"I think this is about Russia reasserting itself on the international stage, basically saying that Russia is back and is a force to be reckoned with. I think we underestimated for a long time the extent of the humiliation that Russians felt after the collapse of the Soviet Union," said former Secretary of Defense and CIA head Robert M. Gates.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/Putin-quote-of-the-day-photo-e1523310805636.jpg188250MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-05-31 01:00:342019-05-30 15:09:11May 31, 2019 - Quote of the Day

“The car business is hell,” said founder Elon Musk when announcing he would sleep in the Fremont Tesla factory until Model S production reached 2,500 units a week.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/05/tesla.png331443Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-30 01:00:252019-05-29 19:38:00May 30, 2019 - Quote of the Day

(WEDNESDAY, JULY 10 BUDAPEST, HUNGARY STRATEGY LUNCHEON)

(ONSHORING TAKES ANOTHER GREAT LEAP FORWARD),

(TSLA), (UMX), (EWW), (KISS THAT UNION JOB GOODBYE),

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-29 01:08:362019-05-28 15:34:27May 29, 2019

Have you tried to hire a sewing machine operator lately?

I haven’t, but I have friends running major apparel companies who have (where do you think I get all those tight-fitting jeans?).

Guess what? There aren’t any to be had.

Since 1990, some 77% of the American textile workforce has been lost, when China joined the world economy in force, and the offshoring trend took flight.

Now that manufacturing is, at last, coming home, the race is on to find the workers to man it.

Welcome to onshoring 2.0.

The development has been prompted by several seemingly unrelated events.

There is an ongoing backlash to several disasters at garment makers in Bangladesh, the current low-cost producer which have killed thousands.

Today’s young consumers want to look cool but have a clean conscience as well. That doesn’t happen when your threads are sewn together by child slave laborers working for $1 a day.

Several firms are now tapping into the high-end market where the well-off are willingly paying top dollar for a well-made “Made in America” label.

Look no further than 7 For All Mankind, which is offering just such a product at a discount to all recent buyers of the Tesla Model S-1 (TSLA), that other great all-American manufacturer.

As a result, wages for cut-and-sew jobs are now among the fastest growing in the country, up 13.2% in real terms since 2007, versus a paltry 1.4% for the industry as a whole.

Apparel industry recruiters are plastering high schools and church communities with flyers in their desperate quest for new workers.

They advertise in languages with high proportions of blue-collar workers, such as Spanish, Somali, and Hmong.

New immigrants are particularly being targeted. And yes, they are resorting to the technology that originally hollowed out their industry, creating websites to suck in new applicants.

Chinese workers now earn $3 an hour versus $9 plus benefits at the lowest paying U.S. factories.

But the extra cost is more than made up for by savings in transportation and logistics, and the rapid time to market.

That is a crucial advantage in today’s fast-paced, high-turnover fashion world. Some companies are even returning to the hiring practices of the past, offering free training programs and paid internships.

By now, we have all become experts in offshoring, the practice whereby American companies relocate manufacturing jobs overseas to take advantage of low wages, missing unions, the lack of regulation, and the paucity of environmental controls.

The strategy has been by far the largest source of new profits enjoyed by big companies for the past two decades.

It has also been blamed for losses of U.S. jobs, with some estimates reaching as high as 25 million.

When offshoring first started 50 years ago, it was a total no-brainer.

Wages were sometimes 95% cheaper than those at home. The cost savings were so great that you could amortize your total capital costs in as little as two years.

So American electronics makers began filing overseas to Singapore, Thailand, Hong Kong, Taiwan, South Korea, and the Philippines.

After the U.S. normalized relations with China in 1978, the action moved there and found that labor was even cheaper.

Then, a funny thing happened. After 30 years of falling real American wages and soaring Chinese wages, offshoring isn’t such a great deal anymore. The average Chinese laborer earned $100 a year in 1977.

Today, it is $6,000, and $26,000 for trained technicians, with total compensation still rising 20% a year. At this rate, U.S. and Chinese wages will reach parity in about 10 years.

But wages won’t have to reach parity for onshoring to accelerate in a meaningful way. Investing in China is still not without risks.

Managing a global supply chain is no piece of cake on a good day. Asian countries still lack much of the infrastructure that we take for granted here.

Natural disasters such as earthquakes, fires, and tidal waves can have a hugely disruptive impact on a manufacturing system that is in effect a highly tuned, incredibly complex watch.

There are also far larger political risks keeping a chunk of our manufacturing base in the Middle Kingdom than most Americans realize. With the U.S. fleet and the Chinese military playing an endless game of chicken off the coast, we are one midair collision away from a major diplomatic incident.

Protectionism constantly threatens to boil over in the U.S., whether it is over the dumping of chicken feet, tires, or the latest, solar cells.

This is what the visit to the Foxconn factory by Apple’s CEO Tim Cook was all about. Be nice to the workers there, let them work only 8 hours a day instead of 16, let them unionize, and guess what?

Work will come back to the U.S. all the faster. The Chinese press was ripe with speculation that Apple-induced reforms might spread to the rest of the country like wildfire.

The late General Motors (GM) CEO Dan Adkerson once told me his company was reconsidering its global production strategy in the wake of the Thai floods.

Which car company was most impacted by the Japanese tsunami? General Motors, which obtained a large portion of its transmissions there.

The impact of a real onshoring move on the U.S. economy would be huge. Some economists estimate that as many as 10% to 30% of the jobs lost to offshoring could return.

At the high end, this could amount to 8 million jobs. That would cut our unemployment rate down by half, at least.

It would add $20 billion to $60 billion in GDP per year or up to 0.4% in economic growth per year.

It would also lead to a much stronger dollar, rising stocks, and lower bond prices. Is this what the stock market is trying to tell us by failing to have any meaningful correction for the past 2 ½ years?

Who would be the biggest beneficiaries of an onshoring trend? Si! Ole! Mexico (UMX) (EWW), which took the biggest hit when China started soaking up all the low-wage jobs in the world.

After that, the industrial Midwest has to figure pretty large, especially gutted Michigan. With real estate prices there under their 1992 lows, if there is a market at all, you know that doing business there costs a fraction of what it did 20 years ago.

So How Does This Thing Work?

https://www.madhedgefundtrader.com/wp-content/uploads/2018/06/worker.png214322MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-05-29 01:04:232019-07-09 03:41:36Onshoring Takes Another Great Leap Forward

Those of you counting on getting your old union assembly line job back in Detroit can forget it.

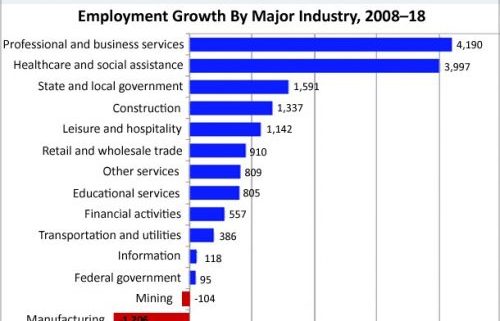

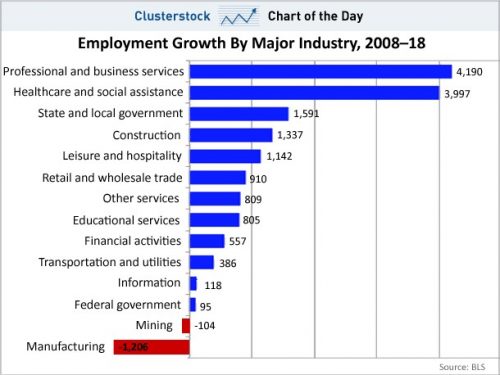

The eight-year forecast published by the Bureau of Labor Statistics shows that 4.19 million jobs will be gained in the U.S. in professional and business services, followed by 4 million health care and social assistance jobs, while 1.2 million will be lost in manufacturing.

This is great news for website designers, Internet entrepreneurs, registered nurses, and masseuses in California, but grim tidings for traditional metal bashers in the rust belt manufacturing states such as Michigan, Indiana, and Ohio.

I’m so old now that I am no longer asked for a driver’s license to get into a nightclub. Instead, they ask for carbon dating.

The real challenge for us aged career advisors is that probably half of these new service jobs haven’t even been invented yet, and if they can be described, it is only in a cheesy science fiction paperback with a half-dressed blond on the front cover.

After all, who heard of a webmaster, a cell phone contract sales person, or a blogger 40 years ago?

Where are all these jobs going to? You guessed it, China, which by my calculation has imported 25 million jobs from the U.S. over the past decade.

You can also blame other lower waged, upstream manufacturing countries such as Vietnam, where the Middle Kingdom is increasingly subcontracting its own offshoring.

These forecasts may be optimistic because they assume that Americans can continue to claw their way up the value chain in the global economy, and not get stuck along the way, as the Japanese did in the 90s.

The U.S. desperately needs no less than 27 million new jobs to soak up natural population and immigration growth and get us back to a traditional 5% unemployment rate.

The only way that is going to happen is for America to invent something new, big, and fast.

Personal computers achieved this during the 80s, and the Internet did the trick in the 90s. The fact that we’ve done squat since 2000 but create a giant paper chase of subprime loans and derivatives explains why job growth since then has been zero, real wage growth has been negative, and American standards of living are falling.

While the current crop of politicians extols the virtues of education, the reality is that we are dumbing down our public education system. How do we invent the next “new” thing, while shrinking the University of California’s budget by 25% two years in a row?

If my local high school can’t afford new computers, how is it going to feed Silicon Valley with a computer literate workforce? The U.S. has a “Michael Jackson” economy. It’s still living like a rock star but hasn’t had a hit in 20 years.

China can have all the $20 a day jobs it wants. But if it accelerates its move up the value chain as it clearly aspires to do, then America is in for even harder times.

I’ll be hoping for the best but preparing for the worst. How do you say “unemployment check” in Mandarin?

Is This Your Future?

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Employment-growth-chart-story-2-image-1-e1526422265887.jpg375500MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-05-29 01:02:142019-07-09 03:41:43Kiss That Union Job Goodbye

I was perusing hundreds of charts over the weekend as I usually do looking for great trading insights when what I saw stunned, frightened, and gobsmacked me. A “Head and Shoulders” top is setting up for the major stock market indexes.

Take a look at the charts below and you will see it is clear as day for the Dow Average, the S&P 500, and the NASDAQ. The Russell 2000 chart shows a “Head and Shoulders” top that has already broken down into bear market territory for the stocks most sensitive to a recession.

I am normally not a big fan of technical analysis. I see it as the refuge of young and inexperienced traders who are unable or incapable of engaging in deep, meticulous, and time consuming fundamental analysis.

However, when the charts confirm what I already know is happing in the real economy, the hair stands up on the back of my neck. And that is exactly what is happening now.

To say that the China trade war has thrown the fat on the fire would be a vast understatement. Every business in the country is now taking a hard look at their business models trying to understand if they can survive a prolonged trade war or go out of business.

It turns out that you cannot manufacture ANYTHING in America without using Chinese parts. You know all of those products that claim they are 100% made in America? Many, if not most, of the parts are Chinese. Only the labor to assemble them is from the US. This has been the dirty little secret of the US economy for a long time.

While the administration is claiming these companies can easily source elsewhere, most of the needed parts are not available at the price or the volume needed to fill the gap, and many of these parts are ONLY made in China. It took 40 years to integrate the Chinese and US economies as an alternative to an endless war and the relationship is not going to be unwound overnight on a whim with a Tweet.

I am not the only one who has noticed this. JP Morgan (JPM) has dramatically cut their growth forecast from 3.2% in Q1 to a lowly 1% in Q2. The Federal Reserve itself warned that trade could demolish the recovery. You break it, you own it. Isn’t it amazing how quickly panics happen? Risk happens fast.

The president has said that trade wars are “easy to win,” but it depends on how you decline “winning.” If “winning” means that we go bankrupt slower than the Chinese, he is probably right. But we all go bankrupt nonetheless.

The impact of the trade war won’t be evident in the economic data for months. The advanced estimate of Q2 GDP won’t be released by the Bureau of Economic Analysis until July 26 (click here).

By the time the administration figures out that this war is unwinnable, we may already be solidly in recession and deep into a bear market for stocks.

And let me ask you this question. How hard do you think the Chinese are going to work to get Donald Trump reelected? They don’t have a presidential election to worry about next year. Someone else does. Better clean up that extra bedroom. The trade war isn’t staying overnight on the sofa. It is moving in as a permanent resident.

So, for the foreseeable future, I strongly advise you to sell into every substantial rally, reduce risk, and pare back your trading. Anything you keep, you have to be able to withstand a 40% drawdown. That’s what all the lead tech stocks did in December.

This is turning into the best “Sell in May and go away”. It might be the summer to take that long-postponed trip around the world. Hmmmm. That’s I’m doing. Stocks dove last week on the trade war escalation, with technology taking the biggest hit. Fears of Chinese retaliation are rampant. All markets are now signaling recession, with bonds up huge and everything else down huge, like all stocks, oil, commodities, and real estate. The bigger they are the harder they fall. Ten-year US Treasury yields plunged to 2.30%. It might be a good summer to take a round the world cruise.

Mad Hedge Market Timing Index plummeted to 28, from a high of 72 just weeks ago. That means stocks have more downside to go, and a solid “BUY” won’t appear for months.

No China meetings will be held for at least a month, says US Treasury Secretary Steven Mnuchin. Don’t expect any respite from this front. It seems preventing Trump’s tax returns from being released is taking up all his time. Also, the US government runs out of money at summer’s end, unless the Democratic-controlled House opens up the checkbook first.

In the cruelest move, China blocked the broadcast of the final episode of Game of Thrones, forcing fanatics to search the Internet for the final conclusion. It looks like this is going to be a no holds barred war.

Tesla finally broke $200, as fears of Chinese tariff hikes hit its parts supply. Analysts cite other “distractions” like the SEC and the margin call on Elon Musk’s leveraged long position in $500 million worth of the shares. Wait for the final capitulation. The “BUY” for (TSLA) is setting up. Electric car subsidies are to return on 2021 and the shares will soar. Expect institutions to front run this move by a year.

Some 90% of the net buying in the market now is corporate buybacks, shrinking the float of available shares by 4% this year, and more than 10% for single stocks like Apple (AAPL), Microsoft (MSFT), Cisco Systems (CSCO), and Oracle (ORCL). Buy ALL of the buyback stocks on big dips.

New Homes Sales were down 6.9%, in April. As in past cycles, they are seeing the recession first, despite ultra-low interest rates. Prices here still rising, thanks to trade war-induced rocketing materials and lumber costs.

Existing Home Sales shed 0.4%, to only 5.19 million units in April, despite year low mortgage interest rates. The good news is that inventory shrank to 4.2 months. A lot of homes are now for sale at “aspirational” prices, with sellers hanging on to last year’s prices. I don’t understand why investors are buying the homebuilder stocks, unless its anticipation of the return of SALT deductions in two years.

The Mad Hedge Fund Trader managed to hang on to new all-time highs last week, despite the horrific trading conditions.

Global Trading Dispatch closed the week up 15.72% year-to-date and is up 0% so far in May. My trailing one-year rose to +20.71%.

The Mad Hedge Technology Letter did fine, making money on longs in Microsoft (MSFT) and Amazon (AMZN). Some 10 out of 13 Mad Hedge Technology Letter round trips have been profitable this year.

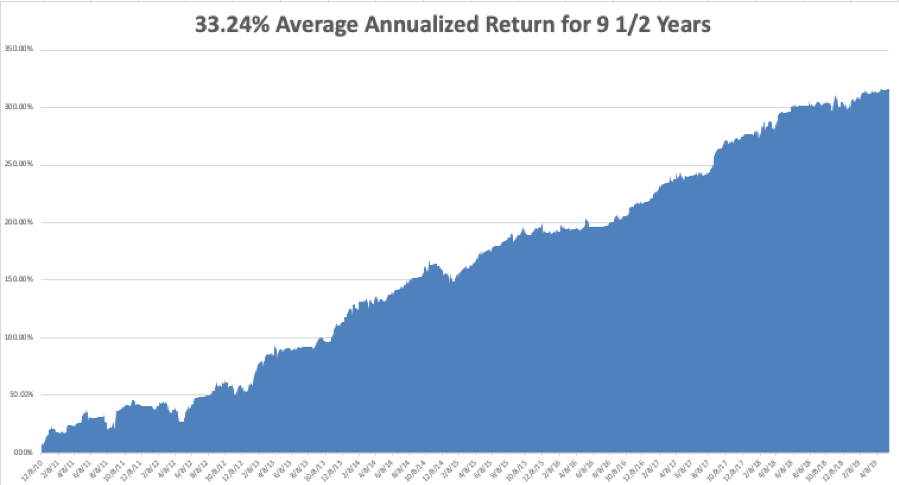

My nine and a half year profit jumped to +315.86%.The average annualized return popped to +33.24%. With the market's incredible and dangerously volatile, I am now 70% in cash with Global Trading Dispatch and 80% cash in the Mad Hedge Tech Letter.

I’ll wait until the markets enjoy a brief short-covering rally before adding any short positions to hedge my longs.

The coming week will see only one report of any real importance, the Fed Minutes on Wednesday afternoon. Q1 earnings are almost done.

On Monday, May 27 at 8:30 AM, the markets are closed for the Memorial Day holiday.

On Tuesday, May 28, 9:00 AM EST, the Case Shiller CoreLogic National Home Price Index is out.

On Wednesday, May 29 at 4:00 AM, MBA Mortgage Applications are out for the previous week.

On Thursday, May 30 at 8:30 AM, Weekly Jobless Claims are published. So is the first revision of the Q1 GDP. A second update on Q1 GDP is also published.

On Friday, May 31 at 8:30 AM, we learn the April Core Inflation.

As for me, I’ll be leading the local Memorial Day parade with my fellow veterans. I always consider myself lucky at these events because they are well attended by men with missing arms and legs and rising in wheelchairs. I am heartened by the young kids I see siting on curbs waving small American flags.

I firmly believe that the world will never see a large army war again. WWII needed 17 million men under arms, Vietnam 9 million, and the War in Iraq

2.8 million. You can see the trend. The next war will be fought by a few thousand programmers….and we will win.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-28 01:02:452019-07-09 03:41:50The Market Outlook for the Week Ahead, or Here Comes the Head and Shoulders Top

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-27 04:04:072019-05-27 16:16:18May 27, 2019

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.