Global Market Comments

February 18, 2016

Fiat Lux

Featured Trade:

(MY MOST DANGEROUS ADVENTURE EVER),

(BRING BACK THE UPTICK RULE!)

I was walking into the post office here in Incline Village, Nevada when I came across three little old ladies sitting at a card table.

One asked ?Have you registered yet for the February 20 Nevada caucus??? I answered that I was an independent, as I didn?t trust anyone. That meant I couldn?t vote in either Nevada primary.

We got to talking.

They thought it was fascinating that my dad was the head of the Republican Party in Southern California during the 1950?s, that I worked in the White House under president Ronald Reagan, and had met 9 out of the last 11 US presidents (missed Johnson, who died young, and George W. Bush, who never came to California).

They mentioned that the Republican Women?s Association was having a debate party this coming Saturday night.

Would I like to come?

Throughout my life, I have never turned down a mission, no matter how dangerous or suicidal.

This would be a particularly risky venture, as Nevada is not only a pro gun state, it is an active gun using state. Every other pickup truck has a gun rack in the back window holding a high-powered rifle or a shotgun.

And who knows what the ladies are packing in their purses?

I said I?d love to come.

I then called my office in Florida and cautioned them that if they didn?t hear from me by Tuesday morning they should call the Incline Village police department and have Tahoe Search and Rescue look for my bullet riddled body.

Given the age of the members, it was an early event, starting at 6:00 PM at a local bar. I sat down at a table with four couples, all over seventy, nursing amber ales.

While the Republican debate went on in the background on a big screen TV through the haze (indoor smoking is still legal in Nevada, as is everything else), I started to solicit their views.

I asked what was the big deal about Hillary Clinton.

?Benghazi!? They shouted in unison.

But doesn?t the Republican Women?s Association have an interest in women?s? rights?

?Email server!? they responded in kind.

Not even equal pay for equal work?

?Benghazi!? they repeated, with more passion.

But what about global warming? Every Republican candidate is a card carry denier on an issue most Americans are concerned about.

?Email server!?

So given a choice between Hillary and Donald Trump, the primary frontrunner, who would they vote for?

One woman said she would vote for Trump because she liked a ?strong? candidate. The others said they wouldn?t vote at all.

I asked a number of other questions.

Here were the answers:

?Benghazi!?

?Email server!?

?Benghazi!?

?Email server!?

I couldn?t help but point out that whoever the Republican candidate was, they would lose if they ran their campaign on ?Benghazi!? or ?Email server!? The average American doesn?t have the slightest interest in any of these issues.

At this point, my hosts were glumly staring into their ales. I decided that I had worn out my welcome and made for the door while I still could.

Republican predictions of election outcomes are wildly inaccurate, because they only talk to each other, or others who agree with them, always an invitation for disaster.

This is why it came as a complete shock when they lost the popular vote in six out of the last seven presidential elections, soon to be seven out of eight.

The real problem is that Republicans spend two years proving to the base how conservative they are to win the primary, and only two months to move to the middle and win the national election. Not all the money in the world can pull off that swing.

The one out of six elections the Republicans won was in 2004, for George W. Bush?s second term, which is always a lay up. He only won by a narrow 3 million votes.

The Citizen?s United Supreme Court decision, which allowed unlimited anonymous campaign donations, put a turbocharger on this trend. It made available unlimited funds to even the weakest candidates. It thus forced frontrunners to become more shrill and radical to get the necessary media attention.

That created this year?s Republican Primary circus, which has offended and appalled their entire country, it not the world.

Therefore, I believe that Citizen?s United will ultimately lead to the destruction of the Republican Party, unless a future more liberal Supreme Court repeals it.

Adjust your long-term portfolio accordingly.

Oh, and before I left the bar, I paused at the door, just in case anyone was following me.

You never know.

![Presidential Candidate]() Which One Will It Be?

Which One Will It Be?

?I?d rather vote for a dried dog turd than Donald Trump,? said Liz Mayer, a strategist for the Republican Party.

Global Market Comments

February 17, 2016

Fiat Lux

Featured Trade:

(WHY I?M BUYING THE EURO),

(FXE), (UUP), (DXJ), (RSX), GREK),

(THE CASE FOR EUROPE),

(FXE), (DXJ), (RSX), GREK),

(OPTIONS FOR THE BEGINNER)

CurrencyShares Euro ETF (FXE)

PowerShares DB US Dollar Bullish ETF (UUP)

WisdomTree Japan Hedged Equity ETF (DXJ)

Market Vectors Russia ETF (RSX)

Global X FTSE Greece 20 ETF (GREK)

?

I am used to my readers thinking that I have gone ?Mad?, am out of my tree, or have started smoking California?s number one cash crop (hint: it?s not almonds).

Such was the abuse that I received last week when I demanded they buy oil at $28 a barrel last week. After all, no other authority than Barron?s said it would imminently plunge to $20.

By the way, I kicked those call options out this morning with a three day, 23% profit. Buy the rumor, sell the news.

I got similar levels of thankless abuse this morning when I then told them to buy the Euro (FXE).

WHAT? COME AGAIN?

I think the Euro (FXE) has just entered a new uptrend against the US dollar (UUP).

We have spent over a year putting in a bottom for the beleaguered continental currency at $103, which right now, looks like it is holding like the Rock of Gibraltar.

If you can?t trade options here, just buy the (FXE) outright for a move to $116 in coming months.

We broke through the 200-day moving average to the upside two weeks ago, and are falling back to test that line. The old resistance at $108.49 is the new support.

ECB president, Mario Draghi, has once again threatened further stimulus in March to keep the continent?s meager growth rate growing. That gave us a $2.4-point pull back today from the recent top, and a nice entry point for this call spread.

However, past experience has proven that Mario is a better talker than a doer.

Not only that, what quantitative easing Mario Draghi has already implemented seems to be working. The latest Euro Zone GDP growth rate came in at 0.30%, not exactly robust, but better that the negative numbers we saw last year.

All we need now is for China, Europe?s biggest customer, to post some better economic numbers, and it will be off to the races for the Euro.

Now that the prospect of further interest rate rises by the Federal Reserve has been thrown out the window, the dollar has run out of appreciation fuel.

I have been to Greece many times over the past 45 years, and I?ll tell you that I just love the place. The beaches are perfect, the Ouzo wine enticing, and I?ll never say ?No? to a good moussaka.

However, I don?t let Greece dictate my investment strategy.

Greece, in fact, accounts for less than 2% of Europe?s GDP. It is not a storm in a teacup that is going on there, but a storm in a thimble. Greece is really just a full employment contract for financial journalists, who like to throw around big words like bankruptcy, default and contagion.

I have other things to worry about.

In fact, I am starting to come around to the belief that Europe is looking pretty good right here. Cisco (CSCO) CEO, John Chambers, announced that he was seeing the early signs of a turnaround.

Fiat CEO, Sergio Marchionne, the brilliant personal savior of Chrysler during the crash, thinks the beleaguered continent is about to recover from ?hell? to only ?purgatory.?

Only a devout Catholic could come up with such a characterization. But I love Sergio nevertheless because he generously helps me with my Italian pronunciation when we speak (aspirapolvere for vacuum cleaner, really?).

What are the two best performing stock markets since the big ?RISK ON? move started last Thursday? Greece (GREK) (+5%) and Russia (RSX) (+7.5%)!

And here is where I come in with my own 30,000 foot view.

The undisputed lesson of the past five years is that you always want to own stock markets that are about to receive an overdose of quantitative easing.

Since the US Federal Reserve launched their aggressive monetary policy, the S&P 500 (SPY) nearly tripled off the bottom.? Look how well US markets have performed since American QE ended 18 months ago.

Europe has only just barely started QE, and it could run for five more years. Corporations across the pond are about to be force-fed mountains of cash at negative interest rates, much like a goose being fattened for a fine dish of foie gras (only decriminalized in California last year).

Mind you, it could be another year before we get another dose of Euro QE, which is why I just bought the Euro (FXE) for a short-term trade.

A cheaper currency automatically reduces the prices of continental exports, making them more competitive in the international markets, and boosting their economies. Needless to say, this is all great new for stock markets.

Get Europe off the mat, and you can also add 10% to US share prices as well, as the global economy revives. The Euro drag dies and goes to heaven.

Buy the Wisdom Tree International Hedged Equity Fund ETF (HEDJ) down here on dips, which is long a basket of European stocks and short the Euro (FXE). This could be the big performer this year.

Praise the Lord and pass the foie gras!

It?s all a Matter of Perspective in Greece

Global Market Comments

February 16, 2016

Fiat Lux

Featured Trade:

(NO ZERO INTEREST RATES HERE!),

(TLT), (BAC), (C), (JPM), (MS), (GS),

(THE NEW COLD WAR),

(THE HISTORY OF TECHNOLOGY)

iShares 20+ Year Treasury Bond (TLT)

Bank of America Corporation (BAC)

Citigroup Inc. (C)

JPMorgan Chase & Co. (JPM)

Morgan Stanley (MS)

The Goldman Sachs Group, Inc. (GS)

Global Market Comments

February 12, 2016

Fiat Lux

Featured Trade:

(JANET LAYS AN EGG)

(SPY), (TLT), (FXY), (GOOGL), (AAPL), (TWTR), (FB),

(WHO THE GRAND NICARAGUA CANAL HAS WORRIED)

SPDR S&P 500 ETF (SPY)

iShares 20+ Year Treasury Bond (TLT)

CurrencyShares Japanese Yen ETF (FXY)

Alphabet Inc. (GOOGL)

Apple Inc. (AAPL)

Twitter, Inc. (TWTR)

Facebook, Inc. (FB)

Financial markets often behave like demanding, spoiled, and fickle children. If they don?t get what they want RIGHT NOW they throw a temper tantrum.

That is exactly what bourses are doing around the world.? The Dow Average rallied 500 points this week in the hope that my former Berkeley economics professor, Federal Reserve governor Janet Yellen, would suddenly turn into an ultra dove.

It was thought that she would totally cave on any interest rate increases for the rest of 2016 at her Wednesday Humphrey-Hawkins testimony in front of a hostile congress.

Instead, Janet laid an egg. Risk markets everywhere suffered cardiac arrest.? The 500-point rally quickly turned into a 700-point loss. Blink, and you lost your last chance to get out.

The Japanese yen rocketed as hedge funds rushed to cover their shorts, which they had been using to fund their rapidly fading ?RISK ON? positions. Panic dumping long positions mean those yen shorts are no longer needed.

What is particularly gob smacking is to see a ten year Treasury yield crater to only 1.50%. As I outlined in last week?s Global Strategy Webinar, the (TLT) is clearly headed for its old all time high of $135, which equates to a parsimonious 1.36% yield.

If you refinanced your home last month to cash in on lower interest rates, better plan on doing it again next month!

Both the Treasury market and global bank shares are now discounting another Great Recession that is absolutely nowhere on the horizon.

It all vindicated my aggressive hedging of my trading book, which I put into place at the beginning of January.? Gotta love those (SPY) April $182 puts! They?re better than Ambien in helping me sleep at night.

February is shaping up to be a very big month for the Mad Hedge Fund Trader?s model trading portfolio.

In the meantime, more data came out this morning confirming the recession that isn?t.

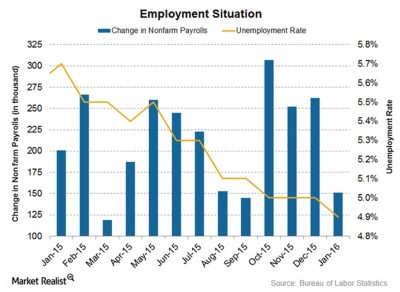

The Thursday weekly jobless claims plunged by 16,000 to 261,000, within spitting distance of a new 14 year low.

This is on the heels on last week?s respectable +175,000 January nonfarm payroll. This compares to a monthly LOSS of -700,000 jobs we saw in 2009.

Sure, the 0.7% US Q4 GDP is nothing to run up the flagpole and salute. But it is still growth. Most industries are reporting record profits.

I have to admit, I have never seen the economy so bifurcated.

In my daily customer calls I hear of Armageddon in the oil patch. But you can?t find office space in the San Francisco Bay area to save your life. And there are several whales looking for a staggering 10,000-20,000 square feet EACH!

These are all operations that started out in a garage only a decade ago. Add up the market capitalization of Google (GOOGL), Apple (AAPL), Facebook (FB), Twitter (TWTR), and Uber and we have created $1 trillion of equity out of thin air in only ten years.

Eventually, all good corrections come to an end. The hot money gets sold out, the margin clerks have taken their pound of flesh, the newbies get wiped out, and we run out of traders willing to chase the move down.

Then the cash rich long-term funds suddenly realize that we have a market that is selling at a 15X multiple in an economy that is about to speed up again. In addition, there is nothing else to buy.

Then it is off to the races to new all time highs by year end.

I am sticking to my New Year forecast of a 15% selloff that takes the S&P 500 down to $1770, which then rallies 20% by the end of December.

![Employment Situation]() Recession? What Recession?

Recession? What Recession?

![Janet]() Janet Lays an Egg

Janet Lays an Egg

Global Market Comments

February 11, 2016

Fiat Lux

Featured Trade:

(THE BATTERY IN YOUR FUTURE), or

(THE GREENING OF EXXON),

(USO), (SNE), (TSLA), (XOM),

(SCAM OF THE MONTH)

United States Oil (USO)

Sony Corporation (SNE)

Tesla Motors, Inc. (TSLA)

Exxon Mobil Corporation (XOM)