Global Market Comments

May 6, 2020

Fiat Lux

Featured Trade:

(NOW THE FAT LEADY IS REALLY SINGING FOR THE BOND MARKET),

(TLT), (TBT)

Global Market Comments

May 6, 2020

Fiat Lux

Featured Trade:

(NOW THE FAT LEADY IS REALLY SINGING FOR THE BOND MARKET),

(TLT), (TBT)

The most significant market development so far in 2020 has not been the epic stock market crash and rebound, the nonstop rally in tech stocks (NASDQ), the rebound of gold (GLD), or negative oil prices, although that is quite a list.

It has been the recent peaking of the bond market (TLT), which a few weeks ago was probing all-time highs.

I love it when my short, medium, and long-term calls play out according to script. I absolutely hate it when they happen so fast that I and my readers are unable to get in at decent prices.

That is what has happened with my short call for the (TLT), which has been performing a near-perfect swan dive since April. The move has been enough to boost me back into positive numbers for 2020.

The yield on the ten-year Treasury bond has soared from 3.25% in 2018 to an intraday low of 0.31% in March.

Lucky borrowers who demanded rate locks in real estate financings at the end of January are now thanking their lucky stars. We may be saying goodbye to the 3% handle on 5/1 ARMS for the rest of our lives.

The technical damage has been near-fatal. The writing is on the wall. A 1.00% yield for the ten-year is now easily on the menu for 2020, if not 2.00% or 3.0%.

This is crucially important for financial markets, as interest rates are the well spring from which all other market trends arise.

Wiser thinkers are peeved that the promised bleeding of federal tax revenues is causing the annual budget deficit to balloon from a low of a $450 billion annual rate in 2016 to $1.2 trillion last year and over $5 trillion in 2020.

Add in the bond purchases from the Fed’s new promise of $8 trillion in quantitative easing and you get true government borrowing of $13 trillion for 2020. It will all end in tears for bond and US dollar holders.

And don’t forget the president, who recently threatened to default on US Treasury bonds, just as the Treasury was trying to float $3 trillion in new issues. It is a short seller’s dream come true.

As rates rise, so does the debt service costs of the world’s largest borrower, the US government. The burden will soar in a hockey stick-like manner, currently at 4% of the total budget.

What is of far greater concern is what the tax bill does to the National Debt, taking it from $24 trillion to $32 trillion over the next year, a staggering rise of 50%. Even Tojo and Hitler couldn’t get the US to buy that much. If we get the higher figure, then we are looking not at another recession, but at yet another 1930-style depression.

Better teach your kids to drive for UBER early, as they are the ones who are going to have to pay off this gargantuan debt. That is if (UBER) is still around.

So what the heck are you supposed to do now? Keep selling those bond rallies, even the little ones. It will be the closest thing to a rich uncle you will ever have, if you don’t already have one.

Make your year now because the longer you put it off, the harder it will be to get.

Global Market Comments

May 5, 2020

Fiat Lux

Featured Trade:

(FIVE STOCKS TO BUY AT THE BOTTOM),

(AAPL), (AMZN), (SQ), (ROKU), (MSFT)

With the Dow Average down 1,400 points in three trading days, you are being given a second bite of the apple before the yearend tech-led rally begins.

So, it is with great satisfaction that I am rewriting Arthur Henry’s Mad Hedge Technology Letter’s list of recommendations.

By the way, if you want to subscribe to Arthur’s groundbreaking, cutting-edge service, please click here.

It’s the best read on technology investing in the entire market.

You don’t want to catch a falling knife, but at the same time, diligently prepare yourself to buy the best discounts of the year.

The Coronavirus has triggered a tsunami wave of selling, tearing apart the tech sector with a vicious profit-taking few trading days.

Here are the names of five of the best stocks to slip into your portfolio in no particular order once the madness subsides.

Apple

Steve Job’s creation is weathering the gale-fore storm quite well. Apple has been on a tear reconfirming its smooth pivot to a software services-tilted tech company. The timing is perfect as China has enhanced its smartphone technology by leaps and bounds.

Even though China cannot produce the top-notch quality phones that Apple can, they have caught up to the point local Chinese are reasonably content with its functionality.

That hasn’t stopped Apple from vigorously growing revenue in greater China 20% YOY during a feverishly testy political climate that has its supply chain in Beijing’s crosshairs.

The pivot is picking up steam and Apple’s revenue will morph into a software company with software and services eventually contributing 25% to total revenue.

They aren’t just an iPhone company anymore. Apple has led the charge with stock buybacks and gobbled up a total of $150 billion in shares by the end of 2019. Get into this stock while you can as entry points are few and far between.

Amazon (AMZN)

This is the best company in America hands down and commands 5% of total American retail sales or 49% of American e-commerce sales. The pandemic has vastly accelerated the growth of their business.

It became the second company to eclipse a market capitalization of over $1 trillion. Its Amazon Web Services (AWS) cloud business pioneered the cloud industry and had an almost 10-year head start to craft it into its cash cow. Amazon has branched off into many other businesses since then oozing innovation and is a one-stop wrecking ball.

The newest direction is the smart home where they seek to place every single smart product around the Amazon Echo, the smart speaker sitting nicely inside your house. A smart doorbell was the first step along with recently investing in a pre-fab house start-up aimed at building smart homes.

Microsoft (MSFT)

The optics in 2018 look utterly different from when Bill Gates was roaming around the corridors in the Redmond, Washington headquarter and that is a good thing in 2018.

Current CEO Satya Nadella has turned this former legacy company into the 2nd largest cloud competitor to Amazon and then some.

Microsoft Azure is rapidly catching up to Amazon in the cloud space because of the Amazon effect working in reverse. Companies don’t want to store proprietary data to Amazon’s server farm when they could possibly destroy them down the road. Microsoft is mainly a software company and gained the trust of many big companies especially retailers.

Microsoft is also on the vanguard of the gaming industry taking advantage of the young generation’s fear of outside activity. Xbox-related revenue is up 36% YOY, and its gaming division is a $10.3 billion per year business.

Microsoft Azure grew 87% YOY last quarter. The previous quarter saw Azure rocket by 98%. Shares are cheaper than Amazon and almost as potent.

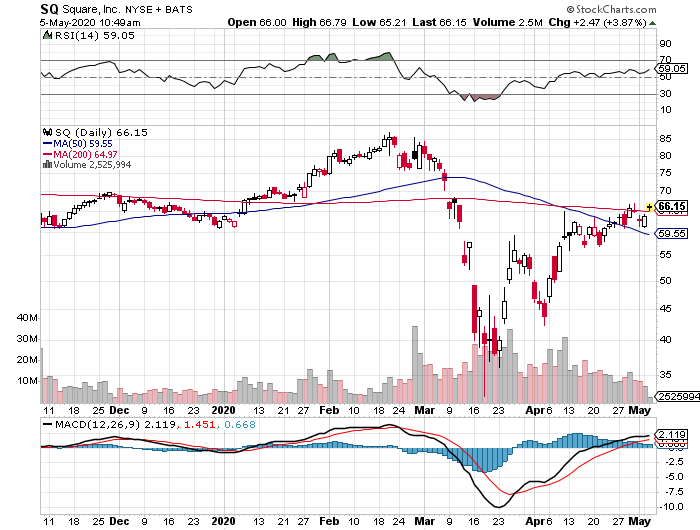

Square (SQ)

CEO Jack Dorsey is doing everything right at this fin-tech company blazing a trail right to the doorsteps of the traditional banks.

The various businesses they have on offer makes me think of Amazon’s portfolio because of the supreme diversity. The Cash App is a peer-to-peer money transfer program that cohabits with a bitcoin investing function on the same smartphone app.

Square has targeted the smaller businesses first and is a godsend for these entrepreneurs who lack immense capital to create a financial and payment infrastructure. Not only do they provide the physical payment systems for restaurant chains, they also offer payroll services and other small loans.

The pipeline of innovation is strong with upper management mentioning they are considering stock trading products and other bank-like products. Wall Street bigwigs must be shaking in their boots.

The recently departed CFO Sarah Friar triggered a 10% collapse in share price on top of the market meltdown. The weakness will certainly be temporary, especially if they keep doubling their revenue every two years like they have been doing.

Roku (ROKU)

Benefitting from the broad-based migration from cable tv to online steaming and cord-cutting, Roku is perfectly placed to delectably harvest the spoils.

This uber-growth company offers an over-the-top (OTT) streaming platform along with the necessary hardware and picks up revenue by selling digital ads.

Founder and CEO Anthony Woods owns 21 million shares of his brainchild and insistently notes that he has no interest in selling his company to a Netflix or Apple.

Roku’s active accounts mushroomed 46% to 22 million in the second quarter. Viewers are reaffirming the obsession with on-demand online streaming content with hours streamed on the platform increasing 58% to 5.5 billion.

The Roku platform can be bought for just $30 and is easy to set-up. Roku enjoys the lead in the over-the-top (OTT) streaming device industry controlling 37% of the market share leading Amazon’s Fire Stick at 28%.

The runway is long as (OTT) boxes nestle cozily in only 40% of American homes with broadband, up from a paltry 6% in 2010.

They are consistently absent from the backbiting and jawboning the FANGs consistently find themselves in partly because they do not create original content and they are not an off-shoot from a larger parent tech firm.

This growth stock experiences the same type of volatility as Square.

Be patient and wait for 5-7% drops to pick up some shares.

Global Market Comments

May 4, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE NEXT BOTTOM IS THE ONE YOU BUY),

(SPY), (SDS), (TLT), (TBT), (F), (GM), (TSLA), (S), (JCP), (M)

It was only a year ago that I was driving around New Zealand with my kids, admiring the bucolic mountainous scenery, with Herb Albert and the Tijuana brass blasting out over the radio. Believe me, the tunes are not the first choice of a 15-year-old.

Today, it is all a distant memory, with any kind of international travel now unthinkable. For me, that is like a jail sentence. It is all a reminder of how well we had it before and how bleak is the immediate future.

Stock traders have certainly been put through a meat grinder. The best and worst months in market history were packed back to back, down 39% and then up 37%. At the March 23 low, the Dow average had fallen by 11,400 in a mere six weeks. Those who lived through the 1929 crash have lost their bragging rights, if there are any left.

However, like my college professor used to say, “Statistics are like a bikini bathing suit. What they reveal is fascinating, but what they conceal is essential.”

Most of the index gains were achieved by just five FANG stocks. Virtually all of the gains were from “stay at home” companies taking in windfalls from cutting-edge online business models. The “recovery” had a good week, and that was about it.

The other obvious development is that if any business was in trouble before the health crisis, you can safely write them off now. That includes retailers like Sears (S), JC Penny’s (JCP), Macy’s (M), almost all brick-and-mortar clothing sellers, and the small and medium-sized energy industry.

The worst economic data points since the black plague are about to hit the tape. Some 30 million in newly unemployed is nothing to dismiss, and that number grows to 40 million if you include discouraged workers.

That is 25% of the workforce, the same as peak joblessness during the great depression. But $14 trillion in QE and fiscal stimulus is about to hit the market too.

Which brings us to the urgent question of the day: What to do now?

It’s a vexing issue because this is not your father’s stock market. This is not even the market we’d grown used to only six months ago. All I can say is that the virology course I took 50 years ago today is worth its weight in gold.

I think you would be mad not to count a second Covid-19 wave into your calculations. This could occur in weeks, or in months, after the summer respite. This makes a second run at the lows a sure thing. I don’t think we’ll make it, but a loss of half the recent gains is entirely possible.

That takes us back down to a Dow Average of 21,000, or an S&P 500 (SPX) of 2,400.

If you are a long term investor looking to rebuild your retirement nest egg, there are only two sectors left in the market, Tech and Biotech & Healthcare. Looking at anything else is both risky and speculative. So, if we do get another meltdown, these are the only areas you should target.

If I am wrong, the market will probably bounce along sideways in a narrow range for months. That is a dream scenario if you pursue a vertical bull and bear call and put option spread strategy that I have been offering up to followers for the past decade.

Pending Home Sales Were Down a Staggering 20.8% in March and off 16.3% YOY. The worst is yet to come. The West, the first into shelter-in-place, was down a monster 26.8%. Prices still aren’t moving because nobody can buy or sell. The way homebuilder stocks like (LEN) and (KBH) are trading, I’d say your home will be worth a lot more in a year when the huge demographic push resumes. I’m not selling.

The 60,000 peak in deaths proposed by the administration only weeks ago is now looking wildly optimistic. Their worst-case scenario of 200,000 deaths, the announcement of which set the March 23 bottom of the Dow Average at 18,200, is now likely.

It will take place when the epidemic peaks in the southern and midwestern states that never sheltered in place or went in late and are coming out early. That second wave may well create a second bottom in stock prices, and that is the one you jump into and buy with both hands.

US Corona Deaths topped 66,000 last week, more than we lost after a decade of the Vietnam War. Total cases exceed one million.

Bank of America sees negative 30% GDP this quarter annualized, so says CEO Brian Moynihan. His economists expect negative 9% in Q3 and plus 30% in Q4. Suffice it to say, this is the ultra-optimistic case. Q4 doesn’t include the millions of businesses that will disappear because the Paycheck Protection Plan is failing so badly. Most government aid will take three to six months to hit the economy.

US GDP crashed 4.8% in Q1, the worst quarter since the depths of the 2008 Great Recession. Q2 will be far worse. We are now officially in recession, which should last 3-4 quarters. But is it already in the price? Next week’s April Nonfarm Payroll report should be a real humdinger.

Ford (F) lost $5 billion in Q2, and there is no guidance about the future. Avoid (F) on pain of death. Late to electric, they may not make it this time. They’re still in the buggy whip business.

Weekly Jobless Claims topped 3.8 million, bringing the six-week total to a staggering 30 million, more than those lost at the peak of the Great Depression. Florida, California, and Georgia led with applications. This implies a U-6 Unemployment rate of 25% with next week’s April Nonfarm Payroll Report. And the Dow Average is up 37% since March 23?

The Bond Market crashed on a Trump threat to default on US Treasury bonds, of which China owns $900 billion. It’s Trump’s retaliation for the Middle Kingdom spawning the Coronavirus, which he calls the “Chinese virus.” The (TLT) dropped three points on the news. Good thing I am triple short a market that is about to get crushed by massive government borrowing.

A glut of imported autos is parked at sea, steaming in circles, awaiting a recovery in the US economy. They are no doubt finding company with imported oil tankers. So many unwanted cars coming in the land-based storage areas were overflowing. It’s tough to see (F) and (GM) recovering from this. Keep buying made in the USA (TSLA) on dips, which is headed to $2,500 a share.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had one of the best weeks in years, up a blistering +8.05%. We are now only 6.67% short of a new all-time high. The 100 new subscribers who came in the previous week are sitting pretty and must think I’m some sort of guru.

My aggressive triple weighting in short bond positions came in big time when Trump threatened to default on US debt. My shorts in the S&P 500 (SPY) helped. I took profits on my last long there the previous week. (SDS), another short play, clawed back some losses.

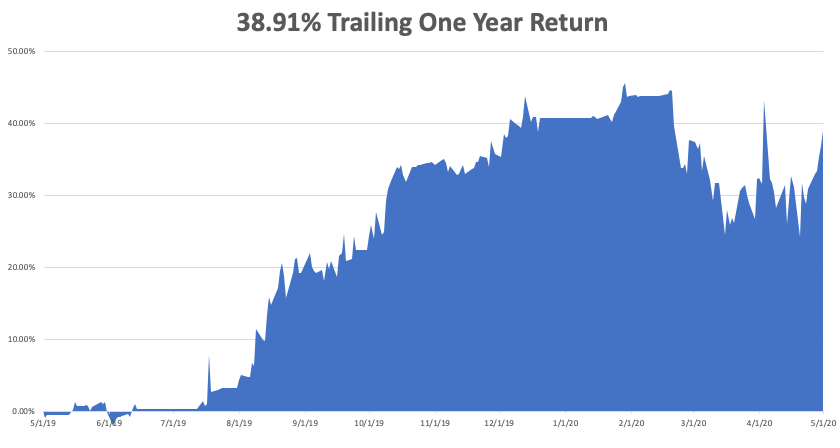

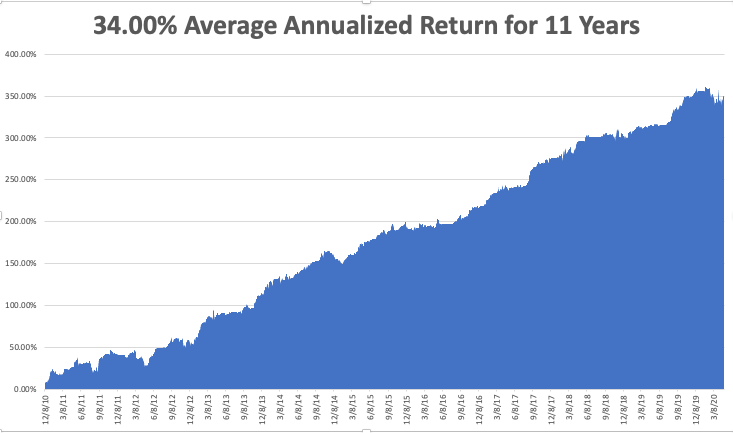

We closed out up a blockbuster +4.55% in April and May is up +2.11%, taking my 2020 YTD return up to only -1.75%. That compares to a loss for the Dow Average of -18.20% from the February top. My trailing one-year return returned to 38.91%. My ten-year average annualized profit returned to +34.00%.

This week, Q1 earnings reports continue and so far, they are coming in much worse than the most dire forecasts. We also get the monthly payroll data, which should be heart-stopping to say the list.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 4 at 9:00 AM, the US Factories Orders for March are out and are expected to be disastrous. Berkshire Hathaway (BRK/B) and Eli Lilly (LLY) report.

On Tuesday, May 5 at 11:00 AM, the US Crude Oil Stocks are published and will be another bomb. Netflix (NFLX) and Coca-Cola (KO) report.

On Wednesday, May 6, at 7:15 AM, API Private Sector Employment Report is released. Lan Research (LRCX) and Electronic Arts (EA) announce earnings.

On Thursday, May 7 at 8:30 AM, another horrible Weekly Jobless Claims are out. Bristol Myers Squibb (BMY) reports.

On Friday, May 8, the April Nonfarm Payroll Report is printed, the worst unemployment rate since the Great Depression. AbbVie (ABBV) reports.

As for me, to battle cabin fever, I am setting up a tent in my back yard and staying there tonight, just to change the scenery. The girls need one more campout to qualify for camping merit badge, an important Eagle Scout one, and this will qualify.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

May 1, 2020

Fiat Lux

Featured Trade:

(A NOTE ON ASSIGNED OPTIONS OR OPTIONS CALLED AWAY)

(TRADING THE NEXT KOREAN WAR)

With the May 15 options expiration only ten trading days away, there is a heightened probability that your short options position gets called away.

We have the good fortune of having a large number of deep in-the-money call and put options spreads about to expire at their maximum profit points, five to be precise.

If that happens, there is only one thing to do: fall down on your knees and thank your lucky stars. You have just made the maximum possible profit for your position with less risk. You just won the lottery, literally.

Most of you have short option positions, although you may not realize it. For when you buy an in-the-money put option spread, it contains two elements: a long put and a short put. The long put you own, but the short put can get assigned, or called away at any time and delivered to its rightful owner.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it.

All you have to do was call your broker and instruct him to exercise your long position in your May puts to close out your short position in the May puts.

Puts are a right to sell shares at a fixed price before a fixed date, and one option contract is exercisable into 100 shares.

Sounds like a good trade to me.

Weird stuff like this happens in the run-up to options expirations.

A put owner may need to sell a long stock position right at the close, and exercising his long Put is the only way to execute it.

Ordinary shares may not be available in the market, or maybe a limit order didn’t get done by the stock market close.

There are thousands of algorithms out there which may arrive at some twisted logic that the puts need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, puts even get exercised by accident. There are still a few humans left in this market to blow it.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it.

This generates tons of commissions for the broker but is a terrible thing for the trader to do from a risk point of view, such as generating a loss by the time everything is closed and netted out.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many ways to steal money legally that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.

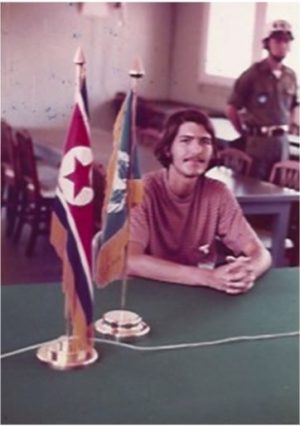

There are disturbing rumors circulating that North Korean dictator, Kim Jung-un, either has the Coronavirus or is dead.

With North Korea firing several short-range missions again and three years’ worth of high-level US negotiations having come to absolutely nothing, the prospect of another Korean War is back on the table.

The big question for these traders is how to trade it, or better yet, make money from it.

I was copiloting a Boeing Stratofortress B-52 bomber during the mid-1970s, and our mission was to bomb North Korea. In the back, we carried four thermonuclear weapons.

Since we had bolted steel blast shields to the inside of our cockpit windshield, we were flying entirely on instruments. It was a three-hour flight to our target from Anderson Air Force Base in Guam.

Ten minutes before we reached our destination, we received an order to abort, and we turned the great lumbering birds back to our Pacific island base. After we returned from our seven-hour ordeal, we headed straight for Guam’s spectacular Tarague Beach, which only those with base access could access.

It was 1975, and this was a training mission that took place every Monday to Thursday. On Friday, we carried a load of conventional bombs and dropped them on a gunnery range in Western Australia, to practice air-to-air refueling each way.

We knew the North Koreans were tracking us on radar every step of the way. The message was very clear: Be good, or we’ll fly the extra ten minutes.

Some 45 years, these training missions are still going on.

Except for one thing: next time, there may not be an order to abort. The bombers will fly the last ten minutes. The Second Korean War will be on.

Donald Trump desperately needs a foreign policy win to get us to stop talking about the Corona epidemic. Thousands of Americans are still dying every day. He has to project strength.

Kim Jong-un has to keep his country in a permanent state of war to remain in power, and they don’t retire former leaders to pleasant bucolic golf clubs. In other words, he, too, has to project strength.

Given this calculus, it’s hard not to see a Second Korean War starting sometime in the future.

A carrier battle group from the Seventh fleet is already on station in the Yellow Sea. In ten days, it may be joined by a Nimitz class supercarrier, the USS Carl Vinson battle group, out of San Diego.

The Implications of a Second Korean War for your investment portfolio is potentially vast. But over the long term, they may not be as bad as you think.

Look at the performance of the markets going into America’s last two major wars, and you’ll get some idea of what’s coming.

When Saddam Hussein first invaded Kuwait in July of 1990, the initial market reaction was to sell off sharply, with the S&P 500 (SPX) diving some 20% (see charts below).

President George H.W. Bush endlessly threatened the Iraqis to leave, or else, while relentlessly carrying out one of the largest military buildups in Middle Eastern history.

I know because I participated as a Marine Corps pilot.

But then, a funny thing happened. Gradually convinced that the war would take place, the market started to grind up.

When the “Shock and Awe” US attack took place the following February, stocks rocketed some 30%, and never went down.

However, it was a different time. The US was far more dependent on Middle Eastern oil in those days. And for the US economy, it was the eve of the Dotcom Boom.

The Second Gulf War was a similar story, as the market was still in the throes of the Dotcom Bust.

We got the ritual 10% selloff during the military buildup. When the war commenced, we saw one of the sharpest rallies in market history, some 20% in a month. Stocks continued to gain until the Great Recession kicked in six years later.

So the pattern seems to be clear. The saber rattle is worse than the war. Hang on to your stocks and you will do well. If you get nervous, just turn off the TV and go play golf.

Over the longer term, a lot will depend on how long the Second Korean War will last.

A quick, decisive victory will be hugely market positive. Get four carrier groups in place and North Korea’s defensive capability will be gone in a day.

First, cruise missiles will take out their radar, then anti-aircraft installations, then their aircraft and communications.

Good luck running a 1.8-million-man army with motorcycle messengers. North Korea lacks a national network of towers to support cell phones.

Here’s the thing that most people don’t realize about the North Korean Army. Not a single individual has combat experience. We, on the other hand, have lots.

Much of the North Korean weaponry is World War II surplus, given to them by the Russian, Chinese, and surrendering Japanese. The imposing missiles you see on TV on parade days are all dummies.

Yes, the North Koreans have 100 nuclear weapons. But they have no functional delivery system. Any attempt to move them will bring their immediate destruction. And we know where they all live.

The 500,000-man South Korean army can provide a blocking action at the demilitarized zone to prevent a land invasion, while we take apart the North’s defenses piecemeal.

There are also 28,500 US troops in South Korea to provide logistics and support for a sustained air war.

In a sense, this is a war for which we have been preparing for 70 years.

Here will be the price.

The North Koreans have 10,000 long-range artillery dug into mountains just north of the demilitarized zone within range of Seoul, a city with a population of 10 million.

I know because I’ve seen them.

I was one of the first western journalists to visit North Korea in 1974. Somewhere in the NBC archives, there is a reel of shaky 8 mm footage to confirm this.

It might take 1-2 weeks of B-52 raids using conventional weapons to degrade this threat. There’s no doubt the North Koreans will cause substantial damage in the meantime.

But it would be worth the cost.

A unified Korea would be a hugely stabilizing development for Asia. Good for the US, not so good for China.

It would also allow the use of the greatly save on its defense budget, now that money needs to be spent elsewhere. Every allocation of American military resources I have seen over the past 50 years had a Korean War contingency to it. Not needing it anymore is worth $50 billion a year.

This is the dream scenario.

The nightmare scenario has the war dragging out for years and Chinese and Russian involvement, as with the first Korean War. It could go on for 18 years, as with our current war in Afghanistan.

The backbreaking cost of the second Iraq War, some $3 trillion, was a contributing factor to the Great Recession when stocks fell 52%.

Winning the war will be the easy part. Peace will be much heavier lift, for it means we immediately inherit 25 million starving people in the North.

How our relations with China fare during all of this is anyone’s guess.

Long term, this is all very market and risk positive. How big the bumps will be along the way is anyone’s guess as well.