Global Market Comments

February 24, 2015

Fiat Lux

Featured Trade:

(DIPPING MY TOES BACK INTO GOLD),

(GLD), (SLV), (GDX), (ABX), (PALL)

(THE GAME CHANGER IN INDIA),

(INP), (PIN), (EPI), (EEM), (CEW), (ELD),

(USO), (KOL), (CU), (GLD)

SPDR Gold Shares (GLD)

iShares Silver Trust (SLV)

Market Vectors Gold Miners ETF (GDX)

Barrick Gold Corporation (ABX)

ETFS Physical Palladium (PALL)

iPath MSCI India Index ETN (INP)

PowerShares India (PIN)

WisdomTree India Earnings (EPI)

iShares MSCI Emerging Markets (EEM)

WisdomTree Emerging Currency Strategy (CEW)

WisdomTree Emerging Markets Local Debt (ELD)

United States Oil (USO)

Market Vectors Coal ETF (KOL)

First Trust ISE Global Copper Index (CU)

One of my best calls of 2014 was to plead with readers to avoid gold like the plague, periodically dipping in on the short side only.

Gold certainly delivered disappointment in spades, falling 4%, while the US stocks, bonds and the dollar were on fire. The barbarous relic has been in a bear market since it peaked at $1,922 an ounce at the end of August, 2011.

Gold shares have fared much worse, with lead stock Barrick Gold (ABX) dropping a gob smacking 81% since then, and the gold miners ETF (GDX) suffering a heart rending 74% haircut.

However, the recent price action suggests that hard times may be over for this hardest of all assets. Despite repeated attempts, the yellow metal has failed to break down below the $1,100 support level that I have been broadcasting as the line in the sand.

It rallied $230 off the bottom, and then recently gave up half that move. (GDX) has performed even better, popping 44%. For a sideways to eventually rising gold market, this is a great place to get involved with a short dated call spread.

The Chinese are far and away the world?s largest gold buyers. So when the Chinese Lunar New Year rolls around, the biggest participants disappear. That explains where the latest triple digit dump came from. This will end soon.

Few people realize how small the gold market is. All of the gold mined in human history, from King Solomon's mines, to the bars still in Swiss bank vaults bearing Nazi eagles (I've seen them) would only fill 2.5 Olympic sized swimming pools.

That amounts to 5.3 billion ounces, about $8.6 trillion at today's prices. For you trivia freaks out there, that is a cube with 66 feet on an edge.

China is the world?s largest producer of gold (13.1%), followed by Australia (10%) and the US (8.8%).

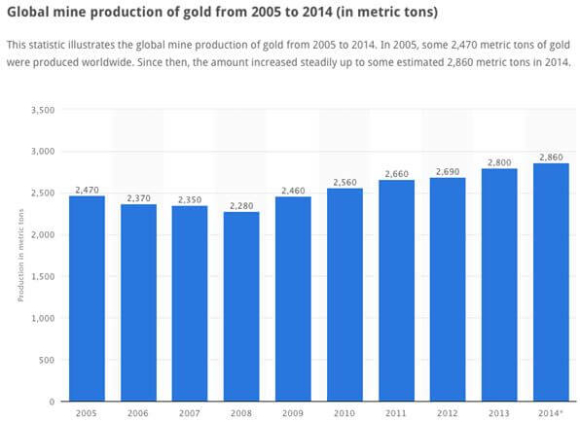

The problem for gold bears is they?re not making it anymore. Production has been only rising incrementally in recent years, reaching 2,860 metric tonnes, or 100.9 million ounces in 2014. This is worth $116 billion at today?s prices (see chart below).

That would rank gold 5th as a single Fortune 500 company, just ahead of General Electric (GE). It is also only .38% of global public debt markets worth $40 trillion.

That is not much when you have the entire world bidding for it, governments and individuals alike. Talk about getting a camel through the eye of a needle!

The old inflation adjusted high of $2,300, nearly $400 higher than the record absolute price of $1,928. No wonder buying is spilling out into the other precious metals, silver (SLV), platinum (PPLT), and palladium (PALL).

Like an ugly sister, it is hard to love gold in a disinflationary world. However, I think we are getting ripe for a technical rally that could take up $100 or more from here for the nimble. The recent high at $1,228 seems like a chip shot. That works fine for a deep in-the-money call spread position.

When playing in the gold space, I always prefer to buy the futures, or the (GLD), the world?s second largest ETF by market cap, either outright, or through a longer dated call spread. The dealing costs are far too high for trading physical bars and coins, and can run as high as 30% for a round trip.

Having spent 40 years following mining companies, I can tell you that there are just way too many things that can go wrong with them for me to risk capital. They can get nationalized, suffer from incompetent management, hedge out their gold risk, get hit with strikes or floods, or get tarred by poor equity market sentiment.

I do believe that a true bull market in gold will return some day, just not now. Inflation will make a comeback in the 2020?s. Newly enriched emerging markets will also want their central banks to raise gold holding to western levels, which implies a long term purchase of several thousand metric tonnes.

For all the statistics about gold you?d ever want to read, please visit the World Gold Council at their site at http://www.gold.org/supply-and-demand.

So far in 2015 the Indian stock market has handily beaten that of the US, by 10.6% compared to 5.3%.

?The India election result is the biggest development to affect emerging markets over the last 30 years.? That is what retired chairman of Goldman Sachs Asset Management and originator of the ?BRIC? term, Jim O?Neal, told me last week.

Indeed, the stunning news has sent long term country specialists scampering. In my long term strategy lectures I have been titillating listeners for years with predictions that India was about to become the next China.

With half the per capita income of the Middle Kingdom, India was lacking the infrastructure needed to compete in the global marketplace. All that was needed was the trigger.

This is the trigger.

With a new party taking control of the government for the first time in 50 years, the way is now clear to carry out desperately needed sweeping political and economic reforms. At the top of the list is a clean sweep of corruption, long endemic to the subcontinent. I once spent four months traveling around India on the Indian railway system, and the demand for ?bakshish? was ever present.

A reviving and reborn India has massive implications for the global economy, which could see growth accelerate as much at 0.50% a year for the next 30 years. This will be great news for stocks everywhere. It will help offset flagging demand for commodities from China, like coal (KOL), iron ore (BHP), and the base metals (CU).

Demand for oil (USO) grows, as energy starved India is one of the world?s largest importers.

A strengthening Rupee, higher standards of living, and relaxed import duties should give a much needed boost for gold (GLD). India has always been the world?s largest buyer.

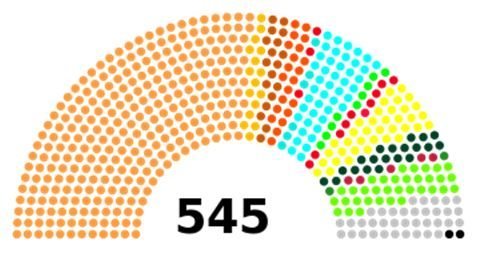

The world?s largest democracy certainly delivers the most unusual of elections, a blend of practices from today?.and a thousand years ago. It was carried out over five weeks, and a stunning 541 million voted, out of an eligible 815 million, a turnout of 66.4%. That is far higher than elections seen here in the United States.

Of the 552 members in the Lok Sabha, the lower house (or their House of Representatives), a specific number of seats are reserved for scheduled castes, scheduled tribes, and women. Gee, I wonder which one of these I would fit in?

Important issues during the campaign included rising prices, the economy, security, and infrastructure such as roads, electricity and water. About 14% of voters cited corruption as the main issue.

Some 12 political parties ran candidates. The winner was Hindu Nationalist Narendra Modi of the Bharatiya Janata Party (BJP), who led a diverse collection of lesser parties to take an overwhelming majority. For more details on this fascinating election, please click here at http://www.ndtv.com/elections.

It is still early days for the Bombay stock market, which has already rocketed by a stunning 20% since the election results became obvious last week.

This could be the beginning of a ten-bagger move over coming decades. Managers are hurriedly pawing through stacks of research on the subcontinent they have been ignoring for the past four years, the last time emerging markets peaked.

In the meantime, the action has spilled over into other emerging markets (EEM), their currencies (CEW), and their bonds (ELD), which have all punched through to new highs for the year.

I?ll be knocking out research o specific names when I find them. Until then, use any dip to pick up the Indian ETF?s (INP), (PIN), and (EPI).

?China is still the 800 pound gorilla. Maybe it?s no longer going to grow at 10%, but it?s still going to grow at a faster rate than Europe or the US,? said Edwin Rodriguez Jr., the biggest financial advisor in Louisiana, with $2.8 billion in assets.

Global Market Comments

February 23, 2015

Fiat Lux

Featured Trade:

(THE SPRING IN CISCO?S SYSTEM?S STEP), (CSCO),

(REPORT ON THE 6th ANNUAL SKYBRIDGE ALTERNATIVES CONFERENCE)

Cisco Systems, Inc. (CSCO)

I thought I noticed a spring in the step of Cisco Systems (CSCO) CEO John Chambers when he strutted out on TV to announce earnings last week.

Revenue came in just shy of $12 billion, a 7% improvement over fiscal 2014's Q2, and earnings per share really popped -- up 70% on a GAAP basis (including one-time items) to $2.4 billion from the prior year's "paltry" $1.4 billion.

Yikes!

Business in the US for the router and telecommunication company is going gangbusters. What is more important is the Chambers is seeing ?green shoots? is Europe, which has been a drag on the company?s earnings over the past several years.

This all presents important implications for the health of the global economy, which could be about to get dramatically better. Bring Europe, Japan, and China online, and we?re there.

It all fits in nicely with my own bullish forecasts for stocks in 2015. This has major implications for your own investment portfolio.

Cisco?s hardware is essential for connecting America?s 336 million cell phones. The Broadband spectrum needed for these devices to talk to each other is the new raw material of the 2000?s, replacing the oil, coal, and steel of an earlier century.

Cisco Systems (CSCO) believes that data delivered to mobile devices will skyrocket, from 4.2 billion gigabytes this year to a breathtaking 24.3 billion gigabytes by 2019 (or 24.2 Exabytes if you are interested). That is a fivefold increase in five years.

Blame all those kids watching full-length high definition motion pictures on their cell phones. My own tracking of share prices is no doubt making its contribution.

That means that at the current rate of capital investment, the US will completely run out of broadband capacity sometimes in 2018.

The answer? A lot more investment spending on all things broadband. This includes, the pipes, fiber optic cable everywhere, transmission towers, repeaters, and of course, lots of new routers.

This is all great news for Cisco.

Indeed, this is creating a gold rush for new spectrum as investors rush to buy the few free frequencies that are left.

In January, the Federal Communications Commission (FCC) auctioned off some government owned airwaves. It expected to receive $15 billion for the Licenses. What did it get? An eye popping $44.9 billion.

This is a game changer, and is enough to pay off 10% of this year?s total federal budget deficit. No doubt, they were popping the Champaign at the Treasury Department.

This has whetted appetites for a much larger auction due in 2016 or 2017, when the government sells off its last pieces of useable bandwidth. Like highly valued beachfront property, they?re not making it anymore.

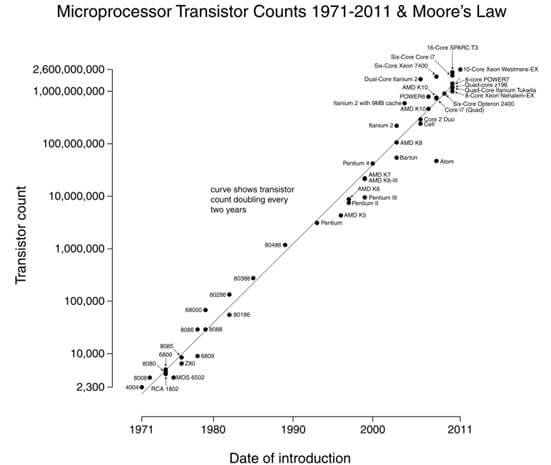

Having covered the computer industry for nearly 50 years, I find all this fascinating. Processing advances have been driven by Moore?s law since 1965. That?s when Intel?s Gordon Moore predicted that computing speed would double every 2 years, while costs halved for the indefinite future. He later amended his theory to 18 months. Here we are in 2015, and he has proved dead on correct.

Telecommunications has its own version. Motorola engineer, Marty Cooper, invented the mobile phone in 1973. He has calculated that ?spectral efficiency? has doubled every 2 ? years since Guglielmo Marconi made his first broadcast in 1910.

Since then, efficiencies have improved by a trillion-fold. Analysts now refer to this forecast as ?Cooper?s Law.?

The logic in picking strikes for the Cisco Systems (CSCO) March, 2015 $27-$29 in-the-money vertical bull call spread is that we can trade against the gap created by the blowout earnings announcement.

With the market having the bit between its teeth, I doubt we will retrace that gap anytime soon.

To visit Cisco?s home page, please click here at http://www.cisco.com/c/en/us/index.html.

![]()

![Marty Cooper]() Way to Go Marty

Way to Go Marty

Once again, I am writing to you from the poolside cabana B-2 at the Bellagio Hotel in Las Vegas. It is a baking hot 100 degrees in the shade and the air is bone-dry, so I?m draining my third rum punch for the day.

The days when I risked getting dragged out to the parking lot to get my hands broken with a hammer for card counting at blackjack have long since passed, so I am able to relax. As with PIMCO?s Bill Gross, that?s how I worked my way through college.

May Bugsy Siegel Rest in Peace.

It is shocking what passes for a tattoo these days, and where they end up. I see young women with elaborate Chinese and Japanese characters inscribed in some highly immodest positions.

Reading this unfathomable language myself, I can tell you that they look like they were brushed by a two year old or are completely unintelligible. I predict a raging bull market in regret in ten years?.if it hasn?t already started.

I have to tell you that the SkyBridge Alternatives Conference (SALT) is the best investment event I have ever attended, bar none. Never have I seen such a concentration of great minds so willing to share with the general trading community market-bending views on all assets classes, long and short.

Some of the best known speakers were humbled, and almost at a loss for words, addressing the impressive firepower assembled before them, 1,800 of the smartest people in the world.

Kevin Spacey started out with a hilarious series of impersonations. Former Prime Minister Tony Blair gave an eye opening assessment of the geopolitical scene. He seems to know more every year. Jim O?Neal, the just retired chairman of Goldman Sachs Asset Management, thought this week?s win by Narendra Modi?s BJP party in India was a game changer, the most significant emerging market event in 30 years.

Omega?s Leon Cooperman peppered us with his favorite stocks. The audience certainly perked up and took note. Last year?s tip gained 65%.

The cost for the four day assembly was a bargain at the price, given that you will probably make all of this back, and much more, on your next trade. This is an education that can make, or break, your year, and even a career. It spoke volumes that the stock market saw the lowest turnover of the year this week. All the players were here.

SALT was hosted by my friend, Anthony Scaramucci, the managing partner of SkyBridge Capital, LLC, a world class networker and high profile operator in the hedge fund industry.

Scaramucci is the author of two books, The Little Book of Hedge Funds: What You Need to Know About Hedge Funds but the Managers Won?t Tell You, and Goodbye Gordon Gekko: How to Find Your Fortune Without Losing Your Soul.

![John Thomas with Anthony Scaramucci]() Meeting the ?Mooch?

Meeting the ?Mooch?

SkyBridge Capital is a research driven alternative investment firm with over $10 billion in?total assets under advisement or management. The firm offers?hedge fund investing solutions?that address?a wide range of market participants from individual retail investors to large institutions.

Their businesses?include?commingled funds of hedge funds products, customized separate account?portfolios,?and hedge fund advisory services. To learn more about their services, please visit their coolest of all websites at http://www.skybridgecapital.com.

Anthony, or ?The Mooch? to his friends, seems to get better at this game every year. One minute, he is frenetically putting out fires, and the next, coolly introducing the next high profile name in a relaxed and suave manner. Every time I saw him, he was on the way to somewhere in a high speed hustle.

He is developing into a world-class entertainer in his own right. He surprised all by announcing this week his purchase and relaunch of the famed PBS TV show, Wall Street Week.

Unfortunately, there was a total press blackout for all of the marquee names with the sole exception of the best one (click here for ?An Evening with David Tepper?). So most of the high-grade intelligence was for ears only, With ?OFF THE RECORD? projected on the gigantic screens in big bold red letters.

You can?t blame these guys for being gun shy. All have been grievously misquoted by the press in the past. This can be a dicey problem when their comments are market moving and they already own big positions. With the former world leaders, there is always the chance of an offhand comment creating an international incident.

Given the choice between restrained, politically correct views approved by compliance departments or intelligence agencies, and the real, but unquotable skinny, I?ll definitely take the latter. You?ll learn the market impact of what was said in my coming Trade Alerts.

Non-stop panel discussions kept us all up to date on the many urgent issues facing hedge funds and their investors. Fee discounts for size, once unheard of, are now becoming common. As the industry is rapidly becoming commoditized, prices are dropping.

There is a rise in the customization of accounts for specific clients. Risk control and transparency have improved dramatically since the 2008 crash. Concerns about the popping of the bond market bubble were almost universal.

Peripheral to the large conference halls were two vast meeting rooms, one with 100 tables, another with 50 white upholstered sofas. There, an army of young, fresh faced marketing reps sold a panoply of hedge fund products to a flotilla of hardened and wizened end investors.

Reading the body language was fascinating. Dozens of small, start up hedge fund managers earnestly articulated their own strategies to potential partners. Every 20 minutes, the buyers of services rotated tables. You could almost feel the supercharged energy of the deals getting done and commerce coursing through the air.

God bless America!

![John Thomas with Jim Chanos]() No, Jim, You?re Wrong!

No, Jim, You?re Wrong!

There are now 23 hedge fund strategy categories, some with another half dozen subdivisions. You need a PhD in math from MIT to understand some of the more abstruse ones. Managers can now outsource any service to third party providers, be it compliance, tech support, investor relations, or support staff. The business has been sliced and diced so many ways it is dizzying.

The elevators hummed with the language of finance; duration, convexivity, alphas, betas, deltas, thetas, and price earnings ratios. Baff

led vacationers from the Midwest might have thought they took a wrong turn and landed in Greece by accident.

At night, the guests were treated to a blowout party around the Bellagio?s ornate swimming pool complex. A rock band boomed out the music, and the torsos of dancers gyrated wildly in true bacchanalian fashion.

A fire breather roamed about singeing the guests, as did elaborately dressed women on stilts wearing fantastic feathered costumes. Tarot card and palm readers were available if you wanted to learn your 2014 performance numbers in advance.

Comely waitresses served all the iced tequila shots you could drink, which had ?headache? written all over them. The hotel wisely stationed lifeguards around the pools in case a drunken reveler fell, or was thrown in. I asked one shapely attendant if she would save me if I inadvertently took a plunge, and she cautiously answered ?yes.?

It was all a scene worthy of The Great Gatsby.

Because I recently started posting my pictures on the site, I was mobbed by fans, dispensing some 200 business cards that evening. Why do I feel like the protagonist, Nick Carraway? Or am I the doomed Wall Street titan Jay Gatsby himself?

Of course, CNBC?s Fast Money crowd was there in force, and I was able to spend some quality time with Steve Weiss, Josh Brown with the permanently tousled hair, Jersey boy Guy Adami, and ?Harvard Girl? Melissa Lee. All were in fine spirits.

I managed to pin down short selling legend, Jim Chanos, telling him he is wrong about China for the umpteenth time. Still, he has already made a fortune there on the downside in recent years, and admitted he did carry some longs there against his shorts.

When I first jumped into the industry 30 years ago, there were only two dozen hedge funds managing a miniscule amount of money, and we all knew each other. Most of Wall Street thought we were all crooks. Now you have 10,000 funds managing $2.7 trillion, accounting for 50%-70% of all trading volume. Pension funds have made the industry respectable, and huge.

Asian readers still have the opportunity to sign up for the Singapore SALT Conference to be held on October 21-24, 2014 at the posh Marina Bay Sands Hotel (website: http://saltconference.com/saltasia2013/index.html ). After that, you will have to wait for the next Las Vegas conference in May, 2015.

The highlight of the event was a private concert by rock legend, Lenny Kravitz. A production company from Los Angles hauled out ten truckloads of sound equipment to make it happen with industrial strength. ?Watch out, it?s going to be LOUD,? warned the producer, as he handed me a pair of earplugs.

Minutes later, the rock legend took the stage and the base notes ruffled my shirt, reverberated through my chest, and vibrated my hair. I thought I was going to have a heart attack. His rendition of American Woman was outstanding. After the show, I immediately ran upstairs and downloaded Lenny?s latest album from iTunes.

I saw one of the richest men in the world casually walk up to the stage to get his ears blasted out, dressed in blue jeans, loafers, and a blue checked shirt with the tail hanging out. Girls walked up to shake his hand, and wouldn?t let go. Half the women were wearing six inch stilettos with red soles, meaning they ran a grand a pair.

I saw my buddies, Trademonster?s Najarian brothers, rocking out with their hair down, taking selfies. I have watched these two interact for years, and they make an amazing team. I wish I got along with my brother so well.

It was sad to see film legend, Francis Ford Coppola, now a fragile 75, struggle to get into his chair. I know he inhaled great draughts of the sixties, because I saw him there. To us rebels and iconoclasts of that tumultuous decade, Francis was our god.

I reminded him that I was an extra in his Vietnam War classic, Apocalypse Now, appearing in the USO scene when it was shot in the Philippines nearly 40 years ago.

He looked down at me somewhat disdainfully. ?You mean the one with the bunnies?? he asked. ?That?s the one,? I replied. ?That must have been interesting,? he answered.

What was I thinking? He clearly didn?t have the slightest idea who I was; so I let him tap his mismatched electric blue sock clad feet in peace. The result was the same as if the kid who mixed the hay with the mud approached the man who built the pyramids.

The next day, some of the younger kids from marketing were clearly wrecked and could have walked out of the morning after scene from The Hangover, which was shot at the Bellagio. I?m sure they spent the morning shuffling the stacks of business cards they collected, wondering who some of these people were. Ah, the price of youth!

And who the hell is John Thomas?

After drinking my meals for four days, I managed to cover all the bases. I even spent time with the hairy chest and silver chain crowd in the lukewarm pool, who leased office space to hedge funds. Business was booming.

Out of suntan lotion and Lenny still ringing in my ears, I ran for a taxi and off to my next speaking engagement at 8:00 AM the next morning in Orlando, Florida.

Oh, did I tell you how hard it is to get your clothes off when they are soaking wet?

My dry cleaner is going to hate me.

My Never Ending Search for New Trading Ideas

My Never Ending Search for New Trading Ideas

?Vision without execution is just hallucination.? said Thomas Edison.

Global Market Comments

February 20, 2015

Fiat Lux

Featured Trade:

(A NOTE ON THE FRIDAY OPTIONS EXPIRATION),

(FXY), (GILD), (SPY), (VIX),

(TLT), (IWM), (QQQ), (SCTY), (USO), (GLD),

?(AN EVENING WITH TEXAS GOVERNOR RICK PERRY),

?(LNG), (UNG), (TSLA)

CurrencyShares Japanese Yen ETF (FXY)

Gilead Sciences Inc. (GILD)

SPDR S&P 500 ETF (SPY)

VOLATILITY S&P 500 (^VIX)

iShares 20+ Year Treasury Bond (TLT)

iShares Russell 2000 (IWM)

PowerShares QQQ Trust, Series 1 (QQQ)

SolarCity Corporation (SCTY)

United States Oil ETF (USO)

SPDR Gold Shares (GLD)

We have several options positions that expire on Friday, and I just want to explain to the newbies how to best maximize their profits.

These include:

The Currency Shares Japanese Yen Trust (FXY) February $84-$87 vertical bear put spread

The Gilead Sciences (GILD) February $87.50-$92.50 vertical bull call spread

The S&P 500 (SPY) February $199-$202 vertical bull call spread

My bets that (GILD) and the (SPY) would rise, and that the (FXY) would fall during January and February proved dead on accurate. We got a further kicker with the two stock positions in that we captured a dramatic plunge in volatility (VIX).

Provided that some 9/11 type event doesn?t occur today, all three positions should expire at their maximum profit point. In that case, your profits on these positions will amount to 13% for the (FXY), 19% for (GILD) and 20% for the (SPY).

This will bring us a fabulous 5.58% profit so far for February, and a market beating 6.11% for year-to-date 2015.

Many of you have already emailed me asking what to do with these winning positions. The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck and pat yourself on the back for a job well done. You don?t have to do anything.

Your broker (are they still called that?) will automatically use your long put position to cover the short put position, cancelling out the total holding. Ditto for the call spreads. The profit will be credited to your account on Monday morning, and he margin freed up.

If you don?t see the cash show up in you account on Monday, get on the blower immediately. Although the expiration process is now supposed to be fully automated, occasionally mistakes do occur. Better to sort out any confusion before losses ensue.

I don?t usually run positions into expiration like this, preferring to take profits two weeks ahead of time, as the risk reward is no longer that favorable.

But we have a ton of cash right now, and I don?t see any other great entry points for the moment. Better to keep the cash working and duck the double commissions. This time being a pig paid off handsomely.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. Keep in mind that the liquidity in the options market disappears, and the spreads substantially widen, when a security has only hours, or minutes until expiration. This is known in the trade as the ?expiration risk.?

One way or the other, I?m sure you?ll do OK, as long as I am looking over your shoulder, as I will be.

This expiration will leave me with a very rare 100% cash position. I am going to hang back and wait for good entry points before jumping back in. It?s all about getting that ?buy low, sell high? thing going again.

There are already interesting trades setting up in bonds (TLT), the (SPY), the Russell 2000 (IWM), NASDAQ (QQQ), solar stocks (SCTY), oil (USO), and gold (GLD).

The currencies seem to have gone dead for the time being, so I?ll stay away.

Well done, and on to the next trade.