cystic fibrosis treatment Alyftrek, which snagged its FDA approval ahead of schedule in late 2024. They're looking at $8.3 billion in annual sales by 2030. As someone who's studied market-moving data across Asia and Wall Street, I know transformative numbers when I see them.

What really catches my attention is Vertex's pricing strategy. They've set Alyftrek's annual list price at $370,269, about 7% higher than their previous treatment Trikafta's $346,048. The drug expands Vertex's CF franchise into 31 additional mutations, potentially treating about 150 new CF patients in the U.S. alone. That's the kind of market expansion that creates blockbusters.

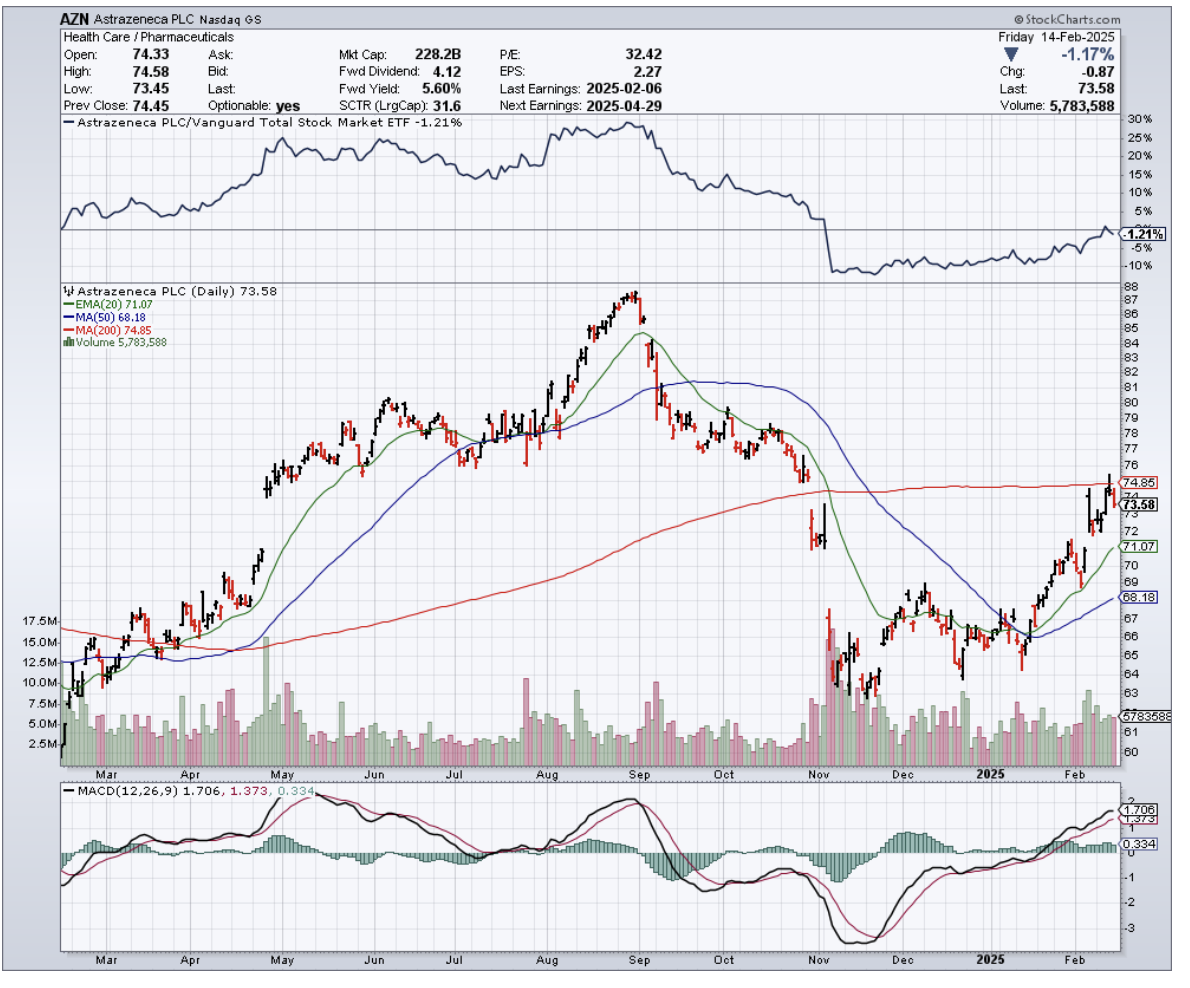

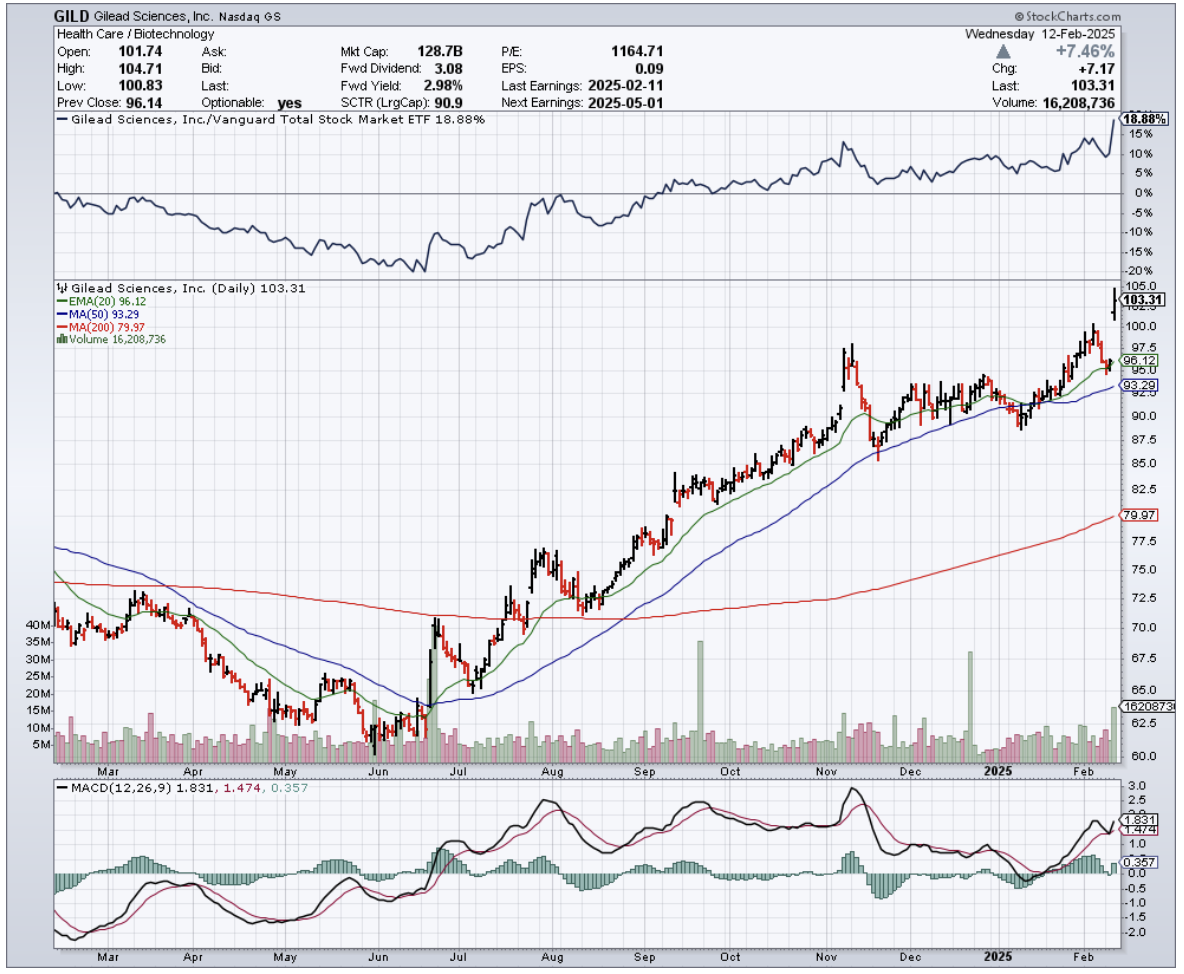

The second spot belongs to Daiichi Sankyo (DSNKY) and AstraZeneca's (AZN) Datroway, projected for nearly $6 billion in 2030 sales. They've already secured their first FDA approval this January for breast cancer. But here's what you need to watch: the bigger opportunity lies in lung cancer. While they faced setbacks in 2023, including patient deaths that intensified doubts, they're now advancing toward first-line treatment data in the second half of 2025. The AVANZAR trial could open up a major market opportunity, particularly if they can leap ahead of Gilead's (GILD) Trodelvy.

Speaking of opportunities, Vertex appears again with suzetrigine, their non-opioid pain management drug targeting both acute and neuropathic pain. With a January 30th FDA decision date looming, they're aiming to become "the first novel pain mechanism to reach the market for decades." My analysis points to just under $3 billion in annual sales by 2030. As someone who knows a thing or two about pain management these days, I can tell you that new approaches without addiction potential are pharmaceutical gold.

The pattern here is clear: we're seeing a concentration of breakthrough therapies across multiple high-value indications. From Sanofi's (SNY) tolebrutinib for multiple sclerosis to GSK's (GSK) depemokimab for severe asthma, which reduced asthma exacerbations by 54% compared to placebo, these aren't just incremental improvements - they're potential market reshaping events.

Looking ahead, we've got Johnson & Johnson's (JNJ) nipocalimab for myasthenia gravis, which could be the start of multiple autoimmune disorder approvals. GSK's meningococcal vaccine is targeting peak sales of $2.4 billion across its portfolio. Even Innovent and Eli Lilly's mazdutide for diabetes and obesity is showing promise in the Chinese market.

Will all these projections materialize? That's the $29 billion question. But even if only half hit their marks, we're looking at one of the most significant years for pharmaceutical launches in recent memory. The smart money is watching these developments closely, particularly in companies with multiple promising candidates.

Speaking of watching closely - my therapist is giving me that look again. Time to get back to those exercises. But between you and me, a potentially historic year in pharmaceutical launches is a lot more interesting than leg lifts. And with $29 billion in projected sales on the horizon, the pain in my portfolio might be easier to manage than the one in my hip.

The market will be watching these launches carefully. So should you.

Mad Hedge Biotech and Healthcare Letter

February 18, 2025

Fiat Lux

Featured Trade:

(A TALE OF TWO SHOTS)

(GILD), (MSFT)

The smell of antiseptic and sounds of beeping monitors filled the air as I walked through a Tokyo hospital ward back in 1975.

As a fresh UCLA biochemistry graduate working in Japan, I was visiting a friend who had contracted hepatitis B - a common affliction in Asia at the time.

Little did I know that decades later, I'd be analyzing a company that would revolutionize not just hepatitis treatment, but potentially end the AIDS epidemic as we know it.

That company is Gilead Sciences (GILD), and they just delivered a knockout Q4 that has Wall Street's attention.

But the real story here isn't in the numbers - though believe me, we'll get to those. It's about what's coming next.

Last week, Gilead reported Q4 revenue of $7.57 billion, beating estimates by $420 million. Not too shabby for a company some analysts had written off as past its prime.

And here’s another thing that got my attention: their new HIV prevention treatment, lenacapavir, achieved something I've rarely seen in four decades of following biotech - a standing ovation at the AIDS 2024 conference.

Why? Because it worked. Not just worked - it was 100% effective in one trial and 99.9% in another.

For perspective, that's like pitching a perfect game in the World Series, twice. And instead of daily pills, we're talking about two shots per year.

The FDA is expected to weigh in by summer 2025, and after seeing results like these, I'd bet my vintage Japanese sake collection on approval.

The numbers tell quite a story. Gilead's HIV franchise grew 16% year-over-year, with their flagship drug Biktarvy now commanding over 50% market share.

Even with Medicare Part D changes taking a $1 billion bite out of 2025 revenues (thanks, IRA), management still guided for $28.2-28.6 billion in revenue.

That's not just maintaining course - that's sailing straight through a hurricane without spilling your coffee.

Their oncology business isn't sleeping either. Trodelvy hit $1.3 billion in 2024 sales, up 19% from last year.

Their cell therapies Yescarta and Tecartus are performing like seasoned kabuki actors, bringing in $390 million and $98 million respectively in Q4.

On top of these, Gilead has over 50 clinical programs running simultaneously.

For those keeping score at home, that's more shots on goal than a World Cup final. And they don't face any major patent cliffs until late 2033 - practically an eternity in biotech years.

Speaking of shots on goal, let's talk about that stock price.

Shares have climbed from $71 to around $100 since my last recommendation. Not bad, but given what's in the pipeline, I think we're still in the early innings here.

The company's latest breakthrough, Livdelzi for liver disease, already pulled in $30 million in its first quarter.

Some analysts are talking about $2 billion in peak sales - and having seen my share of liver disease cases during my time in Asia, I wouldn't be surprised if they're being conservative.

Looking ahead to 2025, Gilead has several potential catalysts.

Two major Trodelvy trial readouts, potential lenacapavir approvals worldwide, and expansion into new markets.

They've come a long way since their Harvoni glory days of 2015, transforming from a one-hit wonder into a diversified powerhouse.

Is the stock cheap? Not as cheap as when I first recommended it. But with lenacapavir looking like it could change the game in HIV prevention, this feels like watching Microsoft (MSFT) in the early days of Windows - you know something big is coming, even if you can't quite see the whole picture yet.

The last time I saw scientific results this promising was during China's opening up in the late 1970s, when decades of isolated research suddenly became available to the world.

As for my friend from that Tokyo hospital? He recovered fully, thanks to medical advances that seemed impossible at the time.

Today's impossibilities have a funny way of becoming tomorrow's breakthroughs - and that's exactly why I'm rating Gilead a strong buy on any dips.

Mad Hedge Biotech and Healthcare Letter

February 13, 2025

Fiat Lux

Featured Trade:

(TRIPLE-LOCKED AND LOADED)

(AMGN)

Back in 1989, when I was setting up one of the first international hedge funds, I learned a timeless lesson about pharmaceutical stocks: the market doesn't care what you think it should care about—it cares about whatever it wants to care about.

That was on full display last week, as I watched Amgen (AMGN) dance its post-earnings tango and rally despite the FDA putting a mysterious hold on its obesity drug trials.

The stock’s move was exactly what its technical patterns suggested.

After managing hedge fund money for decades, I’ve seen literally millions of chart setups, and AMGN’s current formation is one of those rare “textbook” moments that make veteran traders sit up a little straighter in their ergonomic chairs.

The numbers paint a fascinating picture. Amgen isn’t just any biotech; it’s one of the dwindling few in the Dow 30 that still yield north of 3%. In this market, that’s about as rare as finding a bargain at Sotheby’s.

Better yet, it carries a dividend safety rating of A—something I’ve come to value above all else after living through multiple market crashes.

In my experience, dividend safety is the bedrock on which everything else is built, so seeing that in a company is like stumbling upon a bomb shelter with a view.

Digging deeper, the company just delivered a revenue beat that would make any analyst grin, but the real hook for me is the pattern of earnings revisions.

They’re trending up more than down, fueling a kind of momentum that reminds me of the early days of Genentech’s meteoric rise back in the 1980s.

Of course, there’s an elephant in the room: valuation.

With a D- grade in that department, Amgen’s price tag is about as stretched as my old climbing rope from Mount Everest. But modern markets aren’t your grandfather’s markets anymore.

The days of pure buy-and-hold being a guaranteed winning strategy have gone the way of paper trading tickets, replaced by algorithms and new trading paradigms.

This is why I like to employ what I call the "Triple-Lock Position" strategy.

Essentially, you buy the stock, buy a put for protection, and sell a call to offset that cost - three distinct moves that work together to lock in your risk parameters.

With Amgen hovering around $300, one round lot sets you back roughly $30,000. That price tag is a good reminder that position sizing matters more than ever.

Meanwhile, Amgen’s profitability metrics remain consistently top-tier.

From my hedge fund experience, steady cash flow and consistent profits often trump the promise of explosive growth, especially when storm clouds gather.

In volatile markets, companies that can reliably generate cash tend to outlast the flashier high-flyers.

Then there’s the technical angle. After analyzing enough charts to wallpaper the old Swiss Bank Corp building, I can say these trend lines have been as reliable as a Swiss watch.

Yes, we see the occasional short-term break, but it’s akin to a compass briefly pointing south before swinging back to true north.

For those who track this stuff closely, AMGN appears to be offering one of those rare situations where technical strength aligns with fundamental quality.

So what’s the play? I see Amgen as a “buy the dip” opportunity, but I suggest doing it with a twist. Instead of simply loading up on shares the old-fashioned way, consider collaring your position or using call options to define your risk.

Markets these days reward flexibility, and adapting your strategy to the current environment is crucial—something I learned during the Asian financial crisis, when clinging to outdated rules was a surefire path to disappointment.

All of this brings us back to that FDA hold on AMG 513. The market’s collective shrug reminds me of an old trading floor saying: “The market will decide what to worry about, not us.”

In biotech, as in most sectors, the reaction to news often reveals more than the news itself. Watching how investors brush off certain announcements can be more informative than pouring over the finer details.

Keep a close eye on those trend lines, because they’ve served as a pretty good compass so far. AMGN is showing the kind of setup where technical signals and strong fundamentals converge, and that rarely goes unnoticed for long.

Just remember, in the modern market, it’s not only about what you buy; it’s about how you buy it. The once-reliable buy-and-hold mindset is no more current than my old Financial Times columns from the 1970s.

Now, if you’ll excuse me, I need to check on my option positions. The market waits for no one—not even old hedge fund traders with stories to tell.

Mad Hedge Biotech and Healthcare Letter

February 11, 2025

Fiat Lux

Featured Trade:

(SPLICING THROUGH SKEPTICISM)

(CSRP), (VRTX), (AMZN), (TSLA)

When I pioneered fracking technology in Texas years ago, skeptics said we were crazy. Today's skeptics are saying the same thing about CRISPR Therapeutics (CRSP), and they're just as wrong.

Here's a company sitting on a $1.9 billion cash fortress, burning through a mere $100 million per quarter – giving them enough runway to circle the Earth 19 times – and yet the stock has drifted down to $40, shedding 15% since my last analysis when it was perched at $48.

Talk about the market missing the forest for the trees.

Remember when everyone thought Amazon (AMZN) was just a bookstore? Well, CRISPR Therapeutics isn't just another biotech company – it's the Tesla (TSLA) of gene editing, with Vertex Pharmaceuticals (VRTX) riding shotgun.

And just like Tesla wasn't just about making electric cars, CRISPR isn't just about Casgevy, their FDA-approved treatment for Sickle Cell Disease (SCD) and Transfusion-Dependent Beta Thalassemia (TDT).

Speaking of Casgevy, let's tackle the elephant in the room. Yes, patient enrollment has been slower than a government committee deciding on lunch options. They've collected cells from over 50 patients by year-end, up from 20 in mid-October.

Not exactly setting speed records, but here's what the market is missing: the Centers for Medicare and Medicaid Services just inked a deal with Vertex/CRISPR that could be a game-changer.

Why? Because 50-60% of SCD patients are on Medicaid.

But wait, there's more happening behind the scenes. The company has been quietly building an empire across 5 clinical programs and 10 preclinical programs.

Let's break down what's cooking in their kitchen.

The Casgevy rollout has expanded from 35 treatment centers in October to over 50 by year-end.

Eight jurisdictions have given them the green light, including Saudi Arabia – a market where SCD is about as common as sand.

The UK just signed on for reimbursement, first for TDT in August 2024, and now for SCD.

Their CAR-T program isn't just targeting blood cancers anymore. They've expanded into autoimmune diseases like Systemic sclerosis (SSc) and Idiopathic inflammatory myopathy (IIM).

We're talking about potential treatments for 2.5 million SSc patients globally (125,000 in the US) and 1 million IIM patients (50,000 in the US).

That's not just a market – it's an ocean.

They're even taking shots at liver cancer and cardiovascular diseases. Their latest trial for Heterozygous familial hypercholesterolemia could be a lifeline for patients with this genetic cholesterol disorder.

And speaking of cash runways, their $1.9 billion war chest means they can keep this scientific symphony playing for 19 quarters without passing around the collection plate.

In biotech terms, that's like having enough food to last through three winters.

Institutions are noticing, too. Cathie Wood just backed up the truck, dropping $10 million more into CRISPR, making it her 9th largest holding at $350 million. Her ARK funds now own over 9% of the company.

When smart money moves like this, I pay attention.

Here's the kicker: While most analysts raise their ratings as speculative stocks climb (a strategy that makes as much sense as buying umbrella futures during a drought), I'm doing the opposite.

After all, the fundamentals are stronger than ever, but the price is lower.

Looking ahead to 2025, we've got more potential catalysts than a chemistry textbook. Phase 1/2 trial data for CTX 112 is coming in Q2/Q3, CTX 131 in Q3/Q4, and updates on their Type 1 Diabetes program in the second half of the year.

Remember, this is the same company that has Vertex Pharmaceuticals – the biotech equivalent of having Warren Buffett as your investment advisor – as a partner.

They're not just getting financial support; they're getting a masterclass in how to commercialize breakthrough treatments.

The verdict? Load up on shares while the market gives us this gift wrapped in fear and uncertainty.

Twenty years ago, they called us crazy for thinking we could extract oil from solid rock. Today, they're just as skeptical about editing genes.

History has a funny way of repeating itself.

Mad Hedge Biotech and Healthcare Letter

February 6, 2025

Fiat Lux

Featured Trade:

(YOU MIGHT NEED ASPIRIN FOR THIS ONE)

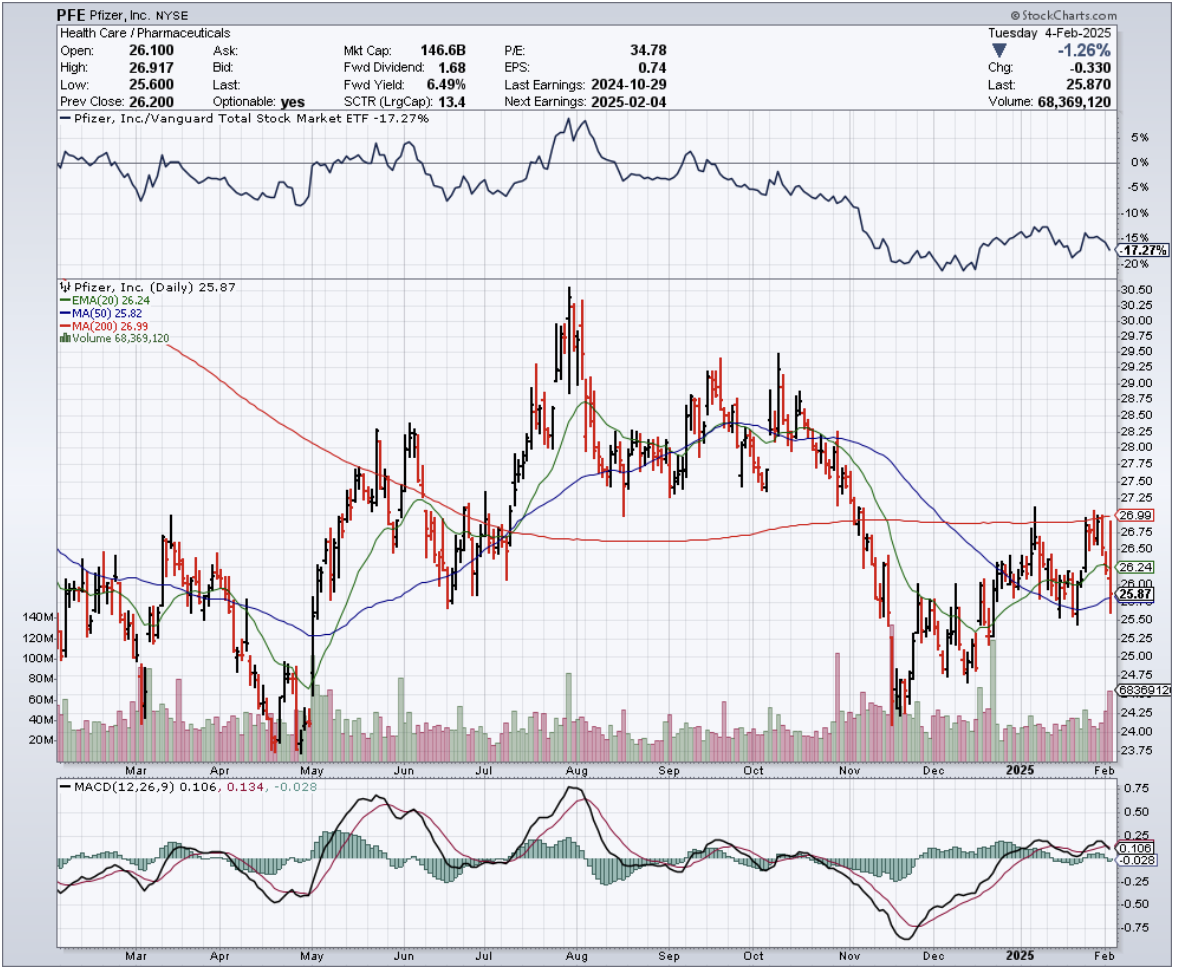

(PFE)

Last Tuesday, while filing away some tax documents, I found myself staring at an old prescription bottle from 2020. The Pfizer (PFE) logo caught my eye, and ironically, that same morning they dropped their Q4 earnings report.

The timing felt symbolic – much like that old bottle, Pfizer's COVID glory days are now just a memory on their financial statements.

The numbers looked good on the surface. EPS of $0.63 beat expectations by $0.17, and revenue came in at a healthy $17.8B, crushing estimates by $540M.

But in the pharmaceutical world, today's blockbuster is tomorrow's generic, and Wall Street knows it. After all, the market's reaction was about as enthusiastic as a patient reading medication side effects.

Let me paint you a picture of what we're dealing with here. Imagine going from making $100.3B in 2022 (those glory days of COVID) to $58.5B in 2023. That's not a haircut – that's a full-blown scalping.

Sure, they bounced back to $63.6B in 2024, but their 2025 guidance of $61.0B to $64.0B suggests they're treading water at best.

Now, here's where it gets interesting, and not in a good way. Remember how I always tell you to look under the hood? Well, Pfizer's engine is about to lose some major parts.

By 2030, they're saying goodbye to patents on Eliquis (a $6.7B revenue generator) and Ibrance (worth $4.8B). That's like losing your two best-performing stocks in your portfolio – it hurts.

Speaking of pain, I had lunch last week with a pharmaceutical industry veteran who couldn't stop talking about the "LOE wave" – that's "loss of exclusivity" in pharma-speak. CEO Albert Bourla puts it at about $17-18 billion in lost revenue over the next 3-4 years.

To put that in perspective, that's like losing the annual GDP of Mongolia. The company's solution? They're promising to deliver $20 billion in new revenues by 2030 through their pipeline of new drugs.

One bright spot worth watching is their oncology division, which grew an impressive 27.4% year-over-year in 2024.

Their promising candidate Atirmociclib, a CDK4i inhibitor for metastatic breast cancer, enters Phase 3 studies in the first half of 2025.

With a 44% historical success rate for these types of studies, it's targeting a massive market – the global breast cancer therapeutics market hit $34.63 billion in 2024 and is expected to reach $89.01 billion by 2034, growing at a healthy 9.90% annually.

That's the kind of growth potential that gets my attention.

The stock currently sports a 6.7% dividend yield, which might look tempting – like that last piece of chocolate cake in the refrigerator at midnight.

But here's the rub: pharmaceutical companies are like Silicon Valley startups with lab coats. They constantly need to innovate just to stay alive. It's not enough to have one hit wonder – you need a whole playlist of blockbusters.

Trading at 8.91x forward earnings with a PEG ratio of 0.20 and 2.5x price/sales, Pfizer does look cheap. But as I always say, sometimes things are cheap for a reason.

Want a shocking comparison? While attending the J.P. Morgan Healthcare Conference, I noticed that analysts are projecting Pfizer's 2029 revenues to be over $5 billion lower than 2024. That's not exactly the inspiring growth story I was hoping to hear.

For those of you hunting for yield (and I know many of you are), let me give you a reality check. That juicy 6.7% dividend looks appetizing until you realize it comes from a company that needs to spend billions just to replace what it's about to lose.

While I love a good yield as much as the next investor, watching a pharmaceutical company's patents march toward expiration is about as comforting as sitting in a dentist's waiting room.

Sometimes the best high-yield investment is the one you don't make – at least until the business fundamentals match the dividend's promise.

Want my advice? Keep an eye on their oncology developments, but keep your powder dry. There's a difference between buying a great company and buying a great stock at the right time.

Right now, Pfizer needs to prove it can fill an $18 billion revenue gap before I'm ready to write them a prescription for my portfolio.